Landlord Insurance Connecticut Quotes: Smart Shopping for Property Owners

Landlord insurance in Connecticut works differently than standard homeowners policies, and getting the right coverage at the right price requires knowing what to look for.

We at Evaristo Insurance help Connecticut property owners navigate landlord insurance quotes and find policies that actually protect their investments. This guide walks you through the coverage types you need, how to compare quotes effectively, and what factors impact your rates.

Understanding Landlord Insurance Coverage in Connecticut

Why Landlord Policies Aren’t Homeowners Policies

The moment you rent out a property, your standard homeowners insurance becomes worthless for protecting your investment. Many Connecticut landlords make a serious mistake by keeping their personal homeowners policy active on a rental property, thinking it covers tenant-related risks. It does not. A homeowners policy explicitly excludes rental income, tenant injuries, and liability claims involving tenants. If a guest slips on your tenant’s spilled coffee and sues, your homeowners policy will deny the claim.

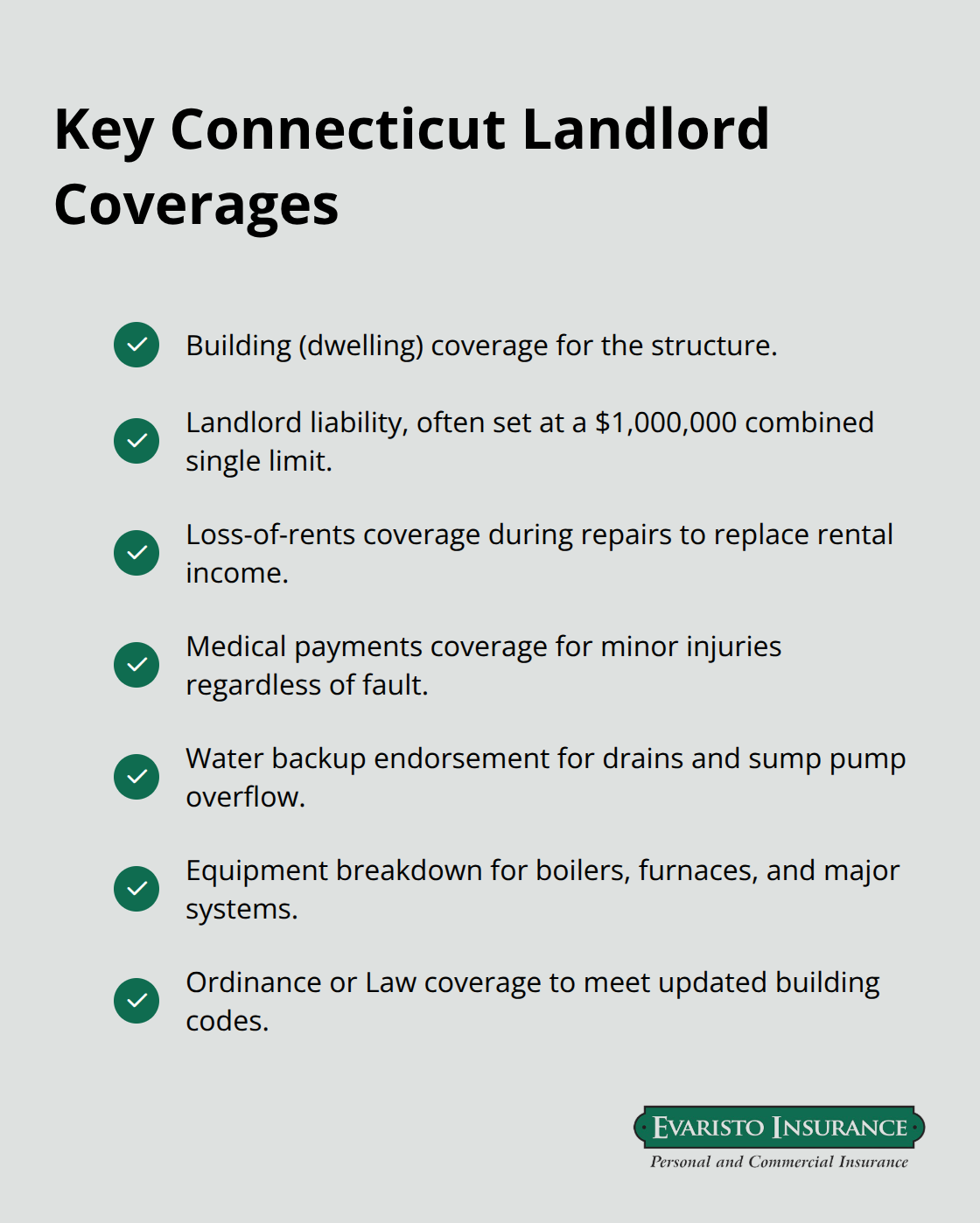

Landlord insurance in Connecticut addresses this gap by covering the building structure, landlord-owned items like appliances and furnishings, liability exposure from tenant or guest injuries, and lost rental income when a unit becomes uninhabitable after a covered loss. Connecticut landlords typically need property damage coverage for the building itself, landlord liability insurance with $1,000,000 combined single limit per occurrence, loss-of-rents protection to replace income during repairs, and medical payments coverage for minor injuries regardless of fault.

Core Protections Every Connecticut Landlord Needs

Beyond these core protections, many Connecticut properties benefit from additional endorsements. Water backup coverage protects against backed-up drains and sump pump overflow, which happens regularly in Connecticut basements during heavy spring rains. Equipment breakdown coverage pays for repairs to major systems like furnaces and water heaters. Ordinance or Law coverage helps cover the cost of bringing a damaged property up to current building codes after a loss-a real expense in older Connecticut properties where code requirements have tightened significantly.

For properties near rivers, the coast, or in designated flood zones, separate flood insurance through the National Flood Insurance Program is essential and typically not included in standard landlord policies. Requiring tenants to carry renters insurance protects both parties and reduces disputes over damaged personal belongings.

How Property Location Shapes Your Coverage Needs

Connecticut’s coastal regions and riverfront areas face elevated risk from storm surge and flooding, which directly affects your insurance costs and required coverages. Waterford and other coastal towns experience freeze-thaw cycles that crack pipes and foundations, making equipment breakdown and water damage endorsements more valuable. Urban areas like Hartford and New Haven have higher liability claims on average, pushing base liability limits higher.

An independent agent familiar with regional risks knows which endorsements actually save money long-term (by preventing claims rather than just covering them after the fact). An agent reviewing your specific property can identify that a Waterford rental near water needs stronger water-related protections, while an inland property in Ellington might prioritize wind and hail coverage instead. Understanding these location-specific risks helps you avoid overpaying for unnecessary coverage while ensuring you don’t leave gaps in protection where you actually need it most.

Getting Accurate Quotes Without Wasting Time

Gather the Right Property Information First

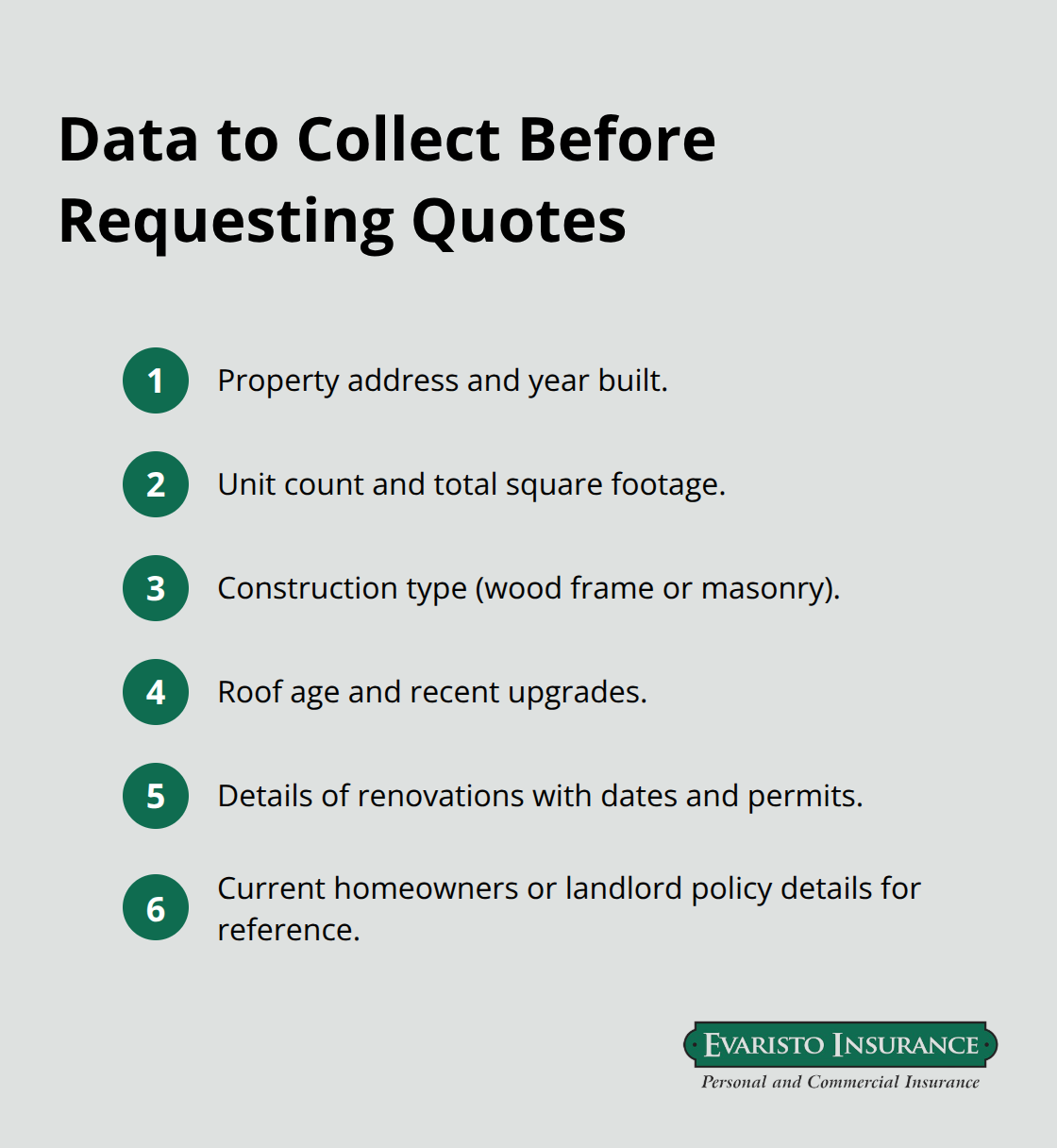

Connecticut carriers need consistent, detailed information to provide accurate quotes you can actually compare. Collect your property address, year built, number of units, square footage, construction type (wood frame versus masonry), roof age, and any recent renovations or upgrades before you contact agents. Carriers price based on these specifics, and incomplete information forces them to make assumptions that inflate quotes or create coverage gaps later.

Your loss history matters significantly. Connecticut carriers weight claims heavily, so properties with clean records typically see better rates than those with claims in the past three years. Gather details on any water damage claims, liability claims, prior fires, or theft. Have your current homeowners or landlord policy available to reference coverage limits and deductibles you’ve selected previously.

Specify Your Rental Use and Tenant Details

The way you use your property determines pricing and coverage options. Tell agents whether the property houses a single tenant, multiple units, or operates as a short-term rental, since each use case triggers different underwriting and pricing. Most carriers also ask about tenant screening practices, lease terms, and whether tenants carry renters insurance. Properties where landlords enforce tenant insurance requirements often qualify for modest discounts because risk transfers partially to the tenant’s carrier.

Compare Beyond the Premium Price

Two carriers might quote you $1,200 and $1,400 annually, but the cheaper option could have a $2,500 deductible while the other has $1,000, or one includes equipment breakdown while the other doesn’t. Request itemized quotes that break out property damage, liability, loss-of-rents, and any endorsements separately so you see what drives the price difference.

Red flags appear when a carrier refuses to quote equipment breakdown or water backup coverage for older Connecticut properties, since these endorsements are standard in the market and their absence signals they’re avoiding risk rather than properly pricing it. Avoid agents who pressure you to decide immediately or who won’t explain deductible and limit options clearly. Legitimate Connecticut agencies walk you through trade-offs between premium, deductible, and coverage limits so you understand what you’re paying for.

Watch for Underpriced Quotes and Poor Service

If a quote comes in significantly lower than others without clear explanation, ask why before accepting it. Underpriced policies often mean inadequate coverage or aggressive claims denial practices. Independent agents comparing multiple carriers catch these problems because they see how different companies handle similar risks, whereas captive agents representing one carrier can’t offer that perspective.

The difference between a $1,200 quote and a $900 quote isn’t always a better deal-it might be a policy that denies your claim when you need it most. Once you’ve identified quotes with comparable coverage, the next step involves understanding which factors actually drive your specific rate and how you can influence them through your choices and property management practices.

Factors That Affect Landlord Insurance Rates in Connecticut

Connecticut carriers price landlord policies on three concrete factors that you can measure and sometimes control. Property location determines your baseline risk exposure, rental property type and unit count directly affect underwriting complexity, and your tenant screening practices plus loss history shape your final premium. Understanding how each factor influences your rate helps you make smarter decisions about where to invest and how to structure your properties for better insurance costs.

Location Matters More Than You Think

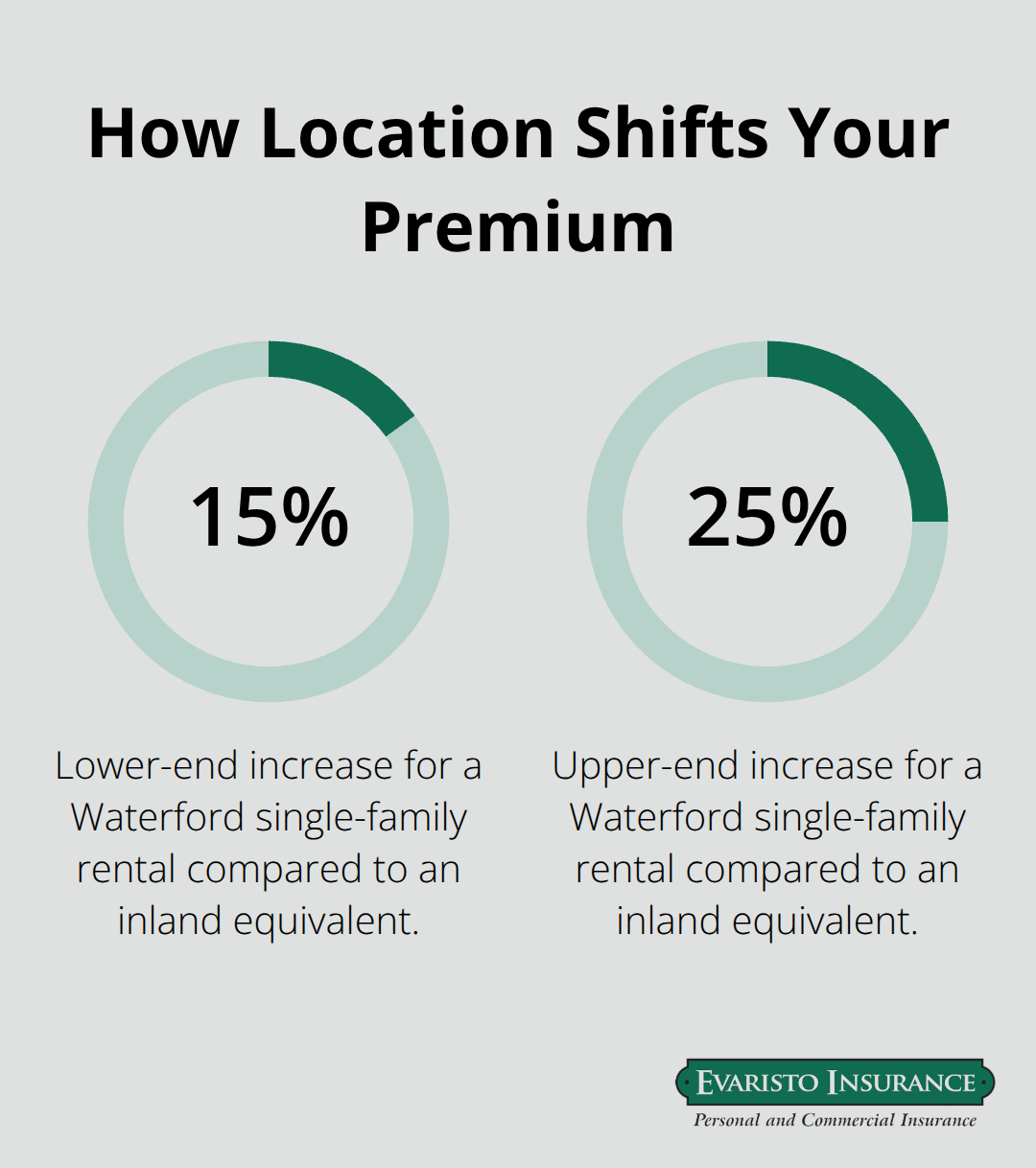

Coastal Connecticut properties in towns like Waterford, Old Saybrook, and Guilford pay significantly higher premiums than inland equivalents because storm surge, flooding, and salt-water corrosion create genuine exposure. A single-family rental in Waterford might cost 15 to 25 percent more annually than an identical property in Vernon or Ellington, even with identical construction and condition. Carriers also weight freeze-thaw cycle damage heavily in coastal areas, since pipes rupture regularly when winter temperatures fluctuate between freezing and mild.

Urban properties in Hartford and New Haven face elevated liability claims compared to suburban rentals, pushing base liability premiums higher across the market. Older properties in downtown areas with higher pedestrian traffic and density trigger additional underwriting scrutiny. River-adjacent properties anywhere in Connecticut qualify for flood insurance requirements through the National Flood Insurance Program, which adds a separate policy cost on top of your base landlord insurance.

Properties within one mile of water see higher equipment breakdown and water damage claims, making those endorsements more expensive and sometimes mandatory depending on the carrier. When you evaluate rental investments in Connecticut, factor insurance location premiums into your acquisition analysis from the start, because a property that seems cheaper upfront might cost considerably more to insure long-term.

Property Type and Unit Count Shape Your Quote Significantly

Single-family rentals receive the most favorable rates because they present straightforward underwriting and lower liability exposure per unit. Two-family and three-family properties cost more to insure because they involve shared spaces, mixed occupancy patterns, and multiple tenant relationships that increase claim frequency. Properties with five or more units typically transition to apartment complex insurance rather than standard landlord policies, which involves different carriers and pricing structures entirely.

Newer construction built after 2000 qualifies for better rates than pre-1950 properties because modern building codes mean fewer water damage claims, fewer electrical fires, and better structural integrity. A 1920s Connecticut farmhouse converted to a rental costs substantially more to insure than a 2005 ranch, all else equal. Furnished rentals cost more than unfurnished because landlord-owned contents coverage adds exposure, and short-term rental use triggers the highest premiums of all since guest turnover creates higher damage and liability frequency.

If you operate short-term rentals, confirm explicitly that your carrier covers that use, because many standard landlord policies exclude it entirely. Roof condition directly affects your rate because a 20-year-old asphalt shingle roof represents genuine risk, while a five-year-old metal or architectural shingle roof costs less. Many Connecticut carriers now offer small discounts for recent roof replacements with documentation.

Tenant Screening and Claims History Control Your Bottom Line

Connecticut carriers scrutinize your loss history heavily because claims predict future claims better than almost any other factor. A property with zero claims in the past five years might receive a 10 to 15 percent premium discount compared to an otherwise identical property with one water damage claim two years ago. Properties with two or more claims in five years face substantial rate increases or outright declination from some carriers.

Requiring tenants to carry renters insurance and naming you as an interested party signals to carriers that you enforce professional tenant relationships and reduces your exposure to tenant-caused damage claims. Properties where landlords document this requirement in leases and collect proof of coverage typically see modest rate reductions. Tenant screening matters because properties with high eviction rates or chronic payment issues indicate higher risk to carriers, even though eviction history doesn’t directly appear on insurance applications.

Carriers infer this from claims patterns, so maintaining stable long-term tenants actively improves your insurance costs. Taking photographs of your property before tenant move-in and documenting the condition creates clear evidence if disputes arise, which reduces claims frequency and severity. Carriers recognize this practice as genuine risk management and sometimes offer discounts for landlords who maintain detailed property documentation.

Final Thoughts

Shopping for landlord insurance Connecticut quotes requires you to evaluate coverage details alongside premium price and understand how location, property type, and your management practices shape your rates. The cheapest option often leaves gaps that cost far more when claims happen, while the most expensive quote isn’t always the best protection. Connecticut landlords who gather accurate property information, request itemized quotes from multiple carriers, and compare coverage specifics make smarter decisions that protect both their buildings and their cash flow.

A local Connecticut agency identifies risks you might miss on your own because regional expertise recognizes which endorsements actually save money long-term. Independent agencies compare multiple top carriers simultaneously, which means you see real options instead of accepting whatever one company offers. They also handle the administrative work of gathering quotes, explaining deductible trade-offs, and coordinating coverage across multiple properties if you own a portfolio.

Evaristo Insurance serves Connecticut property owners with tailored landlord coverage at competitive rates. Our local offices in Ellington and West Hartford mean you work with agents who understand Connecticut’s specific risks and insurance market. Contact us to review your current coverage, get quotes on new properties, or ensure your existing policies still match your actual exposure as your portfolio grows.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.