West Hartford Landlord Insurance: Local Expertise for Landlords

Owning rental property in West Hartford comes with unique challenges that standard homeowners insurance simply doesn’t address. Connecticut’s landlord-tenant laws, local weather patterns, and market conditions all shape what coverage you actually need.

We at Evaristo Insurance work with West Hartford landlords every day, and we’ve seen firsthand how the right insurance strategy protects your investment. This guide walks you through the coverage types that matter most and why local expertise makes all the difference.

What Connecticut Landlord Laws Actually Mean for Your Coverage

Connecticut’s landlord-tenant regulations shape your insurance needs in ways most landlords overlook. The state requires landlords to provide heat and hot water in residential units under Connecticut General Statutes Section 19a-109, which means you’re liable for maintaining essential systems-and your insurance must cover the financial fallout when those systems fail. A burst pipe in January isn’t just an inconvenience; it’s a habitability violation that can trigger enforcement actions and tenant claims. Standard homeowners insurance treats rental properties as a secondary concern and often excludes or limits coverage on structures you don’t occupy. Landlord insurance, by contrast, is built specifically for this exposure. Connecticut also enforces strict security deposit handling under state law, and while this doesn’t directly affect insurance, it reflects the regulatory environment that makes proper coverage non-negotiable. West Hartford landlords operating in this framework need policies that recognize these legal obligations, not policies designed for owner-occupied homes.

Why Standard Homeowners Insurance Fails Rental Properties

Homeowners policies exclude income loss from rental operations entirely. If a fire damages your West Hartford rental and the property sits vacant for three months during repairs, a homeowners policy won’t reimburse the rent you didn’t collect. Landlord insurance includes loss of rents coverage that compensates you for that income gap, typically covering fair rental value while the property is uninhabitable. Liability coverage also differs significantly. A homeowners policy covers injuries on your owner-occupied property; a landlord policy covers injuries to tenants and their guests on a rental property you don’t live in. If a guest slips on ice in your rental’s entryway and sues for medical costs and pain and suffering, your homeowners policy will likely deny the claim because it wasn’t your primary residence. Connecticut landlord insurance typically costs more than homeowners coverage, but that premium difference is actually the cost of having the right protections in place. Skipping landlord insurance forces you to pay repairs, liability judgments, and lost rent entirely from your own pocket-a scenario that routinely costs landlords tens of thousands of dollars.

Water Damage Coverage Requires Explicit Confirmation

Water damage from burst pipes is covered under many landlord policies, but not all-you need explicit confirmation that plumbing-related water damage is included in your contract. Flooding from heavy rain or swollen streams is typically excluded from standard landlord policies and requires separate flood insurance, which is critical if your property sits near low-lying areas. West Hartford’s nor’easters and heavy snow events damage roofs, cause ice dams, and rupture frozen pipes, making water damage a real threat rather than a theoretical one. Your policy should spell out exactly which water-related losses your coverage protects and which ones fall outside the agreement.

Aging Properties Command Higher Premiums

West Hartford’s aging housing stock affects your insurance costs significantly. Older buildings with outdated electrical systems, aging roofs, and original plumbing carry higher claim frequency, and insurers price premiums accordingly. Properties built before 1950 face steeper rates than newer construction. If you own a multi-unit building, standard landlord policies won’t work at all-Connecticut insurance requirements shift to apartment complex or commercial coverage for five or more units. Working with an agency that understands West Hartford’s specific property types, weather patterns, and local market conditions ensures your coverage matches the actual risks you face, not generic assumptions about Connecticut rental properties. This local knowledge becomes especially valuable when you’re trying to find carriers willing to write policies on older properties or when you need to navigate the coverage gaps that affect West Hartford landlords specifically.

Three Coverage Types That Actually Protect Your West Hartford Investment

Dwelling Fire Insurance Reflects Current Replacement Costs

Dwelling fire insurance and structure protection form the foundation of your landlord policy, and this coverage must reflect what your West Hartford property costs to rebuild today, not what you paid for it years ago. Connecticut properties appreciate over time, and if you haven’t updated your dwelling coverage limits in five or more years, you’re likely underinsured. To estimate your home’s replacement cost, you can multiply your home’s square footage by average building costs per square foot in your area. Your policy should cover the replacement cost of the structure itself-the walls, roof, foundation, built-in appliances, and permanent fixtures-at today’s prices, not depreciated value. Request a professional property valuation from your agent every three to five years, and adjust your dwelling coverage accordingly. If your property has unique features like updated electrical systems, newer HVAC equipment, or recent roof replacement, mention these explicitly when getting quotes because they can lower your premiums and demonstrate that your property carries lower risk than comparable older homes in West Hartford.

Liability Coverage Protects Against Tenant and Guest Injuries

Liability coverage protects you when a tenant or their guest suffers an injury on your rental property and holds you responsible. Connecticut courts have awarded substantial judgments in landlord liability cases, and typical coverage limits of $100,000 often prove insufficient when medical bills, lost wages, and pain-and-suffering awards combine. A slip-and-fall injury that requires surgery and months of physical therapy can easily exceed $150,000 in total damages, meaning your policy’s liability limit becomes the difference between a manageable claim and a devastating judgment. West Hartford landlords with older properties or those lacking modern safety features should strongly consider $300,000 to $500,000 in liability limits, and umbrella liability coverage adds another $1 million of protection at a reasonable cost.

Loss of Rents Coverage Bridges Income Gaps During Repairs

Loss of rents coverage reimburses you for income when a covered loss-fire, storm damage, burst pipes-makes the property temporarily uninhabitable. This coverage typically reimburses fair rental value for the property during repairs, though the exact timeline depends on your policy language. If your West Hartford rental generates $2,000 monthly and repairs take four months, loss of rents coverage provides $8,000 in compensation that prevents that income gap from forcing you to draw from personal savings or business reserves. This protection matters most when major damage occurs during peak rental seasons, as the financial impact compounds quickly without proper coverage in place.

Why Local Knowledge Changes Your Insurance Costs

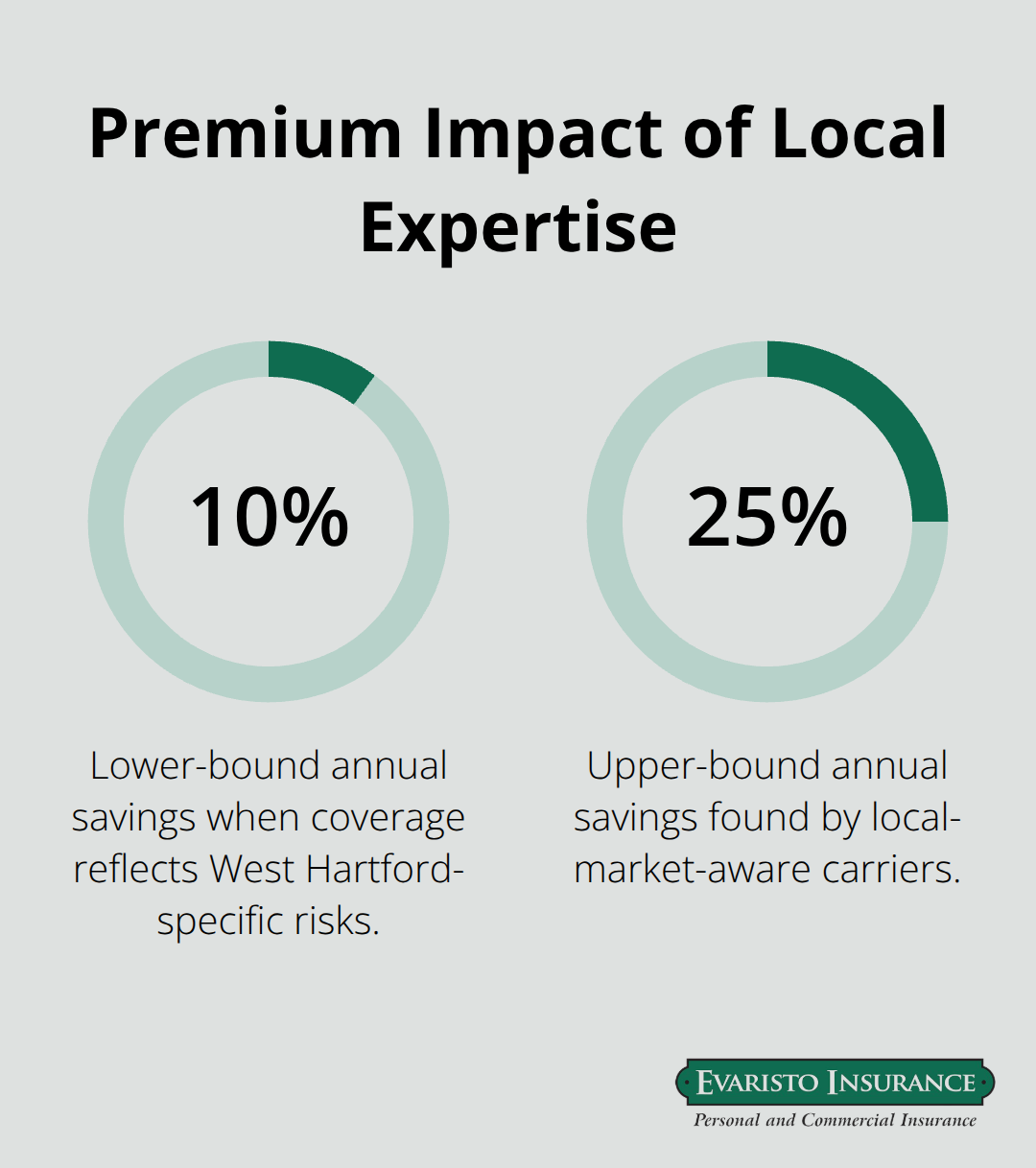

West Hartford’s weather patterns create specific risks that generic insurance carriers either overprice or refuse to cover altogether. The region experiences nor’easters that damage roofs, ice storms that snap tree branches onto structures, and spring flooding that affects properties near the Park River and Trout Brook. A carrier based outside Connecticut applies blanket pricing that assumes all Connecticut properties face identical risk, but your West Hartford property’s actual exposure depends on elevation, proximity to water, tree coverage, and roof age. Properties on elevated ground in neighborhoods like Westmount face different water damage frequency than properties in lower-lying areas near West Hartford’s stream systems. Carriers that understand these local conditions price your policy accurately instead of padding premiums to cover theoretical worst-case scenarios. Independent agencies that compare multiple top carriers often find that the difference between a carrier understanding West Hartford’s specific weather exposure and one that doesn’t ranges from 10 to 25 percent on annual premiums. That savings compounds over a five-year policy period, and more importantly, it means you’re not subsidizing risk that doesn’t actually apply to your property.

Property Values Shift Faster Than Your Coverage Limits

West Hartford’s real estate market appreciated significantly between 2022 and 2024, which means properties purchased five years ago are worth considerably more today. If you set your dwelling coverage limit based on your purchase price or your mortgage value, you’re dramatically underinsured. A West Hartford home purchased for $450,000 in 2019 might be worth $550,000 today, but if your dwelling coverage still reflects the original purchase price, you’d recover only a fraction of actual rebuilding costs if fire destroyed the structure. Replacement cost for residential construction in Connecticut averages $150 to $200 per square foot depending on finishes and location, which means a 2,500-square-foot home costs $375,000 to $500,000 to rebuild today. Mortgage lenders typically require coverage equal to the loan amount, but loan amounts often lag behind actual property values. Request updated property valuations every three years and adjust your dwelling limits accordingly. Local carriers that track West Hartford market conditions understand this appreciation pattern and flag underinsurance automatically during renewal; out-of-state carriers often don’t.

Connecticut Carriers Know Which Risks Insurers Actually Accept

Not all landlord policies are available in Connecticut, and not all carriers willing to write policies in other states will touch West Hartford rental properties with older roofs or deferred maintenance. A carrier might decline to insure a property with a roof older than 15 years, or they might require expensive upgrades before issuing a policy. West Hartford has significant housing stock built before 1960, and many carriers view pre-1950 construction as too risky to insure at standard rates. An independent agency with established relationships across Connecticut’s insurance market knows which carriers accept older properties, which ones require inspections, and which ones will price competitively despite the property’s age. This knowledge matters when you’re trying to insure a rental that other agencies have declined. An independent agency serving Connecticut since 1989 works with carriers that understand Connecticut’s older housing stock and price accordingly, rather than forcing you to accept coverage from high-risk carriers or paying dramatically inflated premiums.

Final Thoughts

West Hartford landlord insurance protects your rental income, your liability exposure, and your ability to recover quickly when damage strikes. Dwelling protection, liability limits, and loss of rents coverage form the foundation of a strategy that keeps your investment secure regardless of what Connecticut’s weather or tenant situations throw at you. Your property’s age, location, elevation, and local market value all affect what coverage you actually need and what you’ll pay for it.

Your next step is straightforward: obtain a property valuation to confirm your dwelling coverage reflects current replacement costs, then contact an agency that understands West Hartford’s specific risks. Don’t accept generic quotes from carriers that treat Connecticut as a single market. We at Evaristo Insurance have worked with West Hartford landlords since 1989, comparing multiple top carriers to find coverage that matches your property and your budget.

Our local offices in Ellington and West Hartford mean we understand the weather patterns that damage roofs, the market conditions that shift property values, and the carriers willing to write policies on older homes. Contact us to discuss your specific property, and we’ll deliver a tailored quote that reflects what your West Hartford rental actually costs to protect. The difference between generic coverage and coverage built for your situation often runs 10 to 25 percent on your annual premium-savings that compound over years while ensuring you’re not underinsured when claims happen.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.