Landlord Coverage CT: Essentials for Connecticut Property Owners

Owning rental property in Connecticut comes with real financial exposure. Without proper landlord coverage CT, a single liability claim or property damage incident can wipe out years of rental income.

At Evaristo Insurance, we’ve helped hundreds of Connecticut property owners understand what protection they actually need-and what gaps could cost them thousands.

What Your Landlord Policy Actually Covers

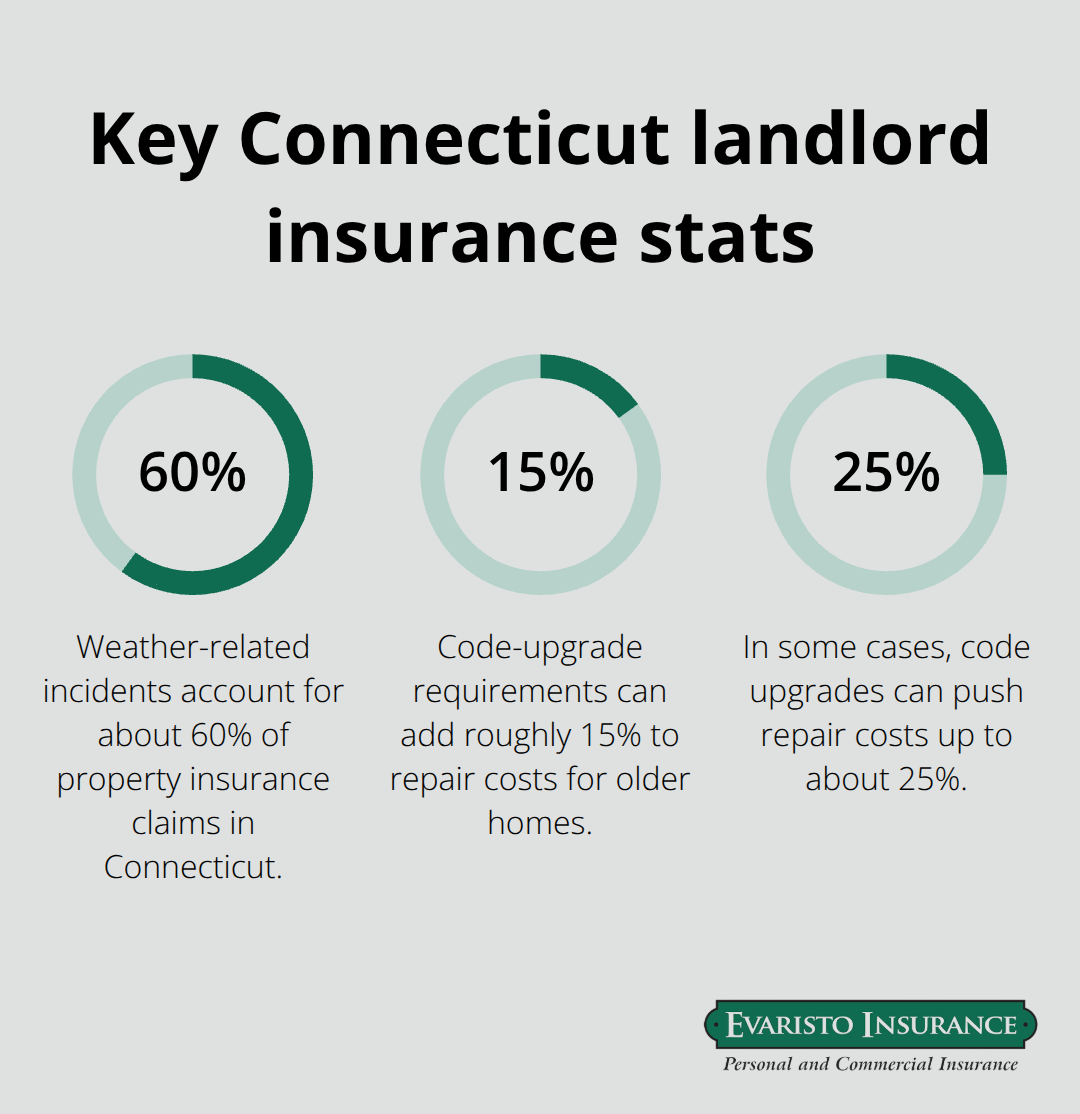

Connecticut landlord insurance protects three critical areas that standard homeowners policies ignore: the building structure, liability exposure, and lost rental income when tenants cannot occupy the property. The building coverage reimburses repair or replacement costs after fire, wind, hail, theft, or vandalism. This matters because Connecticut’s older housing stock faces higher repair costs when damage occurs. Weather-related incidents account for about 60% of property insurance claims in the state, with winter storms representing the highest frequency category. You need coverage limits that reflect your property’s replacement cost, not just its market value. A property worth $250,000 might cost $300,000 to rebuild to current code standards, especially in older neighborhoods where structural updates are required during reconstruction.

Why Liability Protection Isn’t Optional

Liability coverage protects you when a tenant or visitor gets injured on your property. Connecticut’s tenant-protective legal environment means injured parties have strong grounds to sue, and medical costs plus legal defense fees escalate quickly. A slip-and-fall claim can easily exceed $50,000 in medical expenses and legal costs combined. Standard policies typically offer $100,000 to $300,000 in liability limits, but multi-unit properties or properties in higher-traffic areas warrant $500,000 or higher. Many property owners carry umbrella policies for an additional $1 million in protection, costing just $150–$300 annually. Medical payments coverage-usually $1,000–$5,000 per person-covers minor injuries without requiring a lawsuit, reducing the likelihood that injured parties pursue formal claims.

Loss of Rental Income Keeps Your Cash Flow Intact

When a covered peril makes the property uninhabitable, loss of rental income coverage reimburses your lost rent while repairs happen. Most Connecticut policies cover 12–24 months of lost rental income. If your property generates $2,000 monthly rent and repairs take four months, this coverage reimburses $8,000 in lost income. This protection becomes critical during winter storms or fire damage when repairs extend beyond a few weeks. Connecticut landlords on Steadily report median annual premiums around $2,610, reflecting the state’s older housing stock and higher replacement values.

Eviction and Legal Defense Coverage Requires Separate Protection

Standard policies do not cover eviction proceedings or tenant dispute defense costs. Eviction insurance or rent guarantee coverage exists separately and typically carries high premiums with significant deductibles and strict limits, making it expensive relative to the protection it provides. Understanding these gaps matters before you face a tenant dispute that your current policy cannot address.

Connecticut Landlord Insurance Requirements and Regulations

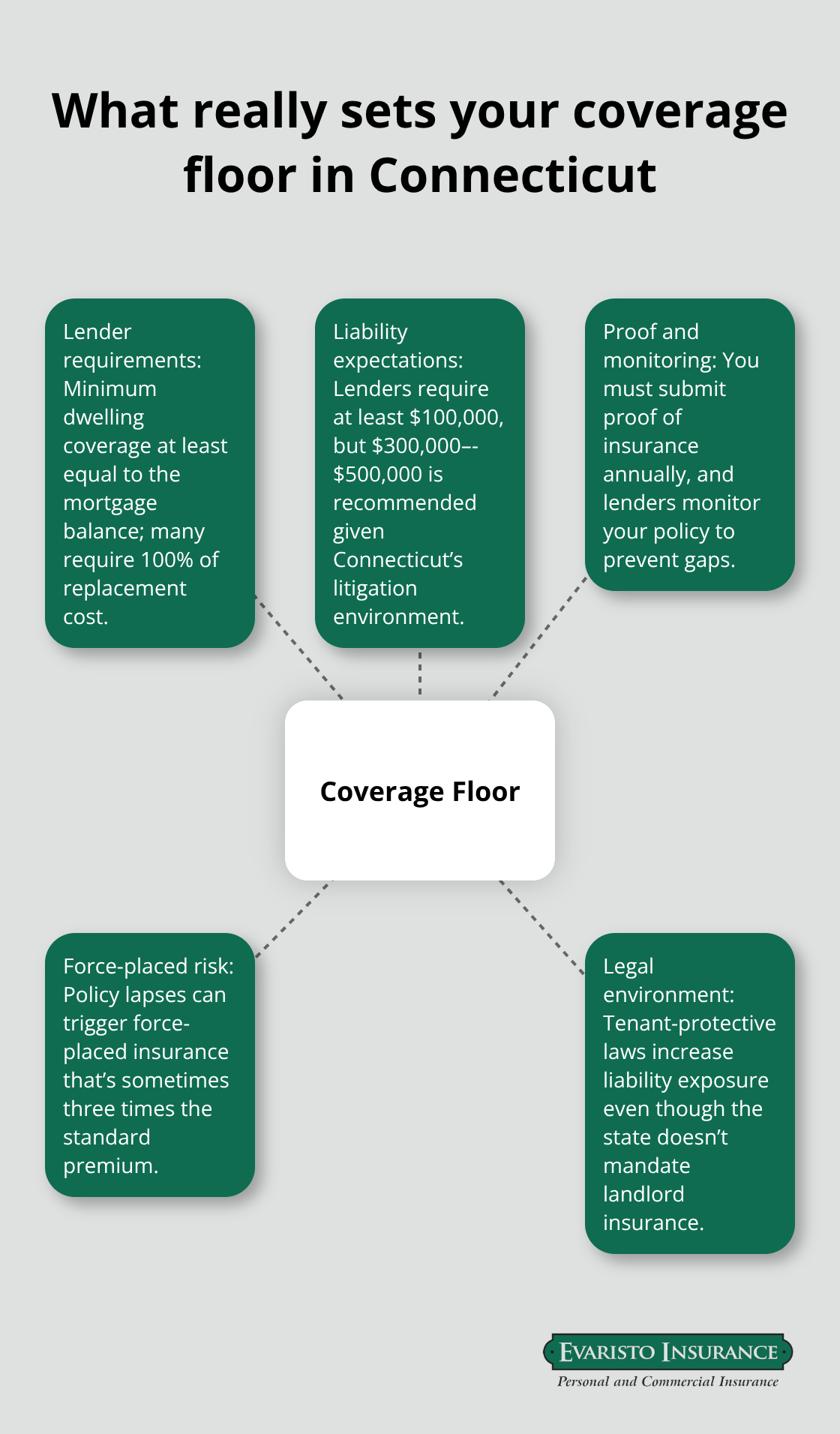

Connecticut does not legally mandate landlord insurance, but this absence of legal requirement creates a dangerous false sense of security for property owners. Your lender almost certainly requires it, and that requirement is non-negotiable if you financed your rental property. Most mortgage agreements include a clause demanding proof of landlord coverage before the lender will release funds or continue the loan. If you own the property outright, the decision falls entirely on you-but Connecticut’s legal landscape makes that decision straightforward: you need coverage. Connecticut’s tenant-protective laws favor renters in disputes, meaning liability exposure is substantial. A single uninsured liability claim wipes out the financial advantage of owning property outright.

Lenders Set the Actual Coverage Floor

Your mortgage lender specifies minimum coverage amounts in your loan documents, and these minimums typically exceed what you might choose on your own. Lenders require dwelling coverage at least equal to the mortgage balance, though many require coverage at 100% of replacement cost. They mandate liability limits of at least $100,000, though we strongly recommend $300,000 to $500,000 for Connecticut properties given the state’s litigation environment. You must submit proof of insurance annually, and lenders monitor coverage to maintain it without gaps. If you allow your policy to lapse, the lender can purchase force-placed insurance at dramatically inflated costs-sometimes three times the standard premium-and add those charges to your mortgage. This scenario costs Connecticut landlords thousands unnecessarily.

Municipal Codes Shape Your Coverage Needs

Municipal property tax assessments and local building codes create additional practical requirements that shape what your policy should include. Older Connecticut properties often trigger code-upgrade requirements during reconstruction, meaning your coverage limits must account for the gap between today’s replacement cost and the cost to rebuild to current standards. Some municipalities in Hartford County and Fairfield County require proof of liability coverage before issuing rental licenses, effectively making coverage mandatory at the local level even though state law does not. Contact your town’s assessor or licensing department to confirm what your specific municipality expects.

Building Code Coverage Prevents Hidden Reconstruction Costs

Connecticut’s housing stock is aging-a large share was built before 1980-and reconstruction costs reflect modern code compliance. Standard policies pay only for repairing or replacing what was destroyed, not for the additional expense to bring repairs up to current electrical, plumbing, or structural codes. A fire in a 1970s home might trigger requirements for updated electrical wiring and insulation that add 15% to 25% to repair costs. Building code coverage endorsements reimburse these upgrade costs, protecting you from absorbing thousands in uninsured expenses. This endorsement costs roughly $75 to $150 annually but prevents catastrophic out-of-pocket losses on older properties.

These regulatory layers and code requirements reveal why Connecticut landlords face coverage gaps that extend far beyond what state law technically mandates. The real protection floor sits much higher than the legal minimum-and identifying those gaps before a loss occurs separates property owners who recover quickly from those who face financial ruin.

Common Gaps in Landlord Policies and How to Avoid Them

Replacement Cost Mistakes That Drain Your Finances

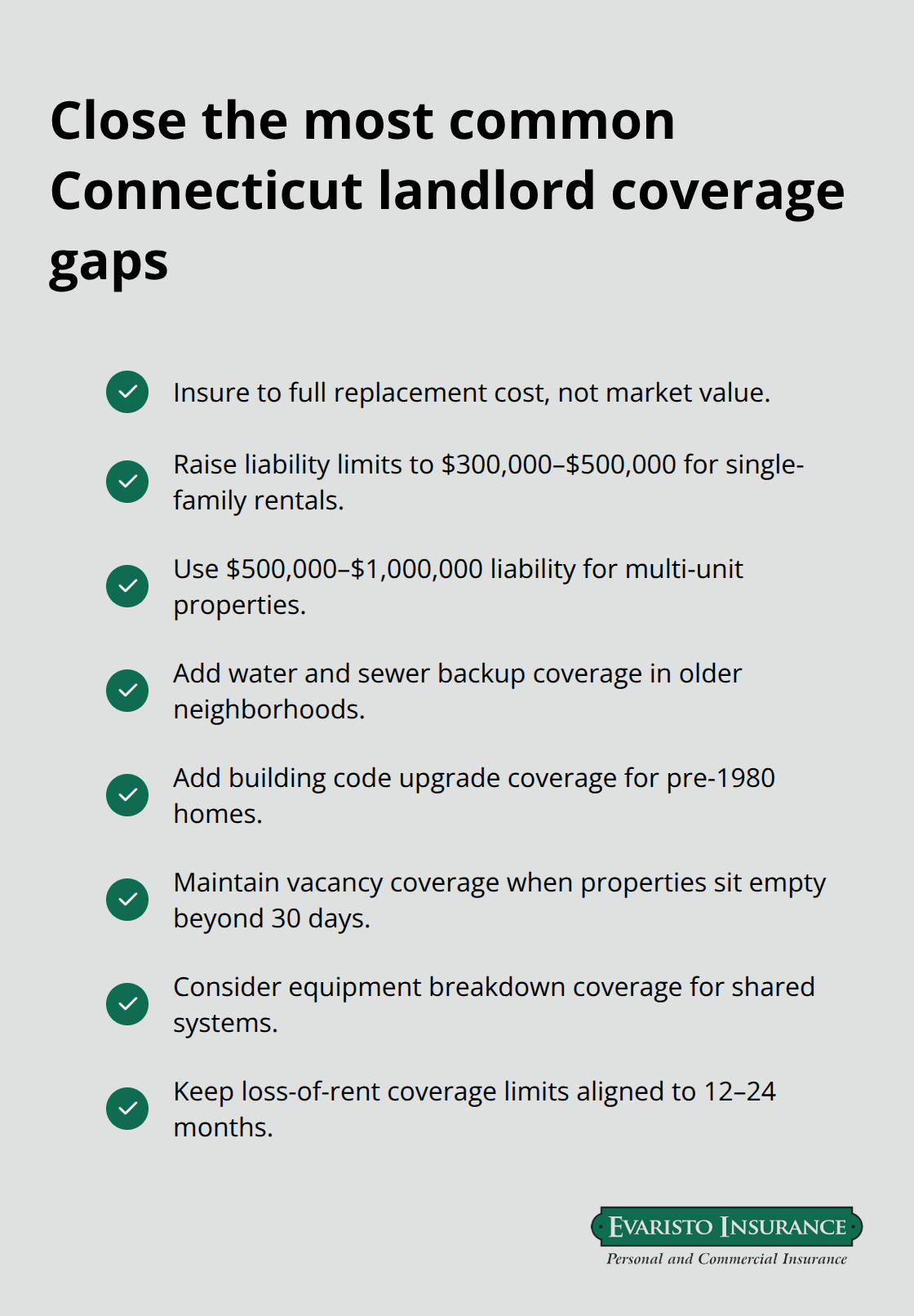

Most Connecticut landlords anchor coverage limits to market value instead of rebuild expenses. A property assessed at $280,000 might cost $350,000 to rebuild to current code standards, especially in towns like Stamford, Hartford, and New Haven where older construction dominates. Property owners set dwelling coverage limits at 80% of replacement cost to save on premiums, then face catastrophic out-of-pocket costs when fire or storm damage occurs. Connecticut’s older housing stock makes this mistake particularly expensive. The state’s median home age sits well above the national average, and reconstruction triggers code-upgrade requirements that standard repair estimates miss entirely. Your coverage limit should reflect full replacement cost, not discounted estimates.

Liability Limits That Leave You Exposed

Liability limits present a second critical gap that Connecticut landlords routinely misjudge. Many carry the minimum $100,000 limit their lender requires, treating that figure as adequate protection when Connecticut’s litigation environment demands far more. A single serious injury-broken bones from a fall on icy steps, dog bite from a tenant’s animal, or injury from a structural defect-generates medical bills exceeding $100,000 within weeks. Legal defense costs alone can reach $50,000 before trial even begins. Multi-unit properties face exponentially higher exposure because more people occupy the premises and more incidents occur statistically. Try $300,000 to $500,000 in liability limits for single-family rentals and $500,000 to $1,000,000 for multi-unit properties. The premium difference between $100,000 and $500,000 in liability coverage typically runs $200 to $400 annually-a trivial expense relative to the financial devastation an underinsured claim creates.

Multi-Unit Properties Require Scaled Coverage

Multi-unit property owners create additional gaps by treating their buildings as if standard landlord policies address commercial exposure. A duplex, triplex, or four-unit building generates significantly higher liability claims frequency than single-family homes. More tenants means more visitors, more maintenance activities, more opportunities for injury. Standard DP-3 policies cover these properties, but coverage limits and endorsements must scale to match exposure. Water damage and equipment breakdown endorsements become essential for multi-unit buildings because shared plumbing systems and HVAC units serve multiple units simultaneously. A burst pipe affecting four units generates four times the disruption and four times the lost rental income compared to single-family damage. Request detailed loss history data from your insurer to identify which perils generate claims most frequently in your specific property type and location. This data shapes which endorsements deliver real value versus which represent unnecessary premium additions.

Water Backup and Vacancy Gaps Create Hidden Exposures

Connecticut landlords consistently overlook sewer and drain backup coverage, yet this peril generates substantial claims in older neighborhoods where municipal sewer infrastructure predates modern standards. A single backup event costs $8,000 to $15,000 in cleanup and structural repair. This endorsement costs roughly $100 to $200 annually and eliminates a catastrophic uninsured exposure that standard policies explicitly exclude. Vacancy coverage represents another frequently missed protection. Properties vacant for more than 30 days lose standard coverage under many policies, creating risk during renovations, tenant transitions, or market slowdowns.

Connecticut’s rental market shows strong demand in Hartford, New Haven, and Bridgeport, but vacancy gaps still occur during seasonal transitions or property repositioning. A 60-day vacancy without proper endorsement leaves the building completely uninsured for theft, vandalism, or weather damage-precisely the perils most likely to strike empty properties.

Final Thoughts

Connecticut landlords who carry inadequate coverage face financial devastation that proper protection prevents entirely. Underestimating replacement costs, carrying insufficient liability limits, and missing specialized endorsements create gaps that cost thousands when losses strike. Your property’s age, location, and tenant occupancy demand landlord coverage CT that exceeds your lender’s minimum requirements substantially, and Connecticut’s litigation environment makes this reality non-negotiable.

Three actions protect your rental investment immediately. Calculate your property’s actual replacement cost by consulting local contractors who understand code requirements in your specific town. Review your liability limits against your property type-single-family rentals warrant $300,000 to $500,000, while multi-unit buildings demand $500,000 to $1,000,000. Audit your endorsements for water backup, building code coverage, and vacancy protection, as these address Connecticut’s specific perils that standard policies exclude.

We at Evaristo Insurance have guided Connecticut property owners through this process for decades, comparing multiple carriers to build coverage that matches your actual exposure and budget. Contact us for a detailed review of your current landlord coverage CT and a competitive quote that reflects what Connecticut landlords truly need.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.