Commercial Landscaper Insurance CT: Protecting Your Business Assets

Running a landscaping business in Connecticut means managing significant equipment investments, seasonal staffing, and liability risks that standard business insurance won’t cover.

Commercial landscaper insurance in CT is specifically designed to protect against the unique hazards your operation faces-from property damage claims to employee injuries on job sites. At Evaristo Insurance, we work with landscapers throughout Connecticut who understand that the right coverage isn’t optional; it’s essential to staying in business.

What Your Commercial Landscaper Insurance Actually Covers

General Liability: Your First Line of Defense

General liability insurance protects you when someone gets hurt or their property gets damaged because of your work. If a client claims you damaged their deck while trimming branches, or a pedestrian trips over your equipment and breaks their leg, general liability covers legal fees, medical expenses, and settlement costs up to your policy limits. Connecticut requires landscapers to carry general liability insurance of at least $1 million per occurrence and $2 million aggregate. Most Connecticut landscapers spend between $1,100 and $2,300 annually for this coverage, making it the most cost-effective protection you can buy.

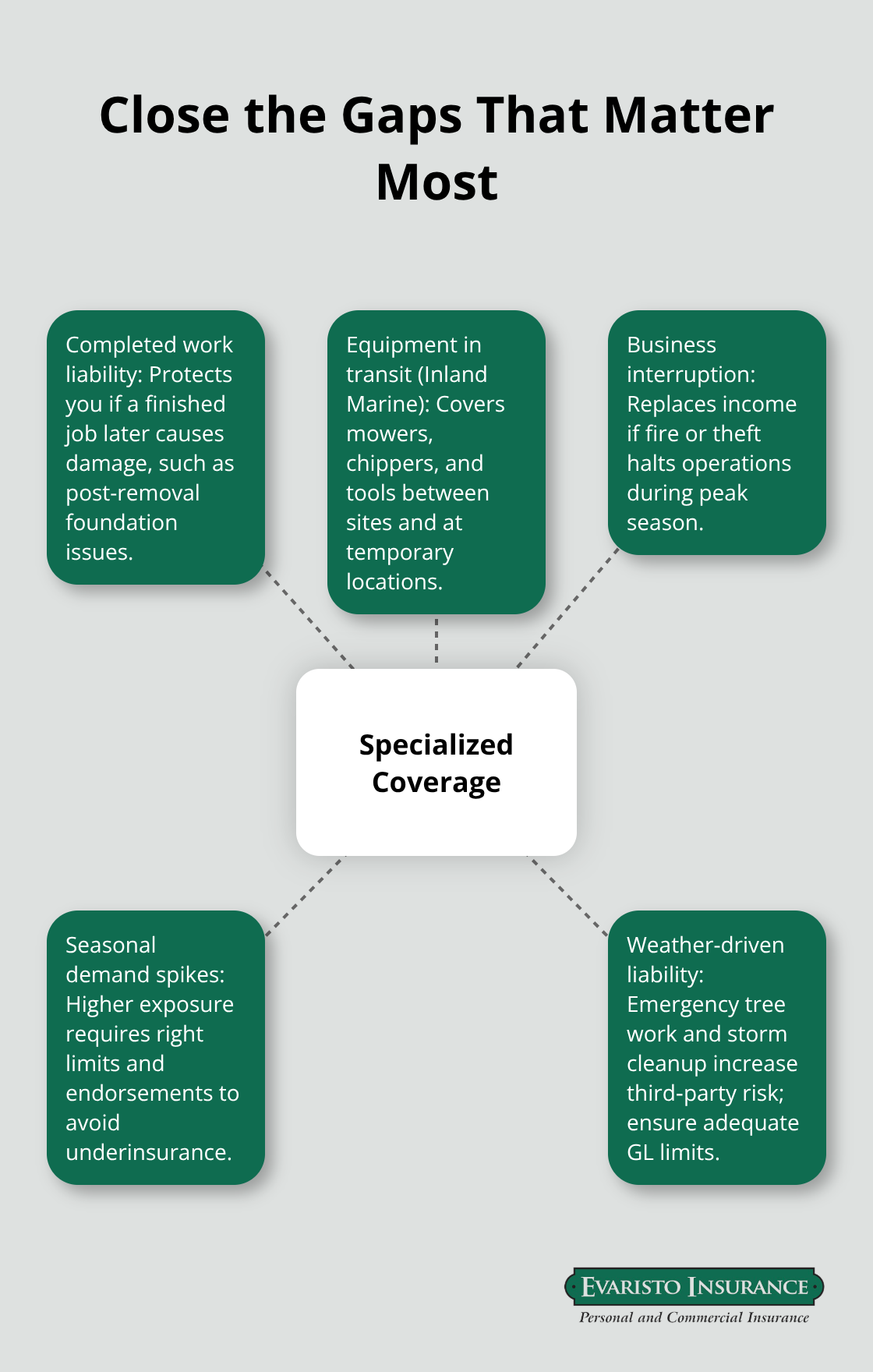

Standard general liability policies often exclude damage to property you were hired to protect or work you’ve already completed. If you remove a tree and it later causes foundation damage, that completed work scenario might not be covered without specialized endorsements. This gap matters more than most landscapers realize, especially when handling high-value residential properties or municipal contracts.

Equipment Protection: Safeguarding Your Tools and Vehicles

Your equipment and vehicles represent your operational backbone, which is why protection matters separately from liability. Commercial auto insurance covers your trucks and trailers on the road, protecting against third-party claims if you cause an accident. Connecticut’s minimum auto liability is 25/50/25, but you should carry higher limits given the value of equipment you transport.

Inland marine coverage protects your mowers, chippers, blowers, and hand tools while they’re in transit between jobs or sitting at temporary job sites. This coverage is essential because the National Insurance Crime Bureau reports that equipment theft costs U.S. businesses about $400 million annually, and landscaping equipment is a frequent target. Commercial property insurance safeguards tools stored at your base facility and can include business interruption protection if fire or theft forces you to pause operations during peak season.

Workers’ Compensation: Protecting Your Team

Workers’ compensation is mandatory in Connecticut for any employer with employees and covers medical costs plus partial wages when someone gets injured on the job. Johns Hopkins University research found that more than 6,000 people per year are seriously injured in lawnmower accidents nationwide, underscoring why this coverage protects both your crew and your business finances. A typical Connecticut workers’ compensation policy costs between $400 and $3,000 annually depending on crew size and the specific tasks your team performs.

These three coverage types form the foundation of commercial landscaper protection, but Connecticut’s regulatory environment and your specific operations may demand additional layers. Understanding what each policy covers-and more importantly, what gaps exist-determines whether you’re truly protected or exposed to catastrophic financial loss.

Why Connecticut Landscapers Face Unique Insurance Demands

State Regulations Create Hard Minimums You Cannot Ignore

Connecticut’s regulatory framework imposes hard minimums that most landscapers initially underestimate. The state requires general liability coverage of at least $1 million per occurrence and $2 million aggregate, but this baseline leaves dangerous gaps for anyone handling high-value residential work or municipal contracts. Connecticut also mandates workers’ compensation for any operation with one employee or more, with penalties including fines and potential license suspension for non-compliance. Individual municipalities and property owners increasingly demand proof of coverage before granting access to job sites, meaning you’ll need certificates of insurance issued quickly and accurately. Landscapers lose contracts regularly because they lack the right documentation or coverage limits to meet client requirements, so treating compliance as a checkbox rather than a competitive advantage costs you money.

Weather Volatility Drives Emergency Work and Liability Exposure

Connecticut’s weather patterns create operational risks that standard policies don’t adequately address. The region experiences unpredictable spring storms, summer downpours, and fall hurricanes that generate emergency tree work and high-liability scenarios-a downed power line, a branch through a neighbor’s window, or debris damaging client property during removal. Rising commercial property insurance rates across Connecticut have hit landscapers particularly hard, with premiums climbing 15-25% over the past two years as insurers account for increased storm frequency and severity. Equipment theft remains a persistent threat; high-end zero-turn mowers and chippers disappear from job sites and trailers regularly, and standard property coverage often excludes equipment at temporary locations unless you add inland marine protection.

Specialized Coverage Addresses Your Actual Risk Profile

The combination of seasonal demand spikes, expensive equipment vulnerable to theft, and weather-driven liability creates a risk profile that generic business insurance simply cannot cover. Specialized landscaper policies address these specific exposures directly, which is why choosing coverage designed for your industry rather than adapting general contractor policies protects your assets and revenue stream far more effectively. Understanding which coverage gaps matter most to your operation-whether that’s completed work liability, equipment in transit, or business interruption during peak season-determines how well your insurance actually protects you when claims arise.

Selecting Coverage That Matches Your Actual Operations

Document Your Services and Equipment Value

Start by listing everything your landscaping business does, not what you think you might do someday. Specific services-lawn maintenance, tree removal, hardscaping, chemical application, snow removal, or equipment rental-each carry different liability profiles and demand different coverage. A crew that only maintains residential lawns faces fundamentally different risks than one that removes trees near power lines or applies herbicides.

Write down your equipment inventory with serial numbers, purchase prices, and replacement costs. Most landscapers underestimate their total equipment value until they list every mower, chipper, blower, trailer, and truck. This number directly determines your inland marine and commercial property coverage limits.

Classify Your Workforce Accurately

Count your employees and classify them correctly, because misclassifying workers as independent contractors to avoid workers’ compensation costs triggers Connecticut Department of Labor investigations and penalties that dwarf the insurance savings. Connecticut requires workers’ compensation coverage for any operation with one employee or more, and the state enforces this requirement aggressively.

Identify Client Coverage Requirements

Document your largest contracts and the liability limits clients require, which often exceed state minimums significantly. A municipal contract or high-value residential project might demand $2 million or $5 million in general liability coverage, and underinsuring for those jobs exposes your entire business to uninsured claims.

Compare Multiple Quotes and Coverage Options

Once you understand your actual risk profile, compare quotes from multiple carriers rather than accepting the first offer. Connecticut’s commercial landscaper market includes national insurers alongside regional specialists, and pricing varies dramatically for identical coverage. A Business Owner’s Policy bundling general liability, property, and business interruption typically costs 20-30% less than purchasing each separately, so comparing bundled packages against individual policies reveals your true savings opportunities.

Request quotes that specify coverage limits, deductibles, and endorsements clearly, because two policies with identical premium prices often provide vastly different protection. Ask each carrier about loss-prevention credits for documented safety training, equipment maintenance programs, or secure storage solutions (these measures can reduce premiums 5-15% annually). Get at least three quotes before deciding, and don’t assume the lowest price provides adequate coverage.

Work with Local Agents Who Understand Connecticut

Local agents understand Connecticut’s specific regulatory requirements and regional weather risks far better than national call centers, which matters when you need certificates of insurance issued quickly or when you face questions about coverage interpretation during a claim. An independent agency compares multiple top carriers to help you identify the best combination of competitive pricing and genuine protection rather than settling for cheap coverage with dangerous gaps.

Final Thoughts

Commercial landscaper insurance CT protects your business from the financial devastation that follows equipment theft, employee injuries, or liability claims. The coverage you carry determines whether a single accident drains your cash flow or your insurer handles it, which is why you should treat insurance as a strategic business decision rather than a compliance checkbox. Connecticut’s regulatory requirements establish hard minimums, but those minimums leave dangerous gaps for anyone handling valuable contracts or high-end residential work.

Start protecting your business by documenting your actual services, equipment inventory, and client coverage requirements (this foundation lets you compare quotes accurately and identify which coverage options genuinely match your risk profile). Request multiple quotes from different carriers, ask about loss-prevention credits that can reduce premiums, and compare bundled policies against individual coverage to find your best value. Working with a local agent who understands Connecticut’s regulatory environment and regional weather patterns gives you a significant advantage over national insurers.

Contact Evaristo Insurance to discuss your specific coverage needs and receive a quote that protects your equipment, your crew, and your business reputation. Our offices in Ellington and West Hartford compare multiple carriers to deliver tailored protection that matches your actual operations.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.