BOP Coverage Connecticut: Simplifying Your Small Business Protection

Running a small business in Connecticut means protecting what you’ve built. A Business Owners Policy, or BOP, combines the essential coverage most small businesses need into one straightforward package.

At Evaristo Insurance, we’ve helped countless Connecticut business owners understand how BOP coverage works and why it matters for their specific situation. Whether you operate a retail shop, service business, or office, this guide walks you through what you need to know.

BOP Coverage Connecticut: What Protection Actually Looks Like

What a BOP Actually Covers

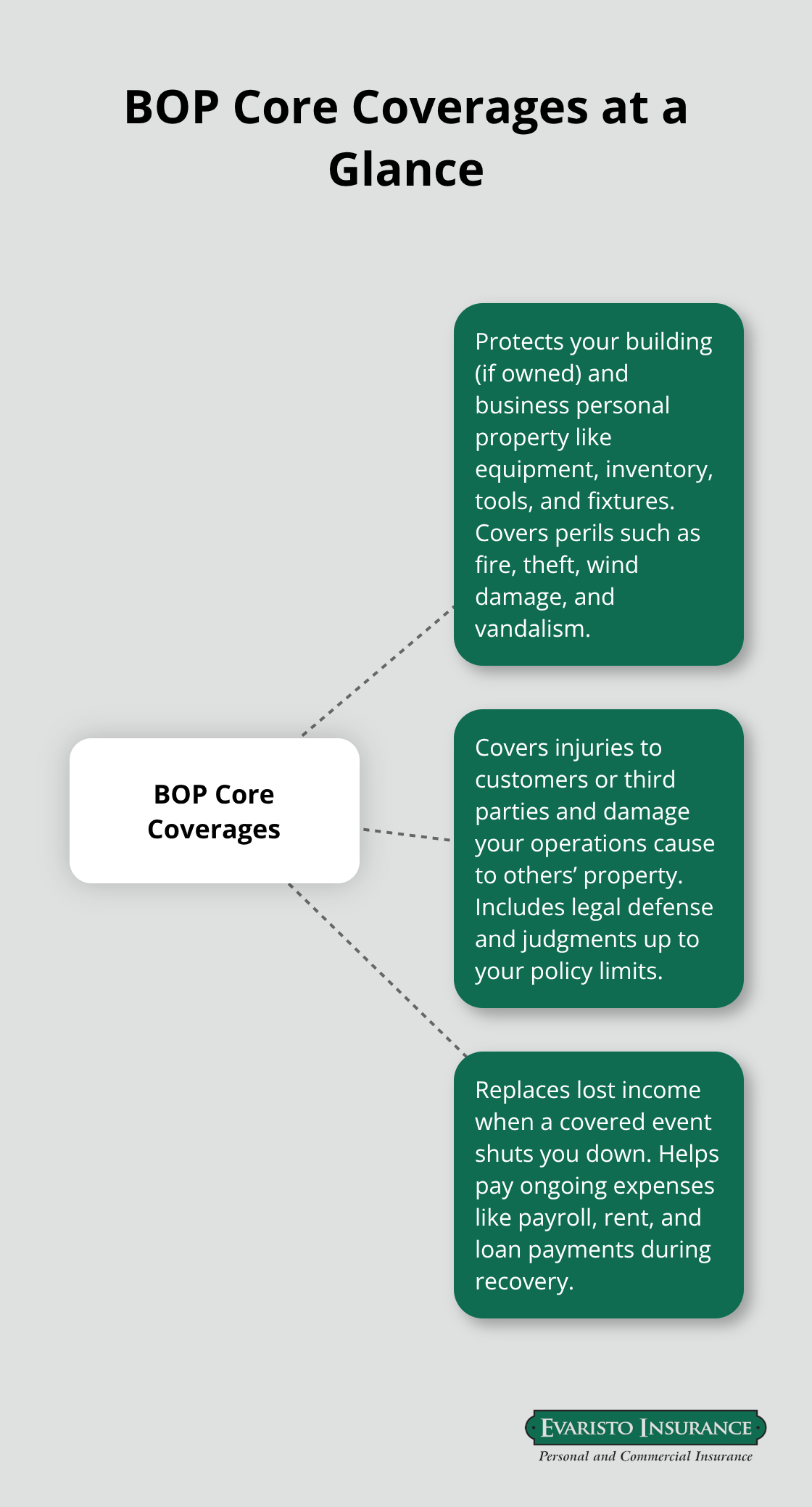

A Business Owners Policy bundles three essential coverages into one package: commercial property insurance, general liability insurance, and business interruption coverage. Property coverage protects your physical assets-the building you rent or own, equipment, inventory, tools, and fixtures-from perils like fire, theft, wind damage, and vandalism. General liability covers you when a customer or third party gets injured on your premises or when your business operations cause property damage to someone else. Business interruption coverage can help supplement your business income if you can’t operate due to a covered event, covering expenses like payroll, rent, and loan payments while you recover.

Connecticut small businesses often find that bundling these three coverages together costs substantially less than purchasing them separately, which is why the BOP model has become the standard protection strategy for owner-operated shops, service businesses, and professional offices across the state.

Connecticut Businesses Face Real, Specific Risks

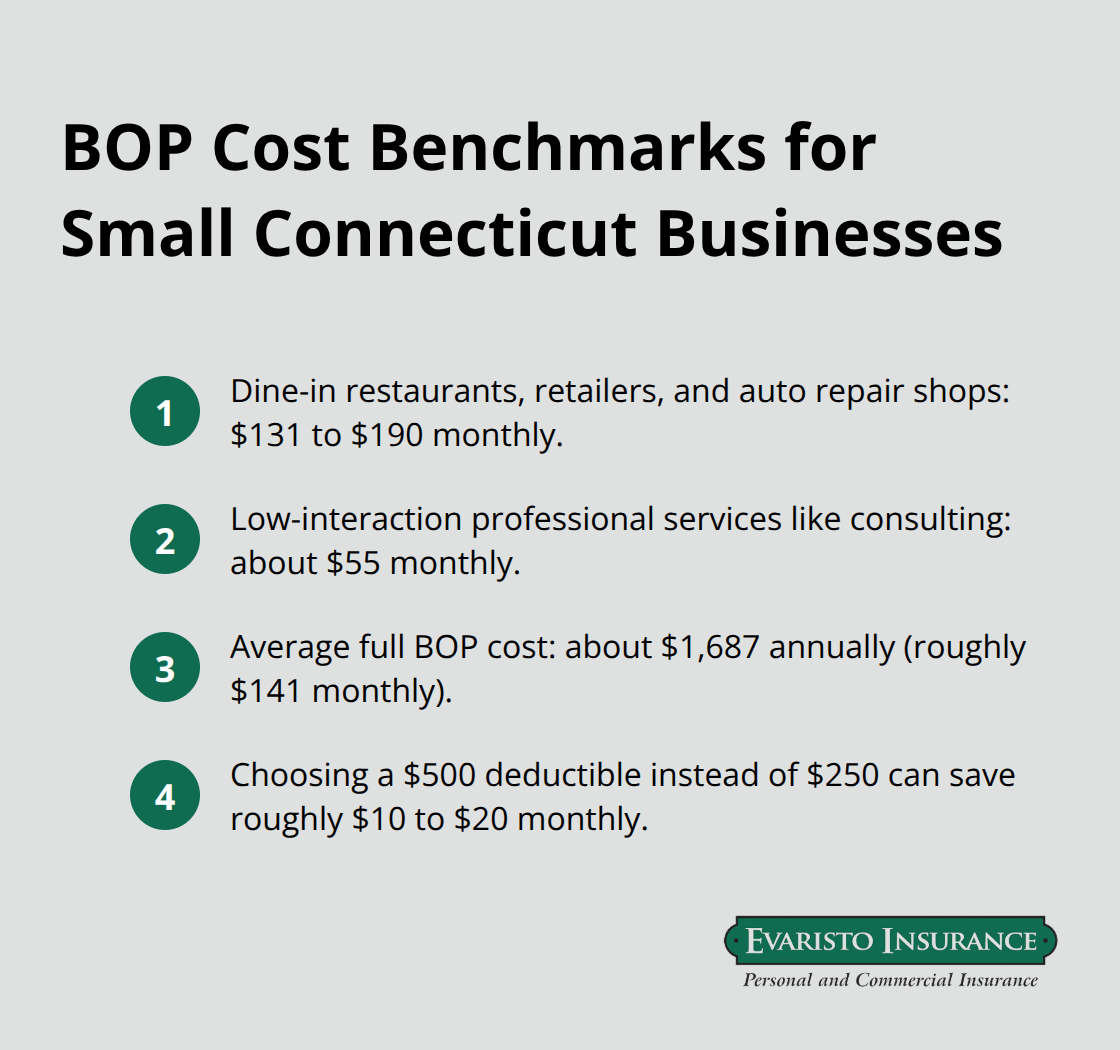

Connecticut’s geography and business environment create exposures that generic insurance solutions miss entirely. Coastal and riverside properties face genuine flood risk, yet standard BOPs exclude flood damage-meaning a business in a flood-prone Connecticut area needs separate flood insurance to stay truly protected. Older commercial buildings, common throughout Connecticut’s established towns, often have aging electrical systems, plumbing, and roofs that increase fire and water damage likelihood. Weather volatility matters too: the 2024 and 2025 storm seasons brought significant wind and water damage claims across the Northeast. If your business operates in a higher-risk industry-restaurants with dine-in service, retail shops, auto repair facilities-your liability exposure is substantially higher than a consulting business. Insureon’s data from roughly 100,000 small business policyholders shows that dine-in restaurants, retailers, and auto repair shops typically pay $131 to $190 monthly for BOP coverage, compared to just $55 monthly for low-interaction professional services like consulting. Location within Connecticut matters: businesses in Hartford or Waterbury neighborhoods with higher crime rates face greater theft and vandalism risk than suburban locations. These aren’t theoretical concerns-they’re the actual loss patterns that shape what coverage you need and what your premium will be.

How BOP Protection Works When Loss Happens

When a covered event damages your business, the property portion of your BOP pays to repair or replace assets based on your chosen coverage limit and deductible. If a kitchen fire forces your restaurant to close for three weeks, business interruption coverage kicks in to cover your lost profits plus ongoing expenses like staff payroll and vendor payments-without this coverage, you absorb those costs entirely out of pocket. General liability protection activates when a customer slips in your store and sues, or when your contractor accidentally damages a client’s property; your BOP pays legal defense costs and any judgment up to your policy limit, protecting your personal assets from seizure. Most Connecticut small business owners choose $1 million per occurrence and $2 million aggregate liability limits, according to Insureon’s customer data, with an average deductible around $500. The deductible amount matters strategically: choosing a higher deductible like $1,000 or $2,500 lowers your monthly premium, but only if you can actually afford to pay that amount when a loss occurs. If your business operates out of a building you own, property coverage protects the structure itself plus your business personal property inside; if you rent, your coverage applies only to the contents and improvements you’ve made, not the landlord’s building. This distinction is critical because underinsuring your property value means claims get reduced proportionally, leaving you short when you need the money most.

Identifying Your Coverage Gaps

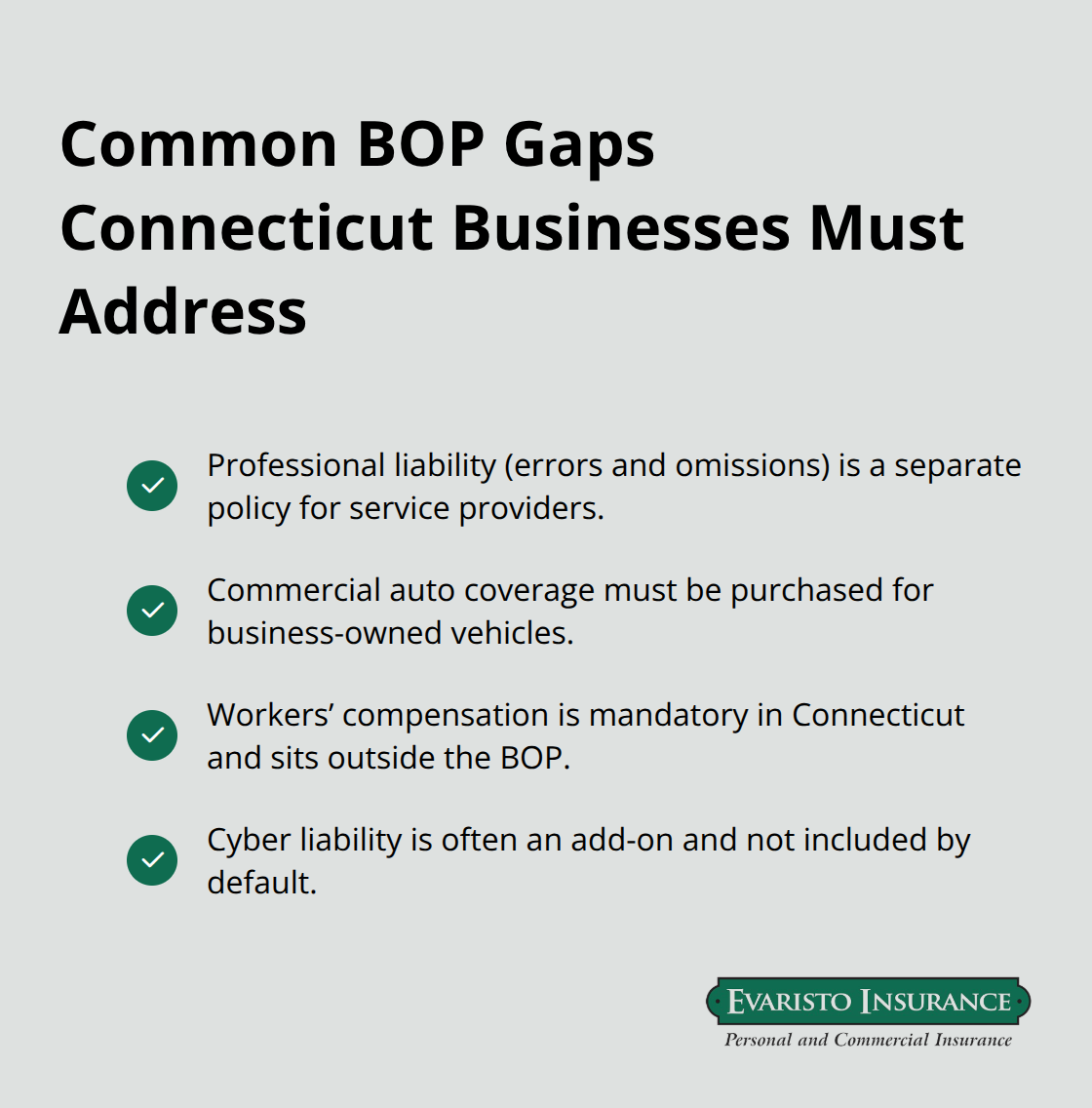

Standard BOP policies leave several exposures unprotected, and Connecticut businesses need to address these gaps intentionally. Professional liability (errors and omissions) sits outside the BOP for consultants, accountants, and service providers-a separate policy covers claims that your work harmed a client financially. Commercial auto coverage doesn’t come with your BOP; all business-owned vehicles require separate auto liability and physical damage insurance under Connecticut law. If your business has employees, workers’ compensation insurance is mandatory in Connecticut and must be purchased separately from your BOP. Cyber liability coverage (protecting against data breaches and network attacks) can be added to some BOPs but isn’t included by default, yet it matters increasingly for any business that stores customer information.

Understanding what your BOP doesn’t cover is just as important as knowing what it does, because gaps in protection can expose your business to catastrophic losses. The next section walks you through how to assess your specific business risks and select the right coverage limits and deductibles for your Connecticut operation.

What Each Part of Your BOP Actually Pays For

Property Coverage Protects Your Physical Assets

Property coverage protects the physical assets that keep your Connecticut business operating. If you own your building, this covers the structure itself plus everything inside-equipment, inventory, fixtures, tools, and furnishings. Renters get coverage for their business personal property and any improvements they’ve made to the leased space, but the landlord’s building structure stays their responsibility. The coverage limit you choose determines your maximum payout, and this number matters enormously. Underestimating your property value creates a proportional penalty: if you insure $100,000 of equipment but actually own $150,000 worth, an insurance company calculates claims based on that underinsurance ratio, potentially paying only 67 cents on every dollar of loss. Connecticut businesses in flood-prone areas near rivers or coastal zones must add separate flood insurance since standard BOPs exclude water damage from rising water-a critical gap given the Northeast’s increasingly severe weather.

Liability Coverage Protects You From Third-Party Claims

Liability coverage within your BOP protects you when someone gets injured at your business or when your operations damage someone else’s property. A customer slips on a wet floor and breaks their arm; your liability coverage pays their medical bills and any judgment if they sue. Your contractor accidentally damages a client’s equipment during a job; liability covers the repair costs and legal defense. General liability doesn’t cover your own employees-that’s workers’ compensation, purchased separately. Connecticut requires all businesses with employees to carry workers’ comp, so this remains outside your BOP regardless of how comprehensive your policy is. Most Connecticut small business owners select $1 million per occurrence and $2 million aggregate limits, though higher-risk industries like restaurants and retail shops benefit from $2 million per occurrence limits given their exposure to customer injuries.

Business Interruption Coverage Replaces Lost Income

Business interruption coverage activates when a covered loss forces you to temporarily close or significantly reduce operations. This form of coverage assists in replacing lost income and paying ongoing expenses like payroll, rent, loan payments, and utilities. Without this protection, you pay employees and landlords from your personal reserves while generating zero revenue-a situation that bankrupts many small businesses within weeks. The Hartford’s data shows average BOP customers pay approximately $1,687 annually for their full bundled coverage, which translates to roughly $141 monthly, making business interruption protection financially accessible for most Connecticut operations.

Deductibles and Premiums Vary by Risk

Your deductible choice significantly affects both your premium and your actual protection. Selecting a $500 deductible costs less monthly than a $250 deductible, but you must be able to afford that $500 out of pocket when a loss occurs-choosing too high a deductible leaves you unable to pay it when needed. Industry and location shape what you’ll actually pay for these coverages. Insureon’s data from their customer base shows dine-in restaurants, retail shops, and auto repair facilities typically pay $131 to $190 monthly for complete BOP coverage, while low-interaction professional services like consulting pay around $55 monthly. Older Connecticut buildings and higher-crime neighborhoods increase premiums substantially, as do businesses with higher employee counts. The property value you’re insuring and whether you choose replacement cost or actual cash value coverage also drive your final premium-replacement cost coverage costs more but pays you enough to actually replace damaged items at current market prices rather than depreciated values.

Understanding these cost drivers helps you make informed decisions about which coverage limits and deductibles align with your business’s financial situation and risk tolerance, setting the stage for selecting the right BOP for your specific Connecticut operation.

Matching Your BOP to Your Connecticut Business Reality

Calculate Your Actual Property Value

Start with your actual property value, not what you think it might be worth. Walk through your business location and inventory with a notepad or spreadsheet, listing every asset that keeps your operation running: equipment, tools, inventory, fixtures, furniture, computers, and signage. Don’t estimate-measure and price. If you own a restaurant, count every piece of kitchen equipment, every table and chair, your POS system, and your full food inventory. If you run a retail shop, photograph and catalog merchandise by category, then price it at replacement cost, not what you paid for it three years ago. This number becomes your property coverage limit. Underinsuring creates claim penalties that can devastate your recovery after a loss.

Match Liability Limits to Your Industry and Location

Your industry and location determine your liability and business interruption needs. If you operate a dine-in restaurant, retail shop, or auto repair facility, Insureon’s data covering roughly 100,000 small business policyholders shows you’ll pay $131 to $190 monthly for complete BOP coverage, reflecting your higher exposure to customer injuries and property damage claims. Professional services like consulting cost around $55 monthly because your interaction with customers creates far less physical risk. Connecticut’s older building stock matters too: a 1950s commercial building with original electrical systems costs more to insure than a 1990s structure, and businesses in Hartford or Waterbury neighborhoods with higher crime rates pay more than suburban operations. Most Connecticut small business owners select $1 million per occurrence and $2 million aggregate liability limits according to Insureon customer data, but restaurants and retail shops with constant customer traffic benefit from $2 million per occurrence limits given their actual loss exposure.

Set Your Deductible Based on Cash Reserves

Your deductible choice requires honest assessment of your emergency cash reserves. Choosing a $500 deductible instead of $250 saves roughly $10 to $20 monthly, but only if you can actually write a $500 check when a loss happens. Selecting too high a deductible leaves you unable to pay it when needed, defeating the entire purpose of insurance.

Work with a Connecticut Insurance Professional

An independent agent can quote your specific business across several insurers, showing you meaningful price differences and coverage variations that captive agents representing a single company cannot offer. When you meet with an agent, bring your property inventory list, your revenue figures, your employee count, and details about your building’s age and construction. Ask specifically what gaps exist between your BOP and your actual exposures: Does your professional liability sit outside the policy? Do you need cyber coverage? What about commercial auto if you operate business vehicles? A thorough agent identifies these gaps upfront rather than discovering them after a claim. Verify that any agent and insurer you work with holds current Connecticut licensing through the Connecticut Department of Insurance, protecting you from unlicensed operators and ensuring financial stability. Ask about the insurer’s financial strength ratings from established agencies before binding coverage-you want an insurer that will actually pay claims when losses occur, not one facing financial difficulty.

Review Your Coverage Annually

Plan to review your BOP annually as your business changes: when you hire your first employee, when you expand your inventory, when you add a second location, or when you invest in new equipment, your coverage limits may no longer match your actual exposures.

Final Thoughts

A Business Owners Policy protects what you’ve built and keeps your operation running when unexpected events strike. Connecticut’s specific environment-from aging commercial buildings to coastal flood risk to higher-crime urban neighborhoods-demands insurance that reflects local reality rather than generic national templates. Your BOP coverage Connecticut addresses the actual losses that close businesses permanently: property damage, liability claims, and lost income during forced closures.

Pull your existing policy this week and compare your property limits against your actual asset inventory, your liability limits against your industry’s typical claim exposure, and your deductible against your emergency cash reserves. If you’ve hired employees since your last review, added equipment, expanded inventory, or moved locations, your coverage limits likely no longer match your actual business. Annual reviews catch these misalignments before losses expose them.

An independent agent can show you pricing across multiple carriers, identify coverage gaps specific to your operation, and explain exactly what your premium includes and excludes. We at Evaristo Insurance have served Connecticut businesses since 1989 as a family-owned independent agency with local offices in Ellington and West Hartford, comparing multiple top carriers to deliver tailored protection and competitive pricing. Contact us today to discuss your specific business risks and get a quote that reflects your actual exposures and budget.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.