Builder Liability Insurance CT: What Builders Need to Know

One lawsuit can wipe out years of profit. We at Evaristo Insurance see builders in Connecticut face serious financial exposure every single day, which is why builder liability insurance in CT isn’t optional-it’s survival.

Your clients demand it, Connecticut’s construction standards require it, and one property damage claim or bodily injury lawsuit will prove why you need it.

What Builder Liability Insurance Actually Covers

Property Damage Claims

Builder liability insurance protects you against the three categories of claims that can destroy a contracting business: property damage, bodily injury, and the legal costs that follow. Property damage claims arise when your work or your crew damages a client’s existing structure, their belongings, or neighboring properties. A misplaced nail that punctures a water line, a dropped tool that cracks a skylight, or debris that damages a neighbor’s roof-these incidents require immediate financial responsibility. The Hartford, a major commercial insurer, notes that general liability policies typically cover these incidents up to your selected limit, which is why Connecticut builders need coverage well above the state minimum. Many contractors mistakenly think minimal coverage is adequate, but a single water damage claim from faulty installation can easily exceed $50,000 to $100,000.

Bodily Injury Claims

Bodily injury claims cover medical expenses, lost wages, and legal judgments when someone is hurt because of your work. This includes injuries to your crew, clients, or third parties at the job site. If a homeowner trips on a loose board you left unsecured and breaks their leg, or if a passerby is struck by falling materials, bodily injury coverage pays the medical bills and any settlement or judgment. These claims often carry the highest financial exposure because medical costs and pain-and-suffering awards can reach hundreds of thousands of dollars on a single incident.

Legal Defense Costs

Legal defense costs represent the most underestimated protection builders need. Hartford reports that even winning a lawsuit costs $25,000 to $50,000 in attorney fees and court costs before the case is resolved. Your builder liability policy covers these defense expenses regardless of whether you’re found liable, which means you’re protected from the moment a claim is filed. This protection alone justifies the annual premium investment.

Coverage Limits That Match Your Work

Coverage limits matter enormously-a $1 million policy is standard for most residential contractors, but commercial projects or high-value renovations often require $2 million or more. Your specific project types, client base, and contract requirements determine the right limit for your business. A local agent who understands Connecticut construction standards can assess your exposure and recommend appropriate coverage. The difference between adequate protection and financial disaster often comes down to selecting the right limit before a claim happens.

Why Builder Liability Insurance Matters in Connecticut

Connecticut’s Legal Requirements for Contractors

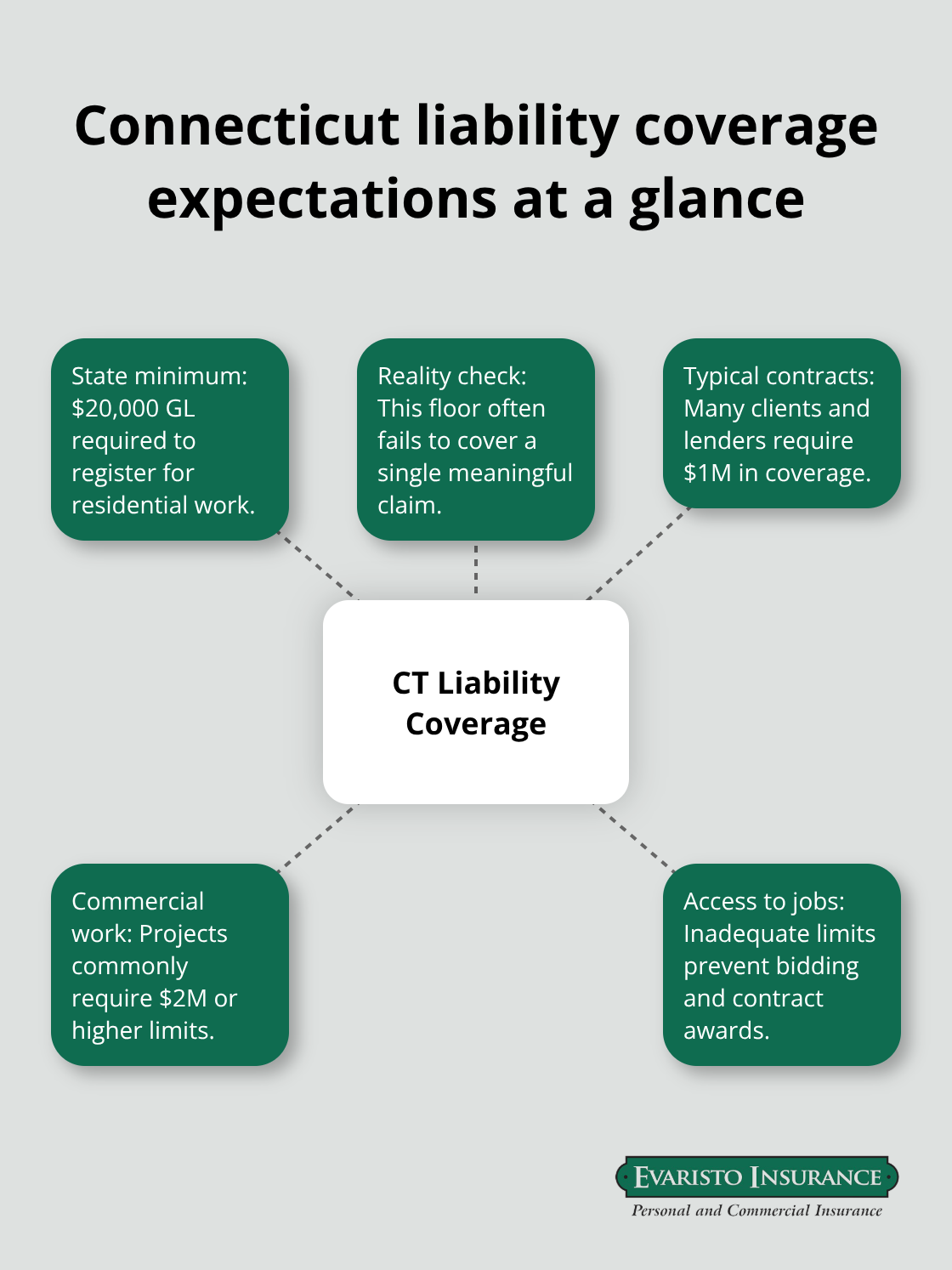

Connecticut’s Department of Consumer Protection mandates that home improvement contractors register and maintain general liability insurance with a minimum of $20,000 in coverage before they can legally contract on residential property. This $20,000 floor exists, but it fails to protect you adequately. A single property damage claim routinely exceeds this amount, leaving you personally liable for the difference. Most legitimate clients and lenders demand $1 million in coverage as a contract requirement, and many commercial projects require $2 million or higher.

Without adequate coverage, you cannot bid on jobs, satisfy client requirements, or shield yourself from the financial devastation a lawsuit creates.

What Clients and Contracts Actually Require

Connecticut’s construction market has become increasingly litigation-conscious, with homeowners and commercial property owners more likely to pursue claims for defects, delays, or damage. General contractors often demand that subcontractors carry their own liability insurance naming the general contractor as an additional insured. Without builder liability insurance, you cannot meet these contractual obligations, which means you lose bids and projects to competitors who maintain proper coverage. Clients increasingly require proof of current coverage before signing contracts, and this expectation has become standard practice across residential and commercial work.

The Real Cost of Claims Without Coverage

Connecticut contractors face claims ranging from $50,000 for property damage to over $500,000 for serious bodily injury incidents. Legal defense costs alone run $25,000 to $50,000 before a case concludes, and your liability policy covers these expenses regardless of fault. One lawsuit without proper coverage does not just cost you the settlement amount-it costs your business its reputation, your ability to secure future contracts, and potentially your personal assets if a judgment exceeds your policy limits. The financial reality is stark: operating without adequate liability insurance exposes you to catastrophic loss.

Why Coverage Gaps Leave You Vulnerable

Connecticut’s strict contractor registration rules, combined with client expectations and the state’s litigation environment, make liability insurance non-negotiable. The question is not whether you can afford insurance-it is whether you can afford to operate without it. Your next step involves selecting the right coverage limits and finding an agent who understands Connecticut’s construction landscape and your specific project risks.

How to Choose the Right Builder Liability Coverage

Assess Your Project Types and Risk Exposure

Start by mapping what you actually build. A contractor handling $50,000 kitchen renovations faces completely different risk than one managing $500,000 commercial builds or high-end waterfront properties. Your project size, complexity, and location determine your exposure and the coverage limits you need. A $1 million general liability policy works for most residential contractors in Connecticut, but if you regularly handle commercial projects, multi-unit renovations, or work near water or utilities, you need $2 million minimum. The Hartford reports that general liability insurance costs approximately $810 per year for small businesses on average, but this varies significantly based on your specific risk profile. Don’t assume the cheapest quote protects you adequately-the $600-per-year policy might carry limits that leave you personally liable for claims exceeding those thresholds. Assess whether your contracts require you to name clients or general contractors as additional insureds, because this affects your coverage structure and your premium. Many Connecticut builders lose jobs simply because they cannot prove adequate limits exist before signing contracts.

Compare Coverage Limits and Deductibles

Your deductible choice directly impacts both your premium and your cash flow. A $1,000 deductible costs less than a $500 deductible, but you pay that $1,000 out of pocket before coverage kicks in. Connecticut contractors handling multiple small projects should consider lower deductibles because small claims happen frequently and you cannot absorb the deductible cost repeatedly. For larger commercial work, a $2,500 or $5,000 deductible makes sense because claims tend to be bigger and less frequent. Coverage limits matter enormously-a $1 million policy is standard for most residential contractors, but commercial projects or high-value renovations often require $2 million or more. Your specific project types, client base, and contract requirements determine the right limit for your business. A local agent who understands Connecticut construction standards can assess your exposure and recommend appropriate coverage. The difference between adequate protection and financial disaster often comes down to selecting the right limit before a claim happens.

Work with a Local Agent Who Understands Connecticut Projects

A local agent understands Connecticut’s contractor registration requirements, client expectations, and the specific construction standards in your region. They know which carriers respond fastest to claims in Connecticut, which underwriters specialize in your type of work, and how to structure your policy so you meet contract requirements without overpaying for unnecessary coverage. An independent agency compares coverage from multiple carriers to match your actual project profile, risk exposure, and budget-not a one-size-fits-all template. This expertise matters more than shopping solely on price, because an agent who understands Connecticut construction can identify coverage gaps that a national quote system misses. They also help you navigate whether your contracts require additional insured endorsements, which affects both your premium and your protection structure. A knowledgeable local agent saves you money by eliminating unnecessary coverage while protecting you against the gaps that matter most.

Final Thoughts

Builder liability insurance in CT protects your business, satisfies your clients, and shields you from the financial devastation a single lawsuit creates. Connecticut’s construction market demands proof of adequate coverage before clients sign contracts, and one claim without proper protection will cost far more than years of premiums combined. Assess your actual project types, compare deductibles based on your claim frequency, and work with an agent who understands Connecticut’s specific construction standards.

We at Evaristo Insurance have served Connecticut builders since 1989 with tailored coverage that matches your actual project profile and risk exposure. Our independent agency compares multiple top carriers to deliver competitive pricing and hands-on advocacy when claims happen, with local offices in Ellington and West Hartford that understand your market. Stop settling for quotes from national carriers who do not understand Connecticut’s contractor landscape.

Contact Evaristo Insurance today to discuss your builder liability insurance needs and receive a quote that reflects your actual exposure. The right coverage lets you focus on what you do best: building quality work.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.