Connecticut Cyber Liability Quotes: Compare and Find the Right Policy

Connecticut businesses face growing cyber threats that can cripple operations and drain resources. Data breaches cost companies thousands in recovery, legal fees, and regulatory fines-expenses that cyber liability quotes in CT can help you prepare for.

At Evaristo Insurance, we help Connecticut business owners understand their coverage options and find policies that match their actual risk profile. This guide walks you through comparing policies, getting accurate quotes, and selecting the protection your business needs.

Why Your Connecticut Business Is a Target

Connecticut’s High-Risk Industries Attract Hackers

Connecticut’s economy runs on finance, healthcare, manufacturing, and insurance-sectors that hackers actively pursue. Businesses in these industries store sensitive customer data, making them lucrative targets. Small and mid-sized companies face particular risk because they typically have weaker cybersecurity defenses than larger enterprises, yet they handle just as much valuable information. A 2024 trend shows attackers increasingly focusing on Connecticut’s smaller firms, betting they’ll pay ransoms faster or lack the resources to defend themselves effectively.

The Real Cost of a Breach in Connecticut

A single data breach in Connecticut can exceed $1 million when you factor in forensics, legal fees, customer notifications, credit monitoring, and regulatory fines. The Ponemon Institute reports the average cost of a data breach in the United States is around $8.19 million, but Connecticut businesses often face compounded expenses because state law requires notification to affected residents and the Connecticut Attorney General within 60 days of discovery. If your breach involves Social Security numbers or tax IDs, you must also provide 24 months of free identity theft protection services. These mandatory expenses exist regardless of whether your traditional business insurance covers them-and it typically doesn’t. Small businesses paying $1,000 to $7,500 annually for $1 million in cyber liability coverage often view this as inexpensive compared to the real costs they’d face without it.

Connecticut’s Strict Notification Laws Demand Preparation

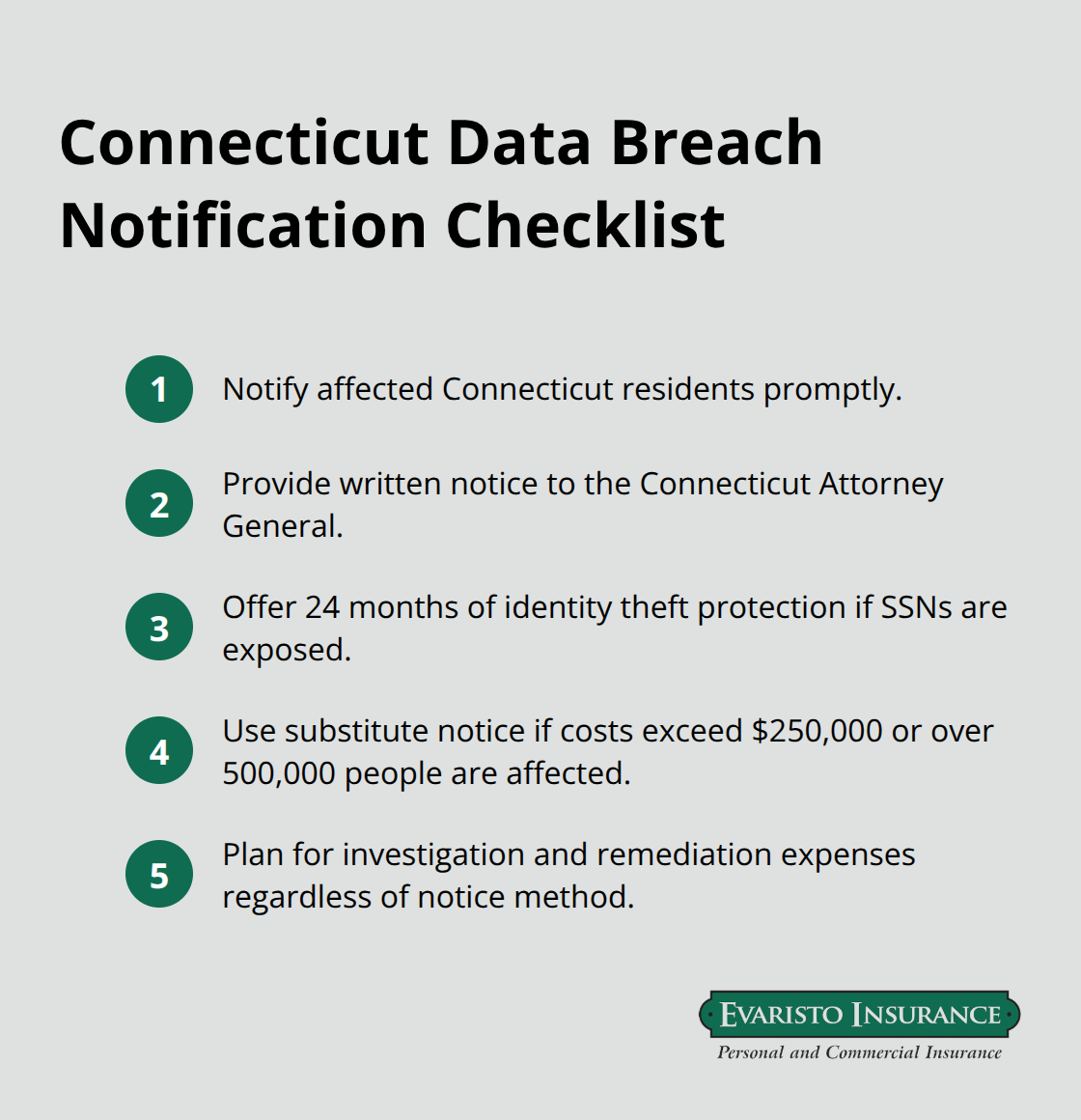

Connecticut General Statute 36a-701b defines personal information broadly to include names paired with Social Security numbers, driver’s license numbers, financial account credentials, medical records, health insurance IDs, biometric data, precise geolocation, and online account passwords. A security breach occurs when unauthorized parties access this data without encryption or other protective measures. Your business must notify affected Connecticut residents, provide written notice to the Attorney General, and offer identity theft services if SSNs are exposed. If notification costs exceed $250,000 or affect more than 500,000 people, you can use substitute notice through email, website posting, or major media outlets-but you still face the underlying investigation and remediation expenses. Cyber liability insurance covers these notification costs, forensic investigations, and legal defense, making it essential for any Connecticut business that handles customer data.

What Happens When You Don’t Have Coverage

Without cyber liability insurance, your business absorbs every dollar of breach response on its own. You’ll pay forensic experts to investigate the incident, hire lawyers to navigate Connecticut’s notification requirements, and fund the credit monitoring services you’re legally obligated to provide. The Connecticut Attorney General can seek direct damages and injunctive relief for noncompliance with notification laws, adding potential penalties to your costs. These expenses hit your cash flow immediately, often before you’ve even determined the breach’s full scope. The right cyber liability policy transfers these financial burdens to your insurer, allowing you to focus on restoring operations and protecting your reputation.

Understanding what your business stands to lose sets the stage for evaluating the specific coverage options available to you.

What Coverage Actually Protects Your Business

First-Party and Third-Party Coverage Work Together

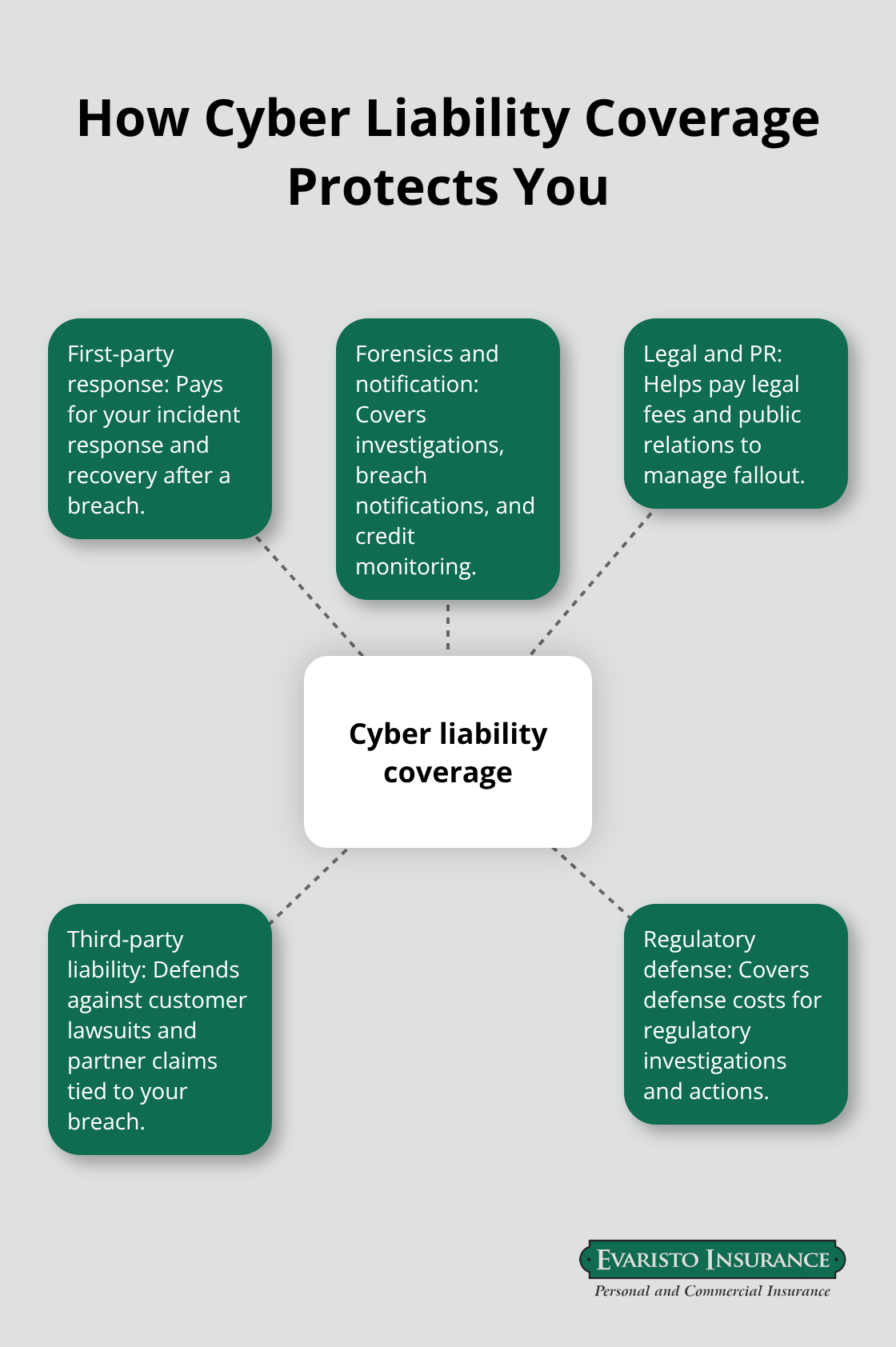

Connecticut cyber liability policies split into two critical categories: first-party coverage that pays for your own incident response and recovery, and third-party coverage that defends you against customer lawsuits and regulatory claims. First-party benefits reimburse forensic investigations, breach notification costs, credit monitoring services, legal fees, and public relations expenses-the direct costs you face after a breach. Third-party coverage handles claims from customers whose data was compromised, defense costs against regulatory investigations, and liability to business partners affected by your breach.

Most Connecticut businesses need both to avoid gaps in protection.

Selecting Limits and Deductibles That Match Your Business

A $1 million combined limit works for many small to mid-sized firms, but healthcare providers and financial services companies handling sensitive regulated data typically require $2 million to $5 million in coverage. Deductibles commonly range from $2,500 to $50,000, and here’s the practical reality: higher deductibles lower your premium but mean you absorb more of the initial breach response costs yourself. Try a deductible you can actually pay out of pocket without destabilizing cash flow. Deductible choice and rider selection drive price far more than base limits do, so prioritize the coverages that match your actual operations rather than accepting defaults.

Specialized Riders Expand Your Protection

Ransomware extortion riders are now standard offerings from most carriers and cover ransom negotiations and sometimes partial ransom payments. Business interruption coverage covers income loss after a privacy or security breach impacts your business. Technology service provider liability protects you when breaches happen because your cloud provider, SaaS vendor, or IT partner fails to secure data, shifting some risk to carriers who can pursue those vendors.

Connecticut’s Regulatory Requirements Shape Your Coverage

Connecticut regulations add complexity: policies must explicitly cover your legal obligation to notify residents and the Attorney General, provide 24 months of identity theft protection when Social Security numbers are exposed, and handle substitute notice requirements if breach costs exceed $250,000. Carriers offering 10 to 25 percent premium discounts for strong security measures (multi-factor authentication, endpoint protection, employee training, and documented incident response plans) make cyber insurance more affordable while incentivizing actual risk reduction. These discounts reward businesses that take security seriously and reduce the likelihood of claims.

When you understand what coverage options exist and how they align with Connecticut’s legal landscape, you’re ready to move forward with gathering the information carriers need to provide accurate quotes tailored to your business.

How to Get Accurate Cyber Liability Quotes in Connecticut

Document Your Data and Operations

Carriers won’t provide meaningful quotes without understanding your actual data environment and operational risk. Start by documenting what personal information your business stores-customer names paired with Social Security numbers, payment card data, health records, employee information, or combinations of these. Specify where this data lives: on-premise servers, cloud platforms like AWS or Microsoft Azure, or a hybrid setup. List your critical business systems and how long your operations can survive if they go offline. A manufacturer losing production for 48 hours faces different financial exposure than a consulting firm with flexible remote work.

Inventory Your Security Controls

Next, catalog your current security controls: multi-factor authentication across all user accounts, endpoint detection software on devices, annual employee security training, or formal incident response plans. Carriers offering 10 to 25 percent premium discounts want proof of these controls, so gather documentation showing implementation dates and scope. Include any prior security incidents, even minor ones, because carriers ask about breach history and will uncover them anyway. Document your industry compliance obligations-HIPAA for healthcare, PCI-DSS for payment processing, GLBA for financial services-since these requirements directly shape coverage needs and pricing.

Set Your Budget and Gather Compliance Details

Establish a budget range for annual premiums before requesting quotes. Knowing you can spend $3,000 to $5,000 yearly helps agents narrow carrier options rather than wasting time on quotes outside your comfort zone. This step accelerates the process and focuses attention on realistic options for your business.

Request Quotes from Multiple Carriers Simultaneously

The comparison process works best when you request quotes from multiple carriers simultaneously using identical information, so differences in pricing and terms reflect actual policy variations rather than how you described your business to each one. Try obtaining quotes from at least three carriers to see meaningful variation in deductibles, riders, and premium costs for identical coverage limits. When quotes arrive, don’t focus only on annual premium-compare the total out-of-pocket exposure by adding the deductible to the premium, then evaluate what each policy actually covers. One carrier might offer $1 million coverage with a $5,000 deductible at $2,800 annually, while another quotes $1 million with a $10,000 deductible at $2,200 annually. The second policy saves $600 per year but costs you an extra $5,000 if a breach occurs.

Work with a Local Independent Agent

An independent agent who represents 15 or more A-rated carriers gives you access to options you won’t find shopping online alone. The agent asks discovery questions about your operations, runs your profile through carrier underwriting systems, and returns quotes tailored to your actual risk rather than generic template answers. Local agents in Connecticut understand state-specific notification laws and which carriers excel at handling breach response in your region, saving you from learning these lessons during an actual incident.

Final Thoughts

Cyber liability quotes in Connecticut reveal a straightforward truth: the cost of insurance runs far smaller than the cost of a breach. A $1 million policy at $1,000 to $7,500 annually protects your business against expenses that routinely exceed $1 million when forensics, legal fees, notifications, and regulatory fines combine. Connecticut’s strict data breach laws make this protection non-negotiable for any business that handles customer information.

The right policy matches your actual data environment, security controls, and compliance obligations rather than accepting generic coverage. You now understand what first-party and third-party coverage accomplish, how deductibles and riders shape your real out-of-pocket exposure, and why Connecticut’s notification requirements demand specific policy language. Document your data, inventory your security controls, and request cyber liability quotes from multiple carriers simultaneously to receive quotes tailored to your business rather than estimates based on incomplete information.

We at Evaristo Insurance have guided Connecticut business owners through this process for decades. Our local offices work with multiple top carriers to find cyber liability coverage that fits your operations and budget, and we contact you to discuss your cyber liability needs and provide quotes that reflect your actual risk profile.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.