Connecticut Home Insurance Costs: Budgeting Your Premiums

Connecticut homeowners face rising insurance costs, and understanding what drives your premiums is the first step toward smarter budgeting.

We at Evaristo Insurance know that Connecticut home insurance costs vary widely based on location, home characteristics, and coverage choices. This guide walks you through the factors affecting your rates, proven ways to reduce them, and current pricing trends across the state.

What Drives Your Connecticut Home Insurance Costs

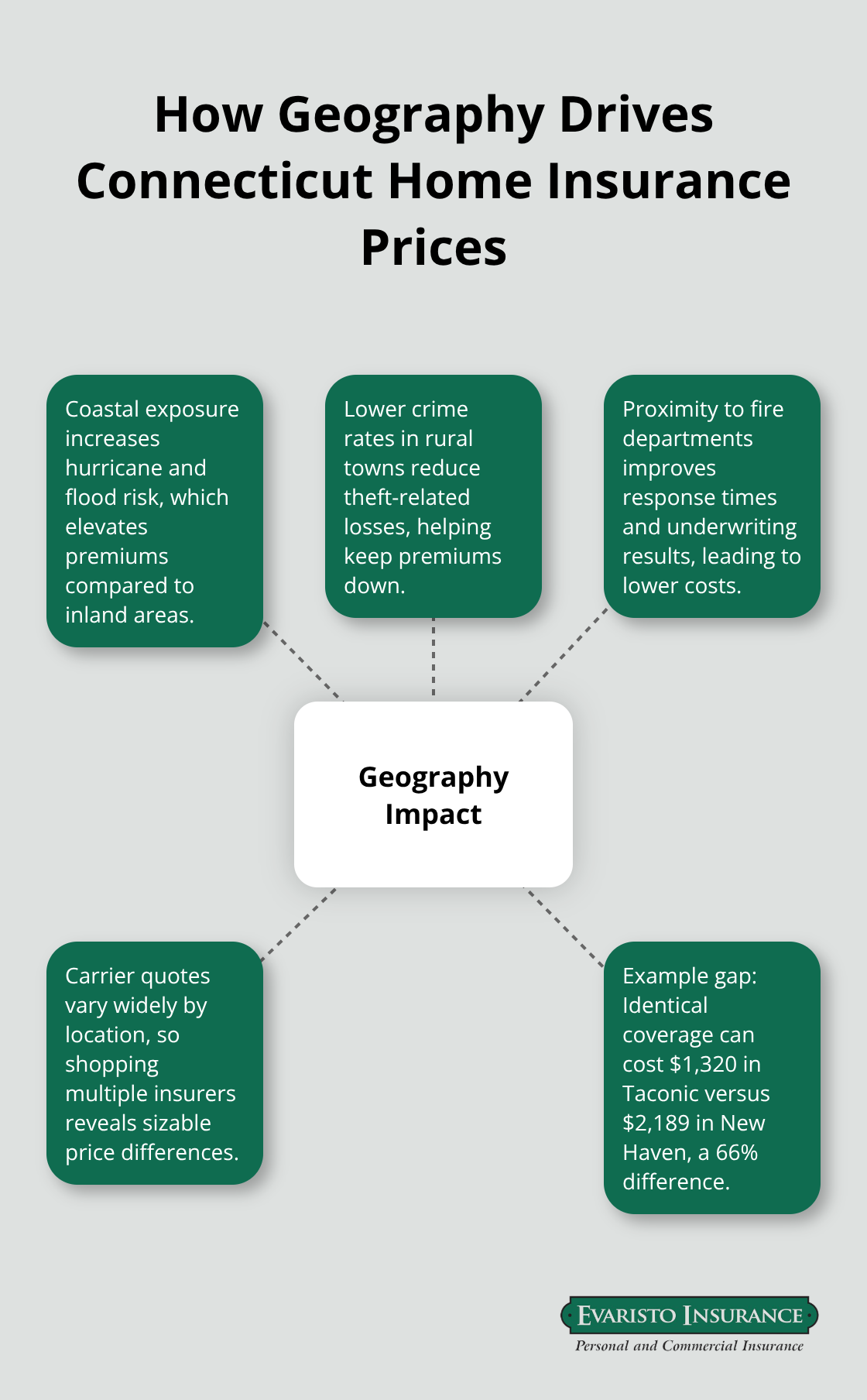

Your Connecticut home insurance premium reflects specific measurable risks that insurers evaluate before quoting you a rate. Location matters dramatically in Connecticut. Coastal properties and towns near water face substantially higher premiums due to hurricane and flood exposure. New Haven homeowners pay around $2,189 annually for $300,000 in dwelling coverage, while inland towns like Taconic average just $1,320, according to Quadrant Information Services data analyzed by Bankrate. Proximity to a fire station directly affects your rate, as does neighborhood crime data. Homes within five miles of a fire department qualify for lower premiums than those in remote areas.

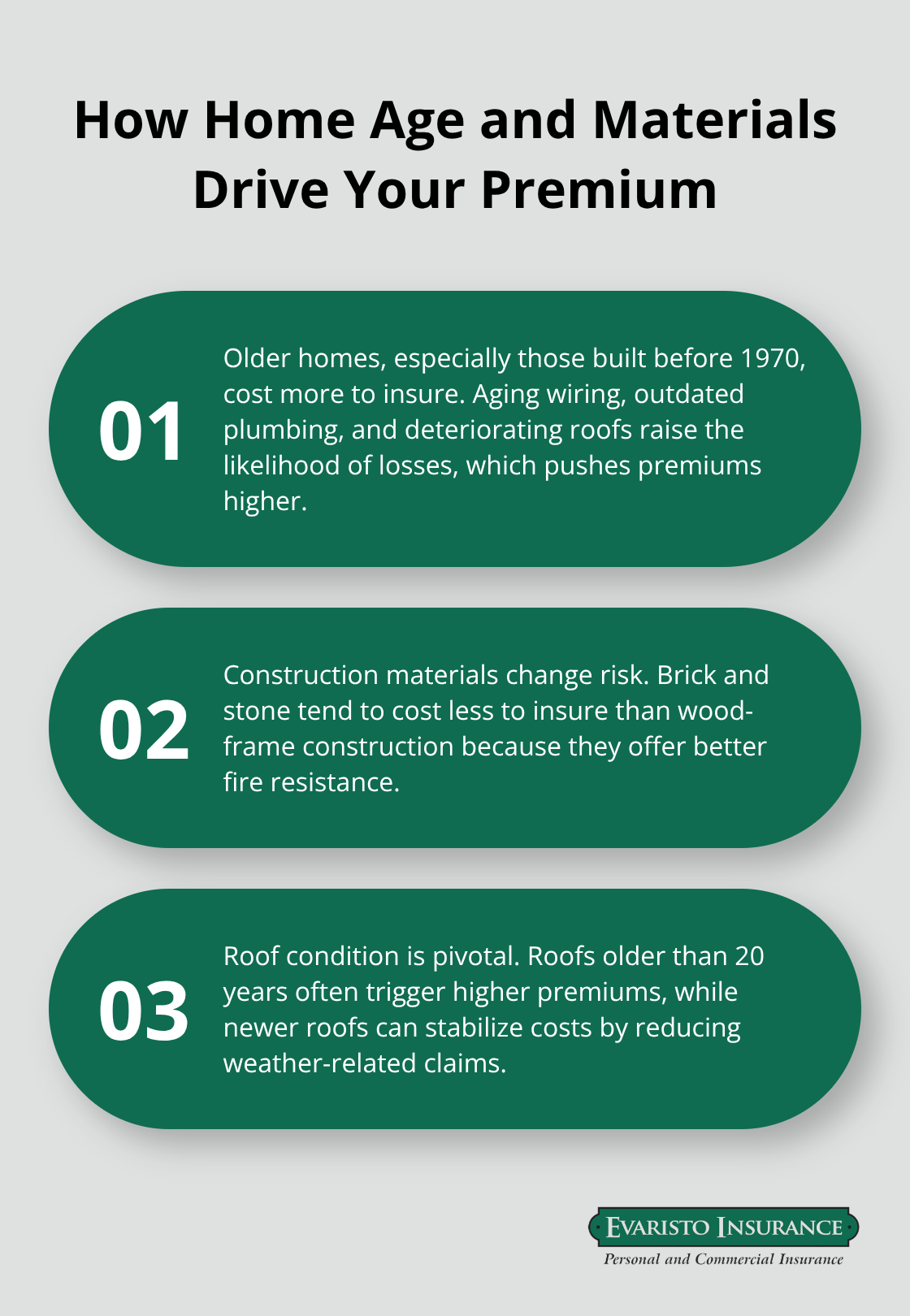

Home Age and Construction Materials Impact Your Rate

Your home’s age and construction materials are equally significant cost drivers. Older homes-particularly those built before 1970-cost substantially more to insure because aging wiring, outdated plumbing, and deteriorating roofs increase loss risk. The type of siding matters too: brick and stone homes typically cost less to insure than wood-frame construction due to better fire resistance.

Roof age is critical; a roof older than 20 years will push your premium higher, sometimes considerably. Home size affects the dwelling coverage amount you need, which directly correlates to your annual cost. A 1,500-square-foot home costs less to insure than a 3,500-square-foot property simply because replacement costs are lower.

How Coverage Limits and Deductibles Shape Your Premium

Your coverage limit decisions fundamentally determine your premium. You must insure a home to its actual replacement cost-underinsuring means you won’t recover fully after a loss, while overinsuring wastes money on unnecessary coverage. Standard Connecticut homeowners policies include dwelling coverage, personal property protection, liability, medical payments, loss of use, and other structures coverage. Adding endorsements like water backup coverage, valuable items protection, or equipment breakdown coverage increases your premium based on the additional risk you transfer to the insurer. Your deductible choice directly impacts cost: a $500 deductible costs more monthly than a $1,000 deductible, but you pay less out-of-pocket when filing a claim. Hurricane deductibles in Connecticut typically range from 2% to 5% of your home’s value and apply during official hurricane warnings.

Understanding these cost drivers positions you to make informed decisions about your coverage. The next section explores concrete strategies to lower what you pay without sacrificing the protection your home needs.

How to Cut Your Connecticut Home Insurance Costs

Bundle Your Policies for Immediate Savings

Bundling your homeowners and auto policies with one insurer typically saves Connecticut homeowners 10-20% on their combined premiums, according to data from major carriers operating in the state. If you currently split your policies between two companies, consolidating them can yield immediate savings without changing your coverage. State Farm, Amica, and Travelers all offer substantial multi-policy discounts in Connecticut, and comparing quotes from bundled packages across carriers takes roughly 15 minutes online. The math is straightforward: a homeowner paying $1,500 annually for home coverage and $1,200 for auto insurance could save $270-$540 per year simply by moving both policies to the same carrier. This approach also simplifies your billing, claim handling, and policy management since you’ll work with one agent and receive consolidated statements.

Upgrade Your Home’s Security and Safety Systems

Installing a monitored burglar alarm system typically earns a 5-10% discount on your homeowners premium, while smoke detectors, deadbolt locks, and fire extinguishers each qualify for smaller credits that add up. If your roof is older than 20 years, replacing it can lower your premium by 15-25% because new roofs significantly reduce weather-related damage claims. Similarly, updating electrical wiring in homes built before 1970 removes a major underwriting concern and opens the door to better rates.

These upgrades transform your home into a lower-risk property that insurers reward with better pricing.

Protect Your Claims History by Avoiding Small Claims

The key difference between paying claims and avoiding them entirely lies in your loss history. Connecticut homeowners who file multiple small claims within five years face premium increases of 10-25% at renewal, making it financially wise to self-insure minor damages under $1,500. If you suffer a covered loss worth less than three times your deductible, paying out-of-pocket prevents a claims record that would haunt your rates for years. Your claims history matters more than almost any other factor because it directly reflects your actual risk to the insurer, and a single avoided claim often pays for the deductible itself through avoided rate hikes at your next renewal.

Understanding these cost-reduction strategies positions you to take action on your current policy. The next section examines how Connecticut’s recent premium trends and regional pricing patterns affect what you’ll pay going forward.

Why Connecticut Home Insurance Premiums Keep Rising

Coastal Exposure Drives Statewide Rate Increases

Connecticut homeowners have experienced significant premium increases since 2020, driven primarily by coastal flooding and windstorm exposure that insurers now price more aggressively. According to the U.S. Treasury’s Federal Insurance Office, average homeowners insurance costs across the nation reached approximately $1,663 annually between 2018 and 2022, but Connecticut’s coastal concentration has accelerated rate adjustments beyond historical norms. Insurers are fundamentally reevaluating their underwriting criteria for Connecticut properties, which means availability tightens and pricing shifts upward regardless of individual home improvements you’ve made. If your home sits within 10 miles of the Connecticut coast, expect your renewal quotes to reflect intensifying weather risk assessments that weren’t factored into premiums five years ago.

This trend will likely continue because climate data shows increasing hurricane frequency and intensity, giving insurers legitimate actuarial reasons to raise rates. Coastal towns like New Haven, Old Saybrook, Clinton, Westbrook, and Niantic now rank among Connecticut’s most expensive insurance markets, with annual premiums for $300,000 in dwelling coverage ranging from $2,029 to $2,189 according to Quadrant Information Services data. Inland properties in towns like Taconic, Staffordville, Scotland, and Somersville cost substantially less, averaging $1,320 to $1,340 annually for identical coverage, creating a pricing gap exceeding $800 per year between coastal and rural properties.

Weather Events Trigger Individual Rate Adjustments

Weather events directly determine whether your individual renewal rate increases or decreases within this broader upward trend. A single hurricane warning that activates your 2-5% hurricane deductible teaches insurers that your specific neighborhood experiences actual loss activity, which translates to higher quotes at renewal even if your claim was modest. Connecticut homeowners in urban areas like Hartford, New Haven, and Bridgeport face compounding cost pressure from both weather exposure and theft-related losses that rural properties avoid entirely.

Geography Creates Dramatic Price Differences

Rural and inland towns experience lower premiums because they avoid hurricane risk, maintain lower crime rates, and typically offer better fire department proximity-creating a triple advantage in underwriting costs. If you’re shopping for coverage or renewing soon, requesting quotes from multiple carriers simultaneously reveals how dramatically your location influences pricing. A homeowner in Taconic might pay $1,320 with one carrier while an identical home in New Haven costs $2,189 with the same company, a 66% difference driven entirely by geography and weather exposure.

Final Thoughts

Connecticut home insurance costs reflect measurable risks that you can influence through informed decisions and strategic action. Location, home age, coverage limits, and deductible choices form the foundation of what you pay annually, while bundling policies, upgrading safety features, and protecting your claims history deliver concrete savings that compound over time. Connecticut’s rising premiums driven by coastal exposure make these cost-reduction strategies more valuable than ever, particularly if you live within 10 miles of the coast or in high-crime urban areas.

Your next step requires gathering quotes from multiple carriers using identical coverage amounts and deductibles, then comparing the actual numbers side by side. Don’t assume your current insurer offers the best rate-Connecticut’s pricing spreads between carriers often exceed $500 annually for identical homes. Request quotes that include all available discounts for bundling, safety devices, and claims-free history so you see your true cost after savings apply.

We at Evaristo Insurance serve Connecticut families and businesses with direct access to agents who understand your specific risks, from coastal hurricane exposure to inland weather patterns. Rather than navigating carrier websites alone, working with an independent agency means we advocate for your interests by shopping your coverage across multiple insurers simultaneously. Contact Evaristo Insurance to discuss your Connecticut home insurance needs with local experts who know your market inside and out.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.