Connecticut Homeowners Insurance Tips: Save More Without Sacrificing Coverage

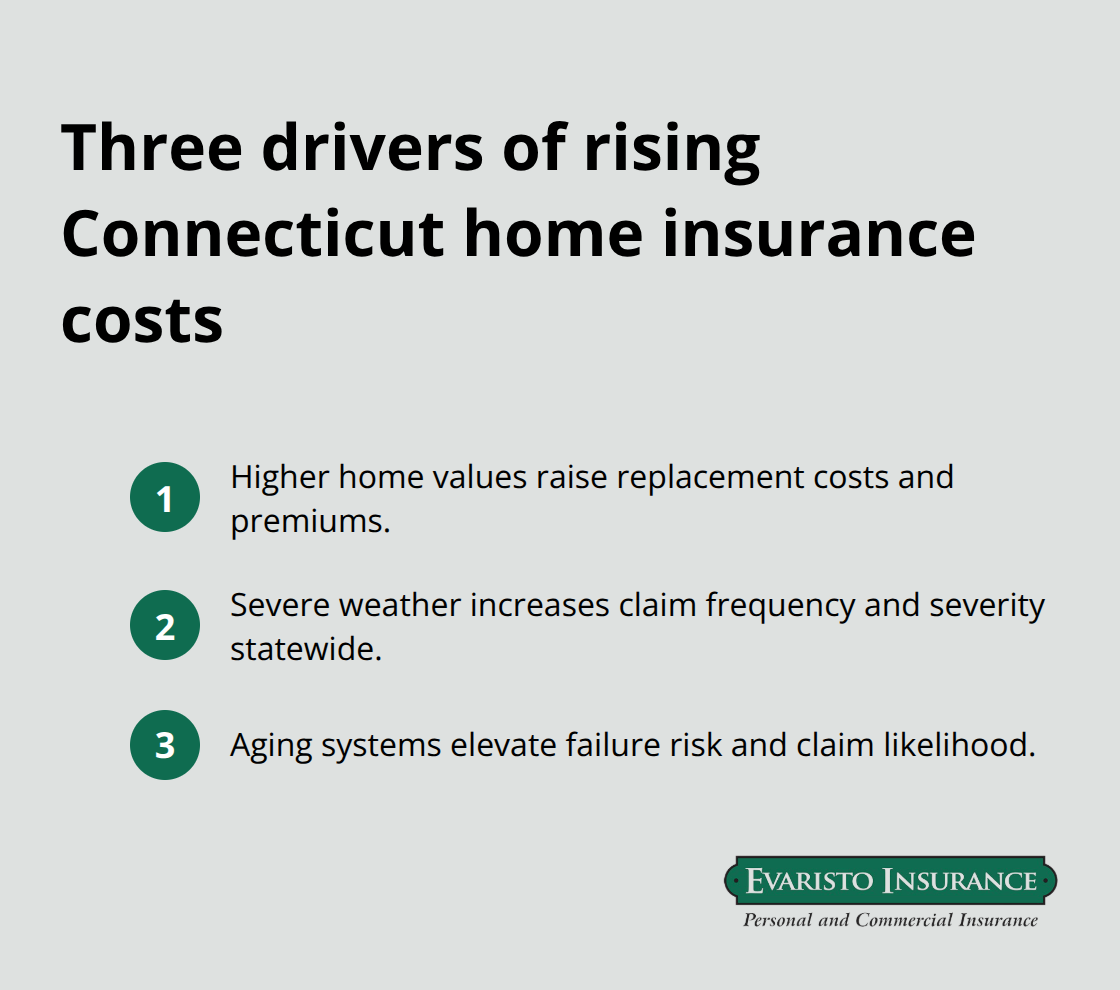

Connecticut homeowners are watching their insurance premiums climb faster than ever. Rising home values, severe weather patterns, and aging home systems are pushing costs up across the state.

We at Evaristo Insurance know that paying more doesn’t mean you need less coverage. This guide shares concrete Connecticut homeowners insurance tips to reduce what you pay while keeping your home fully protected.

Why Your Connecticut Home Insurance Costs Keep Rising

Home values drive your premium upward

Home values across Connecticut have climbed steadily, and your insurance costs reflect that reality. In Fairfield County, homeowners pay an average of about $2,225 per year for coverage, while Hartford County averages around $1,721 annually and New Haven County sits near $1,881. Insurers calculate premiums based on what it would cost to rebuild your home from scratch. When your home’s replacement cost increases, your premium follows. A $50,000 jump in your property’s value translates directly into higher coverage limits needed and higher premiums to match. This isn’t negotiable-underinsuring creates serious risk, so higher home values mean higher costs unless you actively adjust your coverage strategy.

Weather patterns drive claim frequency and costs

Connecticut’s coastal proximity and winter severity create genuine exposure that insurers price accordingly. The Atlantic tropical storm season runs from June 1 through November 30, and this window alone generates significant claims activity. Winter weather compounds the problem-ice dams, heavy snow loads, and freeze-thaw cycles damage roofs and pipes at scale across the state. Homes farther from the coast still face wind and storm damage, while coastal properties contend with hurricane deductibles that can run 5 percent or higher of your dwelling coverage. Insurers have responded to increased claim frequency with rate increases, and this trend shows no signs of reversing. Your premium reflects Connecticut’s actual weather risk, not theoretical risk.

Aging home systems cost more to insure

A home built in 1985 costs significantly more to insure than one built in 2015, and your insurer knows this. Older electrical systems, plumbing, roofing materials, and HVAC equipment fail more often, triggering water damage and fire claims. Insurers specifically underwrite homes on roof age, wiring type, and heating system condition because these directly predict losses. A roof that’s 20 years old presents real risk-ice dam damage, wind damage, and general deterioration are measurable problems. If your home has original plumbing from the 1980s or earlier, water damage claims become more likely, and your premium reflects that exposure. Upgrading these systems costs money upfront, but it’s one of the few ways to actually reduce your insurance costs rather than simply accept them.

Understanding these three cost drivers sets the stage for what comes next: concrete strategies that actually lower your premiums without leaving your home exposed.

How to Actually Lower Your Premiums Without Cutting Coverage

Bundle auto and home policies for substantial savings

Consolidating your auto and home policies with one insurer cuts your total premium significantly. Insurers offer bundling discounts that typically range from 10 to 25 percent depending on the carrier and your profile. If you currently split auto coverage from one company and home coverage from another, consolidating saves real money each month. Contact your current auto insurer first to request a home quote, then shop that quote against standalone home policies from other carriers. The bundled rate often beats the standalone price even before discounts apply. This matters because you reduce the cost of both policies simultaneously rather than paying separate premiums to multiple companies.

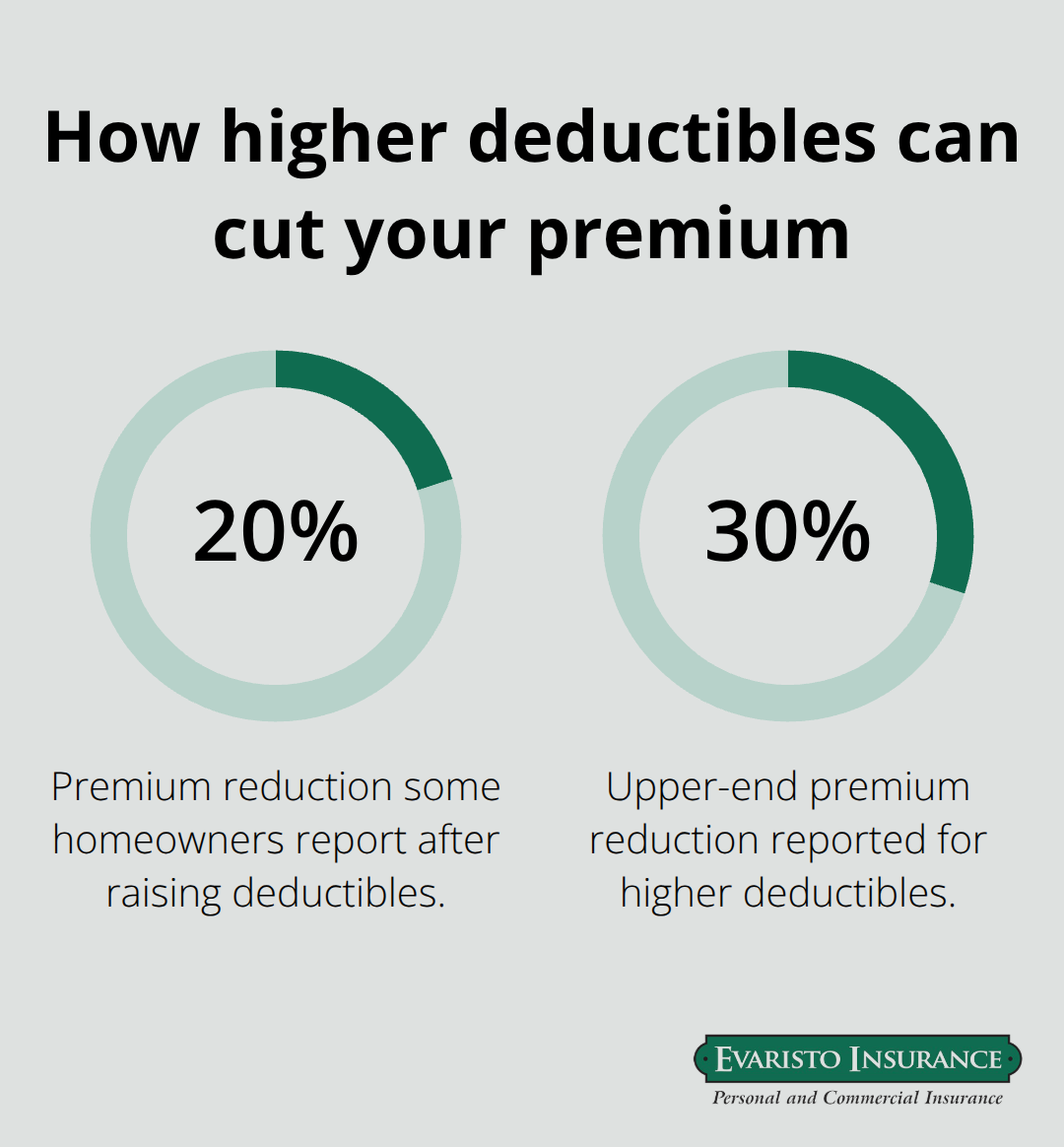

Increase your deductible strategically to lower monthly costs

Your deductible choice directly controls your premium, and higher deductibles produce meaningful savings. A $1,000 deductible costs substantially less than a $500 deductible on the same coverage. Some Connecticut homeowners raise their deductibles to $2,500 or $5,000 and see 20 to 30 percent premium reductions. The critical rule is simple: only increase your deductible if you can actually pay it from your own funds after a loss.

A $5,000 deductible saves money only if you have $5,000 in accessible savings. Don’t create a situation where you can’t afford to file a claim because the deductible exceeds your available cash.

Wind and hail deductibles operate separately from your standard deductible and can be flat amounts or percentages of your dwelling limit, typically ranging from 1 to 5 percent. Hurricane deductibles are even higher and apply only during hurricane warning periods as defined by the National Hurricane Center. Understanding these separate deductibles prevents surprises when you file a claim during storm season.

Install monitored safety devices to reduce risk and premiums

Monitored fire and smoke detectors, sprinkler systems, and centrally monitored security systems generate immediate premium discounts from most Connecticut carriers. These investments lower claims frequency and severity simultaneously. Water leak sensors represent newer technology that detects pipe failures before they cause thousands in damage, and insurers reward these installations with rate reductions. A $300 water sensor that prevents a $15,000 claim pays for itself instantly. Document every safety improvement you make and notify your insurer in writing, as some discounts require proof of installation. Coastal homeowners installing storm shutters also qualify for premium reductions while simultaneously protecting their properties during hurricane season.

Upgrade home systems to improve insurability and reduce costs

A roof replacement generates one of the largest premium discounts available. Notify your insurer immediately after roof work completion with documentation from your contractor. New roofs resist wind damage, ice dams, and weather deterioration far better than aging ones, and insurers price this reduced risk directly into your premium. Upgrading electrical systems from outdated wiring to modern standards similarly reduces fire risk and claim potential. Plumbing updates prevent water damage claims, which represent one of the costliest loss categories in Connecticut homes. These upgrades require upfront investment, but the premium reduction and reduced claim risk justify the expense over time. Track all improvements with receipts and photos, as this documentation supports your claim value if future damage occurs and proves your home’s current condition to your insurer.

These strategies address what you pay and what you’re insured for, but they only work if you truly understand what your policy covers. The next section walks through the coverage gaps most Connecticut homeowners miss and how to spot them before a loss occurs.

Finding the Right Coverage at the Right Price

Compare declarations pages, not just premium quotes

Shopping for homeowners insurance in Connecticut means comparing actual policy language, not just premium quotes. Most homeowners select the cheapest quote without understanding what differs between carriers, and this mistake costs thousands when a claim arrives. Request declarations pages from at least three carriers-not just premium estimates. A declarations page shows your exact coverage limits, deductibles, and what’s included or excluded. One carrier might offer replacement cost for personal property while another pays only actual cash value, and that difference determines whether you recover $8,000 or $5,000 when your belongings are damaged.

Request quotes using identical coverage limits across all carriers so you compare apples to apples. If one quote is dramatically lower, examine the declarations page to find what coverage was reduced. Lower premiums often mean lower liability limits, higher deductibles on wind or hail, or exclusions you didn’t notice. The Connecticut Insurance Department publishes homeowners insurance FAQs that clarify what standard policies include, and reviewing this resource before you shop prevents confusion when comparing quotes.

Identify the coverage gaps that standard policies hide

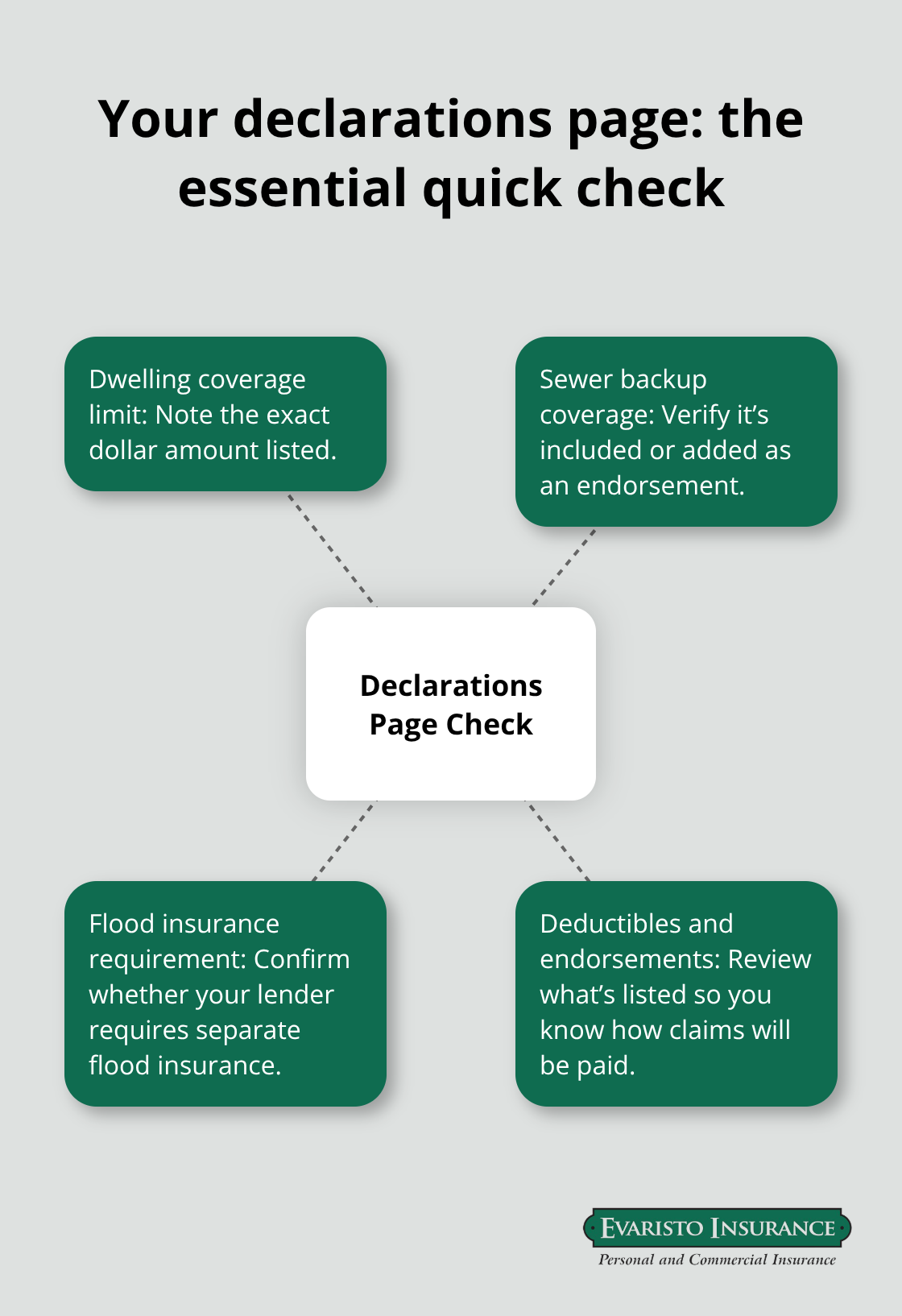

Your actual policy contains coverage gaps that only become visible when you read the exclusions section carefully. Flood damage is completely excluded from standard homeowners policies, yet Connecticut residents assume it’s covered until water enters their basement during a heavy rain event. Federal Flood Insurance through the National Flood Insurance Program requires a 30-day waiting period before coverage begins, so waiting until June when storm season approaches means you’re unprotected.

Sewer backup coverage is optional and excluded by default on most policies, yet a single backed-up sewer line costs $15,000 to $25,000 to repair. Water from a failed sump pump is similarly excluded unless you add backup coverage as an endorsement. These two exclusions (sewer backup and sump pump failure) represent the most common coverage gaps Connecticut homeowners face.

Review your policy’s declarations page immediately

Read your policy’s declarations page when it first arrives and mark these three items specifically: what your dwelling coverage limit is, whether you have sewer backup coverage, and whether flood insurance is required by your lender. This three-point check takes ten minutes and prevents costly surprises later. Your declarations page lists your exact coverage limits, deductibles, and any endorsements you’ve purchased, making it the single most important document in your policy file.

Schedule an annual review with a local independent agent

Schedule an annual review with a Connecticut independent agent before June when tropical storm season begins. An agent who represents multiple carriers can identify coverage gaps in your current policy and shift you to a carrier offering better protection at competitive rates. This review takes one hour and often reveals $300 to $600 in annual savings while actually improving your protection. An independent agent compares multiple top carriers to find coverage that matches your actual Connecticut exposure, not generic national policies that miss local risks.

Final Thoughts

Reducing your Connecticut homeowners insurance costs requires three concrete actions: understanding what drives your premiums, implementing strategies that lower them without cutting coverage, and reviewing your policy annually with someone who knows Connecticut’s specific risks. Rising home values, severe weather patterns, and aging home systems will continue pushing costs upward across the state, but you control how you respond to these forces. Bundling policies, raising deductibles strategically, installing safety devices, and upgrading home systems produce real savings that compound year after year.

Working with a local independent agent transforms Connecticut homeowners insurance tips from abstract advice into actionable protection tailored to your actual situation. An agent representing multiple carriers compares options across different companies rather than pushing you toward one insurer’s products, and they identify coverage gaps in your current policy that standard policies exclude-particularly flood risk and sewer backup damage. This expertise matters because cost-reduction tactics work only when applied to policies that actually cover your home’s specific risks.

Contact Evaristo Insurance to review your current coverage and identify savings opportunities you’ve missed. Schedule your annual policy review before June when tropical storm season begins, and bring your current declarations page to that conversation. Our local offices in Ellington and West Hartford mean you work with people who understand your neighborhood’s specific risks and insurance landscape.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.