Connecticut Homeowners Protection Options: A Guide to Coverage Choices

Your homeowners insurance policy is one of the most important financial decisions you’ll make as a Connecticut resident. Yet many homeowners don’t fully understand their Connecticut homeowners protection options or whether their current coverage actually matches their needs.

At Evaristo Insurance, we’ve helped thousands of Connecticut families navigate these choices and build protection plans that fit their specific situations. This guide walks you through the coverage options available to you, how to evaluate what you actually need, and how to find the right balance between protection and affordability.

What Your Connecticut Homeowners Policy Actually Covers

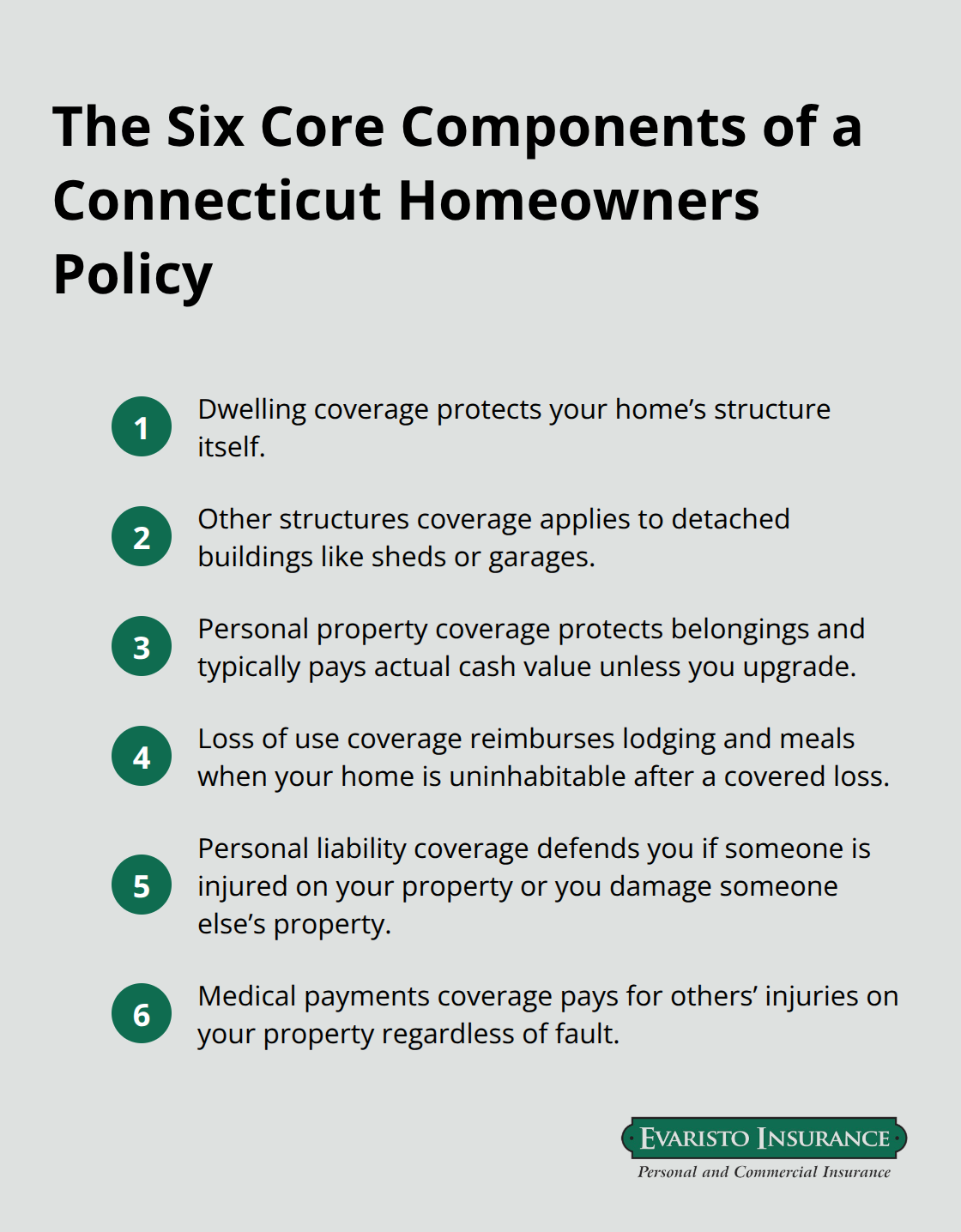

The Six Core Components of Your Policy

Connecticut homeowners policies contain six core components, and understanding each one matters because gaps between what you think you’re covered for and what you actually are covered for can be expensive. Dwelling coverage protects your home’s structure itself, while other structures coverage handles detached buildings like sheds or garages. Personal property coverage protects your belongings inside the home or damaged away from it, though this typically pays actual cash value rather than replacement cost unless you upgrade. Loss of use coverage reimburses lodging and meals if your home becomes uninhabitable after a covered loss. Personal liability coverage defends you if someone is injured on your property or you damage someone else’s property, and medical payments coverage pays for others’ injuries on your property regardless of fault.

Understanding Your Premium and Deductible

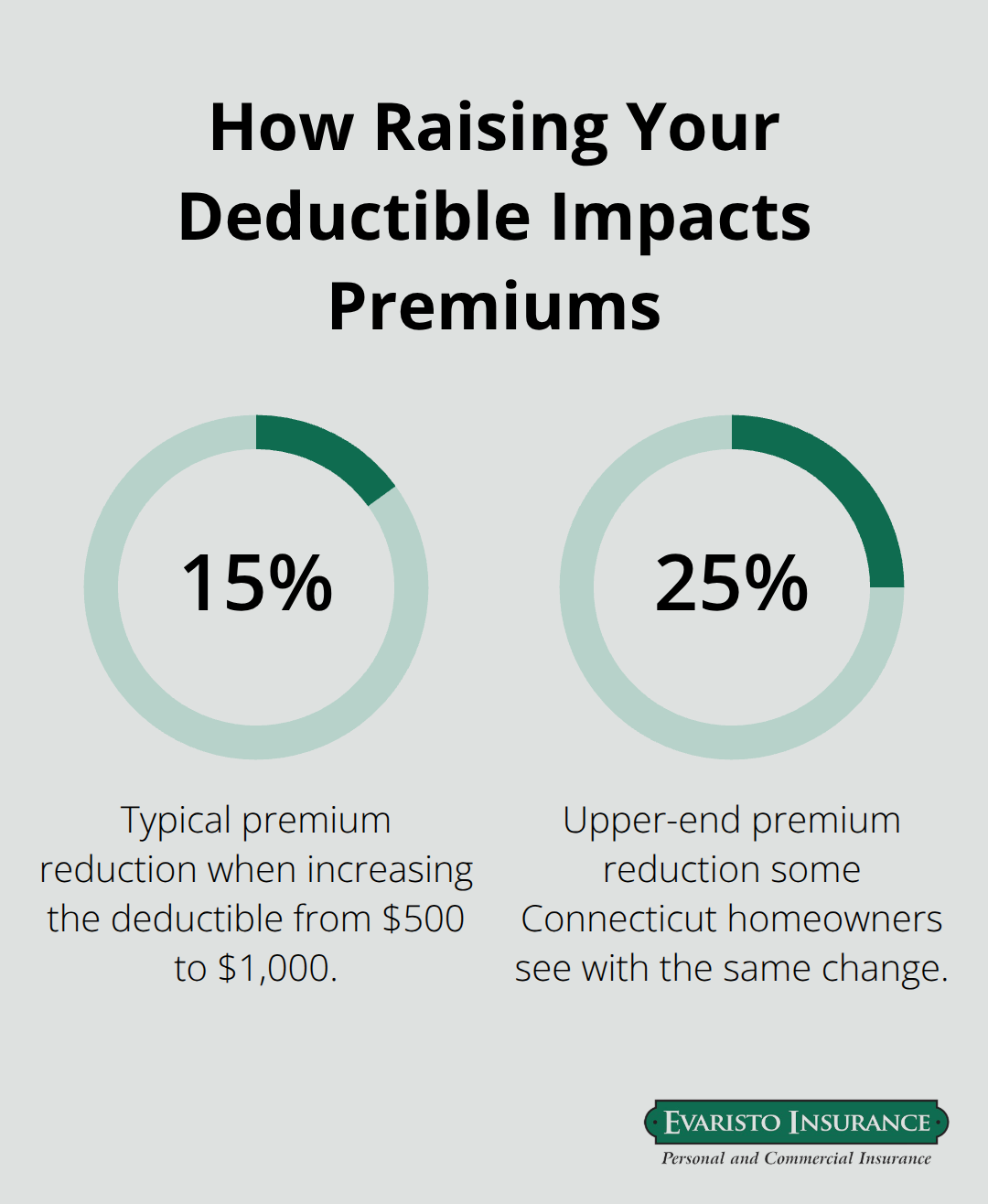

For a Connecticut home with $300,000 in dwelling coverage, the average annual premium runs about $2,231 according to current market data, which is slightly under the national average of $2,270. Most Connecticut homeowners choose deductibles of $500 or $1,000 to reduce premiums, and this choice significantly affects your costs. Higher deductibles lower your premium but mean you pay more out of pocket when you file a claim.

Critical Exclusions in Standard Policies

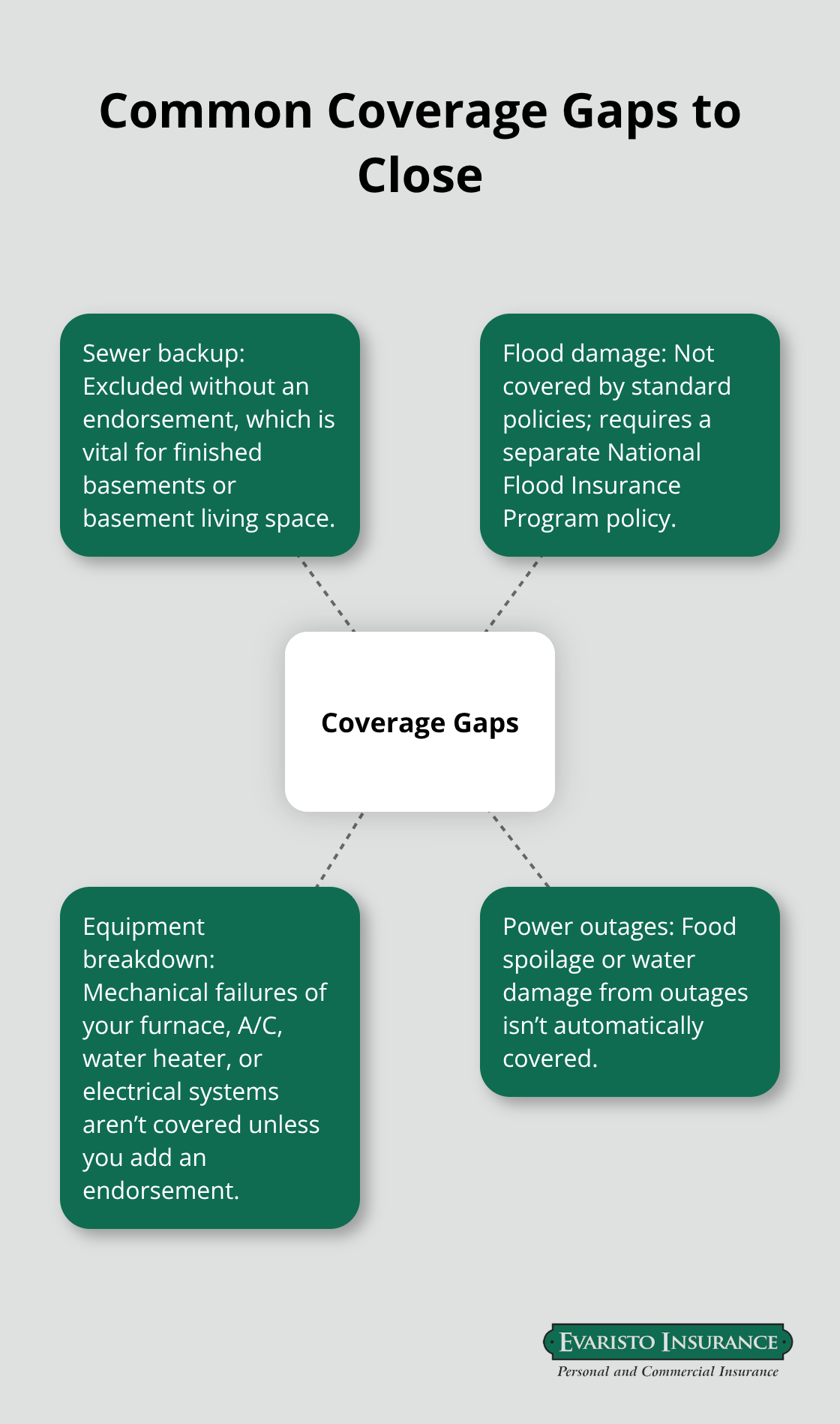

What standard policies exclude matters just as much as what they cover. Flood damage is completely excluded from your homeowners policy and requires separate flood insurance through the National Flood Insurance Program if your community participates. Sewer backup damage is also excluded unless you add a specific endorsement, which is important if you have basement living space or finished basements. Your policy won’t cover theft of watercraft outside your home, damage from earth movement or nuclear events, business property, or animals and birds.

How Connecticut’s Climate and Regulations Shape Your Coverage

Connecticut’s climate creates specific exposure-the state has experienced 31 federally declared disasters since 1953-so understanding these exclusions helps you identify where endorsements or additional policies make sense. Connecticut regulations require that if you have a mortgage, your lender will mandate sufficient homeowners insurance and dictate minimum coverage levels, though Connecticut state law doesn’t require homeowners to carry insurance on its own. The Connecticut Department of Insurance oversees all policies and complaints, so if you dispute a settlement, you can use the dispute resolution process outlined in your policy or contact the department.

Shopping Across Carriers Reveals Significant Price Differences

When you compare quotes across carriers like State Farm, Travelers, Erie, or others, understand that each company weights rate factors differently, so the same home can cost significantly different amounts depending on the carrier’s underwriting approach. This variation makes it essential to evaluate not just price but also how each carrier handles the specific risks your Connecticut home faces-and which additional coverage options each one offers to fill the gaps that standard policies leave behind.

What Your Connecticut Home Is Actually Worth to Insure

Calculating Your Home’s True Replacement Cost

Start with your home’s replacement cost, not its market value. A Connecticut home worth $500,000 on the real estate market might cost $600,000 to rebuild from scratch due to current labor and material prices. This distinction matters because your dwelling coverage should protect what it would cost to reconstruct your home, not what someone would pay for it today. Many Connecticut homeowners underestimate this number significantly. If your home is older, was built with specific materials, or requires specialized contractors in your area, reconstruction costs climb even higher. A local agent can run a replacement cost estimate specific to your property, your town, and current Connecticut building codes. This single number determines whether your dwelling coverage is adequate or dangerously low.

Valuing Your Personal Property Accurately

Your personal property coverage presents a different challenge entirely. Most Connecticut homeowners have far more belongings than they realize. Electronics, furniture, clothing, kitchen equipment, and everything else inside your home needs valuation. The standard approach most people take-guessing-leads to massive underinsurance. Instead, walk through your home room by room and photograph everything. Check purchase receipts for major items. For items you no longer have receipts for, note the approximate replacement cost today, not what you paid five years ago. This inventory becomes essential if you file a claim because insurers will request proof of ownership and value.

Many homeowners find their personal property coverage limits are too low once they actually add things up. If you own jewelry, art, antiques, or collectibles, these need separate appraisals and scheduled coverage because standard personal property limits won’t adequately cover high-value items. A single piece of jewelry might be worth $8,000, but your personal property coverage might have a $2,500 limit per item unless you specifically schedule it. Connecticut homeowners frequently need valuable items blanket coverage, which can increase protection for jewelry or silverware up to $10,000 per item depending on your policy.

Identifying Coverage Gaps That Standard Policies Leave Behind

The real gaps emerge when you consider what standard coverage doesn’t address. Sewer backup flooding in your basement, which Connecticut homeowners face regularly, isn’t covered without an endorsement. Flood damage from any source requires separate National Flood Insurance Program coverage. Equipment breakdown-your furnace failing mid-winter or your air conditioning system dying in summer-typically isn’t covered, though some carriers offer equipment breakdown endorsements. Power outages causing food spoilage or water damage aren’t automatically covered either.

These gaps exist precisely because standard policies exclude them, which means you need to actively identify which gaps apply to your specific situation. A finished basement changes your needs entirely compared to an unfinished one. A home near water faces different risks than an inland property. A home with an older roof has different vulnerabilities than one with a newer roof. Your location within Connecticut-whether you’re in a flood zone, near a fire station, or in a high-wind area-directly impacts which additional coverage makes financial sense for your situation and which endorsements will actually protect you when loss occurs.

Protecting Against Water Damage and Liability Gaps

Flood Insurance and Sewer Backup Coverage

Flood damage destroys Connecticut homes regularly, yet most homeowners don’t realize their standard policy excludes it entirely. The National Flood Insurance Program covers building damage and personal property losses from flooding, and your community likely participates in this federal program. If you live in a flood zone, your mortgage lender will require you to carry flood insurance-this isn’t optional. Even if you’re not in an official flood zone, Connecticut’s climate delivers heavy rain, nor’easters, and rapid snowmelt that cause basement flooding regularly. Sewer backup coverage costs roughly $50 to $100 annually as an endorsement but protects against one of the most common water damage claims in Connecticut basements. Without this endorsement, damage from sewers or drains backing up into your home remains excluded.

Equipment Breakdown and System Protection

Equipment breakdown coverage repairs or replaces your furnace, air conditioning, water heater, and electrical systems after mechanical failure-costs average $150 to $300 yearly depending on your home’s systems. This coverage also covers energy-efficient upgrades up to 125 percent of replacement cost, which matters if your heating system fails and you install a more efficient model. These three endorsements address the water and system failures that destroy Connecticut homes most frequently, and adding them costs far less than recovering from an uninsured loss.

Umbrella Liability Protection

Liability exposure grows significantly if you own property, have visitors regularly, or maintain attractive features like pools or trampolines. Your standard policy includes $100,000 to $300,000 in liability coverage, which sounds adequate until you face a serious injury claim. A single accident where someone sustains severe injury on your property can generate medical costs, lost wages, and pain-and-suffering claims exceeding $1 million. An umbrella policy provides $1 million to $2 million in additional liability coverage above your homeowners and auto policies combined, costing $150 to $300 annually for the first million dollars. Connecticut homeowners with pools, significant property value, or regular entertaining should carry umbrella coverage-the protection is inexpensive relative to the risk.

Scheduled Coverage for High-Value Items

High-value items demand scheduled coverage rather than relying on personal property limits. Jewelry, art, antiques, and collectibles need individual appraisals and scheduled amounts on your policy because standard coverage caps individual items at $2,500 to $5,000. A valuable items blanket endorsement increases protection for jewelry or silverware up to $10,000 per item, protecting collections without requiring separate appraisals for each piece. Connecticut homeowners with estates, inherited jewelry, or significant art collections should schedule these items specifically-the premium cost is minimal compared to the replacement value you’re protecting.

Final Thoughts

Comparing quotes across multiple carriers reveals significant price differences for identical coverage on your Connecticut home. State Farm, Travelers, Erie, and other major insurers weight factors like roof age, proximity to fire stations, and claims history differently, so the same $300,000 dwelling coverage costs substantially different amounts depending on each carrier’s underwriting approach. Requesting three to five quotes takes roughly 30 minutes but often uncovers premium differences of $500 or more annually, making the effort worthwhile when you evaluate Connecticut homeowners protection options.

Adequate protection at an affordable price requires intentional choices about deductibles and optional coverage rather than simply selecting the lowest quote. Raising your deductible from $500 to $1,000 typically reduces your premium by 15 to 25 percent, though you must actually afford that deductible when a loss occurs.

Adding flood insurance, sewer backup coverage, and equipment breakdown protection costs $200 to $400 annually but protects against the specific water and system failures that destroy Connecticut homes most frequently.

At Evaristo Insurance, we compare multiple top carriers to find coverage matching your actual needs and budget rather than pushing policies that maximize commissions. Our team runs replacement cost estimates specific to your property and town, identifies which endorsements make financial sense for your situation, and explains exactly what your coverage protects. Contact us to discuss your specific situation and receive quotes reflecting what your Connecticut home actually needs.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.