Connecticut Landscaper Insurance: Protecting Your Outdoor Team

Running a landscaping business in Connecticut means managing more than just plants and equipment-you’re managing real liability risks. At Evaristo Insurance, we’ve seen too many landscapers operate with gaps in their coverage that could cost them thousands.

Connecticut landscaper insurance isn’t one-size-fits-all, and general liability alone won’t cut it. This guide walks you through exactly what your outdoor team needs to stay protected.

What Connecticut Requires for Landscapers

Connecticut law mandates that landscapers with employees carry workers’ compensation insurance, with general liability coverage of at least $1 million per occurrence and $2 million aggregate to operate legally. These aren’t suggestions-they’re hard requirements. Fail to carry workers’ comp and you face fines and potential legal action that can shut down your business. The Connecticut Department of Labor enforces these rules strictly, and contractors regularly get caught short when they haven’t verified their actual obligations against their current policies.

How Your Service Mix Shapes Your Coverage Needs

Your specific service mix determines what else you need beyond state minimums. A crew doing tree removal and excavation faces different exposures than one focused on lawn mowing, so your class code matters. The National Council on Compensation Insurance assigns different rates based on the work you perform. Misclassifying your crew or understating payroll during an audit means back payments and premium increases that hurt your bottom line.

Why General Liability Falls Short

Most landscapers think general liability handles everything, then face devastating gaps when claims hit. A worker suffers a back injury from lifting, and you discover your policy has limits too low to cover rehabilitation and lost wages. A crew member damages a client’s fence, and general liability covers it, but then another worker gets electrocuted near a power line, and that claim exhausts your coverage.

Landscaping has one of the highest rates of occupational injuries and illnesses across all industries, yet many Connecticut landscapers operate with only the minimum required coverage. Workers’ compensation claims are the most common in landscaping, followed closely by transportation-related injuries since crews move between multiple job sites daily.

The Hidden Exposures Most Landscapers Miss

You also need commercial auto insurance if you haul equipment-many landscapers skip this and then face a vehicle accident that leaves them personally liable. Equipment theft and damage at job sites or in transit requires inland marine coverage that most standard policies exclude. Your actual protection should reflect the physical risks your team faces every day, not just what the law technically demands.

These gaps in coverage leave your business vulnerable. Understanding which specific coverages address your operation’s actual exposures is where the real protection begins.

Essential Coverage Types for Your Landscaping Operation

Workers’ Compensation: The Foundation Your Team Needs

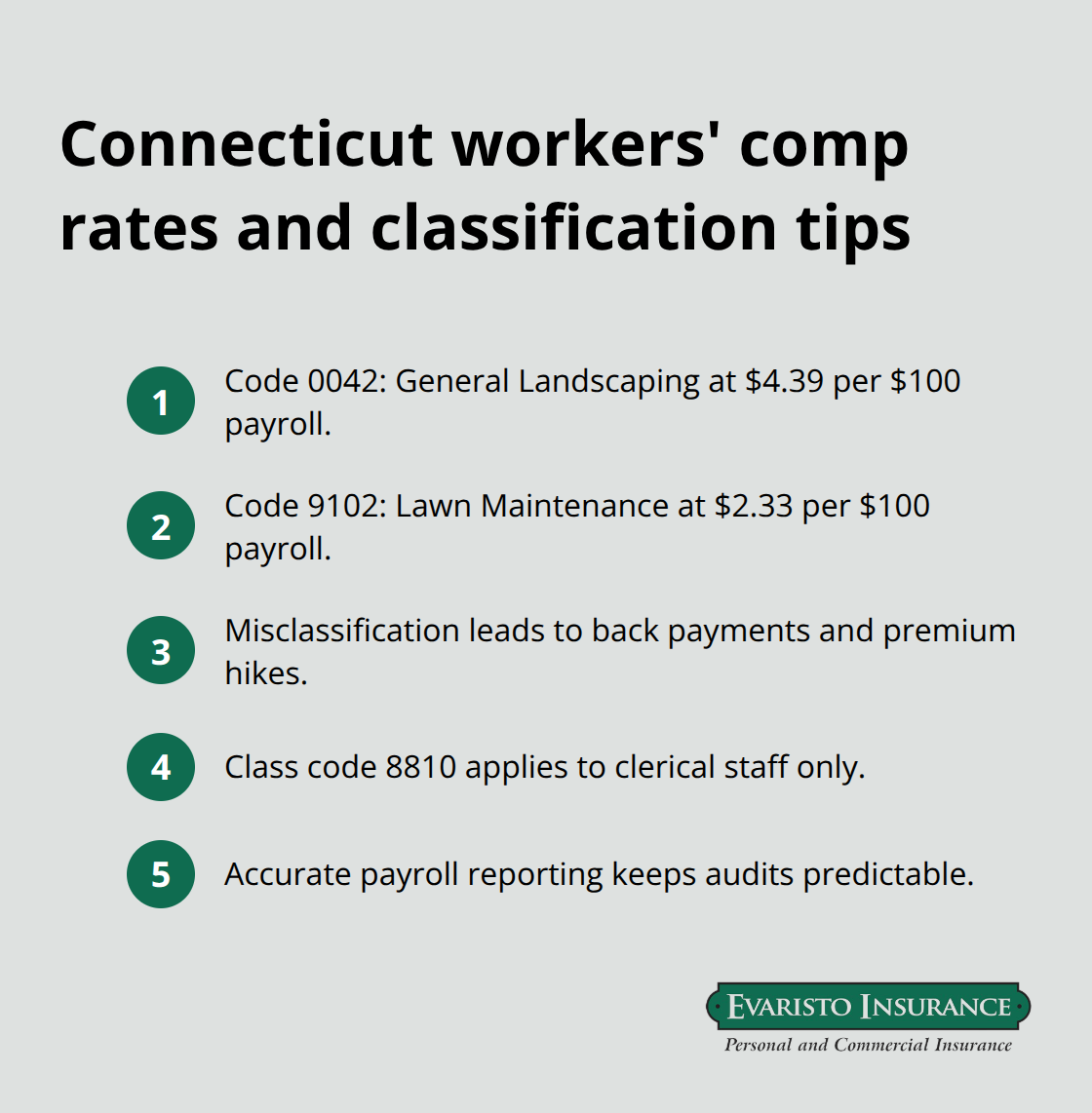

Workers’ compensation becomes mandatory the moment you hire your first employee in Connecticut, and most landscapers underestimate both what this coverage costs and what it actually covers. The National Council on Compensation Insurance sets fixed rates for Connecticut based on your class code and payroll. For landscapers, workers’ comp rates in Connecticut vary by classification: General Landscaping (Code 0042) runs $4.39 per $100 of payroll, while Lawn Maintenance (Code 9102) costs $2.33 per $100 of payroll. This math matters because misclassifying workers or underreporting payroll during an audit triggers back payments and premium increases that damage your bottom line. If you have clerical staff, they belong in class code 8810, not lumped with manual laborers in code 0042 or 9102.

Workers’ comp covers medical expenses, rehabilitation, partial lost wages, and disability benefits-but only if you report payroll accurately and assign the right class codes from day one.

Transportation-related injuries rank as the second-most common workers’ comp claim in landscaping after on-the-job injuries. Your crews moving between job sites daily create exposure that proper classification and accurate records help manage. An audit at year-end can reveal payroll discrepancies that cost thousands in back premiums, so keeping neat records and using an audit checklist protects you from surprises.

Commercial Auto and Equipment Protection

Commercial auto insurance protects your operation when crews haul equipment or travel to client sites. Connecticut landscapers typically pay around $1,810 annually for this coverage, and it becomes essential if you use company vehicles for work. A crew member causes a vehicle accident while transporting a trailer full of equipment, and without commercial auto, you face personal liability that general liability won’t cover. This gap leaves your business exposed to catastrophic claims that could exceed your other policy limits.

Inland marine coverage protects tools, mowers, and equipment in transit or at temporary job sites from theft, vandalism, and accidents-exposures that standard policies explicitly exclude. Many landscapers discover this gap only after equipment disappears from a job site or gets damaged during transport. Equipment protection should match your actual inventory: if you operate $50,000 worth of mowers and tools, your inland marine limits need to reflect that reality.

Building Your Coverage Package

Combining workers’ comp, commercial auto, and inland marine into a coordinated package costs roughly $4,180 annually for a basic operation, though your actual premium depends on business size, services offered, and claims history. The key is matching coverage limits to your actual exposures rather than shopping for the cheapest option and hoping nothing goes wrong. When you work with an independent agent who understands landscaping risks, they can identify which specific coverages address your operation’s actual exposures and help you avoid paying for protection you don’t need while ensuring you don’t skip what you do.

Your coverage stack should reflect the physical risks your team faces every day, not just what Connecticut law technically demands. The next section walks you through how to evaluate insurance providers and find an agent who understands your business well enough to build a policy that actually protects you.

How to Choose the Right Insurance Provider for Connecticut Landscapers

Start with Multiple Quotes from Landscaping-Focused Carriers

Choosing an insurance provider matters more than most landscapers realize, yet many accept the first quote they receive or stick with whoever their friend recommended without understanding what they’re actually buying. General liability insurance for landscaping businesses averages $610 annually, so the difference between a poorly matched policy and one tailored to your actual exposures can mean thousands in unnecessary premiums or catastrophic gaps when claims happen. Request quotes from at least three carriers that specifically understand landscaping operations, not generic commercial insurance providers who treat your business like any other contractor.

When you compare quotes, ignore the headline premium number and instead examine what each policy actually covers. Does the general liability limit of $1 million per occurrence match your risk level, or do you need $2 million because you work on high-value properties? Does the workers’ comp classification match your actual service mix, or has the agent lumped all your crews into one code and missed the clerical staff who should be classified separately?

Verify Coverage Details Before You Commit

Ask each carrier directly whether they cover herbicide and pesticide application if you handle chemical treatments, and confirm that inland marine protection includes equipment in transit to job sites. Connecticut landscapers often discover too late that their commercial auto policy excludes trailers or that their equipment coverage has a $500 deductible when a $50,000 mower gets stolen. A detailed policy review from any provider you’re considering reveals exactly what each coverage does, where gaps exist, and why specific limits matter for your operation.

Evaluate Local Expertise and Claims Support

Local expertise separates providers who understand landscaping from those who don’t. An agent familiar with Connecticut’s specific hazards-from heat exhaustion during summer work to electrocution risks near power lines to tractor rollovers on sloped properties-asks questions about your actual operations and recommends coverages that address real exposures rather than selling you a standard package. When you call a potential provider, ask directly: Have you worked with landscaping crews before? Can you explain which class codes apply to our specific services? Do you handle claims quickly, or do we wait weeks for answers?

Claims support matters intensely because when a worker gets injured or a crew member damages a client’s property, you need your insurance company to move fast and handle the situation professionally. An independent agent who compares quotes from multiple carriers finds you genuine value rather than locking you into one company’s offerings. Local offices let you speak with someone who understands Connecticut landscaping specifically, not a call center agent reading from a script.

Prioritize Carriers with Strong Financial Ratings

Select carriers with A-ratings or better from financial strength agencies to protect yourself against insolvency. A cheap policy from a weak carrier leaves you exposed if that company fails and cannot pay claims when you need them most. Your insurance provider’s financial stability matters as much as the coverage limits on your policy.

Final Thoughts

Connecticut landscaper insurance protects your business from the specific exposures your outdoor team faces every day. Workers’ compensation covers your crew’s injury costs, general liability handles third-party claims, commercial auto protects vehicles hauling equipment, and inland marine coverage shields tools and mowers in transit. These four coverage types form the foundation that keeps your operation running when accidents happen.

Gather quotes from at least three carriers that understand landscaping operations, not generic commercial providers. Compare what each policy actually covers rather than focusing on the headline premium, verify that workers’ comp class codes match your specific services, and confirm that general liability limits reflect your risk level. Request a detailed policy review from each carrier to identify gaps before you commit.

An experienced agent asks questions about your crew size, service mix, equipment inventory, and job site locations rather than selling you a standard package. At Evaristo Insurance, we’ve served Connecticut since 1989 as a family-owned independent agency comparing multiple top carriers to deliver tailored Connecticut landscaper insurance and competitive pricing. Contact us today to review your current coverage and identify what your operation truly needs.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!