Investment Property Liability Coverage: Minimizing Risk Across Your Portfolio

Connecticut landlords with multiple properties face real liability exposure that most standard policies don’t fully address. Investment property liability coverage protects your portfolio from the financial devastation of tenant injuries, property damage claims, and legal costs that can quickly drain your returns.

At Evaristo Insurance, we’ve seen too many local investors underestimate their risk across multiple units. This guide walks you through the specific coverage you need and how to build a strategy that actually works for your portfolio.

What Your Liability Coverage Actually Covers

Investment property liability coverage fills a gap that standard homeowners policies leave wide open. When a tenant slips on your stairs, a visitor sustains an injury on the property, or someone sues you over property damage, your landlord policy steps in to cover medical bills, legal defense costs, and settlements up to your policy limits. Connecticut landlords typically carry $1 million per occurrence and $2 million aggregate in premises liability, though high-risk properties or larger portfolios often require higher limits. The coverage pays for immediate medical expenses, ongoing treatment costs, and court defense fees-expenses that can easily exceed $50,000 in a contested injury case before any settlement is reached. Without adequate liability protection, you face personal exposure to judgments that can seize rental income, force property sales, and drain personal assets.

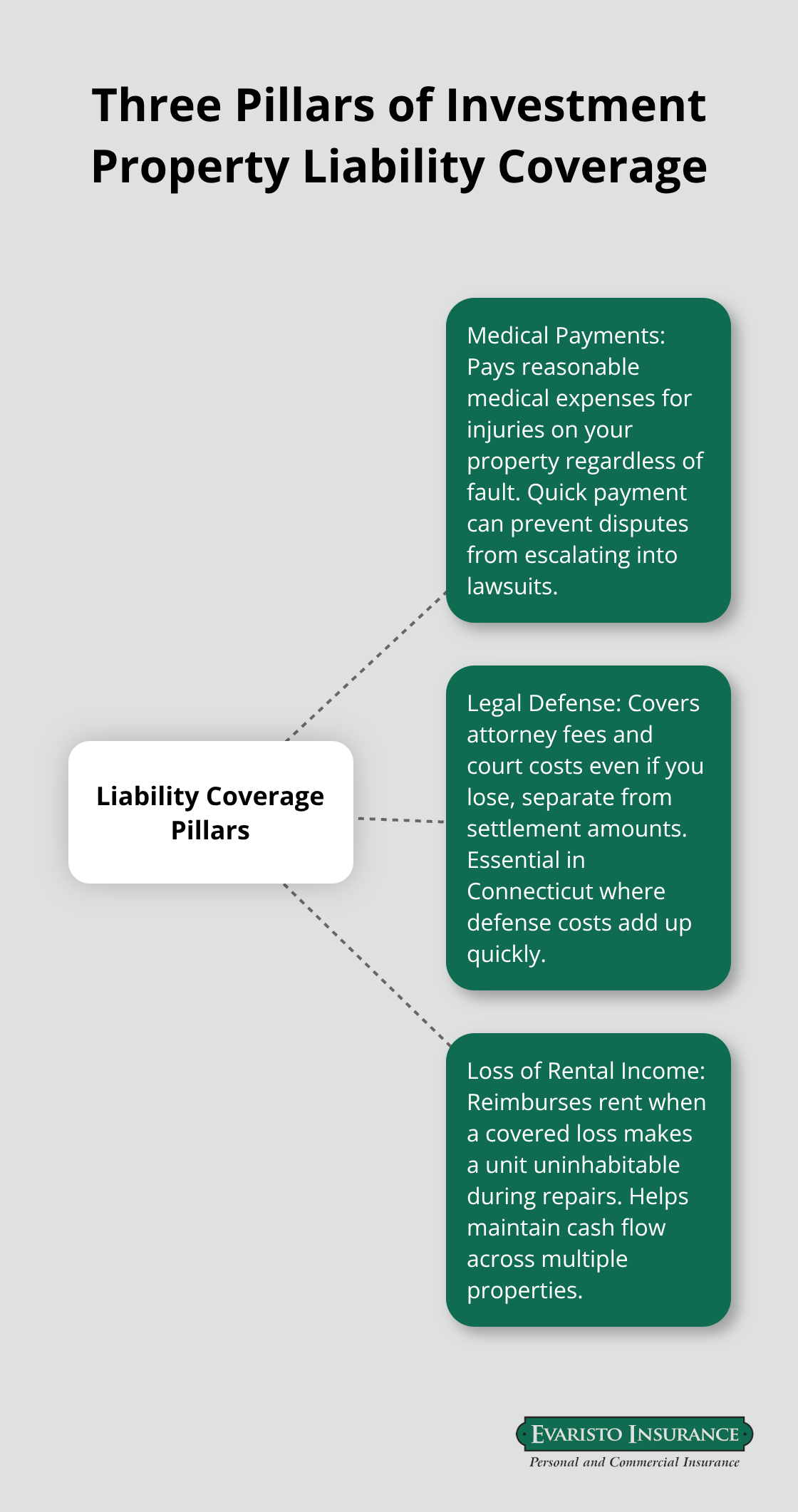

Medical Payments and Injury Claims

Medical payments coverage under your policy covers reasonable medical expenses for injuries that occur on your property, regardless of fault. If a tenant’s guest falls and breaks an arm, your policy may pay their medical bills directly without waiting for a lawsuit. Connecticut’s tenant-friendly legal environment makes this protection essential-tenant injury claims are common and litigation costs are high. The coverage typically includes emergency room visits, hospitalization, surgery, and follow-up care up to a stated limit, often $5,000 to $25,000 per person. Paying these expenses quickly through your policy often prevents escalation to formal lawsuits and protects your relationship with tenants. Many landlords overlook this feature and instead face angry tenants who sue for full damages when medical bills go unpaid.

Legal Defense and Property Damage Claims

Your liability policy covers legal defense costs separately from settlement amounts, meaning your carrier pays your attorney’s fees even if you lose the case. This distinction matters enormously in Connecticut, where defense costs in premises liability cases routinely run $15,000 to $40,000 before trial. If a tenant claims you failed to maintain safe conditions and files suit, your insurance company provides a defense attorney at no cost to you. The policy also covers property damage liability if you accidentally damage a neighbor’s property-for example, if a tree on your rental property falls and damages their fence or roof. Connecticut’s older housing stock creates frequent maintenance disputes; having explicit property damage coverage prevents these disputes from becoming personal financial disasters. Higher limits become essential as your portfolio grows, since courts often award damages based on the defendant’s perceived wealth and property holdings.

Loss of Rental Income Protection

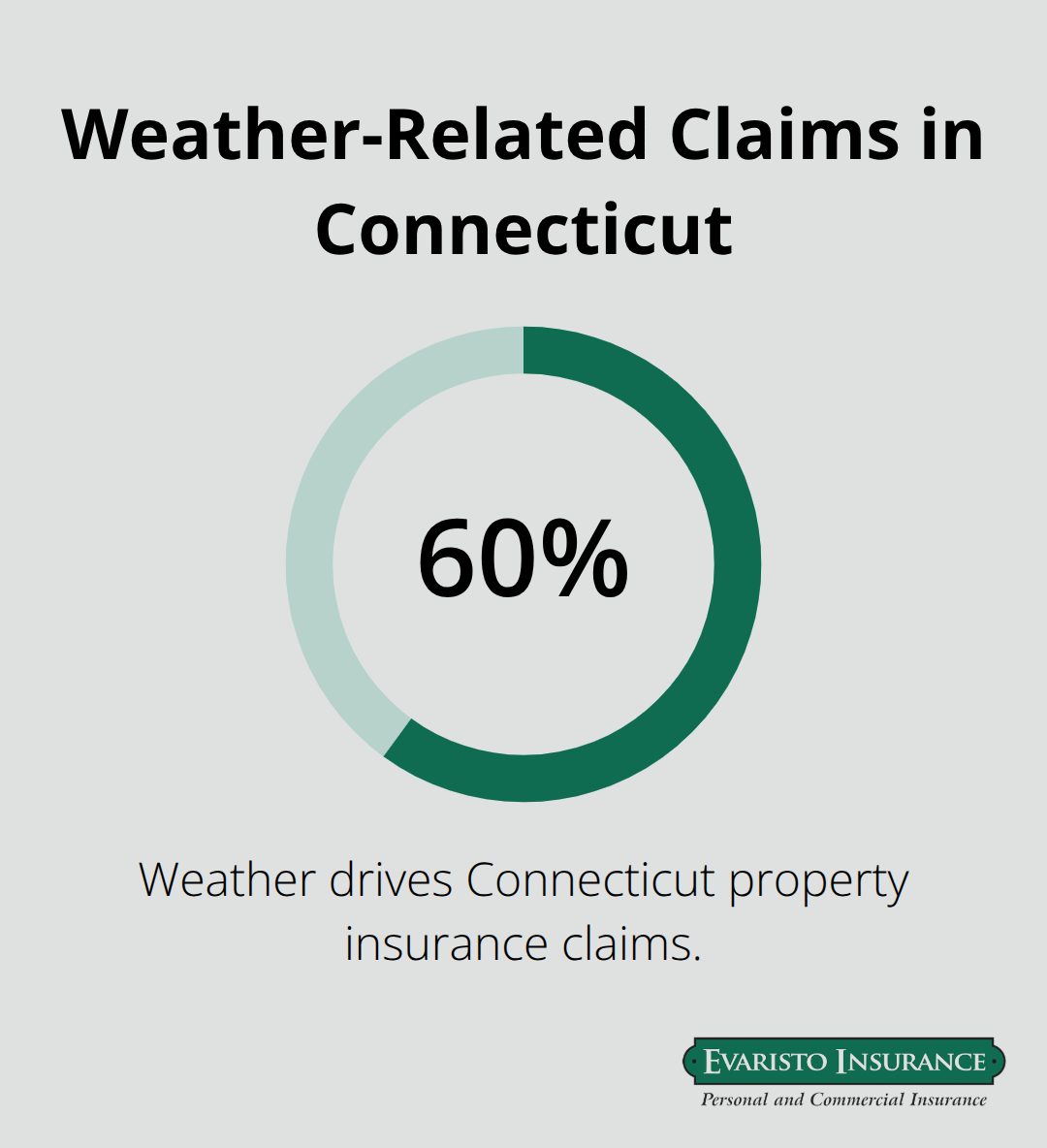

When a covered event makes a rental unit uninhabitable, loss of rental income coverage reimburses the rent you would have collected during repairs. If a fire damages a unit and repairs take three months, this coverage pays your lost rent for that period while you cover mortgage and maintenance costs. Connecticut weather causes roughly 60 percent of property insurance claims, with winter storms and water damage being the most frequent triggers. Loss of rental income is not automatic on all policies-you must add it as an endorsement-and coverage periods vary from 12 to 24 months.

The coverage typically begins after a waiting period (often 7 to 14 days) and continues only for the repair duration, not indefinitely. For landlords managing tight cash flow across multiple properties, this protection prevents forced asset sales or loan defaults when a single property goes offline.

Understanding these three pillars of liability coverage sets the foundation for your portfolio strategy. The next step involves assessing your actual risk exposure across each property and determining whether your current limits match the real threats Connecticut landlords face.

Common Liability Risks Landlords Face in Connecticut

Tenant Injuries and Premises Liability Claims

Tenant injuries represent the most frequent liability claim Connecticut landlords encounter, and the state’s tenant-friendly legal environment makes these claims expensive to defend. When a tenant or their guest suffers an injury on your property-a fall on icy stairs, a slip in the bathroom, an injury from a maintenance failure-Connecticut courts often side with the injured party, especially if documentation shows neglect. Medical payments coverage handles routine injury expenses, but serious cases escalate quickly. A broken leg or head injury can generate $30,000 to $100,000 in medical costs alone, and if the injured person hires an attorney, legal fees add another $15,000 to $40,000 before settlement negotiations even begin.

Connecticut General Statutes 47a-7 and 47a-7a require landlords to maintain safe premises and address maintenance issues promptly; failure to comply creates automatic liability exposure. The state’s Right to Counsel in Eviction Proceedings (Public Act 21-34) has also increased tenant awareness of legal options, meaning more injuries result in formal claims rather than informal resolution. Documenting maintenance requests in writing, addressing repairs within 48 hours, and requiring tenants to carry renters insurance are practical steps that reduce both injury frequency and claim severity.

Weather and Seasonal Hazards

Weather and seasonal hazards cause approximately 60 percent of all property insurance claims filed in Connecticut, making seasonal risk management non-negotiable for portfolio owners. Winter storms deliver roughly 45 inches of snow annually across the state, plus nor’easters and ice storms that damage roofs, burst pipes, and create liability when snow or ice causes tenant injuries. Water damage from burst pipes and plumbing failures ranks second only to weather damage in claim frequency, and these events trigger loss of rental income coverage that reimburses missed rent during repairs.

Connecticut’s older housing stock-much of it pre-1980-compounds these risks because aging plumbing and electrical systems fail more frequently and cost more to repair. Coastal properties face additional hurricane and storm surge exposure, while inland properties contend with flooding that standard policies exclude entirely.

Neighbor Disputes and Property Line Issues

Neighbor disputes and property line issues create a third liability category that many landlords overlook until they face a lawsuit. Tree damage claims occur when branches from your property damage a neighbor’s roof or fence; Connecticut’s dense residential neighborhoods mean properties often sit close together. Fence disputes arise over maintenance responsibility and boundary encroachment, and these conflicts escalate when neighbors hire attorneys. Documenting property boundaries with a survey, maintaining trees and vegetation regularly, and keeping detailed records of any disputes in writing protects you against neighbor claims that can cost $5,000 to $25,000 in legal defense even if you ultimately prevail.

Higher liability limits become essential as your portfolio grows across Connecticut because courts often award damages based on perceived defendant wealth; a landlord owning five properties faces larger potential judgments than a single-property owner. These three risk categories demand different coverage strategies, which means assessing your actual exposure across each property becomes the next critical step in building your portfolio protection plan.

Building Your Liability Strategy Across Multiple Properties

Assess Your Portfolio’s Actual Risk Profile

List every property in your portfolio with its specific characteristics: age, number of units, location (coastal, urban, rural), tenant type, and prior claims history. Connecticut landlords with five or more properties face materially different liability exposure than single-property owners because courts award larger judgments to defendants perceived as wealthy. A property manager handling ten units across Hartford, New Haven, and Stamford encounters different seasonal risks at each location-coastal properties face hurricane exposure that inland properties don’t, and older pre-1980 buildings generate more maintenance claims regardless of location.

Document the last three years of claims for each property, including dates, loss amounts, and whether injuries or property damage drove the claim. This history reveals patterns: if two properties have water damage claims within 18 months, both need immediate plumbing inspection and possibly higher coverage limits. Connecticut’s median landlord insurance premium runs about $2,610 annually, but premiums vary dramatically by property age, location, and claims history. A single large judgment can exceed $100,000 in a contested injury case, making underinsurance catastrophic for portfolio owners.

Evaluate Liability Limits Against Real Exposure

Most Connecticut landlords carry $1 million per occurrence and $2 million aggregate in premises liability, but this baseline works only for small portfolios. A landlord owning five single-family rentals should carry at least $2 million per occurrence; an owner with multifamily properties should go higher. Umbrella liability policies extend protection across all properties at lower cost than raising underlying limits-an umbrella policy often adds $200 to $400 annually for $1 million in additional coverage, far cheaper than raising individual property limits.

The critical mistake occurs when you carry umbrella coverage without synchronizing underlying policy limits; gaps between your property policy limits and umbrella coverage create uninsured exposure. Connecticut’s tenant-friendly legal environment means defense costs often run $15,000 to $40,000 before settlement, so inadequate limits force you to pay defense costs personally once policy limits exhaust. Deductible choices affect both premium and out-of-pocket risk: a $2,500 deductible costs less than a $1,000 deductible but means you absorb more cost when claims occur. For injury claims, your insurer pays defense costs separately from settlement amounts, so deductibles don’t apply to legal defense-only to damages you must pay.

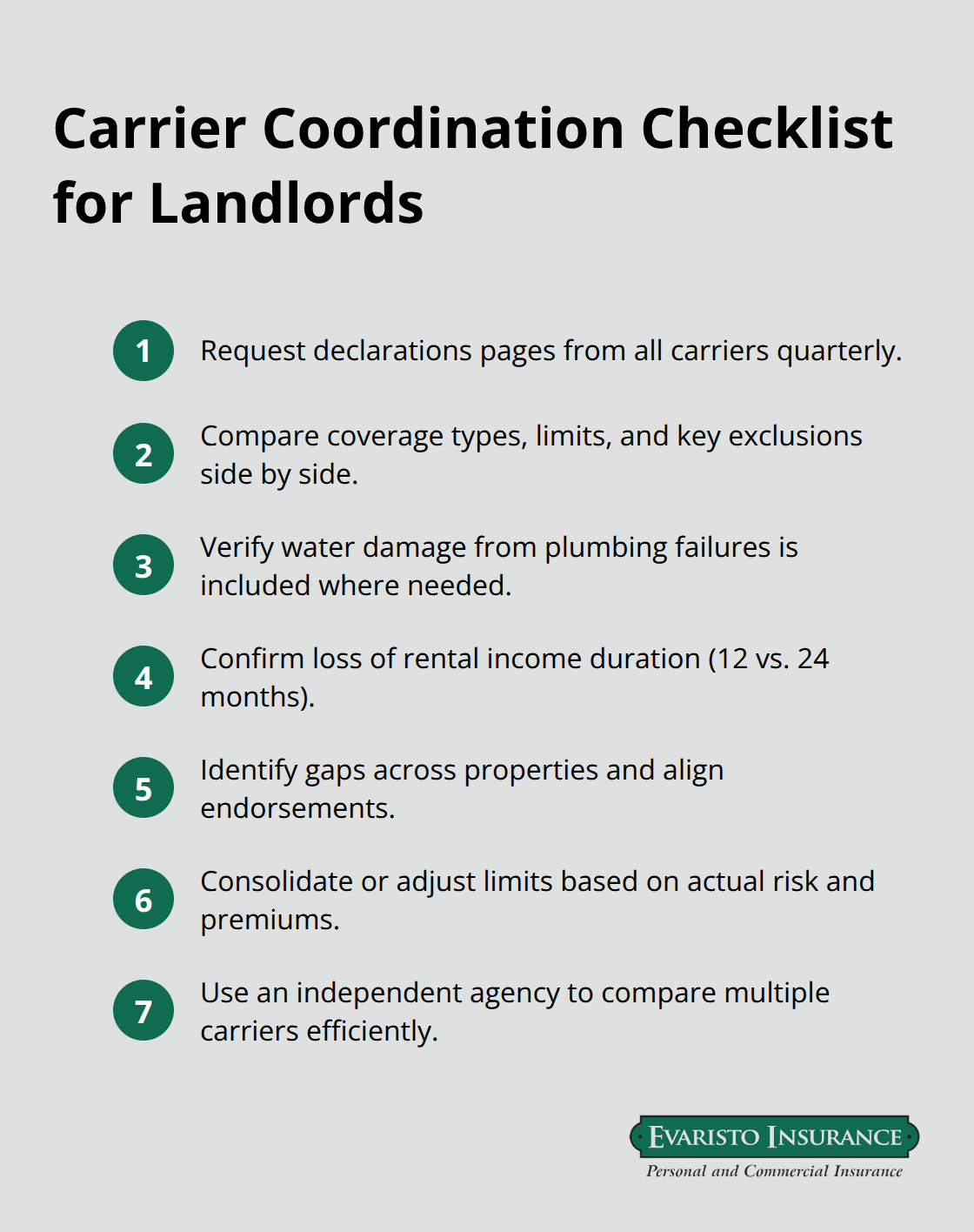

Coordinate Coverage Across Multiple Carriers

Coordinate coverage across carriers if you hold policies with different insurers. Many landlords split properties across multiple carriers seeking lower rates, but this creates dangerous gaps when one carrier’s policy excludes a peril another carrier covers. If one property carries flood insurance through Carrier A and another doesn’t through Carrier B, you’ve created unequal protection across your portfolio during heavy rain events common to Connecticut.

Request declarations pages from every carrier quarterly and compare coverage types, limits, and exclusions side by side. Some carriers exclude water damage from plumbing failures; others include it. Some cap loss of rental income at 12 months; others extend to 24 months. These differences compound across a portfolio.

An independent agency that compares multiple carriers eliminates the administrative burden of tracking separate policies and identifies coverage gaps you’d otherwise miss. Request a formal proposal that shows each property’s coverage type, limits, and annual premium so you can see exactly what you’re paying for and spot opportunities to consolidate or adjust limits based on actual risk.

Final Thoughts

Investment property liability coverage protects your portfolio from the financial devastation that a single injury claim or property damage lawsuit inflicts. Connecticut’s tenant-friendly legal environment and weather-prone climate create real exposure that standard policies don’t address, and underinsurance across multiple properties compounds that risk exponentially. The three core protections-medical payments, legal defense coverage, and loss of rental income-form the foundation of any solid portfolio strategy, but only if your limits match your actual exposure.

Pull together your current declarations pages and list each property’s coverage type, liability limits, deductibles, and annual premium. Compare these limits against your portfolio size and claims history, and flag any gaps between carriers such as water damage exclusions, loss of rental income caps, or missing endorsements. If you own five or more properties, your current $1 million per occurrence limit likely falls short; an umbrella policy extending coverage across all properties costs far less than raising individual limits and simplifies administration.

Connecticut landlords benefit enormously from working with an independent agent who compares multiple carriers and understands local risk factors. Weather causes 60 percent of claims in Connecticut, winter storms hit hard annually, and tenant-friendly laws make injury claims expensive to defend. We at Evaristo Insurance have served Connecticut landlords since 1989, comparing top-rated carriers to deliver tailored investment property liability coverage and competitive pricing-contact us to review your current coverage and build a liability strategy that actually protects your investment across all your properties.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.