Landlord Insurance Deductible CT: How to Budget Your Costs

Choosing the right landlord insurance deductible in Connecticut directly impacts your bottom line. A higher deductible lowers your monthly premium, but it means you’ll pay more out of pocket when you file a claim.

We at Evaristo Insurance help Connecticut landlords find the balance between affordable premiums and manageable out-of-pocket costs. This guide walks you through the numbers so you can make a decision that fits your financial situation.

What Deductibles Actually Cost You

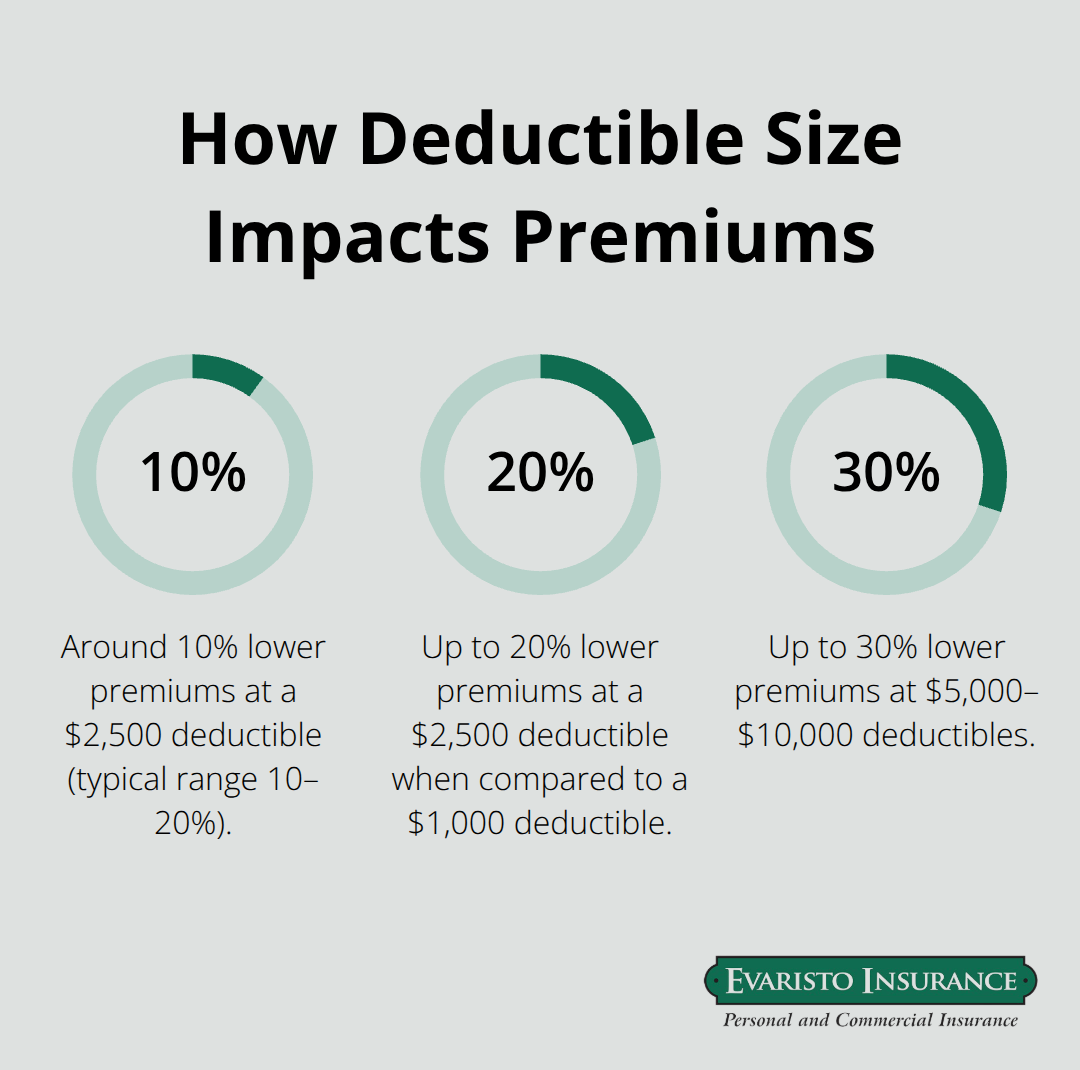

A deductible is the amount you pay out of your own pocket when you file a claim. Connecticut landlords typically choose deductibles ranging from $1,000 to $10,000, and this single decision can swing your annual premium by hundreds of dollars. If you pick a $1,000 deductible, you’ll pay $1,000 toward any covered loss before your insurance kicks in. Jump to a $2,500 deductible, and you’ll see roughly 10 to 20 percent lower premiums. Push it to $5,000 or $10,000, and savings climb even higher-sometimes 25 to 30 percent off your yearly costs. The math seems straightforward until a pipe bursts in January or a tenant’s guest slips on your icy walkway. That’s when the deductible hits your bank account, not your insurer’s.

Assess Your Cash Position First

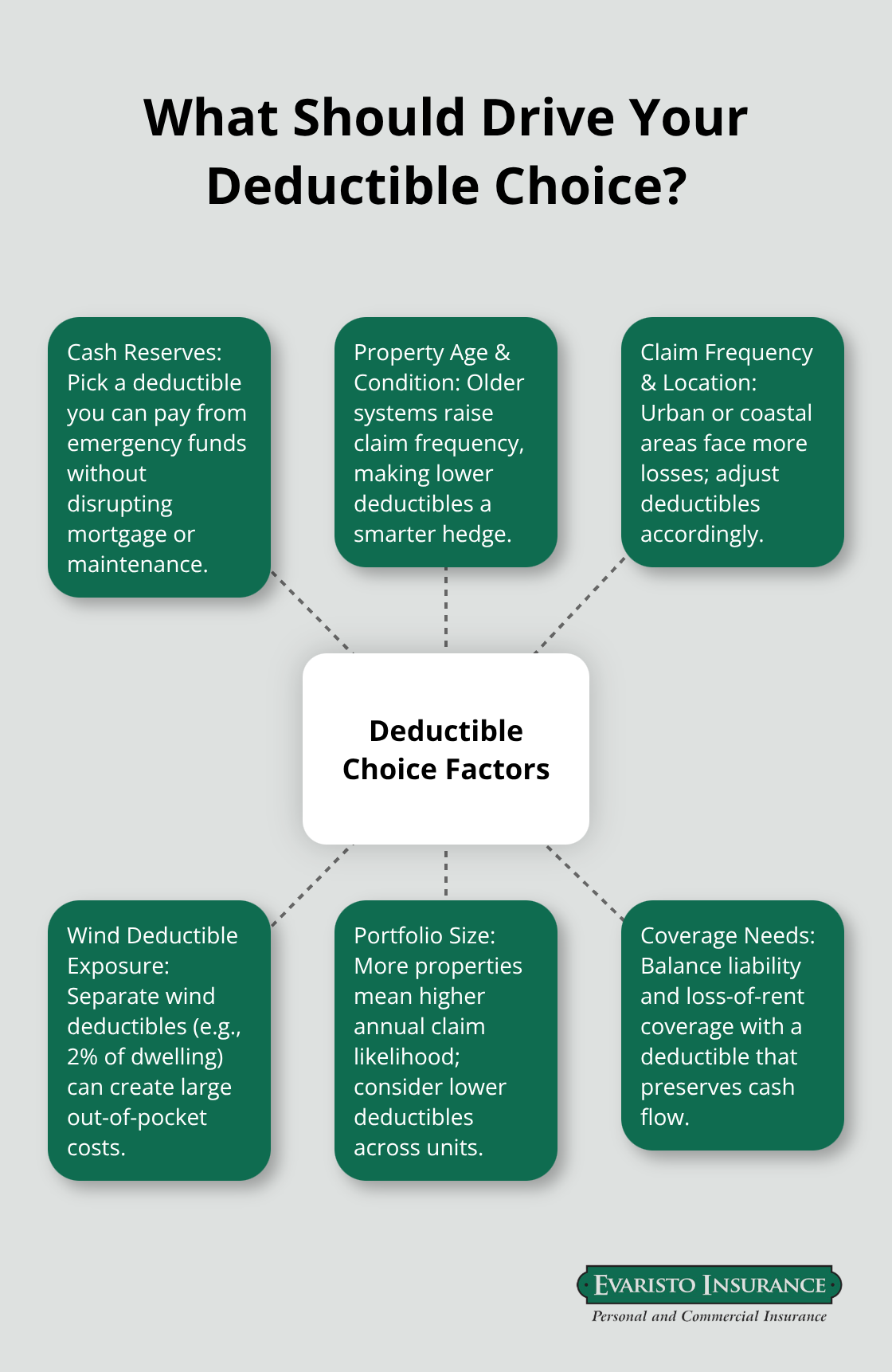

Connecticut landlords face genuine pressure to keep cash flowing, especially if you manage multiple properties or rely on rental income to cover mortgage payments. A $10,000 deductible saves money monthly, but only if you can actually afford to pay $10,000 when disaster strikes. Most financial advisors suggest keeping three to six months of operating expenses in reserve; your deductible should never exceed what sits in that emergency fund. If you own a three-bedroom home that generates $2,000 monthly rent, a $5,000 deductible feels manageable because you can cover it from two months of income. But if you carry higher debt or own multiple properties with tighter margins, that same $5,000 deductible becomes risky. Calculate your actual cash position, then work backward. If you have $8,000 available for emergencies, your deductible shouldn’t exceed that figure.

Account for Property Age and Condition

Property condition also matters significantly. Older Connecticut homes with aging plumbing and electrical systems file more claims, making a lower deductible a smarter hedge against frequent losses. A property built in 1970 will likely trigger more water damage claims than a 2010 construction. You can’t change your building’s age, but you can adjust your deductible to reflect the actual risk your property presents.

Compare Premium Savings Against Claim Costs

Comparing premium savings against potential out-of-pocket costs reveals that the lowest deductible isn’t always the cheapest strategy over time. A landlord paying $1,200 annually with a $1,000 deductible might spend $2,200 total in year one if they file a single $1,000 claim. That same landlord choosing a $5,000 deductible at $900 annually would pay $5,900 if a claim occurs, but $900 if it doesn’t. The real question is your claim frequency. Connecticut properties in urban areas like Hartford and New Haven historically file more claims due to higher tenant turnover, break-ins, and weather exposure. Coastal properties face elevated risk from nor’easters and storm surge.

Watch for Wind Deductibles

Wind deductibles deserve special attention in Connecticut-some insurers apply a separate 2 percent wind deductible, meaning a $400,000 dwelling coverage triggers an $8,000 out-of-pocket cost during hurricane season. That’s not a monthly premium choice; that’s a separate financial planning requirement. You need to account for this additional exposure when you evaluate your total deductible strategy.

Use Local Loss History to Guide Your Choice

If your property’s location or condition suggests higher claim probability, a lower deductible provides genuine protection. Review your property’s loss history and local risk factors before you lock in a deductible that might leave you exposed when you need coverage most. This analysis directly shapes how you’ll budget for landlord insurance and what coverage level actually makes sense for your situation.

How to Build a Realistic Landlord Insurance Budget

Calculate Your Dwelling Coverage from Replacement Cost

You need to establish your property’s replacement cost, not its market value. A three-bedroom Connecticut home worth $350,000 might cost $280,000 to rebuild after a total loss because land value doesn’t factor into reconstruction. Contact local contractors or use the Connecticut Department of Assessment Services to estimate current construction costs per square foot in your area. This number becomes your dwelling coverage limit and directly determines your premium baseline.

Factor in Loss of Rental Income and Liability Exposure

Once you know the replacement cost, multiply your annual rent by the number of months repairs would take after a covered event. If your property generates $24,000 yearly rent and typical water damage repairs take two months, you need $4,000 in loss of rental income coverage minimum. Add your liability exposure next. Properties with multiple units or frequent tenant turnover justify $500,000 to $1,000,000 in liability coverage because injury claims from guests or tenant injuries can exceed $100,000 quickly. Urban Hartford and New Haven properties historically see higher liability claims than suburban or rural Connecticut locations.

Run Deductible Scenarios Through Actual Quotes

Once you’ve identified these core coverage amounts, run deductible scenarios through actual carrier quotes. A $280,000 dwelling replacement cost with a $1,000 deductible might cost $1,100 annually, while a $5,000 deductible drops that to $850. That $250 monthly savings looks attractive until a frozen pipe claim arrives in February and you write a $5,000 check instead of $1,000. The real budget question is whether your cash reserves can absorb the higher deductible without forcing you to borrow money or skip property maintenance payments.

Account for Multiple Properties and Additional Coverage

Multiple properties change the math significantly because claim probability increases with portfolio size. A landlord managing three Connecticut properties faces roughly three times the annual claim likelihood of a single-property owner. This reality argues for lower deductibles on each property because you’ll statistically encounter claims more frequently. However, bundling multiple properties with the same carrier typically yields 10 to 25 percent total discounts, which can offset premium costs substantially. Adding other coverage types like wind, sewer backup, or equipment breakdown to your budget requires honest assessment of your property’s actual vulnerabilities. A 1985 colonial with original plumbing in a flood-prone Hartford neighborhood needs sewer backup coverage at $50 to $150 yearly, but a 2005 ranch on elevated ground in a low-risk zone probably doesn’t.

Plan for Coastal Wind Deductibles and Profit Margins

Connecticut’s coastal properties face mandatory separate wind deductibles that can run 2 percent of dwelling coverage, creating $4,000 to $8,000 out-of-pocket obligations during hurricane season. This isn’t optional budgeting-it’s a hard financial requirement if your property sits near Long Island Sound. Work backward from your total annual rental income to determine what deductible and coverage combination leaves you with acceptable profit margins after insurance costs. The next section shows you how to reduce those costs without sacrificing the protection your rental investment actually needs.

How to Cut Your Landlord Insurance Costs Without Sacrificing Coverage

Connecticut landlords leave money on the table constantly by accepting the first quote they receive. The insurance market in Connecticut includes over 40 carriers competing for rental property business, and premium differences for identical coverage routinely exceed 30 percent between the cheapest and most expensive options. A three-bedroom property might cost $1,200 annually with one carrier and $850 with another, making quote shopping the single highest-impact cost reduction strategy available to you. Compare multiple top carriers for every property because rate shopping yields savings faster than any deductible adjustment or property improvement. Start with at least five different insurers using your actual property details: dwelling replacement cost, liability limits, loss of rental income coverage, and your preferred deductible.

Most carriers now offer online quote tools that deliver estimates in minutes, eliminating the excuse that shopping takes too long. Document each quote with the carrier name, coverage limits, deductible, and annual premium, then compare apples to apples. You’ll frequently discover that a $5,000 deductible with Carrier A costs less than a $2,500 deductible with Carrier B, revealing that deductible strategy alone doesn’t determine your final cost.

Bundling Unlocks Hidden Discounts

Bundling your landlord policy with homeowners, auto, or umbrella coverage at the same carrier typically reduces your total premium by 10 to 25 percent according to most major insurers’ published discount structures. A Hartford landlord insuring both a primary residence and a rental property with separate carriers might pay $2,100 total annually, but bundling those policies at a single carrier could drop the combined cost to $1,680, saving $420 yearly with zero coverage changes. This bundling advantage compounds when you own multiple rental properties because each additional property added to your bundle increases your discount tier. Three properties bundled together often qualify for larger discounts than two properties, making portfolio consolidation financially sensible even if it requires switching carriers. However, bundling only works if the carrier offers competitive rates on all your coverage types. A carrier with cheap landlord insurance but expensive auto coverage might not deliver net savings, which is why comparing bundled quotes matters more than assuming bundling always wins.

Property Maintenance Reduces Your Premiums

Insurers reward landlords who maintain their properties because maintenance correlates directly with lower claim frequency. Installing monitored security systems typically qualifies you for 15 to 20 percent premium discounts when you document these improvements with photos and provide proof of monitoring. A $1,200 annual premium with a 15 percent maintenance discount saves $180 yearly, and that discount persists as long as you maintain the systems. Connecticut properties with updated electrical systems, modern plumbing, and functioning HVAC equipment file fewer claims than properties with original 1970s infrastructure, and insurers price this reality into their quotes. If your property has original wiring or cast iron drain pipes, upgrading these systems before you shop for insurance quotes can yield lower premiums that offset your upgrade costs within two to three years. Regular maintenance also prevents the small claims that accumulate over time; a frozen pipe claim at $2,000 costs you your deductible plus potential premium increases at renewal. Spending $500 annually on preventive maintenance like insulating exposed pipes, cleaning gutters, and servicing HVAC systems prevents claims that would otherwise trigger your deductible and raise your rates.

Final Thoughts

Your landlord insurance deductible in Connecticut shapes both your monthly budget and your financial security when claims arrive. The right choice balances premium savings against cash reserves you can actually access without disrupting your rental business. Higher deductibles cut your annual costs, but only if you can pay $5,000 or $10,000 out of pocket when a pipe bursts or a liability claim surfaces, while lower deductibles cost more monthly but protect your cash flow during emergencies.

Moving forward with your Connecticut landlord insurance requires three concrete actions: calculate your actual replacement cost and liability exposure rather than guessing at coverage amounts, run deductible scenarios through quotes from multiple carriers because premium differences routinely exceed 30 percent for identical coverage, and explore bundling opportunities and maintenance discounts that reduce your total costs by 10 to 25 percent without lowering your protection. These steps take a few hours but typically save hundreds of dollars annually. Contact Evaristo Insurance to compare quotes and build a landlord insurance deductible CT strategy that matches your financial reality and protects your investment.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.