Landlord Protection Strategies CT: Build Resilience for Rental Property

Connecticut rental property owners face mounting pressures from weather damage, tenant disputes, and income loss. These risks demand more than basic insurance-they require strategic landlord protection strategies CT that address your specific vulnerabilities.

At Evaristo Insurance, we’ve helped countless local landlords build resilience through comprehensive coverage and smart risk management. This guide shows you exactly how to protect your investment.

What Threatens Connecticut Rental Properties Most

Weather damage creates immediate financial exposure

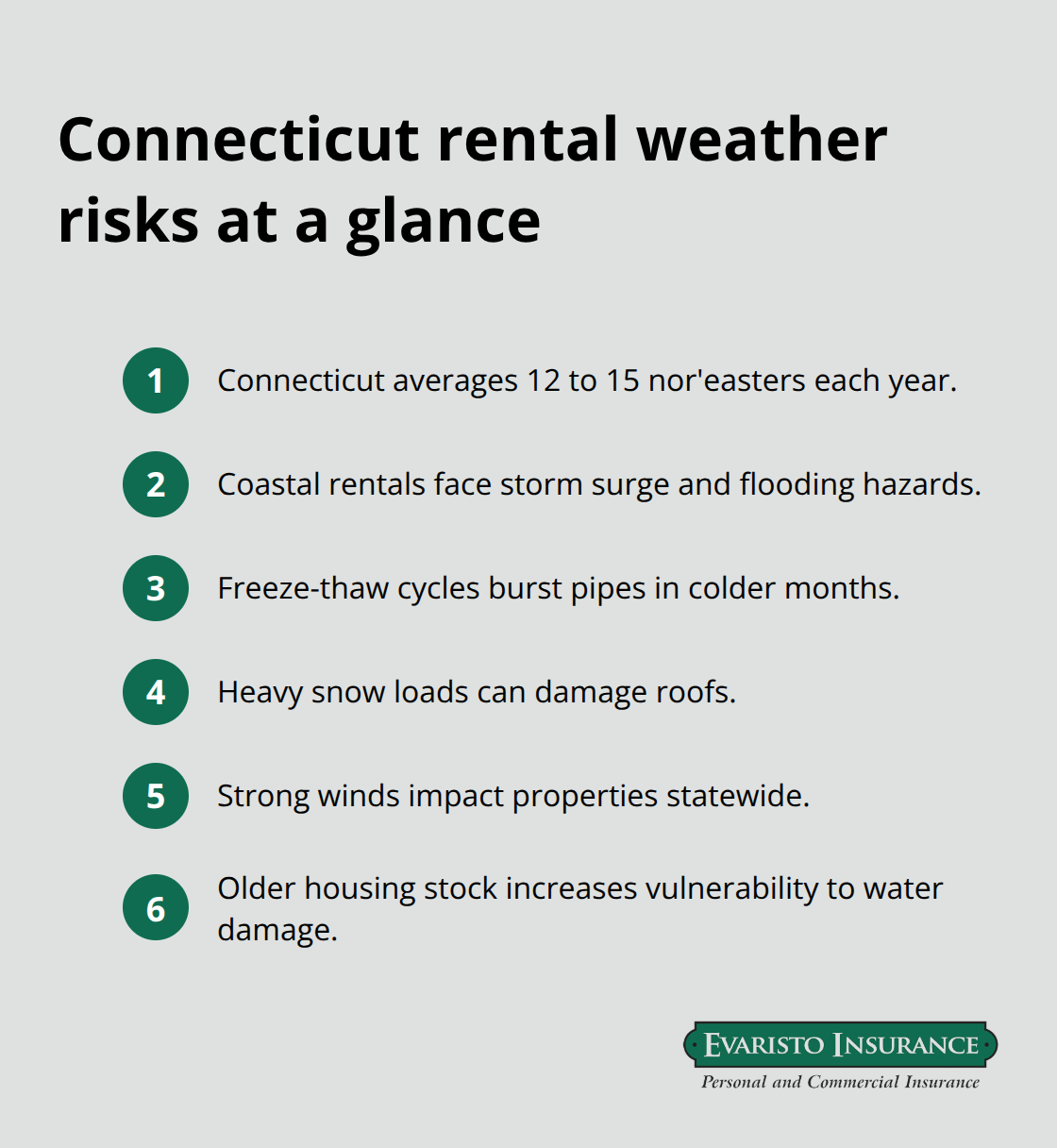

Connecticut experiences an average of 12 to 15 nor’easters annually, with coastal properties facing severe storm surge and flooding risk. Inland properties encounter different hazards: freeze-thaw cycles burst pipes, heavy snow loads damage roofs, and wind affects properties statewide. A single nor’easter can force a property offline for weeks, and standard landlord policies often exclude flood damage entirely. This coverage gap leaves landlords exposed to catastrophic losses.

Connecticut’s older housing stock amplifies weather vulnerability. Properties built before 1980 frequently have aging roofing systems, outdated plumbing, and electrical systems that fail under stress. Water damage claims represent the largest loss category for rental properties in the state, yet many landlords operate with inadequate or incomplete coverage.

Tenant disputes escalate quickly and cost more than expected

Connecticut’s Right to Counsel in Eviction Proceedings law means tenants who are income-eligible may have a free lawyer represent them, extending timelines and increasing legal costs. A contested eviction that once took 60 days now routinely stretches to 120 days or longer. Beyond eviction expenses, liability claims from tenant injuries create serious financial exposure. A slip-and-fall in a stairwell, an injury from a malfunctioning elevator, or a fire caused by inadequate smoke detectors at move-in can trigger six-figure settlements. Connecticut courts award damages aggressively, and landlords without solid liability protection face personal financial liability.

Security deposit disputes also drain resources. Connecticut law requires deposits held in escrow with specific notice procedures. Improper handling exposes landlords to claims for double the deposit amount plus attorney fees.

Vacancy losses compound financial pressure

A single month of vacancy costs roughly 8 to 10 percent of annual rental income when you account for lost rent plus turnover expenses (cleaning, repairs, and marketing). Extended vacancies-common during winter months or after tenant disputes-can cost landlords thousands. Loss-of-rent coverage exists specifically to address this, yet many standard policies either exclude it or limit it severely.

The combination of longer legal timelines, higher tenant protection standards, and income loss creates a financial squeeze that catches unprepared landlords off-guard. Understanding these specific threats allows you to evaluate whether your current coverage actually protects your investment or leaves critical gaps that could devastate your rental business.

What Your Connecticut Rental Property Actually Needs to Be Protected

Three layers of protection address different risks

Connecticut landlord insurance operates in three distinct layers, and most property owners misconfigure at least one. The building structure itself requires protection against the specific perils that damage Connecticut properties most frequently-fire, wind, hail, and theft. Your policy must cover the foundation, walls, roof, and permanently installed systems like furnaces and water heaters that you own. Many landlords assume their policy covers tenant-owned appliances, but it does not. If you provide a stove or refrigerator as part of the rental, that equipment needs explicit coverage under the landlord-owned contents section. Standard policies typically limit this coverage, so review your declarations page carefully.

The second layer is liability protection, which handles the expensive lawsuits that tenants or their guests file when someone gets injured on your property. Connecticut courts award substantial damages for serious injuries, and legal defense costs alone can exceed $50,000 before a case settles. Your policy should include medical payments coverage for minor injuries-this no-fault protection often prevents small incidents from escalating into lawsuits. The third layer is loss-of-rent coverage, which replaces income when a covered peril makes the property uninhabitable. Connecticut landlords frequently skip this, then suffer financially during the weeks or months needed for repairs after storm damage or fire.

State law sets minimum expectations, but lenders demand more

Connecticut state law does not mandate specific coverage amounts, but it does require that you maintain the property in reasonably safe condition and that you carry liability insurance if you have a mortgage. Most lenders require minimum limits of $100,000 for property damage and $300,000 for liability, though properties with multiple units justify higher limits. These minimums often fall short of actual exposure, particularly for multifamily buildings where injury claims multiply with each tenant.

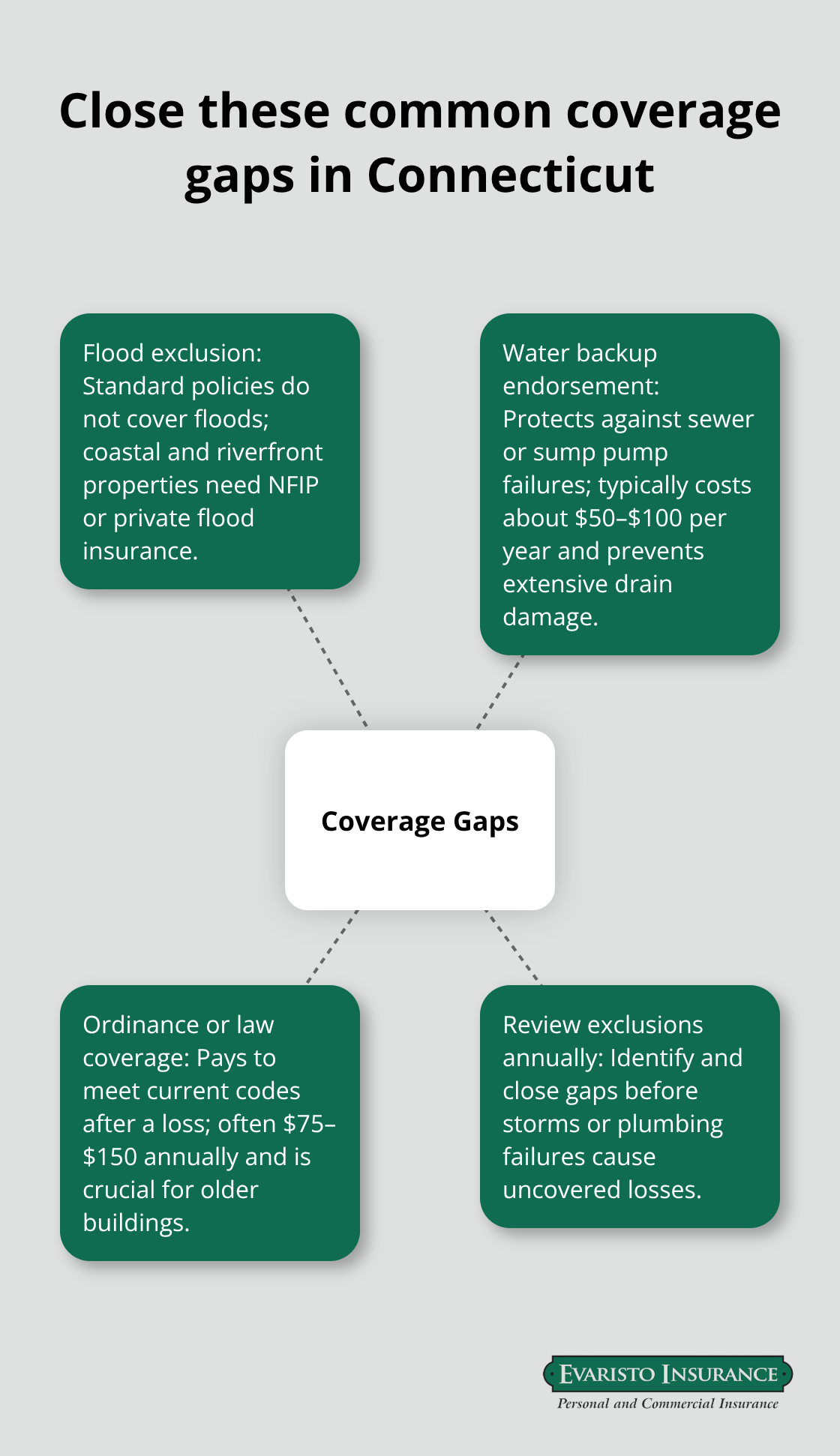

Critical exclusions leave landlords exposed

The real gap in most policies involves exclusions that Connecticut landlords do not anticipate. Standard policies exclude flood damage entirely-Connecticut’s coastal and riverfront properties need separate flood insurance through the National Flood Insurance Program or private carriers. Water backup from sewers or sump pump failures also requires a specific endorsement; this coverage costs roughly $50 to $100 annually but prevents catastrophic losses from backed-up drains. Ordinance or law coverage, typically an optional endorsement costing $75 to $150 per year, reimburses you for the cost of bringing a damaged building up to current building codes after a loss-essential for older Connecticut properties where code requirements have changed significantly since construction.

Vacancy terms and local expertise matter

Extended vacancy can void coverage or trigger premium increases, so verify your policy’s vacancy terms or add a vacancy endorsement if you expect turnover between tenants. A local Connecticut agent who understands regional risks delivers far more value than generic online quotes. The difference between adequate protection and a policy full of gaps often comes down to having someone who knows Connecticut’s specific weather patterns, older building stock, and legal environment review your landlord coverage against your actual property. As a second-generation, family-owned independent agency serving Connecticut since 1989, Evaristo Insurance compares multiple top carriers to deliver tailored protection that addresses these regional vulnerabilities.

Your coverage foundation is now in place, but protection extends far beyond the policy itself. How you manage your property day-to-day-through inspections, tenant screening, and maintenance-determines whether claims actually occur and whether your coverage performs when you need it most.

How to Stop Losses Before They Drain Your Rental Income

Inspections catch problems when repairs cost less

Property inspections catch problems when they cost $500 to fix instead of $15,000. Connecticut’s freeze-thaw cycles, coastal salt spray, and older building stock demand inspections at least twice annually-once before winter to address heating systems, pipe insulation, and roof condition, and once in spring to evaluate water intrusion, foundation cracks, and exterior damage from winter weather. You should document every inspection with photos and written notes. When a pipe bursts three months after your last inspection, your insurance claim strengthens significantly if you have timestamped evidence showing you identified and repaired similar vulnerabilities.

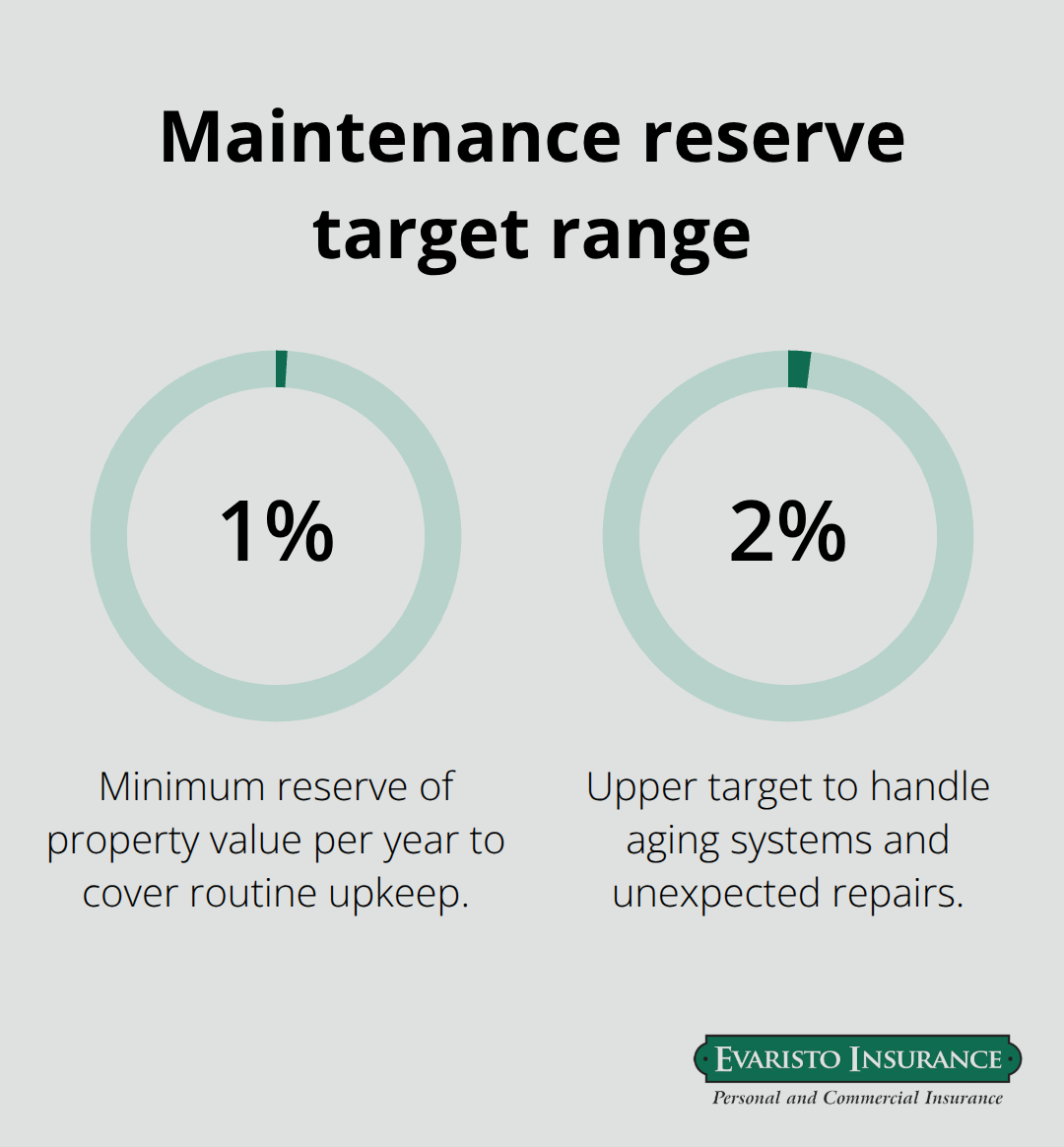

You need to create a maintenance calendar that schedules gutter cleaning before autumn leaves clog them, HVAC servicing before heating season, and smoke detector testing monthly. Set aside 1 to 2 percent of your property’s annual value for maintenance reserves. This approach prevents the scramble to fund repairs that triggers delayed fixes and tenant complaints.

Move-in documentation protects you against false claims

The Connecticut Department of Housing provides a free Pre-Occupancy Walk-Through Checklist that documents unit condition at move-in. You should use it. Photograph every wall, floor, appliance, and fixture. This checklist becomes your defense against tenant claims that you failed to address pre-existing damage. Many landlords skip this step, then face disputes over security deposit deductions or claims that conditions were unsafe at occupancy. The cost of 30 minutes with a camera is insignificant compared to the liability exposure of an undocumented move-in.

Tenant screening prevents months of eviction court

Tenant screening determines whether you spend months in eviction court or collect rent reliably. Connecticut’s Right to Counsel law means contested evictions now stretch to 120 days or longer, so preventing problem tenants matters more than ever. You should run criminal background checks and verify employment and income at a minimum. Tenants with verifiable income and clean records pay rent on time at high rates according to rental housing data.

You need to request references from previous landlords and call them directly rather than relying on written responses. Ask specifically about late payments, property damage, and lease violations. Check credit reports to identify patterns of unpaid obligations. Connecticut law permits reasonable screening fees; charge tenants for background checks to offset costs and signal that you take screening seriously.

You must document every screening decision in writing. If you reject an applicant, record your reasons. This protects you against fair housing complaints and demonstrates consistent, non-discriminatory practices. Many landlords make screening decisions casually, then face legal exposure when applicants claim discrimination. Standardized screening criteria applied uniformly to all applicants eliminate this risk.

Emergency response reduces claim costs and repair timelines

Emergency preparedness means knowing exactly how you will respond when a nor’easter floods a property or a pipe bursts in January. You should identify qualified contractors before emergencies occur. Get three estimates from plumbers, electricians, and water damage specialists while you have time to compare quality and pricing. When disaster strikes at midnight, you will not have time to solicit bids.

You need to store contractor contact information, your insurance policy number, and your agent’s direct line in a document you can access immediately. When a property becomes uninhabitable due to a covered peril, your loss-of-rent coverage only reimburses rent for the period the property is actually uninhabitable. Rapid response to repairs directly translates to lower claim costs. You should know your policy’s definition of uninhabitable and understand what repairs trigger coverage. If your policy requires professional assessment before coverage applies, arrange that assessment within hours of discovering damage, not days.

Final Thoughts

Connecticut rental property owners who implement these landlord protection strategies CT gain a decisive advantage over unprepared competitors. The combination of comprehensive insurance coverage, regular property maintenance, rigorous tenant screening, and emergency preparedness creates a resilience that protects both your income and your personal assets when problems occur. A single major claim or extended eviction can eliminate years of profit, while landlords who invest in proper coverage and smart risk management rarely face catastrophic losses because they catch problems early and respond quickly.

Your insurance policy forms the foundation, but it only performs when you configure it correctly for Connecticut’s specific risks. Standard policies leave critical gaps-flood exclusions, water backup gaps, and inadequate loss-of-rent limits are common mistakes that landlords discover only after a loss occurs. Ordinance or law coverage, vacancy endorsements, and liability limits that match your actual exposure require deliberate choices, not default selections.

Professional guidance accelerates this process significantly. An agent who understands Connecticut’s weather patterns, older building stock, and legal environment identifies gaps that generic online quotes miss entirely. Contact Evaristo Insurance for a comprehensive coverage review that evaluates your current policy against your actual property risks, identifies exclusions and gaps, and recommends endorsements that close vulnerabilities.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.