CT Landlord Protection Plan: Which One Fits Your Portfolio

Connecticut landlords face a critical decision: selecting the right coverage for their rental properties. A CT landlord protection plan isn’t one-size-fits-all, and choosing poorly can leave you exposed to significant financial losses.

At Evaristo Insurance, we’ve helped countless property owners in Connecticut navigate these options. This guide breaks down the coverage types available, compares plans from different carriers, and shows you how to build protection that matches your specific portfolio.

What Connecticut Landlord Insurance Actually Covers

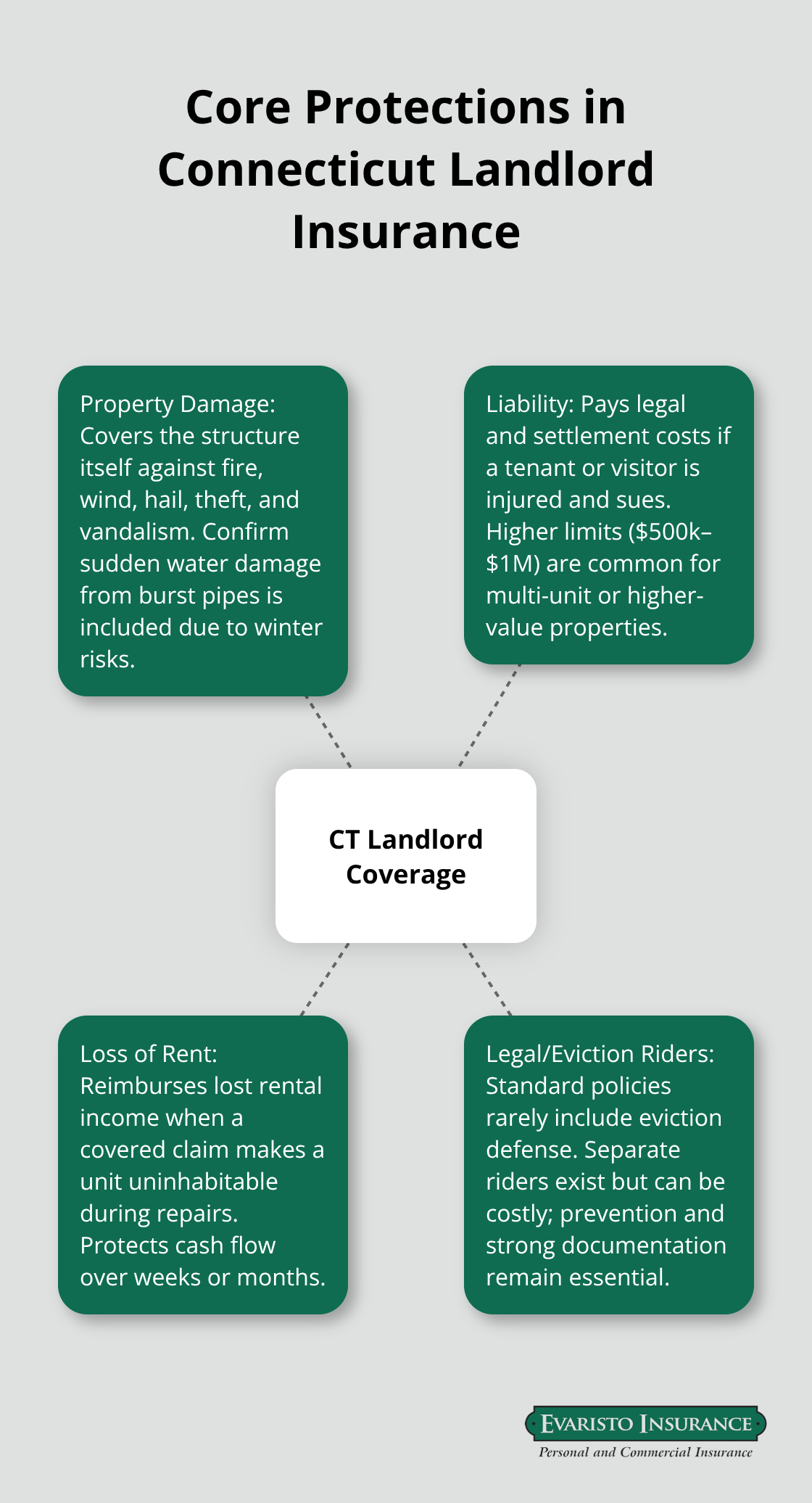

Property Damage Protection

Connecticut landlord insurance protects three distinct areas of your rental business, and understanding each one prevents expensive gaps in coverage. Property damage protection covers the building structure itself-the walls, roof, foundation, and permanent fixtures-against fire, wind, hail, theft, and vandalism. Connecticut experiences about 45 inches of snow annually and frequent nor’easters, making burst pipes and water damage from ice dams serious threats. You must confirm your policy explicitly covers sudden water damage from burst pipes, because this accounts for a substantial share of winter claims in the Northeast.

Liability Protection for Tenant and Visitor Injuries

Liability protection shields you when a tenant or visitor is injured on your property and sues. Connecticut’s tenant-friendly laws and right-to-counsel provisions under Public Act 21-34 mean litigation costs climb quickly. A $300,000 liability limit is the bare minimum; many landlords with multiple units or higher-value properties carry $500,000 to $1,000,000 in liability coverage. This protection directly addresses the financial exposure that Connecticut’s legal environment creates for property owners.

Loss of Rent Coverage

Loss of rent coverage reimburses you when a covered event-fire, burst pipes, storm damage-makes a unit uninhabitable and you lose tenant income during repairs. This coverage protects your cash flow during the weeks or months needed for repairs, which is why it matters more than many landlords realize. Without it, you absorb the full financial impact of vacancy while paying for repairs.

Eviction Costs and Legal Defense

Connecticut landlord policies rarely cover legal defense costs for evictions or tenant disputes without a separate rider. Eviction insurance exists but tends to be expensive and subject to high deductibles, so most landlords skip it. Instead, focus on prevention through strong tenant screening and thorough lease documentation using Connecticut’s official multilingual forms from the Department of Housing. If you face an eviction, costs can exceed $2,000 to $5,000 once attorney fees and court costs accumulate.

Premium Costs and Carrier Comparison

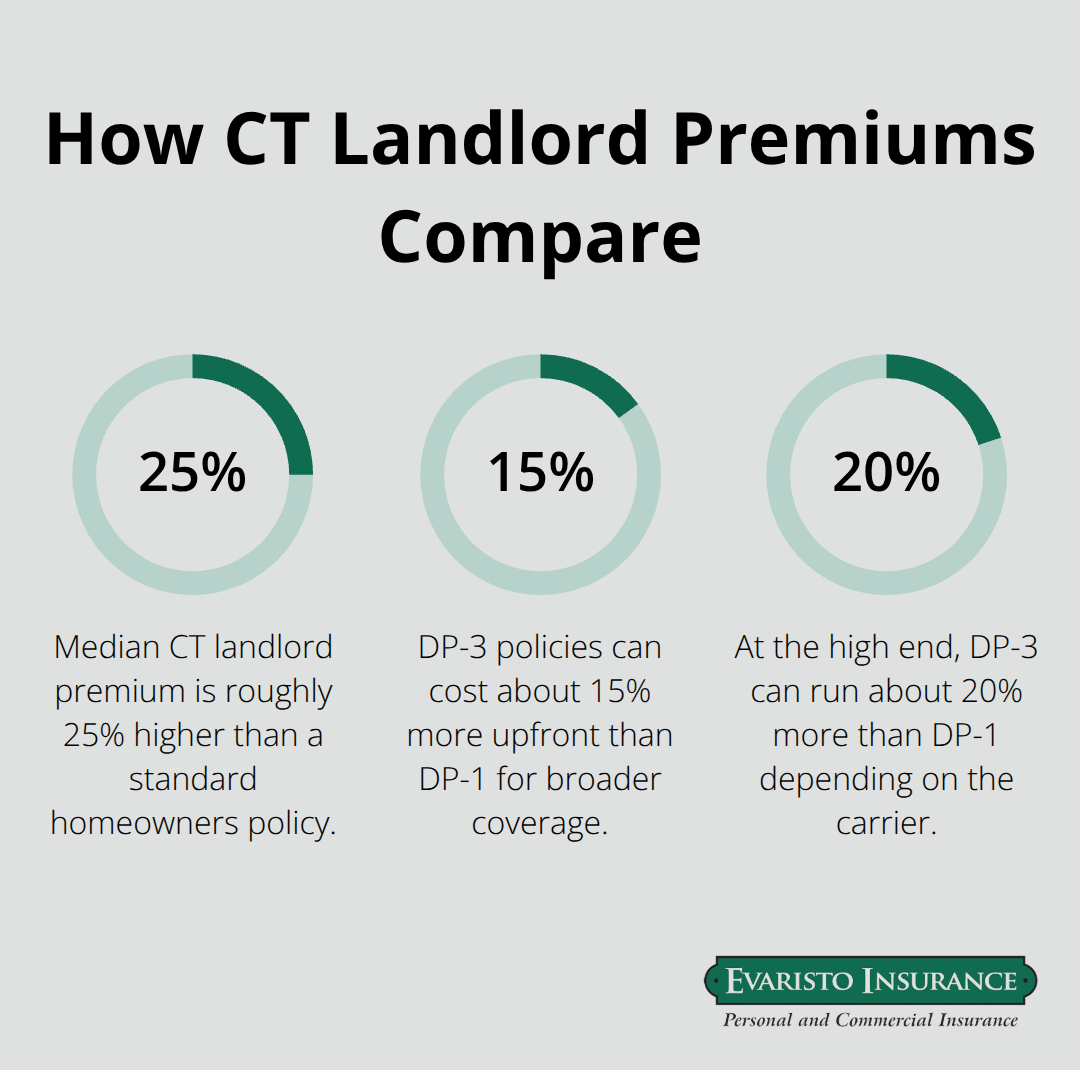

Connecticut’s median landlord insurance premium sits at about $2,610 annually according to Steadily data, roughly 25% higher than a standard homeowners policy. Your actual premium depends on property age, location, crime rates, number of units, and whether you add endorsements for water backup, equipment breakdown, or building code coverage. Single-family rentals typically cost less to insure than multi-unit properties, but multi-unit portfolios often qualify for volume discounts that offset the higher base rate.

Carriers like Travelers, Progressive, and Safeco operate in Connecticut with established claims networks, and comparing them through an independent agent ensures you’re not overpaying for the protection you actually need.

What Connecticut Landlords Actually Pay for Coverage

Connecticut landlords shopping for protection quickly discover that standard landlord policies differ significantly in what they cover and what they cost. The median premium masks real variation-single-family rentals in low-crime areas run $1,800 to $2,200 per year, while multi-unit properties in urban centers like Hartford or New Haven often exceed $3,500. The difference stems from what the base policy includes versus what requires add-ons. Most carriers in Connecticut offer two main tiers: broader DP-3 coverage that includes water damage, theft, and vandalism by default, or stripped-down DP-1 policies requiring you to purchase these protections separately. A DP-3 policy costs roughly 15 to 20 percent more upfront but eliminates surprise gaps when a frozen pipe or break-in occurs. Carriers like Travelers and Safeco operate throughout Connecticut’s market, but their pricing varies based on how they assess local weather risk and claim frequency. An independent agent shopping multiple carriers typically finds 10 to 25 percent premium differences for identical coverage limits, meaning comparison shopping directly impacts your bottom line.

Building Code Coverage Protects Older Properties

Building code coverage, often called ordinance or law endorsement, pays for upgrades required by current code after a loss-a protection that matters for Connecticut’s older housing stock where pre-1980 homes represent a substantial portion of rentals. Without this endorsement, you absorb code compliance costs out of pocket after fire or storm damage, sometimes adding $15,000 to $40,000 to repair expenses. Connecticut’s freeze-thaw cycles and coastal weather patterns trigger claims that activate this coverage regularly, making it more than theoretical protection for property owners in this region.

Water Backup and Equipment Breakdown

Water backup and sump pump overflow coverage protects against the exact scenario many Connecticut landlords face during spring snowmelt or heavy rain, yet fewer than half of landlords carry it. This single endorsement costs $150 to $300 annually but prevents $10,000-plus claims from backed-up sewers or overwhelmed pumps. Equipment breakdown coverage extends protection to major appliances and HVAC systems you own, particularly valuable if you furnish units with refrigerators or heating systems. These two endorsements address the weather patterns and property conditions that generate the highest claim frequency in Connecticut.

Loss-of-Rent Limits Require Careful Attention

Loss-of-rent limits deserve specific attention because standard policies often cap this at $2,500 per month or less, insufficient for a multi-unit property where repairs stretch across several months. Increasing your loss-of-rent limit to match actual monthly income requires minimal premium adjustment but protects cash flow when a fire or burst pipe sidelines units during peak rental season. A landlord with three units generating $1,500 each monthly needs a $4,500 loss-of-rent limit to maintain income protection during extended repairs. Your next step involves matching these coverage options to your specific property type and tenant profile-a process that separates adequate protection from overpriced policies that leave gaps exactly where you need them most.

Matching Coverage to Your Rental Reality

Document Your Property and Income Profile

Your rental property’s age, location, and tenant mix determine which coverages matter most, and selecting the wrong protections costs thousands annually in either premiums or claim denials. A single-family home in a low-crime suburb requires different protection than a three-unit building in Hartford or a furnished short-term rental property. Start by documenting your property specifics: construction year, square footage, number of units, whether you furnish units, proximity to flood zones, and average monthly rental income per unit. Properties built before 1980 need building code coverage because Connecticut’s older housing stock frequently triggers code compliance costs after fire or storm damage-without this endorsement, you pay out of pocket for required upgrades.

Assess Weather and Water Damage Exposure

Connecticut’s 45 inches of annual snowfall and coastal nor’easters mean burst pipes and water backup claims hit landlords regularly, making water damage coverage non-negotiable for any property north of I-95. If your units generate $1,500 monthly rent each and you own three units, your loss-of-rent coverage must reach $4,500 monthly-standard policies capping this at $2,500 leave you severely underinsured. Furnished rentals demand landlord-owned contents coverage for appliances and furniture you provide, while unfurnished units skip this expense entirely.

Evaluate Your Tenant Profile and Risk Factors

Document your tenant profile too: turnover rates, background check results, prior eviction claims, and whether tenants historically maintain renters insurance. High-turnover properties with marginal tenant screening histories justify higher liability limits because problem tenants create proportionally higher injury and damage risk.

Identify Coverage Gaps in Your Current Policy

Your current policy likely contains gaps that surprise you during claims. Request a detailed coverage summary from your carrier showing exactly what perils your policy covers, what limits apply to loss of rent, and which endorsements you currently hold. Many Connecticut landlords discover mid-claim that their DP-1 base policy requires separate purchase of water backup, equipment breakdown, or ordinance coverage-costs they avoided upfront but regret when a frozen pipe floods a unit during February repairs.

Compare your loss-of-rent limits against actual monthly income; if your policy pays $2,500 monthly but you lose $4,500 in rent during a three-month repair cycle, that $7,500 gap comes directly from your pocket. Check whether your liability limit reflects your total portfolio value-a $300,000 limit works for single-family rentals but leaves owners of multi-unit properties dangerously exposed in Connecticut’s litigation-heavy environment. An independent agent shopping your property against Travelers, Safeco, and Progressive pricing reveals 10 to 25 percent premium differences for identical limits, meaning your current renewal rate may simply reflect carrier inertia rather than competitive value.

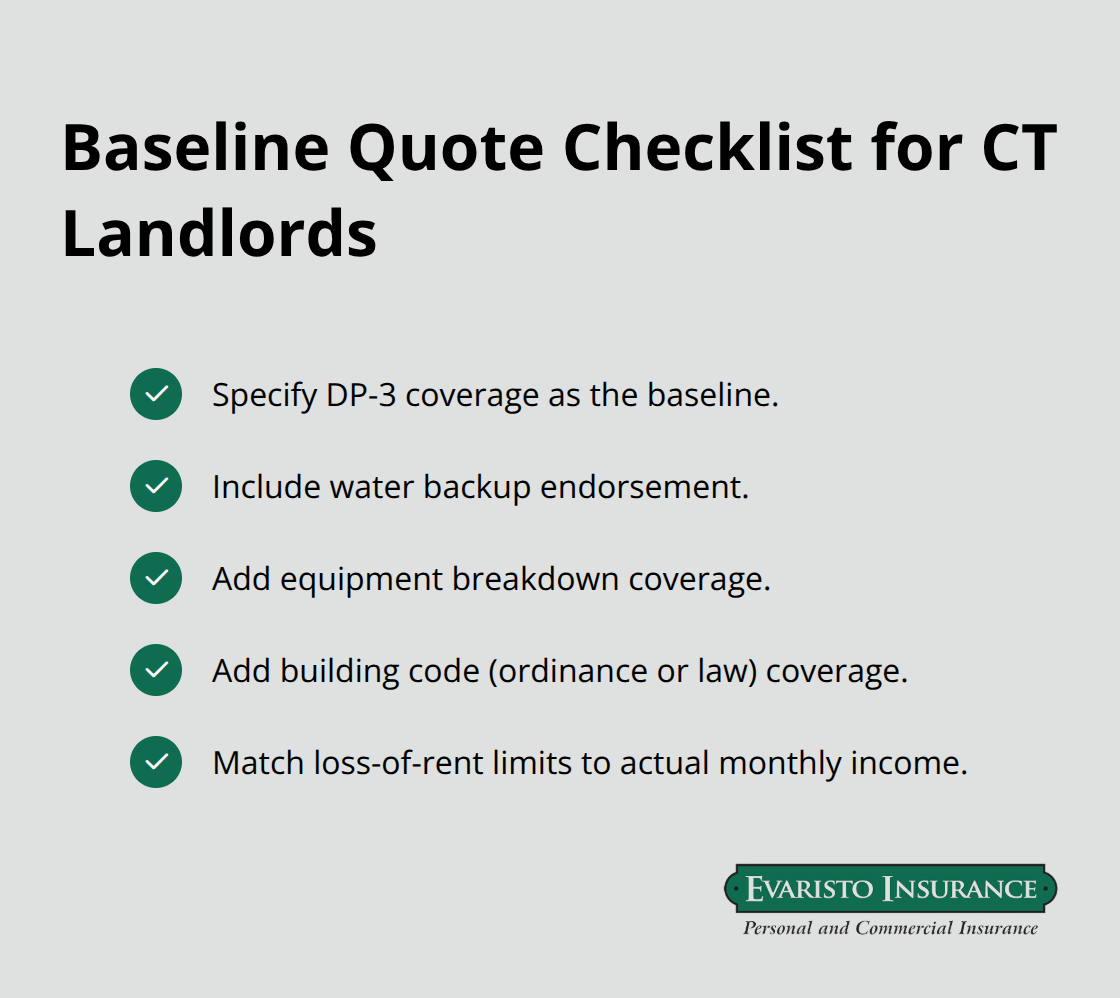

Shop Multiple Carriers with Specific Coverage Baselines

Request quotes specifying DP-3 coverage with water backup, equipment breakdown, building code endorsement, and loss-of-rent limits matching your actual income-this comparison baseline prevents you from selecting plans based on price alone without understanding what protection you sacrifice.

Final Thoughts

Selecting the right CT landlord protection plan requires matching coverage limits to your actual property income and assessing weather exposure specific to Connecticut’s climate. Your property age, location, and tenant profile determine which endorsements matter most-building code coverage for older homes, water backup for properties vulnerable to spring snowmelt, and loss-of-rent limits that reflect actual monthly income. Connecticut’s median landlord insurance premium of $2,610 annually masks significant variation based on what each policy includes versus what requires separate purchase, so a DP-3 policy with water backup and equipment breakdown costs roughly 15 to 20 percent more upfront but eliminates expensive gaps when frozen pipes or break-ins occur.

Local expertise matters in Connecticut because our state’s tenant-friendly laws, freeze-thaw cycles, nor’easters, and older housing stock create specific protection needs that national carriers often underestimate. An independent agent familiar with Connecticut’s rental market identifies coverage gaps that surprise landlords mid-claim and negotiates competitive pricing across multiple carriers-typically finding 10 to 25 percent premium differences for identical limits. We at Evaristo Insurance have served Connecticut landlords for decades, comparing top carriers from our local offices to deliver tailored protection that matches your portfolio rather than forcing you into generic plans.

Your next step involves documenting your property specifics, current coverage limits, and actual monthly income, then requesting detailed quotes from multiple carriers specifying DP-3 coverage with the endorsements your property requires. Contact Evaristo Insurance to review your current policy against competitive options and build protection that addresses Connecticut’s specific risks without overpaying for coverage you don’t need.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.