Connecticut Cyber Liability Insurance: Safeguarding Your Data and Reputation

Connecticut businesses face a growing threat from cyber attacks that can cripple operations and destroy customer trust. Data breaches cost companies an average of $4.45 million per incident, according to IBM’s 2024 Cost of a Data Breach Report.

At Evaristo Insurance, we help Connecticut business owners protect themselves with cyber liability insurance that covers the real costs of attacks-from notification expenses to legal defense and lost income. The right coverage strategy makes the difference between recovery and collapse.

Why Your Connecticut Business Is a Target

Cyber Attacks Hit Connecticut Businesses Hard

Cyber attacks on Connecticut small and medium businesses aren’t rare anymore-they’re routine. According to FBI’s 2024 Internet Crime Complaint Center data, phishing and spoofing remain the most common attack types. Connecticut itself recorded 158 cybercrime victims per 100,000 population in 2020, with an average loss of $7,330 per victim. The FBI estimates only about 15% of cybercrime incidents get reported, meaning the actual damage in Connecticut is significantly higher than official statistics show.

Your Company Size Offers No Protection

Verizon’s 2025 Data Breach Investigations Report found that 83% of breaches involved small- to mid-sized businesses. The average U.S. data breach now costs $10.22 million according to IBM’s Cost of a Data Breach Report 2025, with insider and vendor-related breaches among the most expensive. Human-operated ransomware attacks surged about 275% in one year based on Microsoft data, and ransomware incidents increased 38% between 2023 and 2025 per IBM X-Force Threat Intelligence Index. These aren’t hypothetical threats-they’re happening to Connecticut businesses right now.

The Hidden Costs of a Breach Extend Far Beyond Recovery

The financial hit from a breach extends far beyond immediate recovery costs. Your company faces notification expenses mandated by Connecticut data privacy laws, potential regulatory fines, legal defense costs if customers sue, business interruption losses while systems are restored, and the invisible but devastating cost of lost customer trust. Accenture projects cybercrime costs could exceed $10.5 trillion annually by 2026, reflecting the reality that every business is exposed.

Connecticut’s older victims suffer the largest losses: those aged 50–59 experienced average losses of $20,388 in 2020, and those 60+ lost $10,071 on average. This matters if your company employs or serves older employees and clients. Traditional general liability policies simply don’t cover cyber risks, leaving you exposed regardless of your other insurance. Without dedicated cyber liability coverage, a single breach drains your cash reserves, forces operational shutdowns, and damages your market reputation permanently.

Why Standard Insurance Falls Short

Cyber liability insurance isn’t optional for Connecticut businesses handling customer data, payment processing, or any sensitive information-it’s the only realistic way to transfer that financial and operational risk to an insurer prepared to handle the full scope of modern cyber threats. Understanding what coverage actually protects your business requires knowing exactly what cyber liability policies cover.

What Your Cyber Liability Policy Actually Covers

First-Party and Third-Party Coverage: Know the Difference

Cyber liability insurance splits into two critical parts: first-party coverage that pays your direct losses, and third-party coverage that protects you against claims from customers or business partners harmed by your breach. Understanding this distinction matters because a policy strong in one area might leave you exposed in the other. First-party coverage handles the immediate financial wreckage after an attack-forensic investigation to determine how attackers entered your systems, mandatory notification costs to alert affected customers under Connecticut data privacy laws, credit monitoring services for those customers, business interruption losses while you restore operations, data restoration and recovery expenses, and public relations support to rebuild your reputation. Third-party coverage protects against lawsuits and regulatory action when a breach exposes customer data, covers settlement costs if customers sue for identity theft or privacy violations, pays legal defense expenses as regulators investigate, and covers fines or penalties Connecticut authorities impose.

The distinction matters practically: a ransomware attack that shuts down your operations for two weeks creates massive first-party losses from lost revenue and recovery costs, but minimal third-party exposure. A breach exposing customer payment card data creates the opposite-massive third-party liability from customer lawsuits and regulatory action, but potentially lower first-party costs if you recover quickly.

Ransomware and Cyber Extortion Coverage

Cyber extortion and ransomware attacks warrant specific attention because they’ve become the fastest-growing threat Connecticut businesses face. Human-operated ransomware attacks are by and large financially motivated through extortion, ransomware, and data theft. When criminals encrypt your files and demand payment, cyber liability coverage pays the ransom negotiation process, forensic analysis to understand the attack, system restoration after you regain access, and business interruption losses during the shutdown. Many policies include coverage for extortion threats even without an actual breach, protecting you if criminals threaten to release data they claim to possess.

Verify your policy explicitly covers ransomware response and negotiation, because some carriers exclude ransom payments or limit coverage to investigation costs only. This verification step separates adequate protection from inadequate coverage.

Legal Defense and Liability Protection

Legal defense costs when customers file lawsuits after a breach often exceed settlement amounts. Your policy must include legal defense costs as a covered expense, not as a deductible that reduces your overall limit. Some policies cap legal defense spending or exclude certain types of claims, leaving you vulnerable to regulatory investigations or class-action lawsuits that consume your coverage limits rapidly.

Ensure your coverage includes vendor risk management and mobile device protection relevant to your specific operations. Policies vary widely in what forensic firms, legal counsel, and notification vendors they reimburse, and these variations directly impact your actual protection level.

Evaluating What Your Policy Actually Covers

Review your policy’s definition of covered incident response services carefully, because gaps in coverage create dangerous blind spots. A policy that covers forensic investigation but excludes business interruption leaves you paying recovery costs while losing revenue simultaneously. A policy that covers notification costs but excludes credit monitoring fails to address the full scope of customer protection Connecticut data privacy laws require. The most common mistake Connecticut business owners make is assuming their policy covers everything cyber-related when it actually excludes specific attack types, response services, or cost categories.

Your next step involves assessing your specific industry risks and matching them to the right coverage limits and deductibles for your operation.

Matching Coverage to Your Real Business Risks

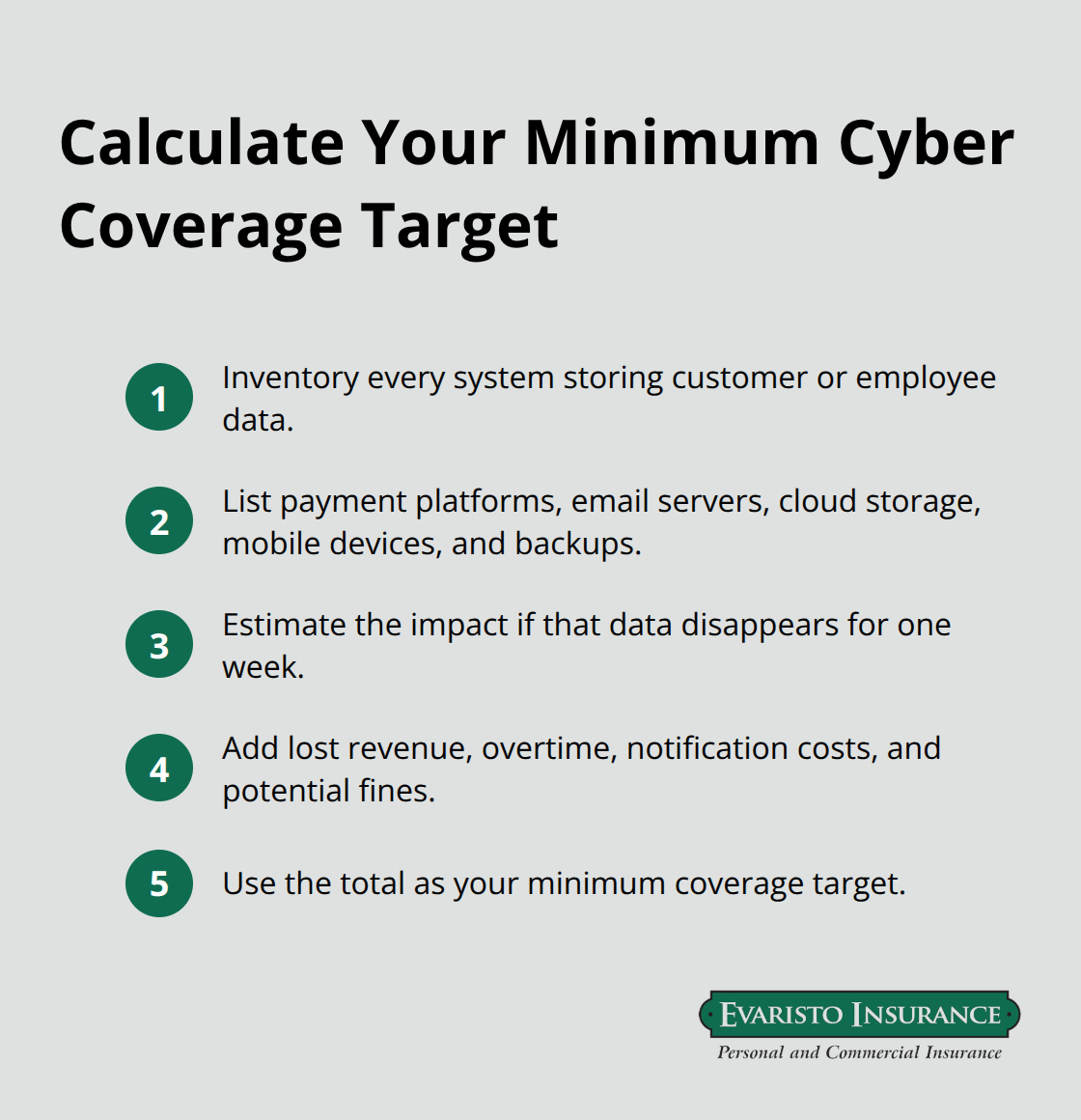

Inventory Your Data and Calculate Your Exposure

Selecting cyber liability coverage starts with brutal honesty about what data your Connecticut business actually handles and what happens if that data disappears or leaks. A plumbing contractor storing customer names and phone numbers faces vastly different exposure than a medical practice holding patient records and insurance information. Many Connecticut business owners overpay for coverage they don’t need while leaving critical gaps in what they do need.

Start by inventorying every system that stores customer or employee data-payment processing platforms, email servers, cloud storage, mobile devices used by field staff, and backup systems. Next, calculate the financial impact if that data disappeared for one week.

Include lost revenue from operational shutdown, overtime costs to restore systems, notification expenses mandated by Connecticut data privacy laws, and potential regulatory fines. That number becomes your minimum coverage target.

Match Coverage Limits to Your Business Size and Industry

Connecticut small businesses with $1 million in annual revenue typically need $1 million to $2 million in cyber liability coverage, though this varies dramatically by industry. A contractor handling payment cards needs higher limits than one accepting checks. A healthcare provider needs substantially higher coverage than a retail business. The mistake most Connecticut owners make is choosing coverage limits based on what their competitors carry rather than what their specific operations require.

Your coverage target should reflect your actual financial exposure, not industry averages. A business processing high volumes of customer payment data faces greater liability than one collecting only contact information. Calculate your potential loss realistically, then add 20% as a safety margin.

Choose Deductibles You Can Actually Afford

Deductibles matter more than many business owners realize because they directly affect your out-of-pocket costs during a breach. A $10,000 deductible sounds manageable until you’re actually recovering from ransomware and facing $50,000 in immediate forensic investigation costs before your insurance kicks in. We recommend Connecticut businesses evaluate their cash reserves and choose deductibles they can genuinely afford to pay within 48 hours of a breach, since recovery speed determines your ultimate financial damage.

Higher deductibles lower your premiums but increase your risk during the critical hours after an attack when you need immediate response resources. The timing matters because forensic firms and incident response teams demand payment upfront, before your insurer reimburses you.

Scrutinize Policy Exclusions and Verify Vendor Coverage

Policy exclusions create the real danger, so review them carefully. Some carriers exclude coverage for incidents involving unpatched software, meaning if attackers exploited a known vulnerability you hadn’t yet fixed, you pay the entire cost yourself. Others exclude insider threats or limit coverage for vendor-related breaches. Connecticut businesses relying on third-party vendors for payment processing or data storage should absolutely verify their policy covers vendor risk management.

Mobile device protection matters specifically for contractors and field service businesses whose employees access customer data on phones and tablets outside secure office networks. Request sample policies from multiple carriers and compare their specific exclusions side by side, because two policies with identical coverage limits can offer dramatically different protection. The exclusions determine what you actually pay out of pocket when an incident occurs.

Work with a Local Agent Who Understands Connecticut Requirements

Working with a local Connecticut insurance agent who understands state-specific data privacy requirements, regulatory trends, and industry-specific exposures transforms this process from overwhelming to strategic. An agent who knows Connecticut’s data breach notification requirements, understands which local industries face elevated cyber risk, and has relationships with carriers offering customized coverage for your specific business type provides value far beyond simply quoting premiums. At Evaristo Insurance, we serve Connecticut businesses from our local offices in Ellington and West Hartford, comparing multiple top carriers to deliver tailored protection that matches your actual exposure and budget.

Final Thoughts

Cyber threats targeting Connecticut businesses accelerate every year. Ransomware attacks increased 38% between 2023 and 2025, business email compromise scams caused $2.8 billion in losses in 2024, and phishing remains the most frequent attack vector. Your Connecticut business faces real exposure regardless of size or industry, and the financial consequences of being unprepared extend far beyond immediate recovery costs.

Connecticut cyber liability insurance protects your bottom line by transferring the financial burden of breach response, legal defense, notification costs, and business interruption to an insurer equipped to handle modern cyber threats. The right policy covers forensic investigation, customer notification mandated by Connecticut data privacy laws, regulatory fines, legal settlements, and lost revenue during system restoration. Without this protection, a single incident drains your cash reserves, forces operational shutdowns, and damages customer trust permanently.

Contact Evaristo Insurance to assess your cyber exposure, review your coverage gaps, and receive a recommendation for Connecticut cyber liability insurance that protects what you’ve built. Our local offices in Ellington and West Hartford connect you with agents who understand Connecticut’s regulatory environment and your industry’s specific risks. We’ve served Connecticut businesses since 1989, comparing multiple top carriers to deliver tailored protection that matches your actual exposure and budget.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.