Small Business Cyber Liability: Securing Your Connecticut Operations

Small business cyber attacks in Connecticut are rising faster than most owners expect. Criminals target companies like yours because they know smaller teams often lack robust defenses and the budget to fight back.

We at Evaristo Insurance see this threat firsthand, and we know the financial damage can be devastating. The right cyber liability coverage combined with solid security practices is what separates businesses that recover quickly from those that don’t.

Why Small Businesses in Connecticut Attract Cyber Attackers

Connecticut small businesses face three hard realities that make them attractive targets. First, attackers know you lack the security infrastructure of larger enterprises. Phishing remains the easiest and most common attack vector-attackers impersonate trusted entities to obtain sensitive data or deploy malware, leading to breaches and downtime. Second, the shift to remote work since the pandemic has created security gaps that criminals actively exploit. Remote-work vulnerabilities have grown significantly, and attackers now use AI-assisted social engineering to mimic communications with industry-specific triggers that prompt rushed responses. Third, the financial impact of a breach hits smaller operations harder because you lack reserves to absorb the costs.

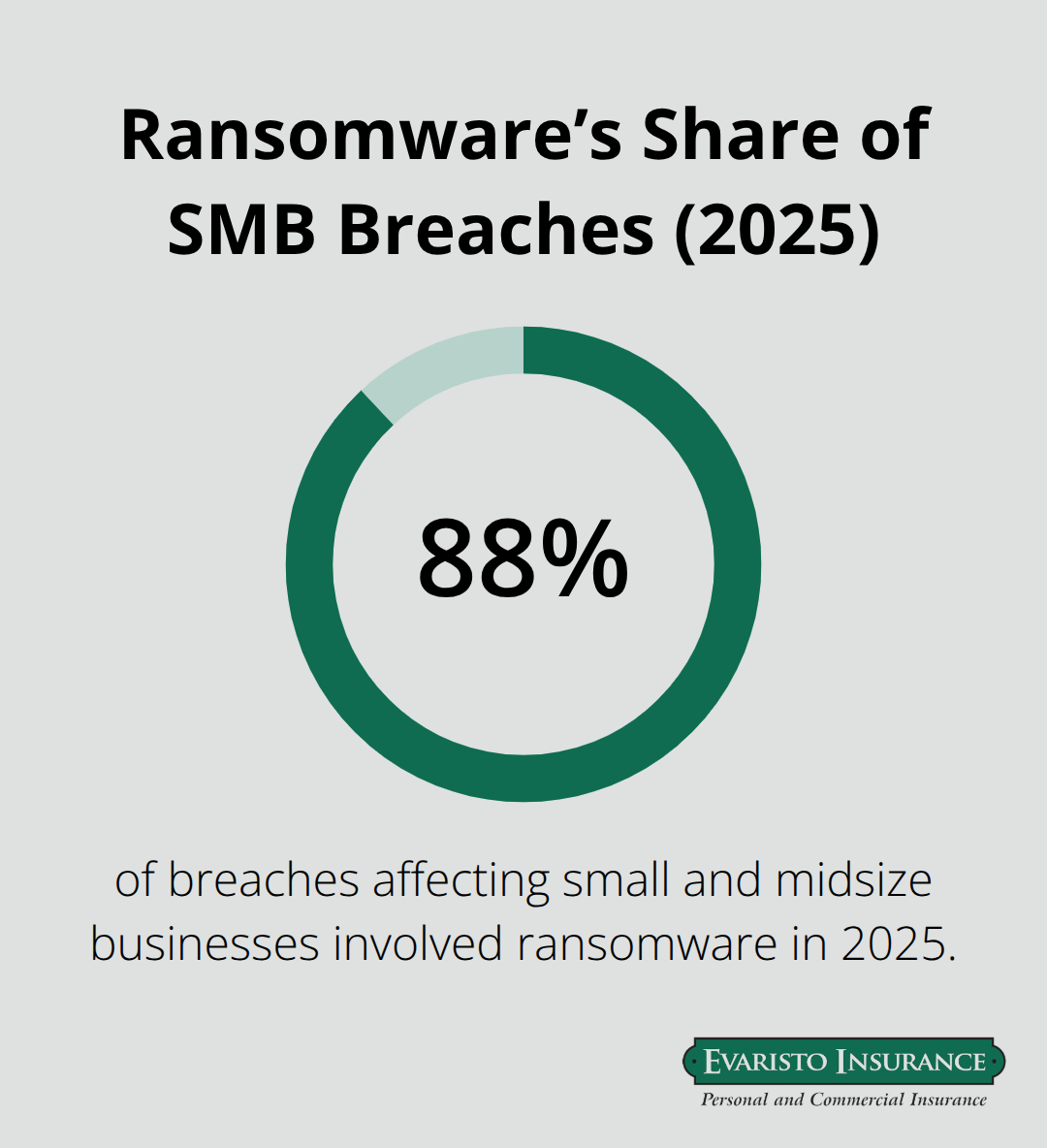

Ransomware attacks have evolved to target small and midsize businesses, with ransomware involved in 88% of all breaches affecting them in 2025.

Limited budgets create wider security gaps

Your security budget is typically a fraction of what larger corporations spend, which means attackers see you as low-hanging fruit. Connecticut’s DoD-related supply chain and sensitive data handling in insurance and financial services create high-value targets, but supply chain attacks also rise to target small and medium-sized businesses to reach larger partners. This means even if you don’t handle classified data, your vulnerability could expose your larger clients. Without robust defenses like multi-factor authentication, email filtering, and endpoint detection and response tools, you rely on luck rather than protection.

Downtime and notification costs drain cash reserves

A single ransomware incident or data breach halts your operations and forces you to spend thousands on incident response, forensics, data restoration, customer notification, credit monitoring services, and regulatory defense. Connecticut law requires notification to affected residents within 60 days of discovery, and if you compromise a resident’s Social Security number, you must offer 24 months of credit monitoring services. Failure to comply with these notice requirements violates the Connecticut Unfair Trade Practices Act, adding legal exposure on top of operational costs.

For small businesses, these expenses happen all at once and often exceed annual profits. Business email compromise attacks specifically target payroll data or vendor invoices by spoofing executives or altering payment instructions-the financial loss is immediate and irreversible.

Why cyber liability coverage matters now

The costs of a breach extend far beyond what most owners anticipate. You face not only the direct expenses of incident response but also the indirect costs of lost revenue while systems are down, potential fines for regulatory non-compliance, and damage to customer trust. Cyber liability insurance covers first-party costs (incident response, forensics, data restoration, business interruption, extortion, notification, and credit monitoring) and third-party liability (privacy liability, network security liability, and media liability). Without this protection, a single incident can deplete your cash reserves and threaten your ability to continue operations. The right coverage, combined with solid security practices, is what separates businesses that recover quickly from those that don’t.

What Cyber Liability Coverage Actually Pays For

Cyber liability insurance splits into two distinct protection layers that work together to cover the financial chaos that follows a breach. First-party coverage handles your direct costs-the expenses you incur to contain and recover from an incident. Second-party coverage protects you against claims from customers, clients, or business partners whose data or operations were harmed by your breach. Understanding what each layer covers prevents the dangerous assumption that a single policy component will cover all your exposure. The average small business cyber insurance cost runs around $129 per month, but this varies significantly based on your data sensitivity, industry, and the security controls you have in place.

Breach response and notification demand immediate cash

When a breach occurs in Connecticut, you face statutory obligations that trigger immediate expenses. Connecticut law requires notification within 60 days of discovery, and if you compromised Social Security numbers or Tax Identification Numbers, you must provide 24 months of credit monitoring services at your expense. The Connecticut Office of the Attorney General must receive notification no later than when residents are notified, and failure to comply violates the Connecticut Unfair Trade Practices Act, exposing you to additional fines. First-party cyber coverage pays for forensic investigators to determine what data was stolen, incident response consultants to contain the breach, legal counsel to navigate notification requirements, the cost of credit monitoring services themselves, and public relations support to manage customer communication. For a small business, these costs easily reach $50,000 to $100,000 before considering any lost revenue. Your cyber policy should clearly specify coverage limits for notification and credit monitoring expenses-many policies cap this at $25,000 to $100,000 depending on your policy tier. Verify that your deductible (typically $1,000 to $2,500) aligns with your cash reserves, because you pay this amount out of pocket before insurance coverage begins.

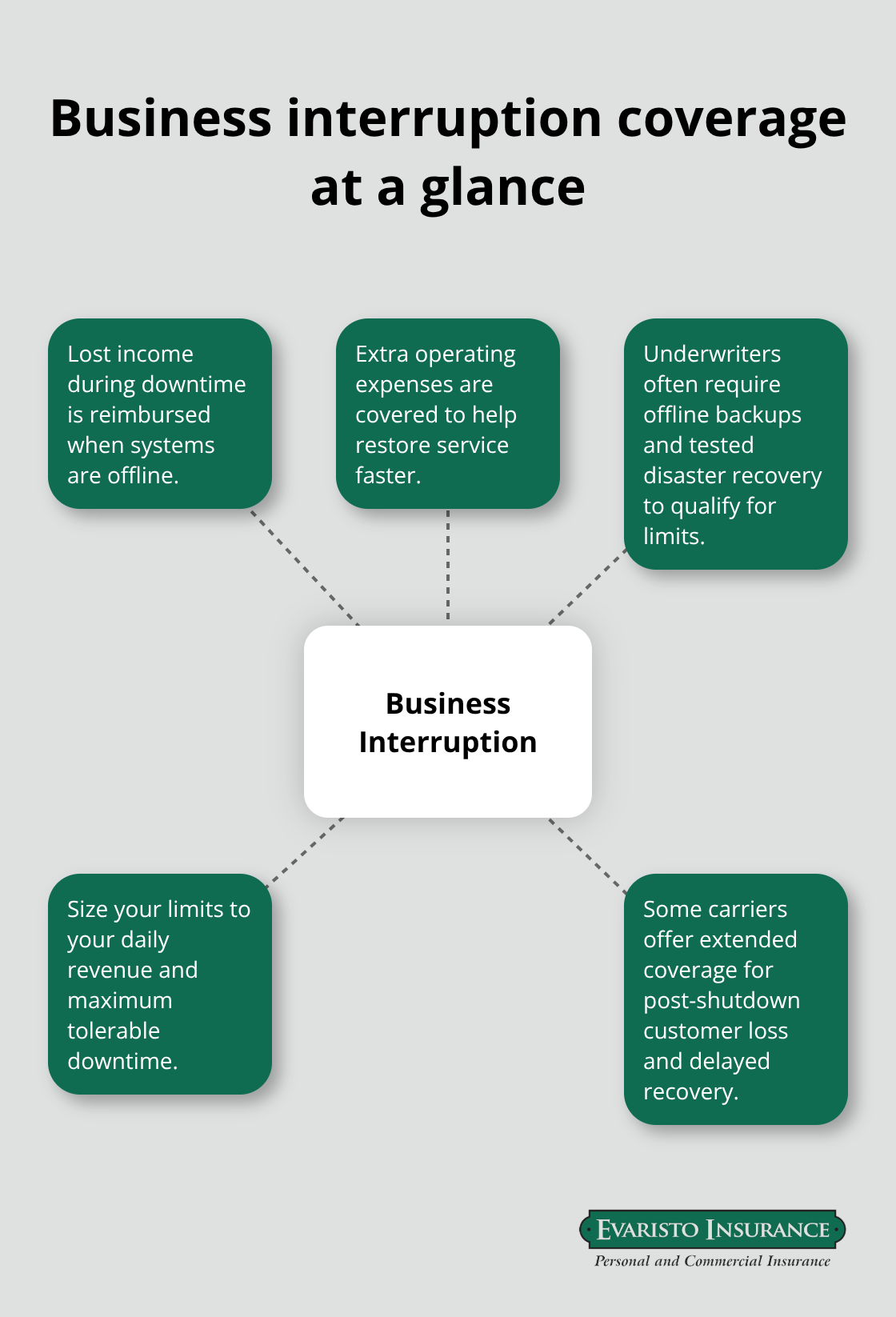

Business interruption coverage protects revenue during downtime

Ransomware and data breaches force operational shutdowns that can last days or weeks. If your point-of-sale system, scheduling software, or customer database goes offline, you cannot serve customers or generate revenue. Business interruption coverage reimburses lost income during the period your systems remain down and pays for extra operating expenses you incur to restore service faster.

For a Connecticut small business generating $10,000 in daily revenue, even a three-day shutdown costs $30,000 in lost income before adding emergency restoration costs. Many underwriters require that you maintain offline backups and test disaster recovery procedures quarterly to qualify for business interruption limits. Policy limits typically range from $25,000 to $250,000 in business interruption coverage, though this should match your actual daily revenue loss. Calculate your maximum tolerable downtime in days, multiply by your average daily revenue, and try to ensure your cyber policy limit covers that amount. Some carriers offer extended business interruption coverage that extends protection beyond the direct shutdown period to account for customer loss and delayed recovery of normal operations.

Legal defense and regulatory costs escalate quickly

If a breach exposes customer data, those customers can sue you for negligence, privacy violations, or breach of contract. Connecticut law does not provide blanket immunity for data handlers, meaning you face direct liability for damages. Third-party cyber liability coverage pays legal defense costs, settlements, and judgments when customers or partners sue over a breach. Regulatory defense coverage covers attorney fees to respond to inquiries from the Connecticut Attorney General’s office or other state regulators investigating your breach response procedures. For tech service providers or businesses handling sensitive client data, these regulatory investigations often cost $15,000 to $50,000 in legal fees alone. Network security liability coverage protects you if your systems accidentally harm a customer’s or vendor’s systems-for example, if a malware infection you failed to detect spreads to a client’s network. Media liability coverage applies if your website or social media become compromised and attackers use them to distribute malware or fraudulent content. Policy limits for third-party liability typically start at $250,000 and extend to $1,000,000 or higher depending on your data volume and client contracts. Review any client contracts or vendor agreements that specify minimum cyber liability limits-many require you to carry $500,000 to $1,000,000 in coverage before they will do business with you.

Comparing carriers reveals significant coverage gaps

Cyber liability forms and coverage terms vary significantly across insurers, and what one carrier includes as standard coverage, another may exclude or charge extra for. Some carriers bundle cyber liability with professional liability or errors and omissions coverage, while others sell it as a standalone product. The policy language matters tremendously-definitions of “data breach,” “network security failure,” and “business interruption” differ between carriers and can affect whether your specific incident qualifies for payment. Deductible structures also vary; some carriers offer separate deductibles for first-party and third-party claims, while others apply a single deductible across all coverage types. Premium costs depend not only on your policy limits and deductible but also on your industry risk profile, the amount of sensitive data you handle, your claims history, and the security controls you have implemented. An independent insurance agent who represents multiple carriers can compare policy forms side by side and identify which coverage aligns with your actual operational risks. This comparison process takes time but prevents the costly mistake of purchasing a policy that looks comprehensive until you file a claim and discover critical gaps.

The specific coverage you need depends on your business model, the data you collect, and the clients or vendors you serve. Your next step involves assessing which of these protection layers matter most to your operations and determining the policy limits that match your financial exposure.

Building Security Controls That Actually Work

Cyber liability insurance covers the financial wreckage after an attack, but the most effective way to protect your Connecticut business is preventing breaches before they happen. Insurance cannot restore your reputation or eliminate the operational chaos of a shutdown, which is why strong security controls matter more than the policy limits you carry. The Connecticut businesses that survive cyber incidents are the ones that combine practical, layered defenses with proper coverage.

Multi-Factor Authentication Stops Account Compromise

Start with multi-factor authentication across all systems that handle sensitive data or connect to your network. MFA blocks 99.9% of account compromise attacks according to Microsoft security research, yet most small businesses still rely on passwords alone. If you use Microsoft 365, Google Workspace, or any cloud-based accounting software, enable MFA immediately for every user account. This means requiring a second form of verification-a phone code, hardware key, or authentication app-whenever someone logs in. The setup takes 30 minutes per employee and costs nothing, but it prevents attackers from accessing your systems even when they steal a password through phishing. Test this with your IT provider or cloud application support; most platforms now offer streamlined MFA rollout tools that reduce implementation friction.

Employee Training Reduces Breach Risk More Than Technology Alone

Employee training is where most Connecticut small businesses fail. You can deploy firewalls and backup systems, but a single employee clicking a malicious link or calling a scammer with wire transfer authority can undo all that investment. Ongoing security training reduces breach risk far more effectively than technology alone because attackers continually adapt their tactics. Conduct training at least quarterly and tailor it to your specific industry and operations-generic phishing simulations are less effective than training that mimics actual threats your business faces. For example, healthcare practices should emphasize social engineering around patient data requests, while manufacturers should focus on supply chain and vendor impersonation. Measure training effectiveness by tracking how many employees report suspicious emails to your IT team or security contact; this metric reveals whether staff actually internalized the training.

Offline Backups Protect Against Ransomware Recovery Failures

Maintain offline backups of critical data and test your ability to restore from those backups at least twice per year. Ransomware attackers specifically target cloud backups and networked storage because they want to eliminate your recovery options. Offline backups stored separately from your network-whether on an external drive kept in a safe location or through a dedicated backup appliance-are your insurance against losing data permanently. Test restoration by actually recovering a sample of files to confirm the backup process works when you need it. Many businesses discover their backups are corrupted or incomplete only when they try to recover after an attack.

Partner With Local IT Expertise to Close Coverage Gaps

Work with a local Connecticut IT provider who understands these requirements and can implement controls that fit your budget and operations. Insurance agents cannot install MFA or conduct training, but we can help you understand which coverage gaps remain after you implement these controls and ensure your cyber policy aligns with the protections you have built.

Final Thoughts

Cyber threats targeting small business cyber CT operations will only accelerate as attackers refine their tactics and expand their toolkits. The criminals targeting your business today are more sophisticated than they were last year, and they will be more dangerous next year. Waiting for a breach to happen and then scrambling to respond costs far more than preventing one in the first place.

The businesses that survive cyber incidents are the ones that refuse to choose between security and coverage. Strong security controls like multi-factor authentication, regular employee training, and offline backups form your first line of defense and directly reduce your breach risk. But even the best security practices cannot eliminate all risk, which is why cyber liability insurance exists-when an attack happens despite your precautions, insurance covers the forensic investigation, customer notification, credit monitoring, business interruption losses, and legal defense costs that would otherwise devastate your cash flow.

We at Evaristo Insurance have helped Connecticut businesses assess their cyber risk and find coverage that actually matches their operations. As a second-generation, family-owned independent agency serving Connecticut since 1989, we compare multiple top carriers to deliver tailored protection and competitive pricing. Contact us today to discuss your cyber liability exposure and build a protection plan that fits your budget and risk tolerance.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.