Connecticut Commercial Cyber Liability: Defending Your Business From Digital Threats

Connecticut businesses are losing millions to cyber attacks every year, and the threat is accelerating. Ransomware, data breaches, and extortion demands are no longer rare events-they’re becoming routine for companies across the state.

At Evaristo Insurance, we’ve seen firsthand how commercial cyber liability in CT protects businesses when digital threats strike. This guide walks you through the real risks your company faces and how the right coverage makes the difference.

The Cyber Threat Reality in Connecticut

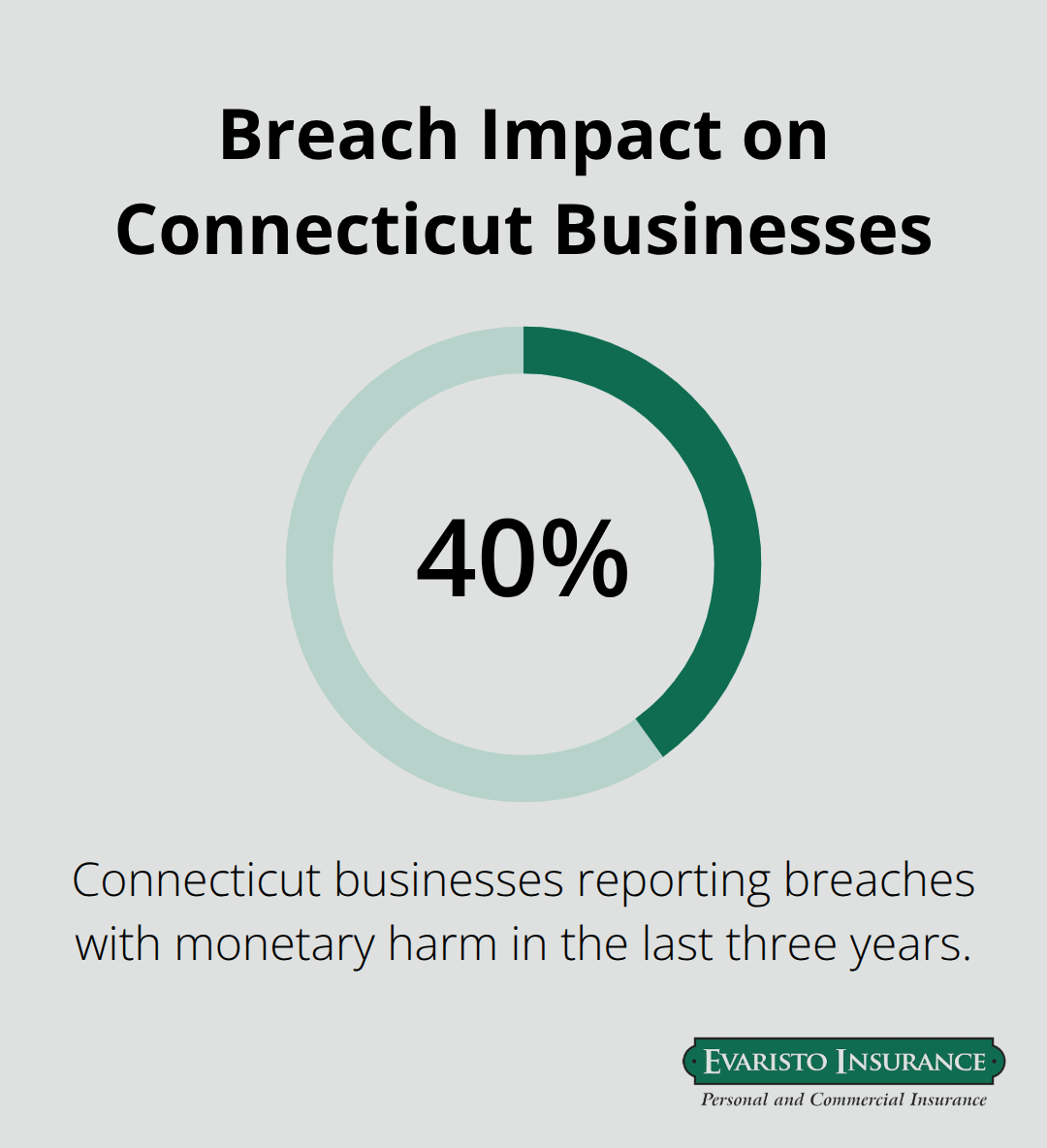

Connecticut municipalities and businesses face active cyber attacks. In January 2026, New Britain fell victim to ransomware that forced the city into extended recovery operations with outside cybersecurity experts and state partners. Just one month later, Meriden experienced a cyber disruption that temporarily moved emergency dispatch to the Connecticut Police Academy and forced staff to rely on handwritten records. These incidents signal what’s happening across the state. The Connecticut Intelligence Center warns that ransomware attackers encrypt data and demand substantial sums to regain access, with average ransom demands reaching about $1.1 million. When attackers layer data extortion on top of ransom demands-threatening to sell stolen information on the dark web-the pressure intensifies dramatically. A Connecticut news outlet reported that approximately 40 percent of Connecticut businesses experienced a breach with monetary harm in the last three years, including data encryption for ransom and intercepted wire transfers. This isn’t theoretical risk; it’s happening to your neighbors right now.

Why Small and Medium Businesses Are Prime Targets

Attackers increasingly target smaller Connecticut businesses as remote work proliferates, viewing them as easier entry points than larger corporations with dedicated security teams. These attackers use artificial intelligence to craft highly targeted phishing and social-engineering messages that bypass basic employee awareness. The Ponemon Institute reports the average cost of a data breach in the United States reaches $8.64 million, yet many small business owners underestimate their exposure because they assume they’re too small to matter. That assumption is dangerously wrong. Connecticut’s aging municipal and health IT environments (often 10 to 15 years old) highlight a broader vulnerability across the state’s business landscape. Recovery costs extend far beyond ransom payments to include forensics, system hardening, business-continuity investments, and the operational disruption that cripples cash flow. West Haven’s 2024 incident demonstrated the value of backups, enabling faster recovery, yet many Connecticut businesses still lack tested backup and restore procedures.

Connecticut’s Data Privacy Laws Create New Obligations

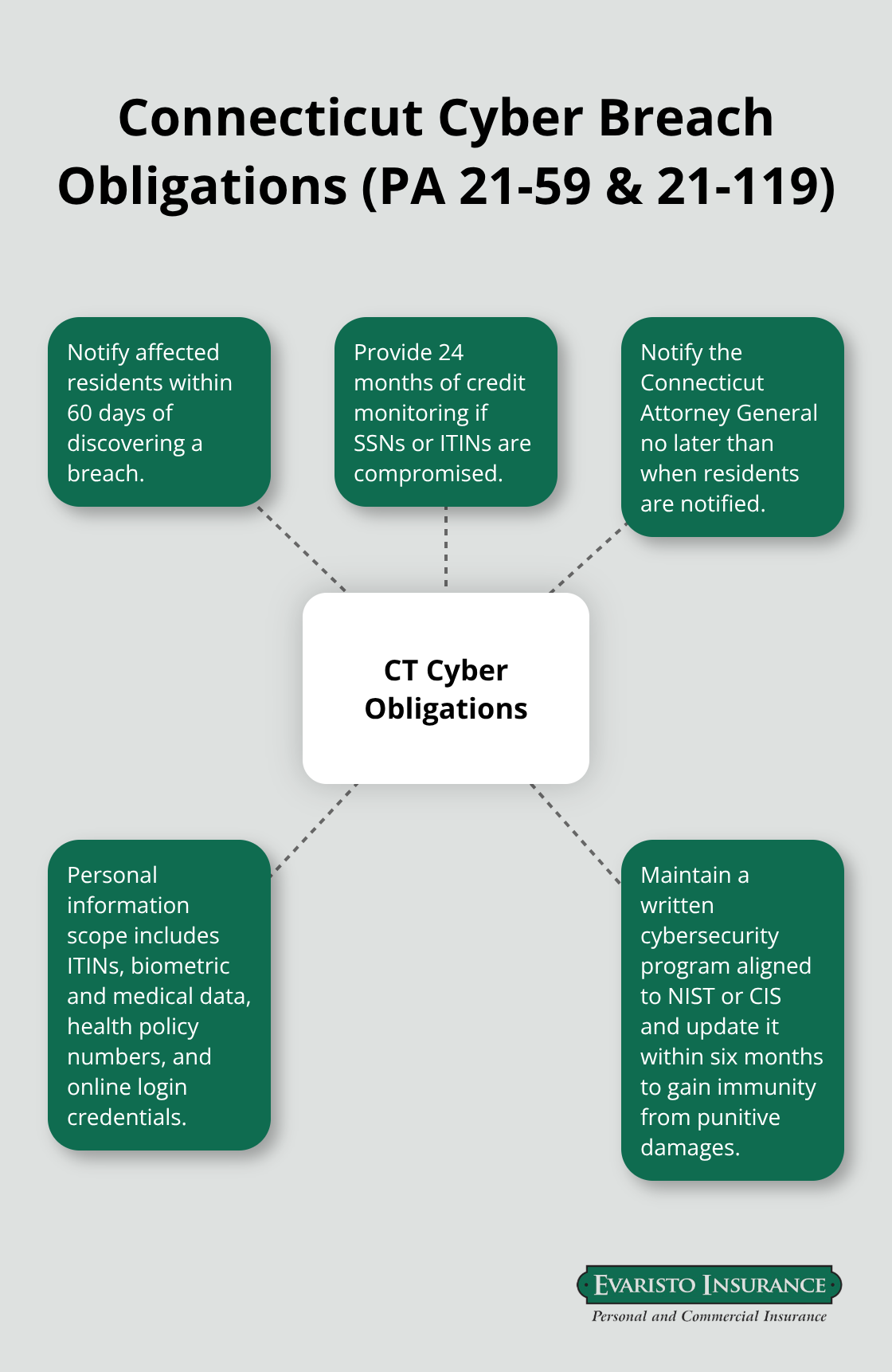

Public Act 21-59 expanded what counts as personal information to include ITINs, government IDs, biometric data, medical information, health policy numbers, and online login credentials. More importantly, it shortened breach notification deadlines from 90 days to just 60 days after discovery. If your breach compromises Social Security numbers or Taxpayer Identification Numbers, you must offer 24 months of credit monitoring to affected residents. Notice to the Connecticut Attorney General must occur no later than when residents are notified, and failure to comply violates the Connecticut Unfair Trade Practices Act.

Public Act 21-119 incentivizes cybersecurity by granting immunity from punitive damages if your business maintains an approved written cybersecurity program aligned with recognized standards (such as the NIST Cybersecurity Framework or CIS Controls)-but you must update that program within six months of any framework revision. These laws shift the financial and legal burden onto business owners who fail to prepare. The Connecticut Attorney General provides an online breach notification form as the preferred submission method, and you’ll receive a confirmation email with a case number starting with PR and seven digits, creating an official record of your response.

Understanding these threats and obligations sets the stage for what your business actually needs to protect itself. The right cyber liability insurance covers the costs that Connecticut law and real-world incidents impose on unprepared companies.

What Cyber Liability Insurance Actually Covers

Cyber liability insurance absorbs the financial devastation that follows a breach or ransomware attack. Unlike general business insurance, which explicitly excludes digital threats, cyber policies address the specific costs Connecticut businesses face when attackers strike. The global average cost of a data breach continues to rise, yet most Connecticut small businesses pay between $1,000 and $7,500 annually for $1 million in cyber coverage. That gap between potential loss and premium cost makes cyber insurance one of the most underutilized risk management tools available.

First-Party Coverage Reimburses Your Direct Costs

First-party coverage reimburses your direct expenses when an attack occurs. Forensic investigations determine how attackers entered your systems and what data they accessed. Ransom negotiation services help you navigate extortion demands, though paying ransom itself carries legal and ethical complications. Breach notification expenses-mandated by Connecticut’s 60-day requirement-cover the cost of contacting affected residents. Credit monitoring for affected individuals becomes necessary if Social Security numbers or ITINs were compromised. Public relations and crisis management protect your reputation after news of the breach spreads. System restoration and hardening prevent future attacks and restore normal operations. When New Britain and Meriden faced disruptions in 2026, these costs mounted quickly as cities hired outside cybersecurity experts and coordinated recovery with state partners.

Third-Party Liability Protects You Against Customer Claims

Third-party liability coverage protects you when customers, partners, or vendors sue after your breach exposes their data or interrupts their operations. Connecticut’s expanded personal information definition under Public Act 21-59 means more of your stored data triggers notification obligations and potential claims. A single breach affecting hundreds of customers can generate multiple lawsuits, and your policy covers legal defense costs and settlements. This coverage proves essential when your incident harms others’ businesses or finances.

Business Interruption and Extortion Coverage Fill Critical Gaps

Business interruption coverage compensates for lost revenue and covers fixed expenses when a ransomware attack shuts down your operations. This protection proves essential when attackers encrypt critical systems and force you offline for days or weeks. Many policies also include extortion liability coverage specifically for ransom demands and data extortion threats (where attackers threaten to sell stolen information on the dark web). Together, these coverages address the operational and financial pressure that attacks create.

Know What Your Policy Excludes

Cyber policies typically exclude future profit losses, costs to upgrade security infrastructure beyond incident response, or compensation for stolen intellectual property value. Understanding these gaps helps you plan additional safeguards or accept the residual risk. Before purchasing coverage, assess what data your business holds, how many customers could be affected by a breach, and whether contracts or laws require minimum coverage amounts. An experienced broker familiar with Connecticut’s regulatory landscape ensures your policy limits match your actual exposure and covers the specific scenarios most likely to disrupt your operations. With coverage in place, your next priority shifts to strengthening the defenses that prevent attacks from succeeding in the first place.

Building Defenses That Actually Stop Attacks

Insurance covers the aftermath, but preventing attacks from succeeding in the first place saves your business from disruption, reputation damage, and the operational chaos that follows breach discovery. Connecticut businesses that face ransomware and data theft attacks often share a common weakness: they lack the layered defenses that make attackers move to easier targets.

Deploy Multi-Factor Authentication Across Critical Systems

Multi-factor authentication stops attackers cold even when they obtain employee passwords through phishing or credential theft. The Cybersecurity and Infrastructure Security Agency recommends MFA across all systems that access sensitive data or critical operations, and Connecticut insurers increasingly require it as a baseline control to maintain cyber liability coverage. Start with email and financial systems where attackers cause the most damage, then expand to remote access tools, administrative accounts, and any system handling customer data. This takes days to implement, not months.

Segment Your Network to Limit Attack Spread

Network segmentation isolates critical systems from less important ones so a ransomware infection on an employee’s workstation doesn’t immediately encrypt your entire operation. West Haven’s faster recovery after its 2024 incident benefited from backups, yet the city could have prevented weeks of disruption entirely through proper segmentation and tested restoration procedures. Test your backups monthly by actually restoring data to a separate environment and verifying it works. Many Connecticut businesses discover their backups are corrupted only after an attack forces them to try recovery, leaving them with no alternative but to pay ransom or accept permanent data loss.

Train Employees to Recognize and Resist Phishing

Attackers use artificial intelligence to craft messages that look legitimate even to cautious employees because phishing and password security matter more than most business owners realize. Connecticut’s cyber threat landscape shows that approximately 40 percent of businesses experienced breaches with monetary harm in recent years, yet many attacks start with a single employee clicking a malicious link or opening an infected attachment. Connecticut insurers expect quarterly phishing simulations where employees receive fake phishing emails to test their awareness, with immediate feedback and retraining for those who fail. Conduct these simulations yourself using free tools from CISA or hire a managed security provider to run them monthly. Require strong passwords (minimum 12 characters with mixed case, numbers, and symbols) and enforce password changes only when accounts show signs of compromise rather than on arbitrary 90-day schedules, which research shows encourages weaker passwords.

Designate an Incident Response Coordinator

Assign a trained incident response coordinator within your organization who understands your systems, knows how to preserve evidence, and can coordinate with law enforcement and your cyber insurance carrier if an attack occurs. When New Britain and Meriden faced disruptions in 2026, cities with designated response coordinators recovered faster and made better decisions about involving outside experts. Document your security measures and keep that documentation current so you qualify for immunity from punitive damages under Connecticut Public Act 21-119, which requires maintaining an approved cybersecurity program aligned with frameworks like NIST or CIS Controls and updating it within six months of any framework revision.

Final Thoughts

Connecticut businesses operate in an environment where cyber attacks are no longer hypothetical risks but active threats that disrupt operations, drain finances, and damage reputations. The incidents in New Britain and Meriden in early 2026 demonstrate that ransomware, data breaches, and extortion demands affect organizations across the state regardless of size. With approximately 40 percent of Connecticut businesses experiencing breaches with monetary harm in recent years and average breach costs reaching $8.64 million nationally, the financial exposure is real and substantial.

Your defense strategy requires two parallel tracks: implement technical and operational controls that make your business a harder target than competitors, and transfer the financial risk through commercial cyber liability CT coverage that absorbs the costs your defenses cannot prevent. Multi-factor authentication, network segmentation, tested backups, and employee training create friction that pushes attackers toward easier prey, while Connecticut’s data privacy laws impose strict notification deadlines and credit monitoring obligations that cyber insurance covers. Third-party liability protection shields you against customer lawsuits following a breach and aligns with Connecticut’s cybersecurity framework, which emphasizes preparation, response, and recovery.

We at Evaristo Insurance understand Connecticut’s specific cyber risks and regulatory landscape. Contact us today to assess your cyber risk and secure coverage that protects your business from digital threats.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.