Commercial Property Insurance in CT: Protecting Your Biz Assets in Connecticut

Your business assets in Connecticut face real risks every day. From fires and theft to severe weather, one incident can devastate your operations without proper protection.

Commercial property CT insurance isn’t optional-it’s a business necessity. We at Evaristo Insurance help Connecticut business owners understand what coverage they actually need and where dangerous gaps often hide.

Why Connecticut Businesses Need Commercial Property Coverage

Connecticut businesses lose millions annually to property damage, and the state’s coastal and inland weather patterns create specific vulnerabilities. Nor’easters bring wind-driven flooding to shoreline towns like Westport and Mystic, while inland areas face frozen pipe damage and snowmelt-related water destruction. These aren’t rare events-they’re predictable risks that hit Connecticut companies regularly.

Most landlords and lenders require proof of commercial property coverage before they fund or lease space, making it a practical requirement even where state law doesn’t mandate it. Your lease agreement almost certainly requires general liability; a Business Owner’s Policy bundles both protections and simplifies management. Industry type significantly affects your premium. Retail operations typically pay lower rates, while manufacturers face higher costs due to heavy machinery and specialized processes, and medical practices incur elevated premiums for high-value equipment and sensitive data servers.

How Connecticut’s Weather Creates Specific Claim Patterns

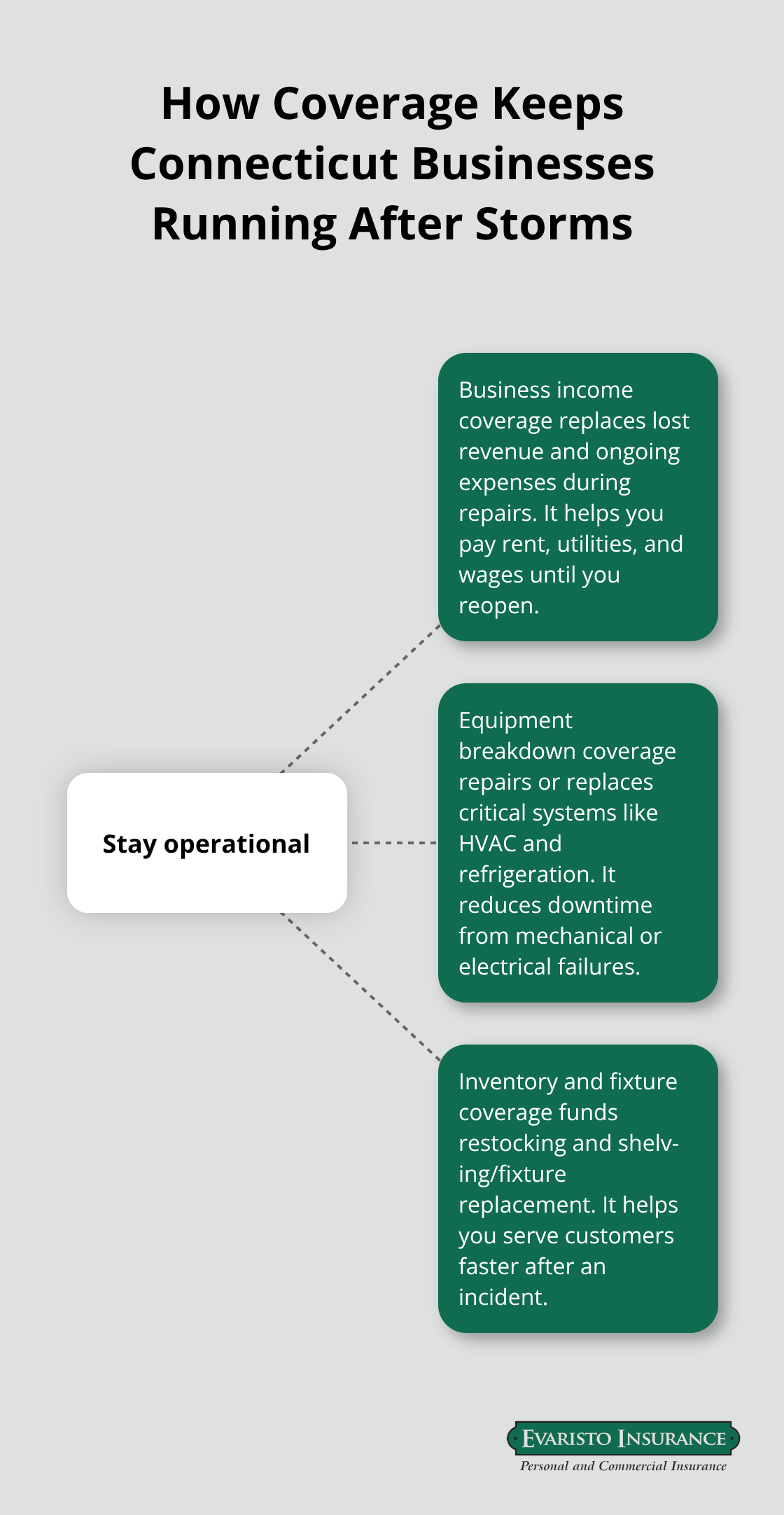

Frozen pipes, storm surge, and wind damage dominate Connecticut claim patterns. A Nor’easter forces you to close for repairs, and you lose revenue while still paying rent, utilities, and employee wages. Business income coverage-included in many comprehensive policies-replaces that lost income and covers operating expenses during the shutdown. Equipment breakdown coverage protects critical systems like HVAC or refrigeration that keep operations running. Inventory and fixture coverage allows you to replace damaged goods and shelving so you serve customers faster after an incident.

Coverage Solutions for Connecticut’s Unique Risks

Inland marine insurance complements standard property policies for contractors and mobile service providers with tools or equipment in transit. Connecticut has strengthened flood disclosure requirements through recent legislative changes, and coastal and flood-prone properties increasingly need separate flood coverage through the National Flood Insurance Program or private carriers. This decision shouldn’t wait-coastal properties face mounting pressure to secure flood protection before underwriting becomes more restrictive.

What Commercial Property Insurance Actually Covers

Building Coverage Protects Your Physical Structure

Building coverage protects the physical structure you own or lease, including walls, roof, HVAC systems, and permanent fixtures like flooring and built-in shelving. A Nor’easter tears off your roof or fire damages your walls-building coverage pays for repairs or rebuilding. Replacement cost coverage matters more than actual cash value. The insurer pays what it costs to rebuild today, not what the building was worth when you bought it five years ago. Connecticut contractors and manufacturers should verify building valuations annually because equipment upgrades and facility improvements increase replacement costs significantly.

Business Personal Property Covers Your Assets Inside

Business personal property coverage protects movable assets inside your building: inventory, equipment, furniture, tools, and electronics. A retail store’s clothing and display cases, a medical office’s diagnostic equipment, a manufacturing operation’s machinery-all qualify for this protection. Your policy should reflect current inventory and equipment values, not last year’s numbers. Underinsurance happens when business owners fail to update valuations after purchasing new equipment or expanding inventory. You’ll face reduced payouts if a loss occurs, making an annual inventory review essential.

Loss of Income and Equipment Breakdown Coverage

Loss of income coverage-also called business interruption insurance-replaces revenue and operating expenses when a covered incident forces you to close temporarily. Connecticut’s freeze-thaw cycles cause significant pipe damage claims that trigger temporary closures. A restaurant shut for three weeks of pipe repairs loses revenue, rent, utilities, and employee wages during that period; loss of income coverage replaces all of it. Equipment breakdown coverage repairs or replaces critical systems like refrigeration or HVAC units, minimizing downtime and keeping operations moving forward.

Additional Protections That Complement Property Coverage

General liability protection-often bundled in a Business Owner’s Policy-covers bodily injury and property damage claims from third parties, complementing your property coverage. Inland marine insurance extends protection beyond your building for tools and equipment in transit or at job sites, essential for Connecticut contractors moving between locations. Flood coverage requires separate purchase through the National Flood Insurance Program or private carriers; standard policies explicitly exclude flood damage. Connecticut’s recent legislative changes, including expanded flood disclosure requirements effective 2026, reflect the state’s commitment to flood risk transparency. Coastal and flood-prone Connecticut properties should secure flood coverage now rather than waiting for underwriting restrictions to tighten further.

Understanding what your policy covers is only half the battle. Many Connecticut business owners discover gaps in their protection only after a loss occurs-and by then, it’s too late to add the coverage they needed.

Where Your Coverage Actually Falls Short

Outdated Valuations Leave You Dramatically Underinsured

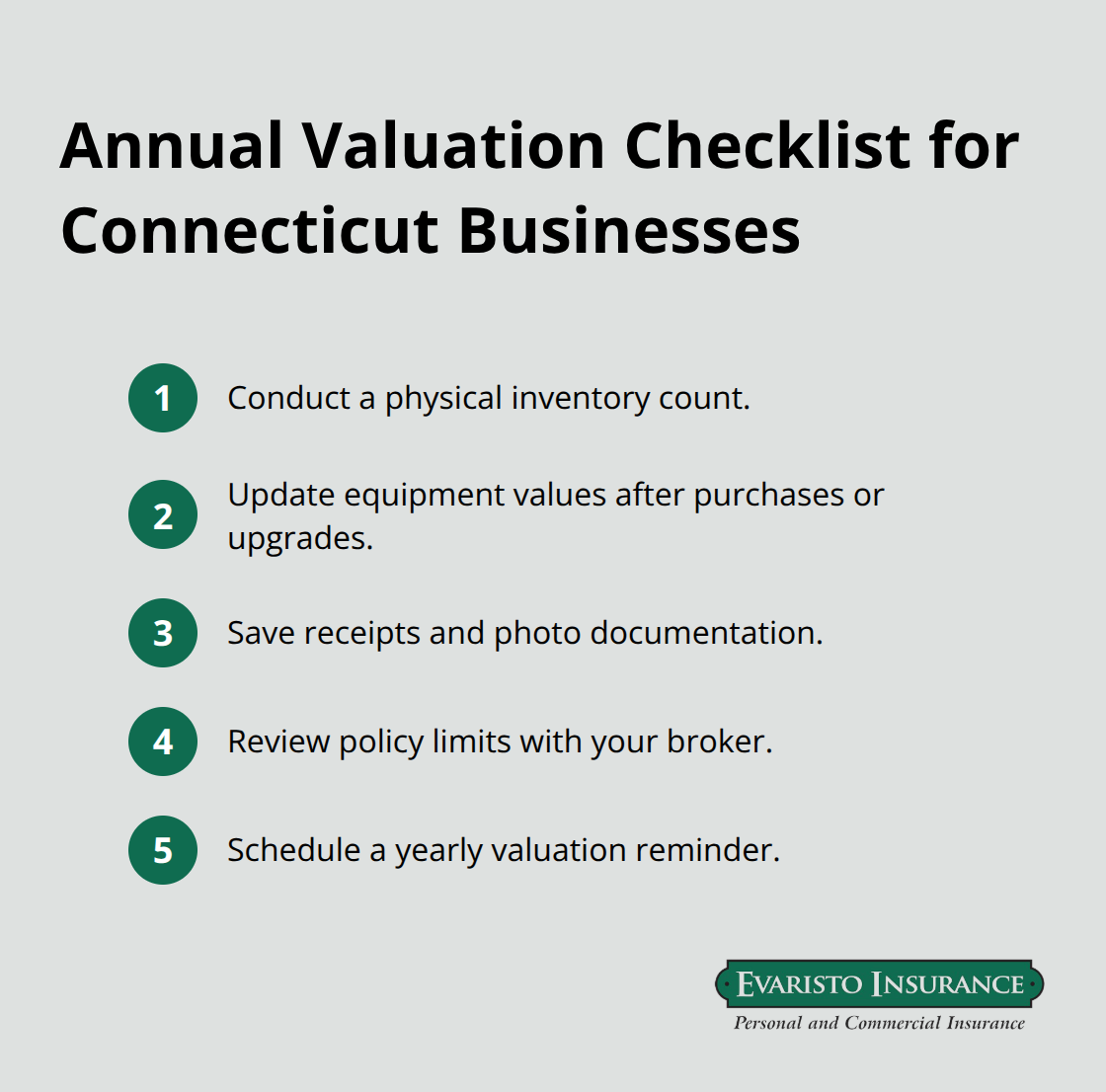

Most Connecticut business owners face a critical gap: policies that reflect inventory and equipment values from two or three years ago. You upgraded machinery, added stock, or expanded your facility, but your policy stayed frozen in time. When fire damages your warehouse, the insurer pays based on those outdated numbers, leaving you thousands short of actual replacement costs.

A manufacturer who installed new CNC equipment worth $75,000 last year but never updated their policy faces a significant shortfall if that equipment burns. The building damage gets covered, but the equipment loss falls short because your policy limits don’t match current asset values. Conduct a physical inventory count and equipment valuation annually, especially after capital investments or facility expansions. Document everything with photos and purchase receipts so your claim adjuster can verify current values quickly and process your claim faster.

Missing Specialty Coverage for Equipment Breakdown

Standard commercial property policies exclude equipment breakdown entirely, yet Connecticut’s freeze-thaw cycles create pipe bursting claims regularly. A restaurant’s frozen pipes force a three-week closure; the building damage gets covered, but without equipment breakdown coverage, that $40,000 walk-in refrigerator replacement comes from your pocket.

Equipment breakdown coverage specifically protects HVAC systems, refrigeration units, and electrical equipment from mechanical failure-protection that standard property policies exclude. Your policy should list these systems explicitly and cover repair or replacement costs. Many Connecticut business owners assume mechanical failures fall under standard coverage until they file a claim and face denial.

Flood and Water Damage Exclusions Create Coastal and Inland Risks

Standard commercial property policies exclude flood damage entirely, yet Connecticut’s weather patterns create two distinct water damage threats. Coastal properties face wind-driven flooding that standard policies won’t cover, and inland areas experience snowmelt water intrusion that many owners assume is covered until they file a claim.

Flood coverage requires a separate policy through the National Flood Insurance Program or private carriers and cannot be added to your standard policy. Connecticut’s 2026 flood disclosure requirements signal that underwriting will tighten further, making now the time to secure flood protection before carriers restrict coastal and flood-zone availability. Coastal and flood-prone Connecticut properties should act immediately rather than waiting for underwriting restrictions to tighten further.

How to Identify Your Specific Gaps

A local insurance agency who understands Connecticut’s specific weather patterns can identify exactly which gaps exist in your current protection. Review your current policy against your actual assets, location risks, and operational needs. Ask your broker whether your policy covers equipment breakdown, whether flood coverage applies to your property, and whether your valuations reflect current asset values.

Final Thoughts

Commercial property CT insurance protects far more than your building-it safeguards your ability to operate, recover, and grow after a loss. The gaps we’ve covered throughout this guide represent real financial exposure that Connecticut business owners face every day. Outdated valuations, missing equipment breakdown coverage, and overlooked flood exclusions aren’t theoretical problems; they’re the exact reasons claims get denied or paid at reduced amounts when you need the money most.

Your specific risks depend on your location, industry, and assets. A coastal retail operation faces different threats than an inland manufacturing facility, and a medical practice with expensive diagnostic equipment needs different protection than a consulting firm. One-size-fits-all policies leave dangerous gaps that only become obvious after damage occurs.

Contact Evaristo Insurance to discuss your specific situation, location risks, and asset values. We’ll identify what’s working, what’s missing, and how to strengthen your protection before the next Nor’easter, equipment failure, or unexpected loss forces you to find out the hard way.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.