Ellington Landscaper Insurance: Local Solutions for Your Crew

Running a landscaping crew in Ellington means managing equipment, protecting your team, and handling liability risks that most business owners never face. Weather delays, vehicle accidents, and on-site injuries can shut down operations and drain your finances fast.

At Evaristo Insurance, we work with Ellington landscapers every day to build coverage that actually matches how your business operates. The right insurance protects both your crew and your bottom line.

The Three Coverages Your Ellington Crew Cannot Skip

General Liability: Your First Line of Defense

General liability insurance is non-negotiable for landscapers in Ellington. Connecticut law requires you to carry at least $1 million per occurrence and $2 million aggregate-this is the floor, not a recommendation. When a client trips on uneven ground your crew created or your team damages a deck during a job, general liability covers their medical bills and legal fees. The average cost runs between $1,100 and $2,300 annually, a small price against a lawsuit that could cost $50,000 or more. Many Ellington landscapers underestimate this risk because nothing has happened yet. That changes the moment a client gets hurt on your watch.

Workers’ Compensation: A Legal Requirement That Protects Everyone

Workers’ compensation is mandatory in Connecticut if you have employees-no exceptions. The Bureau of Labor Statistics reports that landscaping has one of the highest rates of nonfatal occupational injuries and illnesses in any industry, which means your crew faces real danger daily. Connecticut requires this coverage to pay medical costs and lost wages when someone gets injured, and it protects you from employee lawsuits. Typical annual costs range from $400 to $3,000 depending on payroll and headcount.

Many Ellington landscapers misclassify workers as 1099 contractors to avoid this expense, but Connecticut law sees through that if you control their schedule and tools-they may still qualify for benefits, leaving you exposed. This misclassification creates serious liability that no other policy covers.

Equipment and Tools: Protecting Your Most Valuable Assets

Equipment and tools protection matters just as much because your trailer full of mowers, trimmers, and leaf blowers represents tens of thousands of dollars. Inland Marine insurance covers equipment in transit between job sites or at temporary locations, protecting against theft, vandalism, and accidents. Commercial Property insurance safeguards tools stored at your base and covers income loss during downtime from fire or theft. These coverages cost far less than replacing a stolen trailer or losing a week of work because your equipment got damaged.

With these three foundational coverages in place, you’ve addressed the biggest financial threats to your operation. However, the risks don’t stop there-your vehicles and the accidents that happen on the road create their own set of exposures that demand specific attention.

Common Risks Landscapers Face and How Insurance Helps

Weather Stops Work, But Your Bills Keep Coming

Rain in spring costs Ellington landscapers income they cannot recover, and without coverage for business interruption, that lost revenue hits your account directly. Commercial Property insurance with business interruption protection covers lost income when weather or other covered events force you to shut down, giving your operation a financial cushion during seasonal slowdowns. April showers and winter conditions arrive predictably each year, yet many landscapers treat income loss as something they simply absorb rather than protect against.

Vehicle Accidents Create Exposure General Liability Won’t Cover

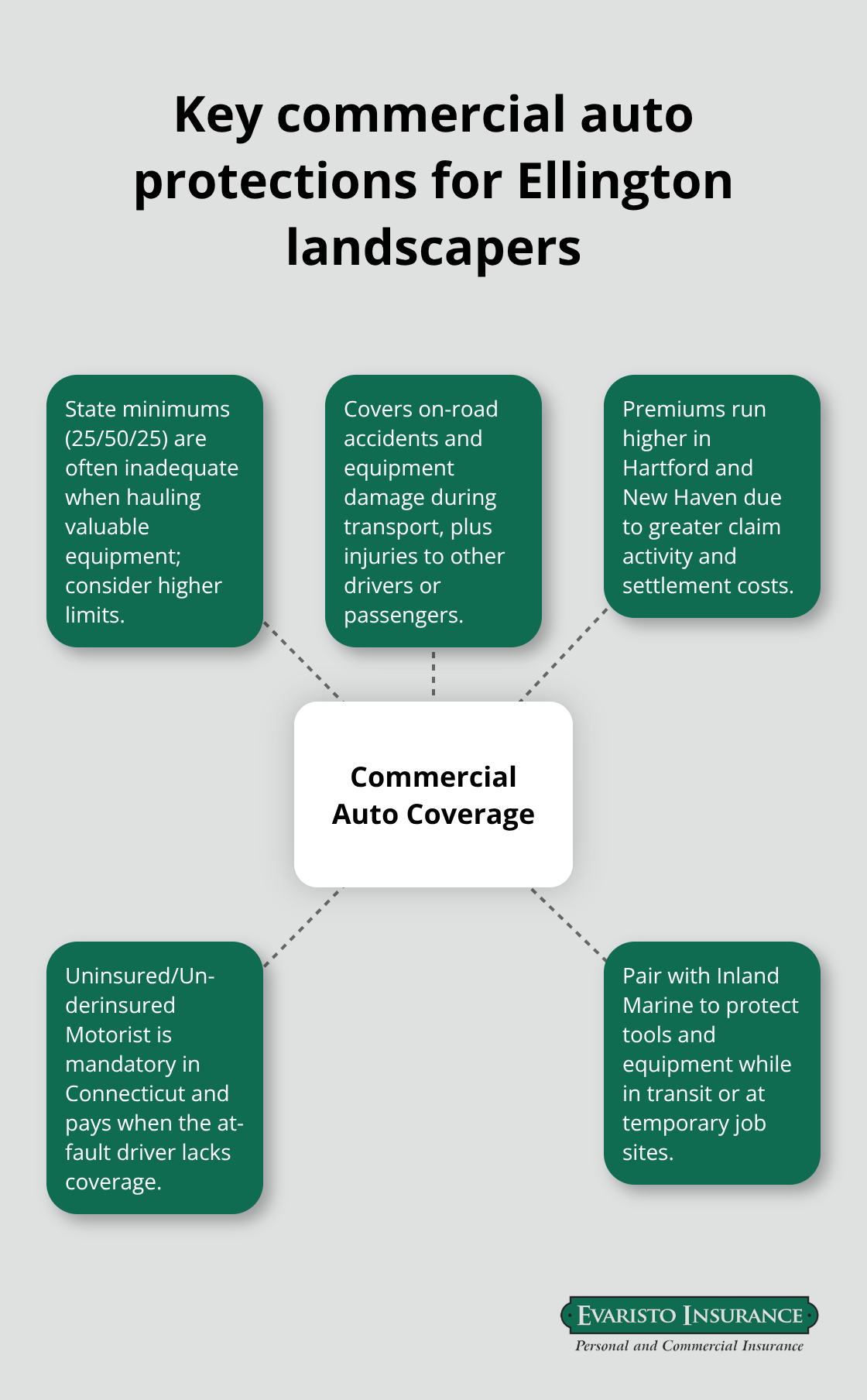

Your vehicles create exposure that general liability won’t touch. Connecticut requires minimum liability limits of 25/50/25 for commercial auto, but that’s inadequate when your truck carries $15,000 in equipment and collides with another vehicle on the way to a job site. Commercial auto insurance covers on-road accidents, equipment damage during transport, and injuries to other drivers or passengers, with typical annual costs around $1,810 for Ellington landscapers.

Driving in Hartford or New Haven pushes premiums higher than smaller towns because claim activity and settlement costs run steeper in larger cities. Uninsured and underinsured motorist coverage is mandatory in Connecticut and essential for your crew-if another driver hits you and lacks sufficient coverage, this protection pays your medical bills and vehicle repairs. You should also consider Inland Marine coverage for tools and equipment while they sit in transit or at temporary job sites, protecting against theft and vandalism that happen between locations.

Client Injuries on Job Sites Trigger Your Most Expensive Claims

Client injuries on your job sites create the most expensive liability claims because they involve medical expenses, legal fees, and sometimes permanent disability costs. A homeowner who slips on freshly mulched ground or gets struck by flying debris from a trimmer faces months of medical treatment, and their attorney will pursue your general liability policy aggressively. At $1,100 to $2,300 annually, general liability remains your cheapest protection against claims that routinely exceed $50,000.

Connecticut requires $1 million per occurrence and $2 million aggregate as the legal minimum, but higher limits or Umbrella insurance make sense once primary coverage limits approach exhaustion on large projects. This layered approach costs less than defending a single major lawsuit. The specific risks your crew handles-whether you trim trees near power lines, apply chemicals to client properties, or operate heavy machinery-determine how much protection you actually need beyond the state minimum.

How Evaristo Insurance Matches Coverage to Your Operation

Assessment Shapes Your Coverage Strategy

We at Evaristo Insurance work differently than national carriers because we spend time understanding how your Ellington crew actually operates before recommending coverage. A landscaper who only handles lawn maintenance faces different risks than one who trims trees near power lines or applies chemical treatments, yet most insurance quotes ignore these distinctions. When you contact us, we ask specific questions about your equipment inventory, crew size, service areas, and highest-risk tasks. A crew of four handling basic mowing and mulching needs different protection than a crew of eight operating heavy machinery and working on high-value residential properties. This assessment phase matters because it prevents you from overpaying for coverage you don’t need while identifying gaps that could cost you thousands.

Connecticut Requirements Meet Your Actual Needs

Connecticut law requires minimum general liability of $1 million per occurrence and $2 million aggregate, but the right limits for your operation depend entirely on project scope and client property values. A crew that works exclusively on modest residential properties may operate safely within state minimums, while contractors handling high-value estates or tree work near power lines should carry higher limits or Umbrella coverage. We compare quotes across multiple carriers because coverage costs vary dramatically based on how insurers rate landscaping risk. One carrier might quote $1,500 annually while another charges $2,100 for identical coverage, and we show you those differences so you understand what you’re paying for.

What Your Coverage Actually Costs

Connecticut landscapers typically spend around $4,180 per year combined for general liability, commercial auto, and workers’ compensation, but your actual cost depends on crew size, equipment value, and whether you handle high-risk services like tree trimming or chemical application. Your commercial auto premium shifts higher if you operate in Hartford or New Haven, where claim activity and settlement costs run steeper than in smaller towns. We help you identify which coverages matter most to your operation and where you can adjust limits or deductibles to fit your budget without creating dangerous gaps.

Local Support When You Need It

Our local offices in Ellington and West Hartford mean you work with someone who understands seasonal weather disruptions, Hartford and New Haven traffic patterns that affect your commercial auto premiums, and the specific compliance requirements Connecticut imposes on landscaping businesses. When you need a certificate of insurance issued the same day for a client contract, you contact us instead of waiting for a national carrier’s processing queue. If a crew member gets injured and you need to file a workers’ compensation claim, we handle the coordination with your insurer so you focus on operations instead of paperwork.

Coverage Adjustments as Your Business Grows

When your business grows and you add crew members or equipment, we review your coverage annually to adjust limits and add protection you’ve outgrown, preventing the common mistake of keeping the same policy year after year while your operation expands. This ongoing relationship means your insurance stays aligned with how your Ellington operation actually changes across seasons and as you take on larger or more complex projects.

Final Thoughts

The right Ellington landscaper insurance protects your business and your team from financial devastation when accidents happen. General liability, workers’ compensation, and equipment coverage form the foundation that keeps your operation running when injuries occur, vehicles collide, or tools disappear. Without these protections, a single client injury or vehicle accident can force you to shut down operations and drain savings you’ve built over years of hard work.

We at Evaristo Insurance understand the specific challenges Ellington landscapers face because we work with crews in your area every day. Connecticut’s weather disrupts schedules, Hartford and New Haven traffic increases your commercial auto risk, and seasonal fluctuations make budgeting for insurance premiums difficult. National carriers apply generic landscaping rates without understanding whether your crew handles basic lawn maintenance or high-risk tree trimming near power lines-that difference matters enormously when it comes to your actual costs and coverage gaps.

Contact Evaristo Insurance today for a personalized quote that matches how your operation actually works. We’ll assess your specific risks, explain Connecticut’s legal requirements, and show you coverage options that fit your budget without creating dangerous gaps. Your crew and your business deserve protection built by someone who understands local landscaping challenges, not generic industry assumptions.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!