Ellington CT Homeowners Coverage: Local Policy Options

Homeowners in Ellington face unique insurance challenges that generic policies often miss. Connecticut’s weather patterns, local property values, and state regulations demand coverage tailored to your specific situation.

We at Evaristo Insurance have helped countless Ellington CT homeowners find policies that actually protect what matters most. This guide walks you through your options and shows you how to avoid costly coverage gaps.

What Connecticut Homeowners Actually Need to Know About Coverage

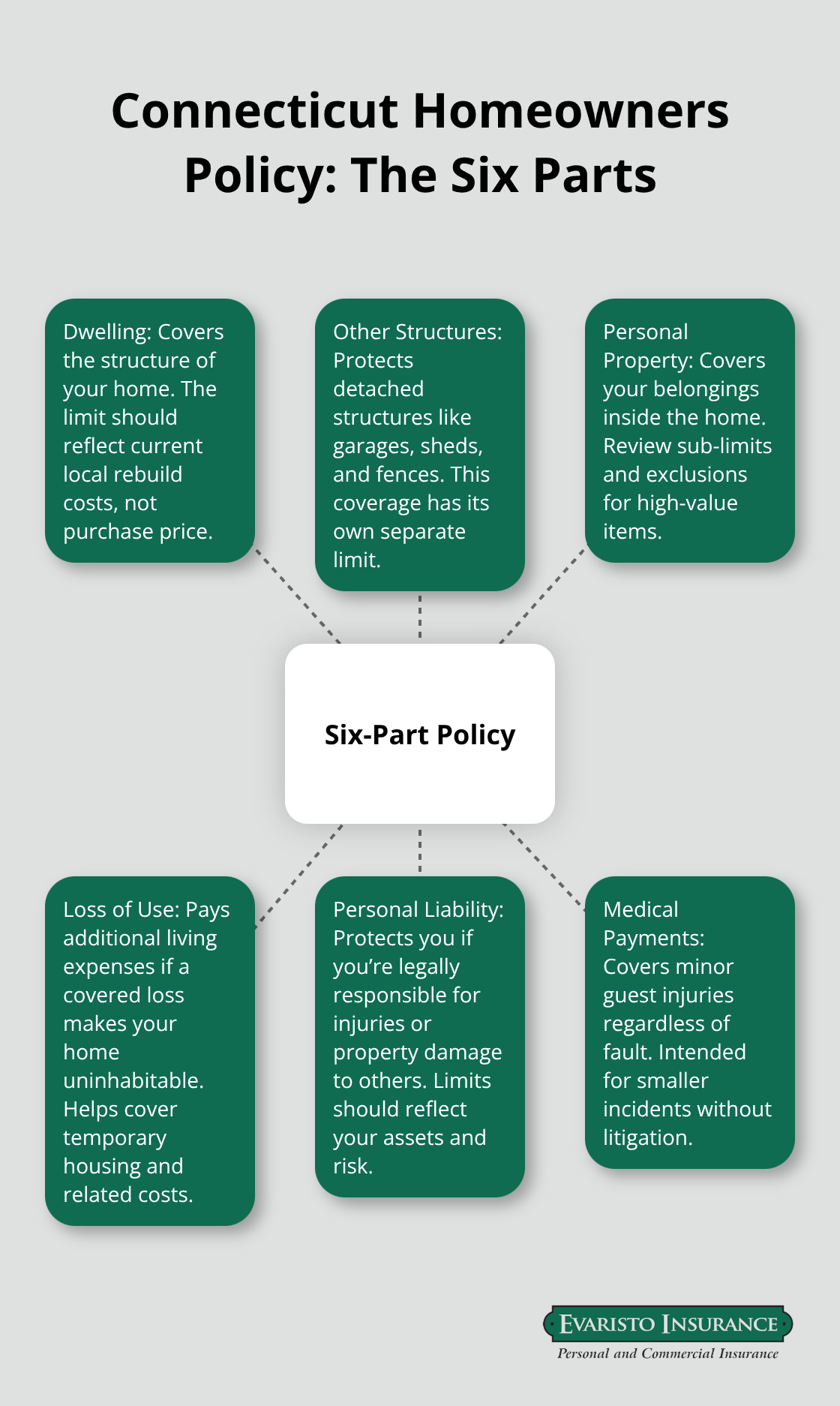

The Six-Part Policy Structure Connecticut Requires

Connecticut homeowners must carry a standard six-part policy structure mandated by lenders and state regulations. These six coverages-Dwelling, Other Structures, Personal Property, Loss of Use, Personal Liability, and Medical Payments-form the foundation of protection, but most homeowners don’t understand what each section actually covers or how much they truly need. The Connecticut Insurance Department reports that homeowners in the state pay an average of $1,582 annually, placing Connecticut in the top third of states for insurance costs. This higher cost reflects genuine risk: Connecticut’s aging housing stock, exposure to nor’easters and hurricane-force winds, and strict building codes that increase reconstruction expenses all drive premiums upward.

Dwelling Coverage That Matches Your Actual Rebuild Costs

Your dwelling coverage must reflect current rebuild costs in your area, not the purchase price of your home-a critical distinction that catches many Ellington homeowners off guard when they discover their five-year-old policy undervalues their property by tens of thousands of dollars. For homes built before 1950, the Connecticut Insurance Department specifically recommends adding code upgrade coverage, since bringing an older structure up to current building standards during reconstruction can add 20 to 40 percent to repair costs. Connecticut’s higher construction expenses make this gap especially dangerous for older properties.

Liability Protection Gaps That Leave You Exposed

Most Connecticut homeowners carry $100,000 or $300,000 in personal liability coverage, but this amount is dangerously low if someone suffers a serious injury on your property. A single lawsuit from a guest who falls on your icy driveway or a neighbor whose child drowns in your pool can easily exceed $500,000 in damages. Connecticut courts have awarded settlements in excess of $1 million for catastrophic injuries, yet most standard policies cap liability at $300,000. An umbrella policy costs only $150 to $300 annually for $1 million in additional protection and represents the single most cost-effective risk management tool available to homeowners.

Water Damage and Sewer Backup Exclusions

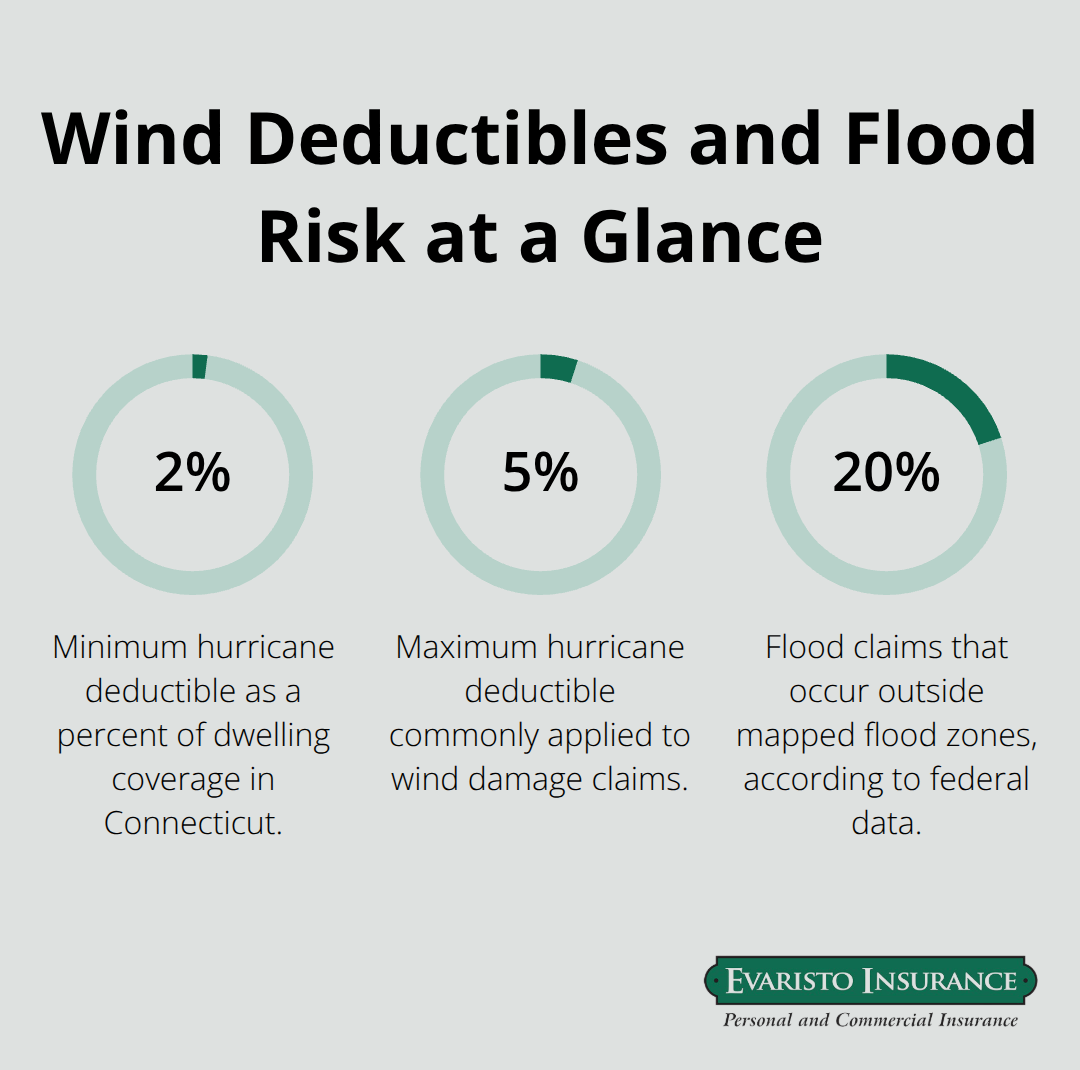

Water damage represents another massive coverage gap-standard policies exclude flood damage, sewer backups, and surface water intrusion, yet about 20 percent of flood claims occur outside mapped flood zones according to federal data. Adding a sewer backup endorsement typically costs $75 to $150 per year and covers one of the most expensive claims homeowners face, with average sewer backup losses exceeding $25,000. Coastal and historic properties in Ellington face even sharper gaps, including wind deductibles of 2 to 5 percent of dwelling coverage that apply specifically to hurricane damage, meaning a $300,000 home could have a $6,000 to $15,000 deductible when a storm hits.

How Local Agents Identify Your Coverage Gaps

These gaps don’t appear in your policy documents-they hide in what your policy explicitly excludes. A local agent who understands Ellington’s specific weather patterns, property values, and neighborhood risks can spot these holes before they cost you thousands. The right coverage strategy combines your base policy with targeted endorsements that address Connecticut’s real hazards, not generic threats.

Which Carriers Offer the Best Value for Ellington Homeowners

Multiple Carriers Mean Better Options for You

We at Evaristo Insurance represent multiple top carriers, which means we can show you options rather than push you toward one insurer’s limited offerings. Connecticut homeowners who shop only one carrier typically overpay by 15 to 25 percent compared to those who compare quotes across multiple companies. The carriers available in Ellington vary in their appetite for older homes, coastal properties, and high-value dwellings, so the cheapest quote doesn’t always deliver the coverage you actually need.

Policy Types That Match Your Home’s Age and Value

HO-3 policies dominate the Connecticut market and work well for standard homes, but if your Ellington property was built before 1950 or has significant value, an HO-5 open-peril policy from carriers like Chubb or USAA provides broader protection for both your dwelling and personal property. The difference matters: an HO-5 covers accidental damage that an HO-3 specifically excludes, which can save you thousands on a single claim. When you request quotes, demand the same coverage limits across all carriers so you’re comparing apples to apples-dwelling coverage reflecting actual rebuild costs, $300,000 minimum liability, and identical deductibles.

Deductible Strategies and Discount Stacking

Most Connecticut homeowners can reduce premiums by increasing their standard deductible from $500 to $1,000, a strategy that works only if you have emergency savings to cover that deductible when a loss occurs. Bundling your auto and home policies may be eligible for multi-policy discounts that make coverage more affordable, and adding security systems, impact-resistant roofing, or maintaining a claims-free history can each reduce premiums another 5 to 20 percent depending on your carrier.

How to Gather and Compare Quotes Effectively

Connecticut homeowners who haven’t shopped insurance in three or more years almost always discover they’re paying significantly more than comparable coverage costs today. Fresh quotes take less than 30 minutes online and often reveal 20 to 40 percent savings once you stack available discounts. Start by documenting your home’s characteristics: year built, square footage, roof age, heating system, electrical wiring condition, distance to the nearest fire station, and any protective devices like deadbolts or burglar alarms. These details directly affect your premium because they influence risk, and carriers price based on specific exposures rather than guesswork. Connecticut Insurance Department data shows that non-smokers pay less than smokers, credit history influences rates, and claims history affects future premiums, which means some homeowners strategically withhold small claims to avoid premium increases that exceed the claim value itself.

Specialized Pricing for Coastal and Historic Properties

Coastal and historic properties in Ellington face specialized pricing: wind deductibles of 2 to 5 percent apply to hurricane damage, and historic homes may use HO-8 policies that focus on repair rather than full replacement, affecting both coverage scope and premium calculations. Once you’ve gathered quotes, review the policy details beyond price-specifically which endorsements are included, what your actual deductibles are for different perils, and whether sewer backup, water damage, or ordinance coverage are added or excluded. The lowest quote doesn’t always deliver the best value if it leaves you exposed to the exact risks that destroyed your home. Understanding what each policy actually covers prepares you to make decisions about the specific protections your Ellington property needs against Connecticut’s weather and regional hazards.

Connecticut Weather Demands Specialized Coverage You Can’t Ignore

Wind Damage and Hurricane Deductibles Create Hidden Costs

Protect your Connecticut property with windstorm insurance. Nor’easters routinely produce hurricane-force winds that damage roofs and siding, coastal erosion threatens property foundations, and heavy snow loads stress structural integrity in ways that standard policies often exclude or severely limit. Your base homeowners policy covers wind damage from storms, but the deductible structure in Connecticut creates a dangerous trap: most carriers apply a separate hurricane deductible of 2 to 5 percent of your dwelling coverage amount, meaning a $300,000 home carries a $6,000 to $15,000 deductible when a hurricane hits. This deductible applies only to wind damage, not to other perils in the same storm, so a nor’easter that damages your roof through wind but also causes interior water damage splits the claim into two separate deductibles. Understanding this distinction before a storm arrives determines whether you can actually afford to file a claim.

Coastal Properties Face Specialized Risks and Market Limitations

Coastal properties in Ellington face even sharper exposure: erosion coverage is typically excluded entirely, and some carriers have simply exited the coastal market, forcing homeowners into the Connecticut FAIR Plan, which offers bare-minimum coverage at premium rates significantly higher than standard market policies. The solution isn’t to accept inadequate coverage-it’s to know exactly what your policy covers before disaster strikes and to add targeted endorsements that address Connecticut’s specific weather patterns rather than generic risks.

Flood Risk Extends Beyond Mapped Flood Zones

Water damage represents the second major exposure Connecticut homeowners consistently underestimate. Flood damage from rising water is excluded from standard policies, but about 20 percent of flood claims occur outside mapped flood zones according to federal data, meaning properties in Ellington that aren’t in Special Flood Hazard Areas still face genuine flood risk from heavy rainfall, poor drainage, or localized flooding. Sewer backup-when municipal sewers overflow during heavy rain and force sewage into your basement-costs homeowners an average of $25,000 or more per claim, yet standard policies exclude this entirely unless you add a sewer backup endorsement for $75 to $150 annually.

Water Damage Coverage Varies by Source and Policy Language

Surface water intrusion, groundwater seepage, and water damage from ice damming on roofs each carry different coverage rules and exclusions depending on your specific policy language. A local agent who understands Ellington’s drainage patterns, soil conditions, and flood history can recommend whether flood insurance through the National Flood Insurance Program makes financial sense for your property, or whether adding sewer backup coverage alone addresses your highest-probability risk. The NFIP typically imposes a 30-day waiting period before coverage activates, so waiting until flood season arrives means you cannot purchase protection in time.

Building Your Water Protection Strategy

Evaristo Insurance helps Ellington homeowners map their specific water exposures and build coverage strategies that address real risks rather than theoretical ones, comparing the cost of endorsements against your property’s actual vulnerability and your financial ability to absorb a loss without insurance.

Final Thoughts

Ellington CT homeowners coverage works only when it matches your actual property, your real risks, and your financial situation. The gaps we’ve outlined-undervalued dwelling coverage, inadequate liability limits, excluded water damage, and hurricane deductibles that surprise you when storms arrive-aren’t theoretical problems. Connecticut homeowners file these claims every year, and those without proper coverage face devastating financial consequences.

Your next step is straightforward: gather quotes from multiple carriers and demand identical coverage limits across all quotes so you compare actual protection, not just price. Document your home’s specifics (year built, roof age, wiring condition, distance to the fire station, and any security features) because these details directly affect your premium and your carrier’s willingness to insure you. Request quotes that include sewer backup endorsement costs, ask about hurricane deductibles explicitly, and confirm whether your dwelling coverage reflects current rebuild costs in your area.

Local expertise matters because Ellington’s weather patterns, property values, and neighborhood risks differ from statewide averages. An agent who understands your specific area spots coverage gaps that national carriers miss and recommends endorsements that address your actual exposures rather than generic threats. We at Evaristo Insurance have served Connecticut homeowners since 1989, comparing multiple top carriers to deliver coverage tailored to your property and your budget.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!