Contractor Liability Insurance CT: Managing On‑Site Risks

One accident on a job site can cost your contracting business thousands in liability claims, legal fees, and lost time. Contractor liability insurance in CT protects you from these financial disasters by covering property damage, bodily injuries, and defense costs.

At Evaristo Insurance, we work with Connecticut contractors every day who face unique on-site risks-from weather delays to equipment theft to third-party injuries. This guide walks you through what coverage you actually need and how to choose the right policy for your business.

What Your Contractor Liability Policy Actually Covers

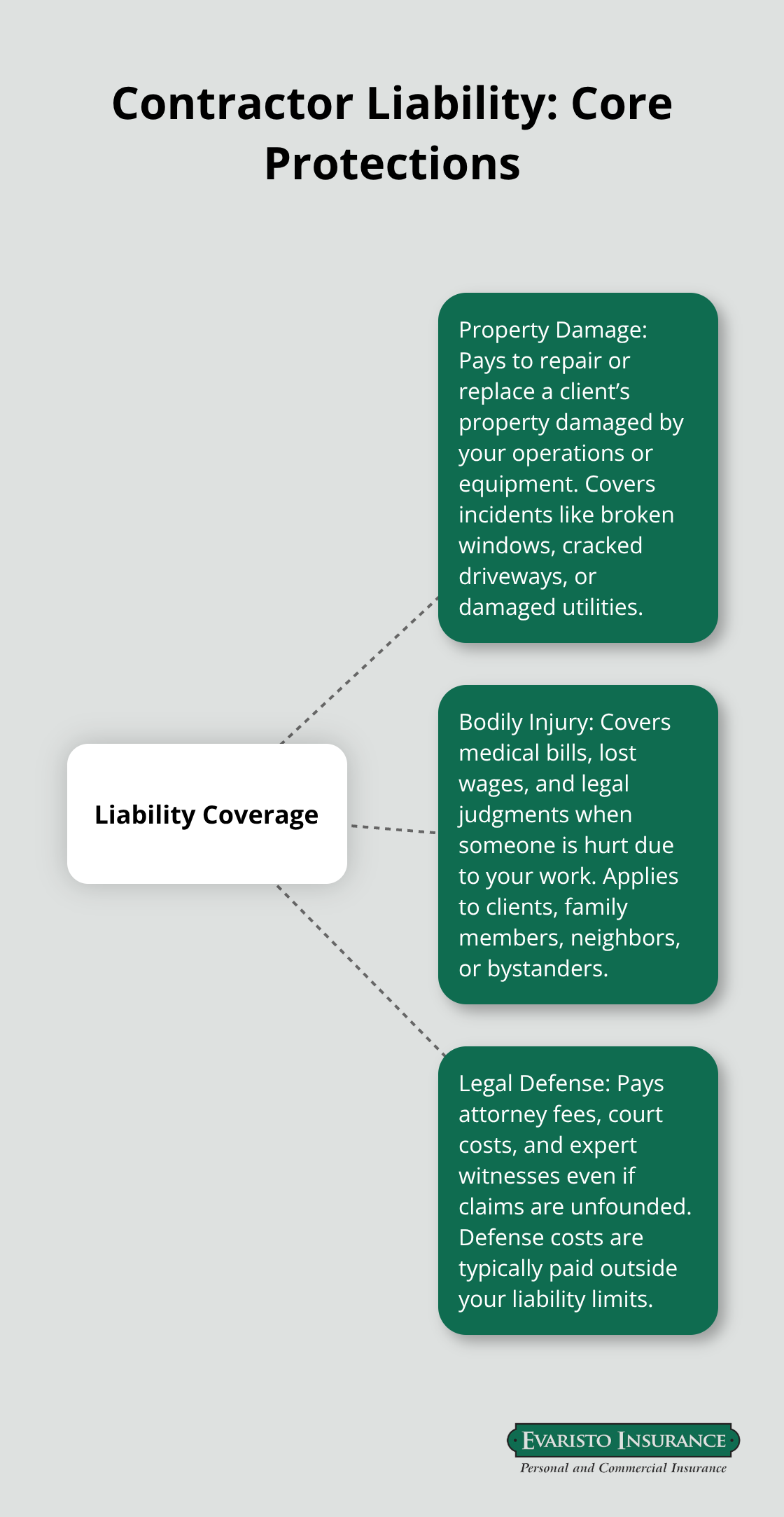

Contractor liability insurance protects your business from three major financial exposures that appear regularly on Connecticut job sites. Property damage coverage pays when your work or equipment damages a client’s home, neighboring property, or existing structures during the project. If you accidentally break a window while installing siding, crack a driveway while operating machinery, or damage underground utilities, this coverage handles the repair costs and associated liability. Bodily injury liability covers medical expenses and legal claims when someone gets hurt because of your work or negligence on site. A customer, their family member, or a passerby injured at your job site can file a claim, and this coverage pays their medical bills, lost wages, and court judgments if they sue. Connecticut contractors typically carry $1 million per occurrence and $2 million aggregate limits, according to Insureon data, which represents the industry standard for residential work.

Property Damage and Bodily Injury: Your Core Protections

These two coverage types form the foundation of contractor liability. Property damage protects your business when your actions harm someone else’s assets on or near the job site. Bodily injury liability steps in when your work causes physical harm to anyone present-clients, their families, neighbors, or bystanders. Together, they address the two most common lawsuit scenarios contractors face in Connecticut.

Without both components, a single accident can wipe out your business savings and future earnings.

Legal Defense Costs: The Hidden Expense Most Contractors Underestimate

The third pillar of contractor liability is legal defense coverage, and this component often surprises contractors who underestimate litigation expenses. When a claim lands, your insurer covers attorney fees, court costs, expert witness testimony, and settlement negotiations before any judgment is paid. Legal defense costs can be covered even if claims are found to be unfounded, which provides significant financial relief for small businesses. Your policy pays these costs separately from your coverage limits, which means you don’t deplete your $1 million protection just defending yourself in court. This separation is critical because a contractor facing multiple claims or a serious injury lawsuit needs robust legal resources without watching their coverage limits disappear into attorney bills. Many contractors mistakenly think general liability covers only the final judgment or settlement, but the legal defense provision is what keeps your business operational while claims are resolved.

Why Coverage Limits Matter More Than Price

The limits you select directly determine how much protection you actually have when disaster strikes. Connecticut contractors who carry inadequate limits face personal liability exposure if a claim exceeds their policy maximum. Selecting the right limits requires honest assessment of your project values, crew size, and risk profile-not just copying what your competitor carries. A local Connecticut insurance agent can help you evaluate whether standard $1 million per occurrence limits fit your work or whether higher limits make sense for larger projects.

Common On-Site Risks Contractors Face in Connecticut

Weather Delays and Material Damage

Connecticut’s weather patterns create real financial exposure for contractors working outdoors. Spring thaw cycles, winter storms, and summer thunderstorms delay projects regularly, and these delays ripple through your budget in ways liability insurance alone cannot address. A roofing crew stopped by three days of rain loses productivity, and if that delay pushes your crew into overtime or forces you to reschedule equipment rentals, those costs compound quickly. Weather damage to materials stored on site-lumber warping, drywall absorbing moisture, or paint freezing in unheated spaces-becomes your financial problem once materials arrive at the job. Your contractor liability policy covers damage you cause to existing structures, but it does not cover weather damage to your own materials or project delays. Many Connecticut contractors carry builder’s risk insurance, which averages about $105 per month and covers materials, equipment, and the structure itself during construction.

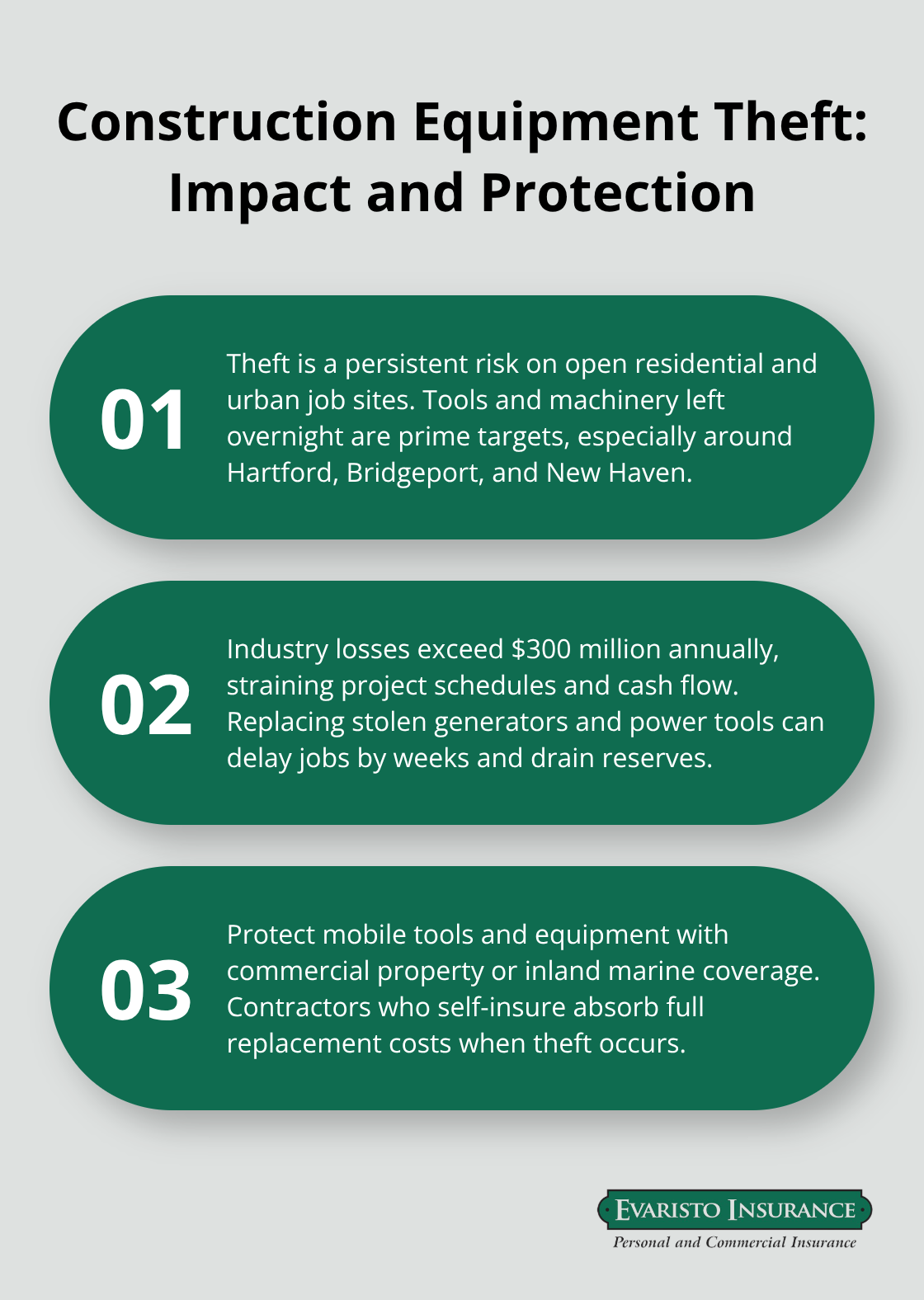

Equipment Theft and On-Site Loss

Equipment theft and damage represent a second major exposure that hits contractors hard in Connecticut. Tools left on open job sites, vehicles parked in residential neighborhoods overnight, and expensive machinery like compressors or generators disappear regularly, particularly in higher-density areas around Hartford, Bridgeport, and New Haven. The National Equipment Register reports that construction equipment theft costs the industry over $300 million annually, and Connecticut’s urban and suburban mix makes job sites attractive targets.

Replacing a stolen generator, pneumatic tools, or power equipment can delay projects by weeks and cost thousands out of pocket if your policy does not cover equipment at job sites. Commercial property insurance or inland marine coverage protects equipment and tools, but many contractors overlook these policies and self-insure, which means absorbing full replacement costs when theft occurs.

Worker Injuries and Third-Party Liability Claims

Worker injuries and third-party claims form the third critical risk category. Connecticut’s workers’ compensation requirements mandate coverage for employees, and violations carry fines up to $5,000 per violation plus criminal penalties, according to the Connecticut Department of Labor. A single serious injury-a fall from scaffolding, electrocution, or crush injury-can trigger both workers’ comp claims and third-party liability claims if a subcontractor or visitor is injured. Third-party bodily injury claims fall under your contractor liability policy, but the medical costs and legal expenses mount quickly. A hospitalization for a serious construction injury easily exceeds $50,000 in medical expenses alone, and if permanent disability results, wage replacement and ongoing care costs multiply further. Proper safety training and equipment reduce both injury frequency and insurance claims, which insurers recognize through lower premiums over time. Your liability limits must account for the possibility of multiple injuries on large projects or high-value residential work where damages can exceed standard $1 million per occurrence limits. Understanding these three risk categories helps you evaluate whether your current coverage matches your actual exposure-and whether you need additional protection before your next project starts.

How to Choose the Right Contractor Liability Policy

Match Your Coverage Limits to Actual Project Risk

Selecting contractor liability coverage starts with honest math about your exposure. Most Connecticut contractors default to $1 million per occurrence and $2 million aggregate because that’s what 97% of their peers carry, according to Insureon data, but defaulting to industry standard limits is exactly how contractors end up underinsured. Your roofing crew handling a $500,000 residential renovation faces different exposure than a crew installing kitchen cabinets in a modest home, yet many contractors pay the same premium for identical limits regardless of scope.

Add up your average project value, multiply by your crew size, and factor in the cost of a serious injury claim (hospitalization for construction injuries averages $50,000 in medical expenses alone). Then ask yourself whether $1 million covers the worst-case scenario on your typical job. If you regularly work on high-value homes in Fairfield County or handle large commercial renovations, standard limits leave you exposed to personal liability if a claim exceeds your policy maximum.

Compare Quotes Across Multiple Carriers

Shopping quotes across carriers reveals dramatic price differences for identical coverage. General liability insurance for construction averages about $82 per month through Insureon data, but premiums vary significantly by trade risk-roofers average $267 per month while locksmiths pay $42 per month, showing how work type drives costs. Connecticut carriers price policies differently based on your claims history, crew experience, safety record, and local loss data, which means three quotes take an hour but save hundreds annually.

When you request quotes, provide detailed information about your specific work-roofing, siding, interior renovation, structural work-because vague descriptions lead to inaccurate pricing. Bundling general liability with commercial property coverage into a business owner’s policy averages about $98 per month and typically costs less than separate policies; the typical GL and property bundle runs around $112 per month for Insureon customers.

Work with a Local Connecticut Insurance Agent

A local Connecticut insurance agent brings knowledge of which carriers underwrite your trade competitively and which ones avoid construction work altogether. They handle certificate of insurance requests and policy adjustments without the back-and-forth of online platforms. As an independent agency, Evaristo Insurance compares multiple top carriers, which means you get options rather than being locked into one company’s pricing or appetite for your risk profile.

Final Thoughts

Contractor liability insurance CT protects your business from the financial devastation that follows a single accident on site. The three coverage pillars-property damage, bodily injury, and legal defense costs-work together to shield your assets when claims arrive. Matching your coverage limits to your actual project risk, rather than defaulting to industry standards, ensures you have real protection instead of just a policy number.

Shopping quotes across multiple carriers reveals pricing differences that can save hundreds annually, and bundling general liability with property coverage typically reduces your overall cost. Connecticut’s regulatory environment, weather patterns, and regional loss history shape which carriers price your work competitively and which ones avoid construction altogether. An independent agent compares multiple top carriers instead of locking you into one company’s appetite for your risk profile.

Gather details about your typical project scope, crew size, and annual revenue, then contact Evaristo Insurance to compare options and discuss whether your current limits match your actual exposure. A certificate of insurance typically issues within 24 hours after applying, so you can move forward with confidence that your business stays protected before your next job starts.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!