Landscape Contractor Insurance CT: Comprehensive Coverage for Professionals

Landscape contractors in Connecticut face unique risks that standard business insurance simply doesn’t cover. From equipment damage to liability claims, the right protection is essential to keep your operation running smoothly.

At Evaristo Insurance, we understand the specific challenges landscape contractors encounter. We’ve built our expertise around helping professionals like you secure the coverage that actually matters.

Why Specialized Insurance Matters for Your Landscape Business

Landscape contractors in Connecticut operate in an environment where standard business insurance creates dangerous gaps. A general commercial policy won’t cover equipment stolen from your truck, won’t protect you when a client’s deck is damaged by your machinery, and won’t pay for an employee’s medical bills after a jobsite accident. Contractors who’ve learned this lesson the hard way understand that these oversights cost real money.

Property Damage Claims Hit Hard and Fast

A single incident can devastate your finances. When your crew damages a client’s fence with heavy equipment or a water feature malfunction causes flooding weeks after installation, general liability insurance covers the repair costs and legal defense. Connecticut general liability insurance for landscapers carries real costs that seem manageable until you face a significant property damage claim out of pocket. That claim wipes out months of profit without proper coverage. Connecticut contractors working on residential properties often deal with high-value homes where damage claims routinely exceed $25,000. The risk isn’t theoretical; it’s baked into every project where your equipment operates near structures, utilities, or expensive landscaping features.

Equipment and Vehicles Require Separate Protection

Your mowers, Bobcats, excavators, and trailers represent your ability to earn income, yet standard policies leave them exposed. Tools and Equipment coverage protects owned or leased gear from theft or damage whether stored at your shop or sitting on a jobsite. Connecticut landscapers who operate year-round and store expensive equipment face real theft exposure, especially during winter months when some sites sit idle. Commercial Auto insurance is equally critical because it covers business-owned vehicles and specifically protects trailers when you list them on your policy-a gap many contractors overlook. A collision involving your work truck leaves you paying repairs from cash reserves while you lose billable hours without this coverage.

Workers’ Compensation Protects Your Team and Your Business

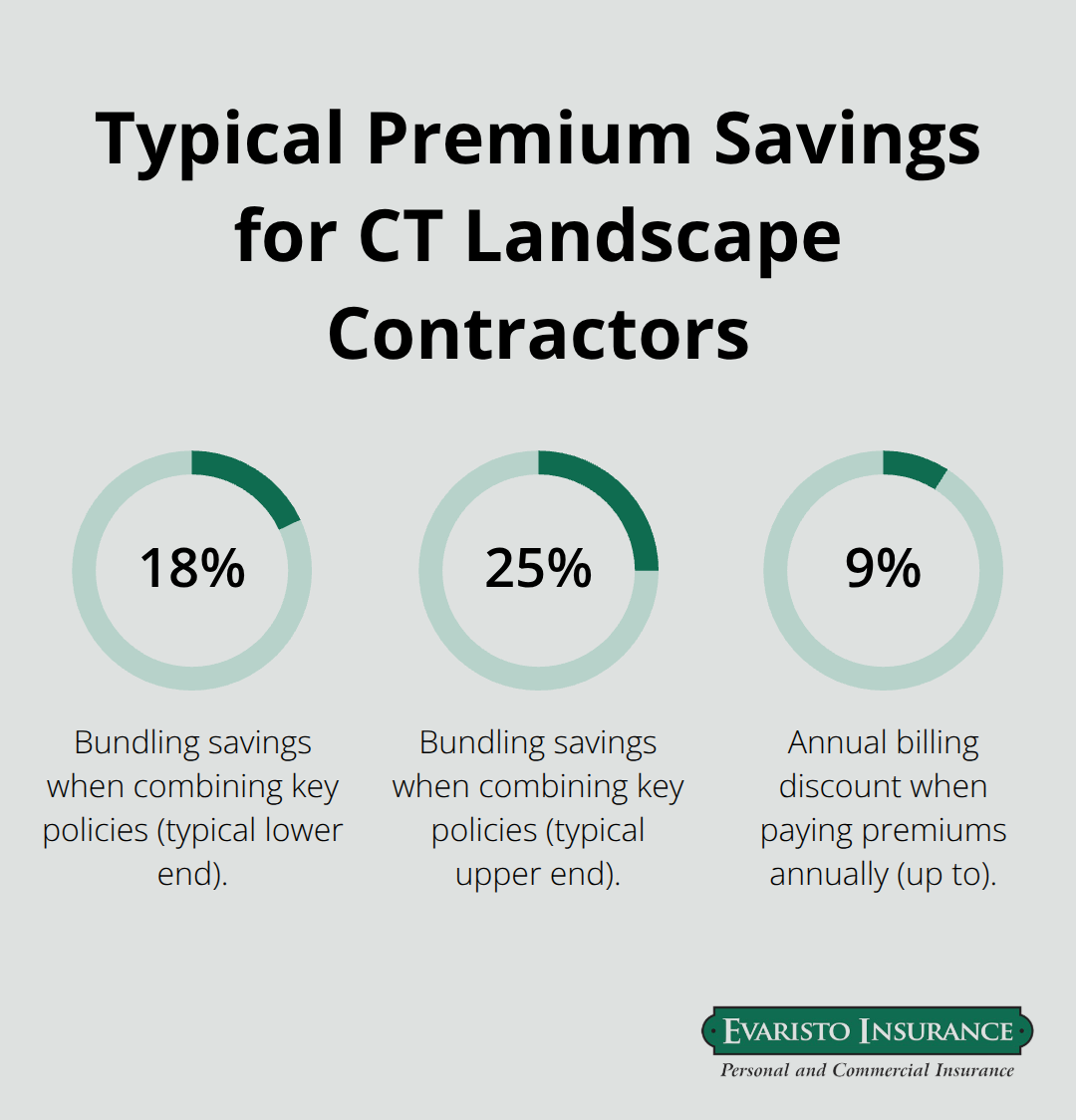

Workers’ Compensation coverage in Connecticut is mandatory once you hire employees, and it covers medical expenses and lost wages for work-related injuries. One serious injury could trigger a lawsuit exceeding $100,000, far surpassing what you’d ever pay in premiums. Specialized landscape contractor insurance bundles these protections together, and bundling typically saves 18 to 25 percent compared to purchasing policies separately.

The specific types of coverage you need depend on your operation’s scope and the services you offer. Understanding what each policy covers-and what it doesn’t-helps you build a protection plan that actually matches your business.

Essential Coverage Types for Landscape Contractors

General liability insurance forms the foundation of your protection, but Connecticut landscape contractors need more than one policy to operate safely. General liability insurance costs between $18 and $1,000 per month for small Connecticut businesses with two employees, covering third-party bodily injury and property damage during and after project completion. This policy pays when a client suffers injury from your equipment or when you damage their property, yet it explicitly excludes vehicle-related accidents. That gap matters because your work trucks, trailers, and equipment represent both your biggest assets and your most frequent source of claims.

Commercial Auto and Equipment Protection

Commercial auto insurance covers business-owned vehicles and physical damage to your trucks and trailers, protecting you from repair costs and lost income when accidents occur. Connecticut contractors often overlook trailer coverage, creating expensive gaps when equipment trailers sustain damage en route to jobsites. Tools and equipment coverage protects owned or leased mowers, Bobcats, excavators, and other gear from theft or damage whether stored at your shop or sitting idle on client properties. Connecticut landscapers who operate year-round face genuine theft exposure during winter months when equipment sits unused, making this coverage a critical investment.

Bundling Policies for Maximum Savings

Bundling these coverages together typically saves 18 to 25 percent compared to purchasing policies separately, which is why many Connecticut contractors combine general liability, commercial auto, and tools coverage into a Business Owner’s Policy or specialized landscaping package. A complete package including general liability, commercial auto, tools and equipment, and workers’ compensation runs approximately $266 per month in Connecticut according to MoneyGeek, significantly less than buying each policy independently. The most practical approach involves paying annually rather than monthly, which yields 6 to 9 percent discounts on your total premiums.

Coverage Limits and Contract Requirements

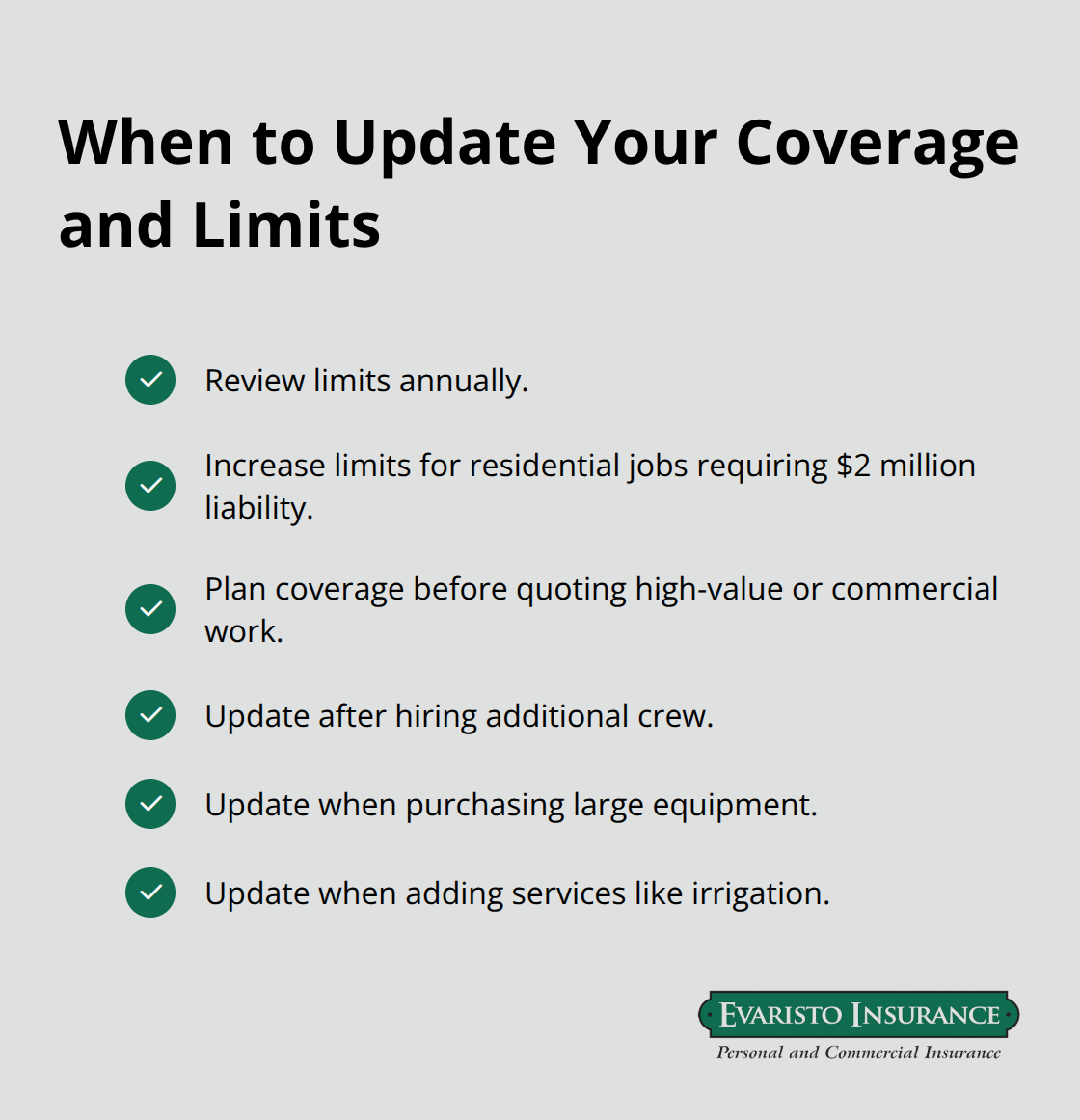

Your coverage limits matter just as much as the policies themselves; residential clients frequently require $2 million in liability limits for contract work, far exceeding the $1 million standard on basic policies. Connecticut contractors working on high-value properties or commercial accounts should plan coverage accordingly before quoting projects. Update your coverage annually or whenever your operation grows-hiring additional crew, purchasing large equipment, or adding services like irrigation work-to avoid gaps and qualify for potential discounts that reflect your reduced risk profile.

The coverage types you select form only part of your protection strategy. Connecticut’s unique weather patterns and seasonal demands create specific risks that demand attention beyond standard policies.

Connecticut’s Toughest Landscape Risks

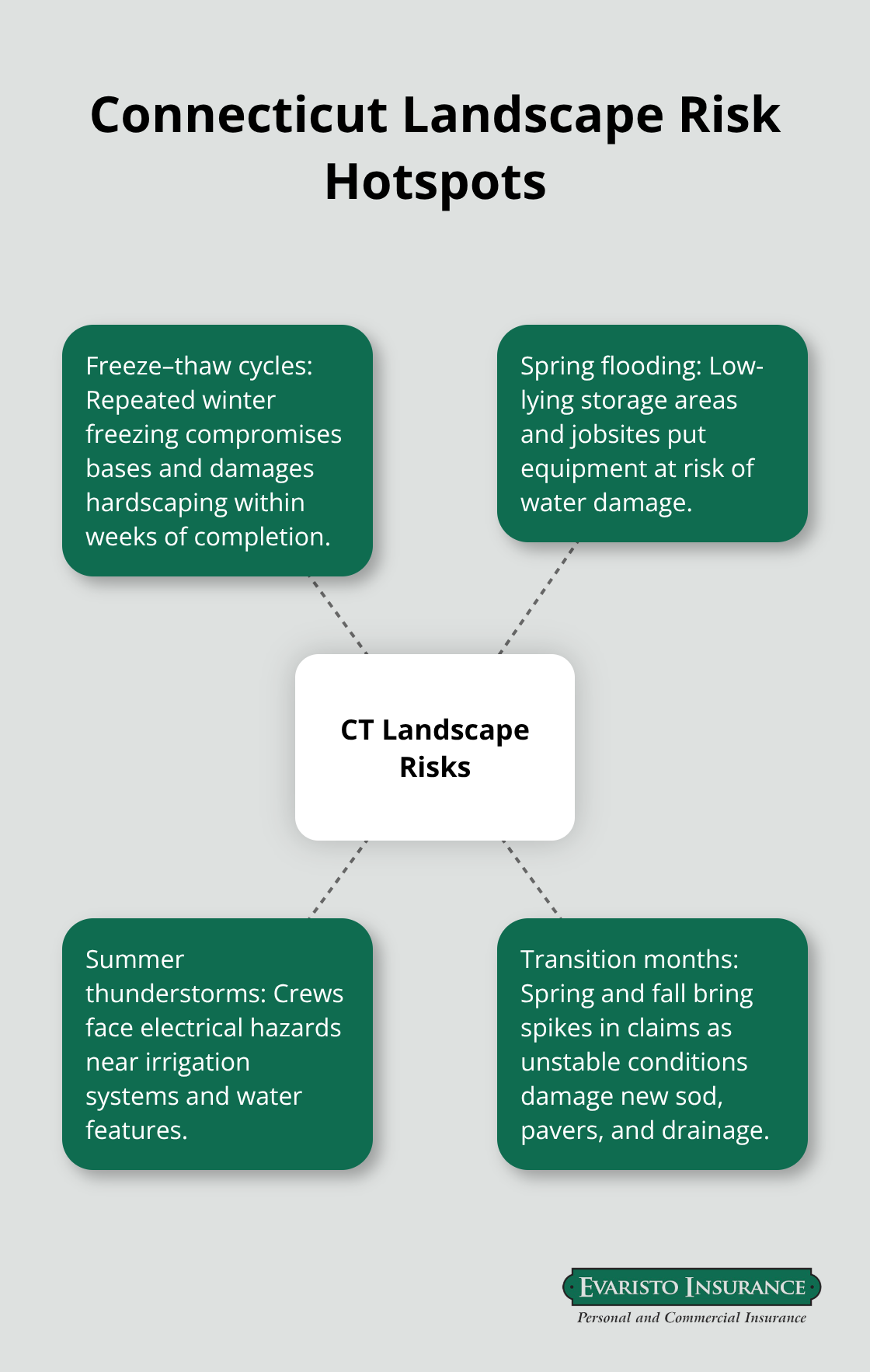

Connecticut’s weather patterns create genuine operational hazards that standard policies don’t adequately address. Winter freeze-thaw cycles damage hardscaping installations within weeks of completion, spring flooding threatens equipment stored in low-lying areas, and summer thunderstorms expose crews to electrical hazards near irrigation systems and water features. Connecticut landscapers operating year-round face weather-related claims that spike during spring and fall transition months when unstable conditions damage newly installed sod, pavers, and drainage systems.

Weather Damage and Seasonal Installation Failures

A retaining wall installed in October can fail by March when repeated freezing cycles compromise the base, leaving your business liable for repairs that can easily reach $15,000 or more on residential properties. Your general liability policy covers the damage claim, but only if you’ve properly disclosed the work scope to your insurer and maintained adequate limits for the project value. Many Connecticut contractors underestimate seasonal risks because they don’t track how weather patterns affect their completed work during critical post-installation periods. Connecticut’s liability environment means contractors should verify that their policies include completed operations coverage, since damage claims often emerge weeks or months after work finishes.

Chemical and Pesticide Liability Exposure

Chemical and pesticide exposure represents a liability exposure that requires explicit coverage verification with your broker. Connecticut landscapers who apply fertilizers, herbicides, or fungicides face claims from client health issues, environmental contamination, or damage to unintended vegetation that can exceed $50,000 when property value is involved. Environmental liability coverage specifically protects against leaks, spills, and chemical drift, yet many standard landscaping policies exclude or severely limit this protection. Verify that your policy explicitly covers the chemicals and application methods your crew uses on client properties.

Slip and Fall Claims on Wet and Sloped Terrain

Slip and fall accidents on client properties occur constantly during wet conditions, icy mornings, or after rain when crews work on sloped terrain or near water features. A client who slips on your freshly installed pavers or a crew member who falls from a wet retaining wall creates medical bills and legal exposure that general liability covers only when your policy explicitly includes premises liability for both completed operations and ongoing work. Increasing your umbrella liability coverage to $1 million or $2 million is advisable when you perform hardscaping, heavy equipment work near buildings, or any project involving digging near underground utilities, as these high-risk activities routinely generate claims exceeding your standard policy limits.

Final Thoughts

Landscape contractor insurance in Connecticut requires a layered approach that addresses the specific risks your operation faces. General liability insurance forms your foundation, protecting against third-party injury and property damage claims that emerge during and after project completion. Commercial auto coverage shields your vehicles and trailers from collision damage and theft, while tools and equipment protection keeps your mowers, excavators, and other gear covered whether stored at your shop or sitting on jobsites. Workers’ compensation is mandatory once you hire employees and prevents catastrophic financial exposure from workplace injuries.

We at Evaristo Insurance understand that Connecticut landscape contractors need more than generic business coverage. Since 1989, we’ve served Connecticut businesses with tailored protection that matches your actual operations, not cookie-cutter policies that leave gaps. Our independent agency compares multiple top carriers to find competitive pricing and coverage that reflects your specific services, equipment values, and risk profile.

Contact Evaristo Insurance to discuss your current coverage and identify any gaps in your landscape contractor insurance CT protection. Our local offices in Ellington and West Hartford serve Connecticut landscape contractors with hands-on advocacy and the expertise to navigate contract requirements, coverage limits, and premium optimization. We’ll review your operation, explain what each policy covers, and help you secure the right combination of general liability, commercial auto, equipment protection, and workers’ compensation at a price that makes sense for your business.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!