Contractor Workers Comp CT: Understanding Your Coverage

Contractor workers comp CT is a legal requirement in Connecticut, yet many contractors operate with gaps in their coverage that could prove costly. At Evaristo Insurance, we’ve seen firsthand how misclassification and insufficient limits leave contractors vulnerable.

This guide walks you through what coverage you actually need, what it covers, and the common mistakes that leave contractors exposed.

What Contractors Must Know About Workers Comp in Connecticut

Connecticut’s Legal Requirements for Contractors

Connecticut law mandates that most contractors carry workers compensation insurance, but the specifics depend on your business structure and how you classify your workforce. The Connecticut General Statutes and the Workers Compensation Commission enforce these requirements strictly, and violations carry penalties that can exceed your annual premium costs. If you operate as a sole proprietor or LLC with employees, coverage is mandatory. If you hire subcontractors, you must verify whether they carry their own insurance or fall under your policy-this distinction matters legally and financially.

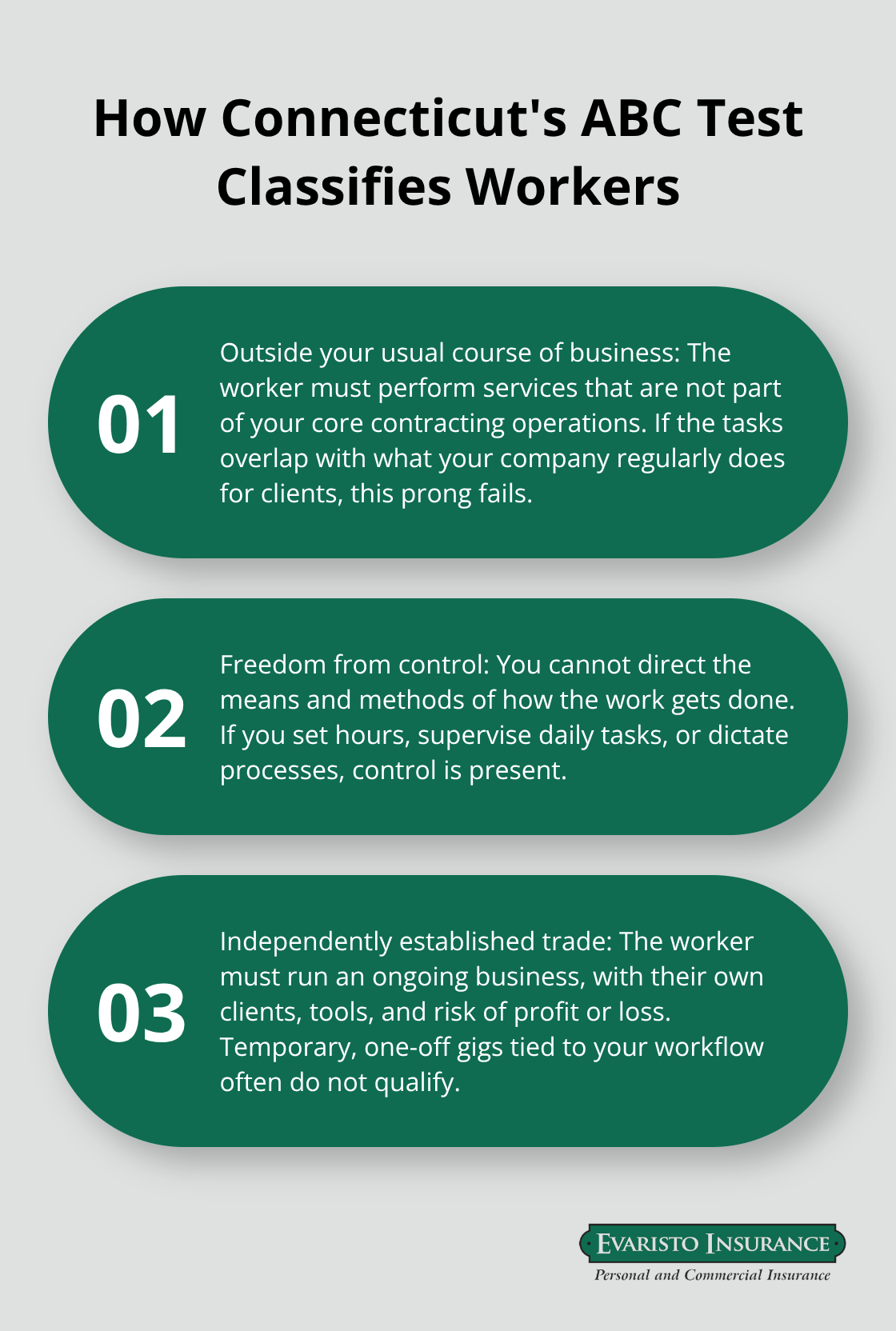

The ABC Test: Employee vs. Independent Contractor

The ABC Test determines whether someone qualifies as an independent contractor or employee in Connecticut. All three criteria must be met: the worker operates outside your usual business, you don’t control how they perform the work, and they maintain an independently established trade. Most contractors fail this test because they direct the work or the tasks fall within their core business. Misclassification exposes you to liability and leaves workers unprotected, so accuracy in classification protects both parties.

Understanding Your Premium Costs

The Hartford reports that Connecticut’s average workers compensation premium sits around $1,555 annually, though this varies significantly based on payroll size, job classification, and claims history. Pay-as-you-go arrangements let you avoid large upfront payments and instead pay premiums based on actual payroll-a practical option for seasonal or growing operations. Your NCCI class code, assigned by the National Council on Compensation Insurance, determines your base rate; higher-risk work like roofing costs substantially more than lower-risk roles like office management.

Multi-State Operations and Self-Insurance Options

Construction contractors and specialty trades face steeper premiums because injury rates in these sectors are documented and factored into pricing. If you operate across multiple states, Connecticut’s legal minimum coverage differs from New York and New Jersey, making compliance more complex. Self-insurance exists as an option for larger contractors, but it requires formal certification, security deposits, and ongoing financial reporting through the Workers Compensation Commission-most small to mid-size contractors find traditional coverage simpler and more cost-effective. Understanding what your policy actually covers becomes critical once you select your coverage type.

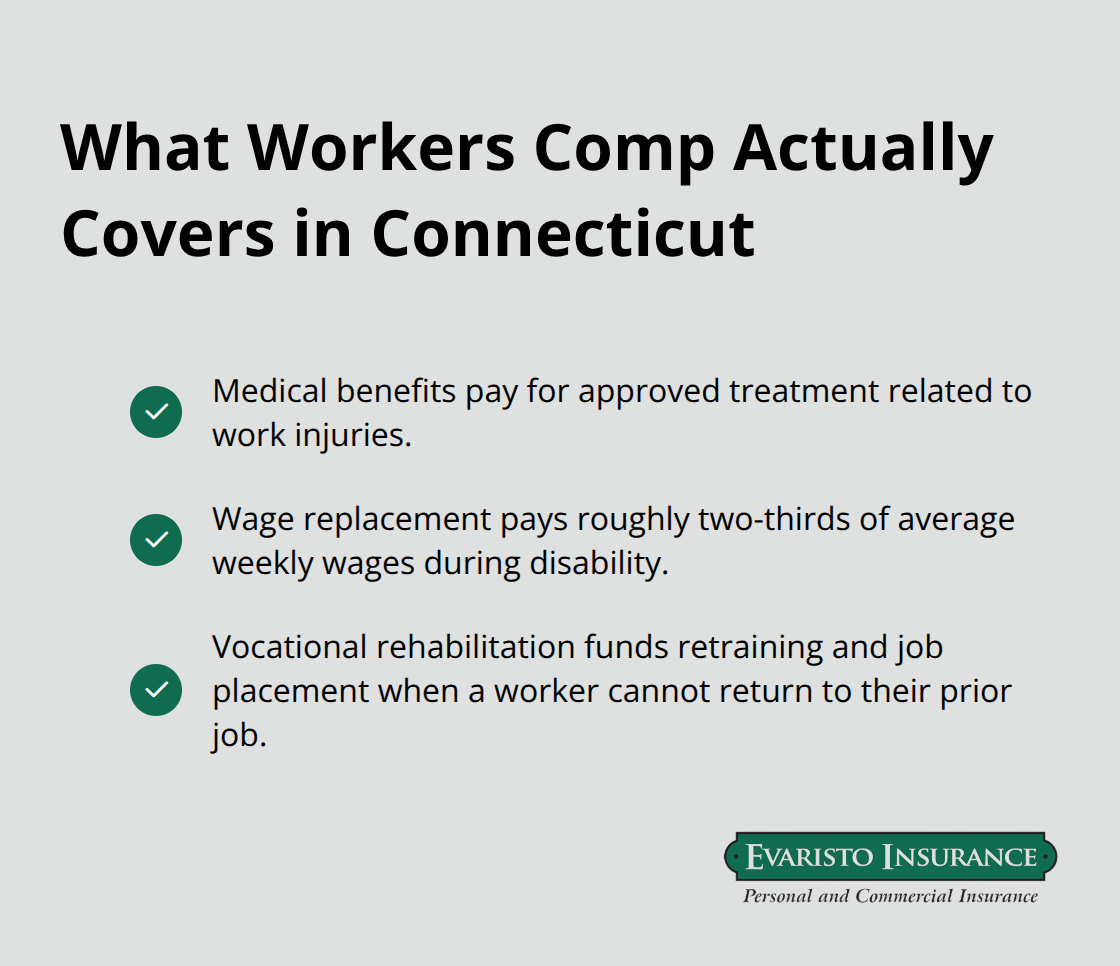

What Your Connecticut Workers Comp Policy Actually Covers

Medical Benefits and Treatment

Connecticut workers compensation policies mandate three core benefit categories that contractors must understand concretely. Medical benefits cover all treatment related to a work injury, including emergency care, surgery, hospitalization, prescription medications, and ongoing physical therapy at facilities using approved practitioners from the state’s official list. Your specific cost depends on your NCCI classification, payroll size, and claims history.

Wage Replacement and Income Protection

Wage replacement covers roughly two-thirds of your employee’s average weekly wage while they cannot work, with Connecticut law setting specific maximum and minimum weekly amounts that adjust annually. This protection matters most when an injury sidelines a skilled worker for weeks or months-the wage replacement keeps your employee financially stable while you manage the operational disruption.

All three categories of reported claims require the use of the DAS Workers’ Compensation Claim Reporting Packet to document the facts of the reported claim, and medical providers expect timely payment under your policy terms.

Vocational Rehabilitation and Return-to-Work Support

Vocational rehabilitation activates when an injured worker cannot return to their previous job and needs retraining or job placement assistance to transition to different work. Connecticut’s vocational rehabilitation programs provide job evaluations, employment capability assessments, and rehabilitation payments to help injured workers return to productive work, but only if your policy includes adequate rehabilitation coverage. These protections are not theoretical; they represent what actually gets paid when your employee files a claim.

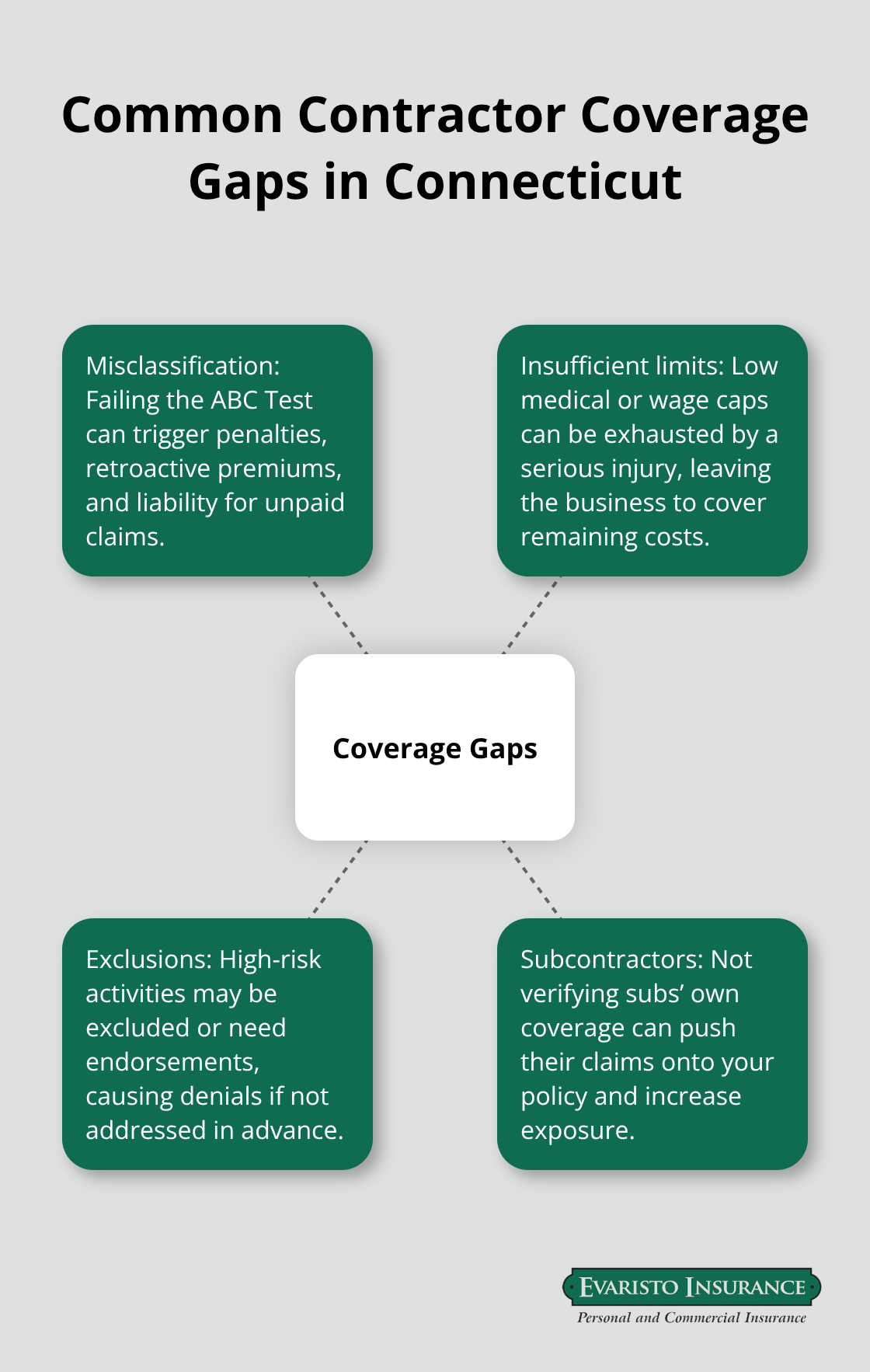

The Real Cost of Insufficient Coverage Limits

Insufficient coverage limits create serious financial exposure for contractors. If your policy caps medical benefits too low or sets disability wage replacement at minimums rather than higher limits, a serious injury quickly exhausts your coverage and leaves you liable for remaining costs. Most contractors discover their actual needs exceed their initial coverage only after reviewing real claims or consulting with a broker who specializes in construction risks. The time to address gaps is now, before an injury occurs, not after.

Identifying Coverage Gaps Before They Cost You

Many contractors underestimate what their policy covers because they never read beyond the declarations page, leaving them surprised when claims are denied for excluded work activities or when coverage limits fall short of actual medical costs. Your policy’s specific exclusions and limits determine whether you face financial exposure on a claim, making a thorough review essential. Understanding these details positions you to spot the common gaps that leave contractors most vulnerable.

Common Gaps in Contractor Coverage

Misclassification of Workers

Misclassification of workers stands as the single most expensive mistake contractors make in Connecticut. The ABC Test applies three factors for determining a worker’s employment status, but contractors routinely misapply it because they focus on one criterion while ignoring the others. Incorrect classification exposes contractors to penalties, plus retroactive premium assessments and potential liability for unpaid workers compensation claims.

What makes this worse is that many contractors classify workers as independent contractors specifically to avoid premium costs, then face enforcement action when the state audits their payroll records. Connecticut’s Workers Compensation Commission actively investigates misclassification, particularly in construction trades where the financial incentive to misclassify is highest. If a worker you classified as an independent contractor files an injury claim and the state determines they were actually an employee, you become personally liable for all medical costs and wage replacement benefits that should have been covered by your policy.

The practical solution is brutal honesty: if you control how the work gets done, if the work falls within your core business operations, or if the worker depends on you for ongoing employment, they are an employee under Connecticut law. Treating them otherwise is not a gray area-it is a violation with real financial consequences.

Insufficient Coverage Limits

Insufficient coverage limits and hidden exclusions create a second category of exposure that contractors discover only when claims hit their desk. Your NCCI classification determines your base premium rate, but it does not determine your coverage limits; you choose those limits when you purchase your policy, and many contractors choose minimums to save money.

Connecticut law sets minimum wage replacement at roughly two-thirds of average weekly wages, but it also sets maximums that adjust annually-your policy might cap benefits at the state maximum even though your employee’s actual wages exceed that cap. Medical benefits similarly operate under limits that your specific policy sets, meaning a serious injury requiring extended hospitalization and rehabilitation can exhaust your coverage while the employee still needs ongoing treatment.

Exclusions for Specific Work Activities

Exclusions for specific work activities hide in policy language that most contractors never read until a claim gets denied. High-risk activities like work at heights above certain thresholds, equipment operation without specific certifications, or work in hazardous environments may carry exclusions or require additional endorsements to your base policy.

A roofing contractor who assumes their policy covers all roofing work might discover it excludes work on steep pitches or structures above a certain height. The only way to identify gaps in coverage is to request a detailed coverage summary from your broker that explicitly lists what is and is not covered under your specific policy terms, then cross-reference that against the actual work your crews perform on job sites (this step prevents costly surprises after an injury occurs). Discovering gaps after an injury costs contractors far more than the time spent on coverage verification now.

Final Thoughts

Contractor workers comp CT protects your business and your crew, but only if your coverage matches your actual operations. Start by pulling your current policy and requesting a detailed coverage summary from your broker that lists every type of work your crews perform, then cross-reference that list against what your policy actually covers. Check your NCCI classification to confirm it matches your business operations, review how you’ve classified each worker under the ABC Test, and correct any misclassifications immediately.

Your claims history directly affects your premiums, so implementing safety programs now reduces both injury frequency and future costs. Training employees on hazard recognition, conducting regular site inspections, and maintaining transparent reporting of near-misses prevent injuries before they drain your coverage limits. These investments lower your premiums over time while protecting your crew.

We at Evaristo Insurance specialize in contractor coverage across Connecticut and understand the specific risks your business faces. Contact us for a free coverage review-we’ll analyze your current policy, verify your worker classifications, and recommend adjustments that protect your business without overpaying for coverage you don’t need. Proper contractor workers comp CT coverage is not optional; it’s the foundation of a sustainable business.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!