Landlord Policy CT Guide: Navigate Coverage with Confidence

Owning rental property in Connecticut comes with real financial exposure. Between tenant disputes, property damage, and liability claims, landlords face risks that standard homeowners policies simply don’t cover.

We at Evaristo Insurance have helped hundreds of Connecticut property owners understand what a landlord policy actually protects-and more importantly, what it doesn’t. This guide walks you through the coverage types you need, the gaps you should watch for, and how to build a protection strategy that matches your investment.

What a Landlord Policy Actually Covers

How Landlord Policies Differ from Homeowners Coverage

A landlord policy is built specifically for property owners who rent out residential units, and it protects against risks that a standard homeowners insurance policy completely ignores. The core difference matters enormously: homeowners policies cover owner-occupied homes, while landlord policies account for tenant-related exposures like liability from guest injuries, loss of rental income when a property becomes uninhabitable, and damage caused by non-owner occupants. If you use a homeowners policy on a rental property, claims get denied because the policy explicitly excludes rental occupancy. This gap costs money when you need coverage most.

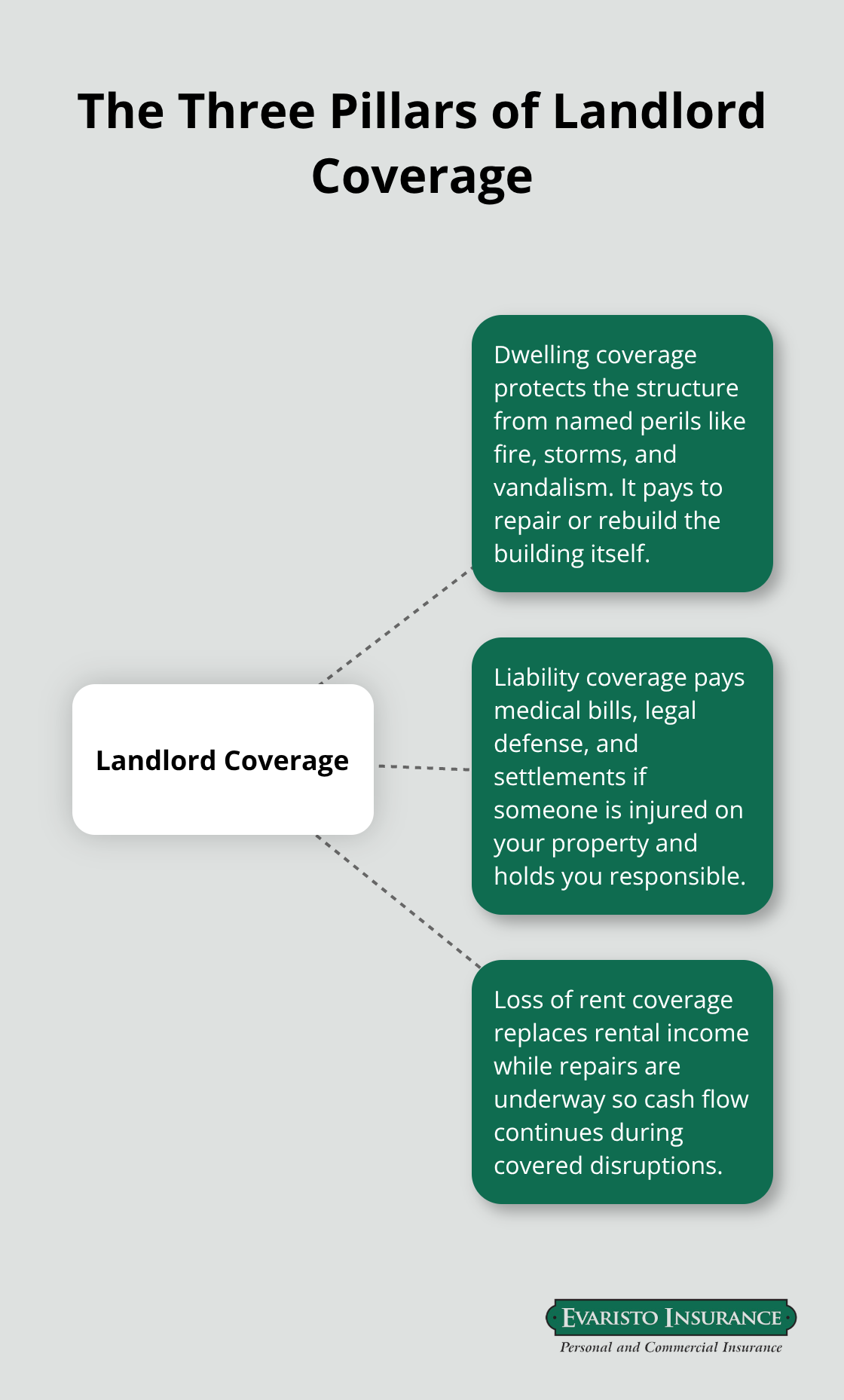

The Three Pillars of Landlord Coverage

Dwelling coverage protects the structure itself against fire, storms, vandalism, and other named perils. Liability coverage handles medical bills and legal fees if someone is injured on your property and sues. Loss of rent coverage replaces your monthly income while repairs are underway-a financial lifeline that prevents you from defaulting on your mortgage while the property sits damaged.

Why Connecticut’s Market Demands Proper Coverage

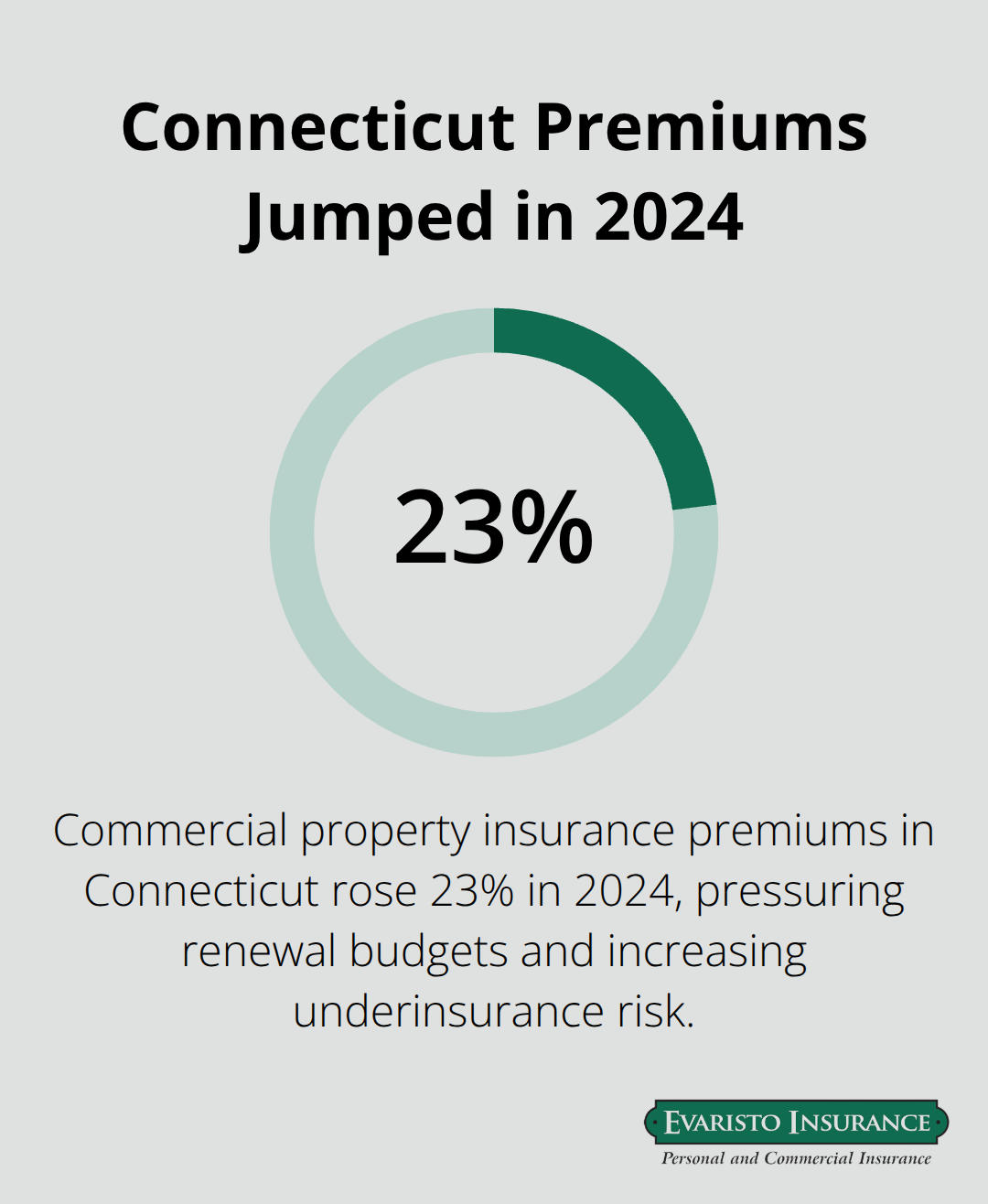

Connecticut’s rental market is projected to reach nearly $1.1 billion by 2025 according to IBISWorld data, which reflects the scale of property investment across the state and the corresponding financial exposure landlords face. Connecticut has no statewide rent control, so your rental income depends entirely on market conditions and uninterrupted occupancy-which is why loss of rent coverage is non-negotiable. Commercial property insurance premiums in Connecticut rose approximately 23 percent in 2024, ranking the state tenth nationwide for increases according to market analysis, which means renewal costs are climbing and underinsurance becomes more financially dangerous.

Real Liability Exposure You Face

The liability exposure is real: a guest slips on ice, a tenant’s visitor falls down stairs, water damage from your negligent maintenance spreads to an adjacent unit. Without proper liability limits, a single incident can exceed fifty thousand dollars in medical bills and legal defense costs. Connecticut law requires landlords to maintain habitable units and make repairs within fifteen days of written notice-failure to do so exposes you to tenant withholding of rent, repair-and-deduct claims, and premises liability lawsuits.

The Cost of Proper Protection

A standard landlord policy typically costs fifteen to twenty-five percent more than homeowners coverage because the risk profile is fundamentally different. Most lenders do require coverage for financed rental properties, yet they don’t verify that coverage actually matches your exposure. The investment in proper coverage is far cheaper than defending a claim without it or rebuilding after a loss with personal funds. Understanding what specific coverage types actually protect your property and income is the next step toward building a strategy that matches your actual exposure.

Essential Coverage Types for Connecticut Rental Properties

Dwelling Coverage: Protecting Your Building’s Replacement Value

Dwelling coverage forms the foundation of any landlord policy and protects the physical structure of your rental property against fire, storms, vandalism, and other named perils. This coverage pays to repair or rebuild the building itself, but the specific dollar amount matters enormously. Connecticut properties vary widely in construction cost depending on location, age, and materials-a three-bedroom home in Hartford costs far less to rebuild than an equivalent property in Fairfield County. Set your dwelling limit based on the actual replacement cost of the structure, not the market value of the land or the purchase price you paid years ago. Underestimating this limit leaves you personally responsible for reconstruction costs that exceed your coverage, which defeats the entire purpose of insurance. Most Connecticut landlords should review dwelling limits every two to three years as construction costs shift, and Connecticut’s 23 percent commercial property insurance premium increase in 2024 reflects broader inflation in repair and materials costs that directly affects rebuilding expenses.

Liability Coverage: Defending Against Injury Claims

Liability coverage is where most Connecticut landlords carry dangerously low limits. This coverage pays for medical bills, legal defense, and settlements when someone is injured on your property and holds you responsible. A guest slips on stairs, a tenant’s visitor falls on an icy walkway, or water damage from your deferred maintenance spreads to an adjacent unit-each scenario creates genuine liability exposure. Connecticut law requires landlords to maintain habitable units and complete repairs within 15 days of written notice, which means negligence claims arise directly from failure to meet these legal obligations. A single serious injury claim easily exceeds $100,000 in medical costs and legal fees, yet many landlords carry liability limits ranging from $100,000 to $1,000,000. Try minimum liability limits of $300,000 per occurrence for single-family rentals and $500,000 or higher for multi-unit properties or properties in high-traffic areas. Consider an umbrella policy that adds an additional $1,000,000 in liability protection at a relatively modest cost (typically $150 to $300 annually) because one catastrophic injury claim can financially devastate a property owner without adequate limits.

Loss of Rent Coverage: Maintaining Cash Flow During Repairs

Loss of rent coverage directly replaces your monthly rental income while your property is uninhabitable due to a covered loss like fire or storm damage. This coverage is non-negotiable in Connecticut because your mortgage lender still expects payment, property taxes do not stop accruing, and you cannot evict tenants for temporary uninhabitability caused by insured damage. Specify the waiting period carefully-typically 14 to 30 days-because coverage does not begin until that period expires, and align the benefit period with realistic repair timelines for your property type. A kitchen fire in a single-family home might require 30 to 60 days of repairs, while water damage in an older building could extend to 90 days or longer. Connecticut’s rental market relies on consistent occupancy to generate the income that supports your investment, which is why loss of rent coverage stabilizes your cash flow when damage threatens that income. Set monthly benefit limits that match your actual rent collection amount, and verify the total benefit cap covers your expected repair duration-choosing a $3,000 monthly limit with a 90-day cap provides $9,000 total protection, which may fall short if repairs extend longer or your rent exceeds that monthly amount. Document your actual monthly rent in your policy file so underwriters understand your coverage needs during renewal.

The specific limits you select for each coverage type determine whether your policy actually protects your investment or leaves gaps that expose you to personal liability. Your next step is identifying the coverage gaps that most Connecticut landlords overlook-the exclusions and limitations that create financial exposure even when you carry a landlord policy.

What Your Landlord Policy Actually Leaves Unprotected

Tenant Belongings Fall Outside Your Coverage

Your landlord policy protects the building structure and covers your liability exposure, but it creates three critical blind spots that catch Connecticut landlords off guard during claims. The first misconception is that your policy covers tenant belongings. It does not. Your policy covers the dwelling and your liability, but a tenant’s furniture, electronics, clothing, and personal property sit entirely outside your coverage. When a fire destroys the rental unit, your dwelling coverage rebuilds the structure, but the tenant’s belongings remain their responsibility. Connecticut tenants should carry renters insurance to protect their possessions, yet many do not. You can address this gap by including language in your lease requiring tenants to obtain renters insurance, though you cannot mandate it legally. The practical approach is to educate tenants during move-in about this coverage gap and recommend they purchase a policy.

Vacancy Periods Create Coverage Restrictions

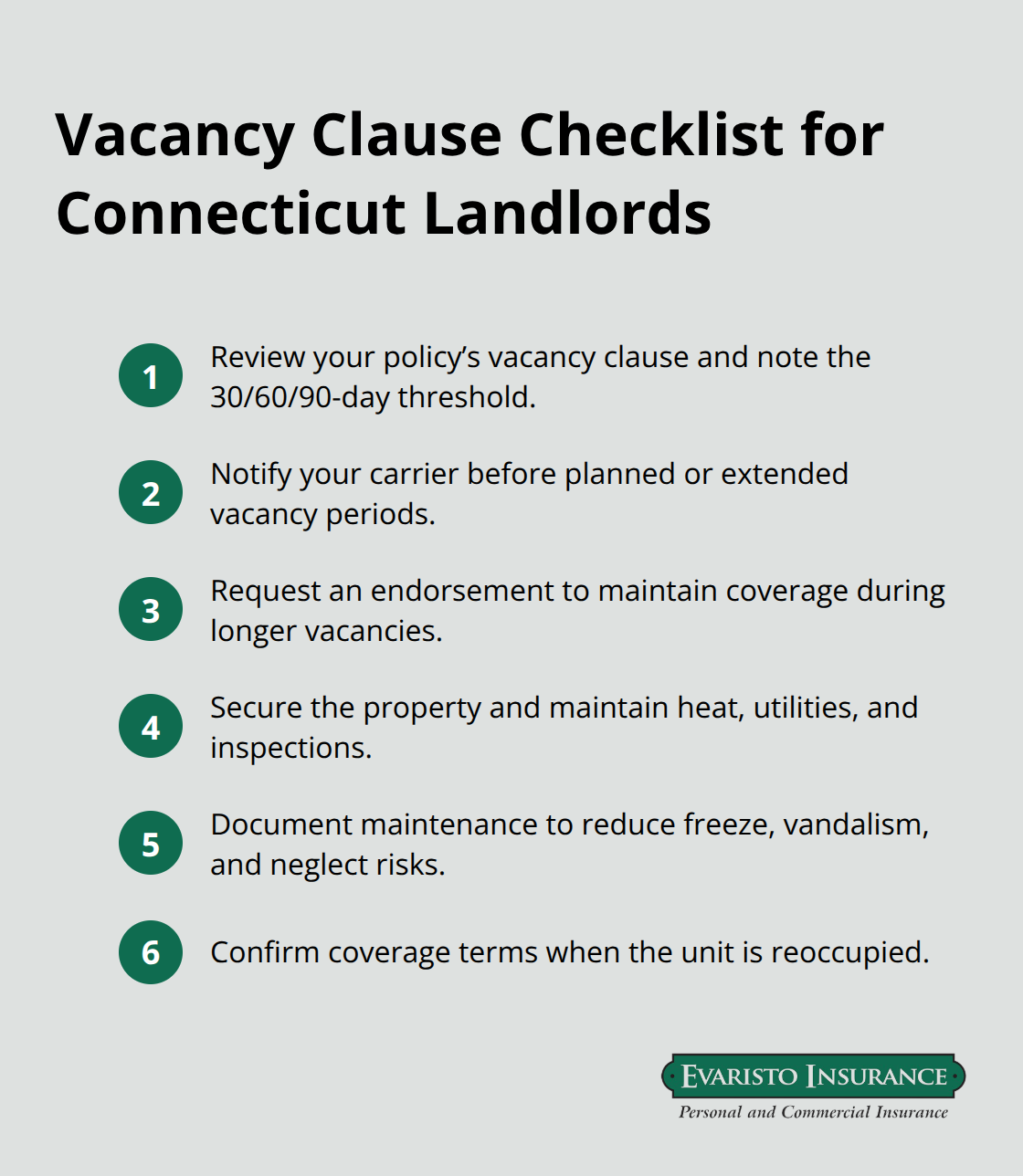

The second gap emerges during vacancy periods. Most landlord policies exclude or severely limit coverage while a property sits unoccupied for 30, 60, or 90 consecutive days depending on your policy language. Connecticut’s rental market dynamics mean properties sometimes remain vacant between tenants, during renovations, or while you search for qualified applicants. An unoccupied building presents different risk exposure to insurers: pipes freeze more easily, maintenance gets deferred, and vandalism occurs more frequently when no one is present. Check your policy’s vacancy clause carefully and notify your carrier before intentional vacancy periods begin. Some carriers require permission or impose temporary coverage restrictions.

If you anticipate extended vacancy, request an endorsement that maintains coverage or explicitly confirm the vacancy period your policy allows.

Maintenance Negligence Claims Face Denial

The third and most expensive gap involves maintenance and negligence claims. Connecticut law requires landlords to maintain habitable units and complete repairs within 15 days of written notice. A failure to fix a known water leak, a delayed roof repair, or negligent maintenance of stairs creates direct liability exposure that your policy may not cover if the claim hinges on your negligence rather than an unexpected accident. Insurance covers sudden, accidental losses, not losses caused by your failure to maintain the property. A tenant slips on icy stairs during a snowstorm and your liability coverage responds. A tenant slips on the same stairs because you ignored a broken step for months and your coverage likely denies the claim based on maintenance negligence.

Document Repairs to Protect Your Coverage

The solution is straightforward: maintain detailed service records for every repair, follow through on tenant maintenance requests within Connecticut’s legal requirement, and photograph completed repairs. Document your responsiveness to keep claims clearly separated from negligence exposure. Carriers now expect proof that you responded promptly to maintenance issues and kept the property in compliant condition. Create a repair request log, assign completion dates, photograph work when finished, and file receipts in a dedicated folder. This documentation directly protects your coverage by demonstrating you acted responsibly rather than negligently when damage occurs.

Final Thoughts

A landlord policy in Connecticut protects your rental income, your building, and your personal assets from the financial damage that a single incident can cause. Dwelling protection rebuilds your structure, liability coverage defends against injury claims, and loss of rent keeps your cash flow stable during repairs. Connecticut’s 23 percent premium increase in 2024 and the state’s projected $1.1 billion rental market reflect the scale of property investment and the corresponding financial exposure you carry.

Set your dwelling limit based on actual replacement cost, not purchase price, and carry liability limits of at least $300,000 for single-family rentals and $500,000 or higher for multi-unit properties. Specify loss of rent coverage that matches your actual monthly rent and realistic repair timelines. Document every repair request and completion to protect yourself against negligence claims, and review your policy annually as construction costs shift and your property exposure changes.

We at Evaristo Insurance have guided Connecticut property owners through this landlord policy CT guide process since 1989. As a second-generation, family-owned independent agency, we compare multiple top carriers to deliver tailored protection and competitive pricing that matches your actual exposure rather than generic templates. Contact Evaristo Insurance to review your current coverage and build a landlord policy strategy that protects your investment with confidence.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!