Connecticut Landlord Insurance: Protecting Your Rental Portfolio

Owning rental properties in Connecticut comes with real financial exposure. Tenant injuries, property damage, and lost rental income can quickly drain your profits if you’re not properly protected.

Standard homeowners insurance won’t cover your rental units, which leaves many Connecticut landlords dangerously underinsured. We at Evaristo Insurance have helped countless property owners in Connecticut understand what Connecticut landlord insurance actually covers and where the gaps typically hide.

What Connecticut Rental Properties Actually Need to Survive

Connecticut’s rental market sits on specific vulnerabilities that most landlords overlook until damage occurs. Properties in older neighborhoods face higher theft and vandalism risk, while coastal and elevated areas deal with water damage from nor’easters and spring flooding. Urban rentals in Hartford and Bridgeport experience elevated liability claims from slip-and-fall injuries and tenant disputes. According to the U.S. Census Bureau, roughly 34% of Connecticut’s 3.6 million residents occupy rental housing, meaning landlords operate in a competitive, high-density market where one uninsured loss wipes out months of profit. The state’s freeze-thaw cycles accelerate pipe damage and foundation settling, creating repair costs that spike quickly if left unaddressed.

Connecticut landlords who treat insurance as a checkbox rather than a strategic protection layer face coverage gaps that cost thousands when claims arise.

Standard Homeowners Policies Leave You Exposed

Your homeowners insurance explicitly excludes rental income and tenant-related liability because you no longer occupy the property as your primary residence. If a tenant’s guest slips on your stairs or a tenant causes accidental damage to the building structure, your homeowners policy denies the claim outright. Lenders financing rental properties refuse to accept homeowners policies, requiring landlord-specific coverage as a loan condition. The DP-3 form-the most comprehensive property form for Connecticut landlords-covers replacement cost value for most perils except flood and earthquake, whereas homeowners policies operate under owner-occupancy assumptions. Travelers, Progressive, Safeco, and other major carriers offer landlord-specific policies that address tenant turnover, loss of rental income during repairs, and the liability exposure unique to renting. Many Connecticut landlords don’t realize their existing homeowners policy leaves them completely exposed until a claim gets rejected.

Full Replacement Cost Protects Your Bottom Line

Connecticut landlords must insure their properties for full replacement cost, not just the mortgage balance. Under-insuring by even 20% triggers coinsurance penalties that reduce your claim payout proportionally-a $50,000 water damage claim might pay only $40,000 if you’re under-insured. Loss of rent coverage reimburses your rental income during repairs after a covered loss, typically costing around $1 per $1,000 of annual rent (a small premium that protects your cash flow during the weeks or months a property sits uninhabitable). Connecticut properties in flood zones require separate flood insurance through the National Flood Insurance Program, which standard landlord policies exclude entirely.

Building Code Upgrades Add Hidden Value

Older homes and multi-unit buildings benefit from building code endorsements that cover the cost of upgrading systems to current code during repairs. A single claim without this protection can add tens of thousands in unexpected costs. These endorsements address the gap between what your policy covers and what local building codes now require, turning a manageable claim into a financial crisis if overlooked. Understanding these layers of protection separates landlords who maintain steady cash flow from those who face unexpected out-of-pocket expenses after damage occurs.

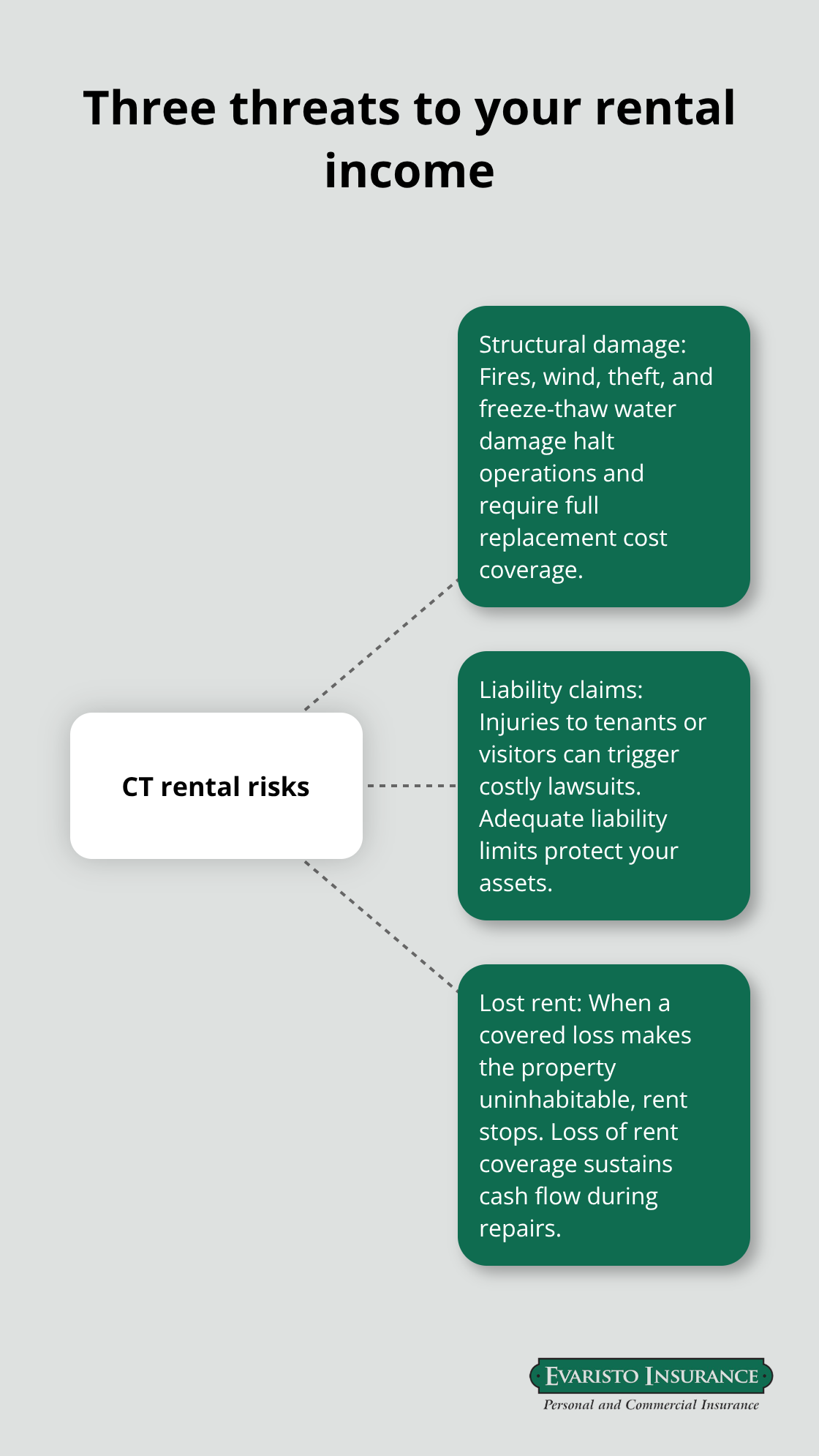

The Three Coverages That Protect Your Connecticut Rental Income

Your rental property faces three distinct financial threats: structural damage that halts operations, liability claims from people injured on your property, and lost rent when the building becomes uninhabitable. Connecticut landlord insurance addresses each threat separately, and skipping any one of them exposes your entire investment to catastrophic loss.

Building Coverage Pays for Structural Repairs

Building coverage pays to repair or rebuild the structure itself after fire, wind, theft, or other covered perils, calculated at full replacement cost rather than what you owe on the mortgage. Connecticut’s older housing stock means many rental properties have outdated plumbing and electrical systems prone to freeze-thaw damage and water intrusion, making accurate replacement cost valuations essential. A burst pipe in January creates water damage that requires weeks of drying, remediation, and repairs before a tenant can move back in. Your insurance covers the structural repairs, but only loss of rent coverage replaces the income you lose during that vacancy period. Under-insuring by even 20% triggers coinsurance penalties that reduce your claim payout proportionally-a $50,000 water damage claim might pay only $40,000 if you’re under-insured.

Liability Coverage Protects Against Injury Claims

Liability coverage protects you when a tenant’s guest slips on icy steps or a visitor claims the property caused them injury, with Connecticut landlords typically carrying $100,000 to $1,000,000 per occurrence depending on property size and risk profile. Liability exposure intensifies with multi-unit properties and frequent tenant turnover, where more people move through the building annually and slip-and-fall claims increase proportionally. Medical payments coverage, included with most Connecticut landlord policies at $1,000 when liability is purchased, covers immediate treatment for injuries on your property regardless of fault. This small benefit prevents minor injuries from escalating into formal liability claims. Your lender requires you to name them as an Additional Insured on the policy, which means the lender receives the same protection as you during claims, ensuring the mortgage lender’s security interest stays intact even after damage occurs.

Loss of Rent Coverage Replaces Your Income During Repairs

Loss of rent coverage reimburses your monthly rental income during the weeks or months your property sits uninhabitable after a covered loss. Without this protection, you absorb every dollar of lost rent while still paying the mortgage, property taxes, and maintenance costs. Loss of rent coverage makes it one of the cheapest protections available relative to the income it safeguards. Connecticut’s older housing stock means repairs stretch longer in older homes, making loss of rent coverage especially valuable for protecting your cash flow. Many Connecticut landlords treat these three coverages as optional add-ons rather than foundational requirements, then face financial ruin when a single event triggers all three exposures simultaneously.

Flood Insurance Requires Separate Protection

Connecticut properties in flood zones require separate flood insurance through the National Flood Insurance Program, which standard landlord policies exclude entirely. Building code endorsements cover the cost of upgrading systems to current code during repairs, addressing the gap between what your policy covers and what local building codes now require. A single claim without this protection can add tens of thousands in unexpected costs, turning a manageable claim into a financial crisis if overlooked.

Understanding these layers of protection separates landlords who maintain steady cash flow from those who face unexpected out-of-pocket expenses after damage occurs. The next section examines where most Connecticut landlords discover dangerous gaps in their coverage-and how to identify these blind spots before a loss exposes them.

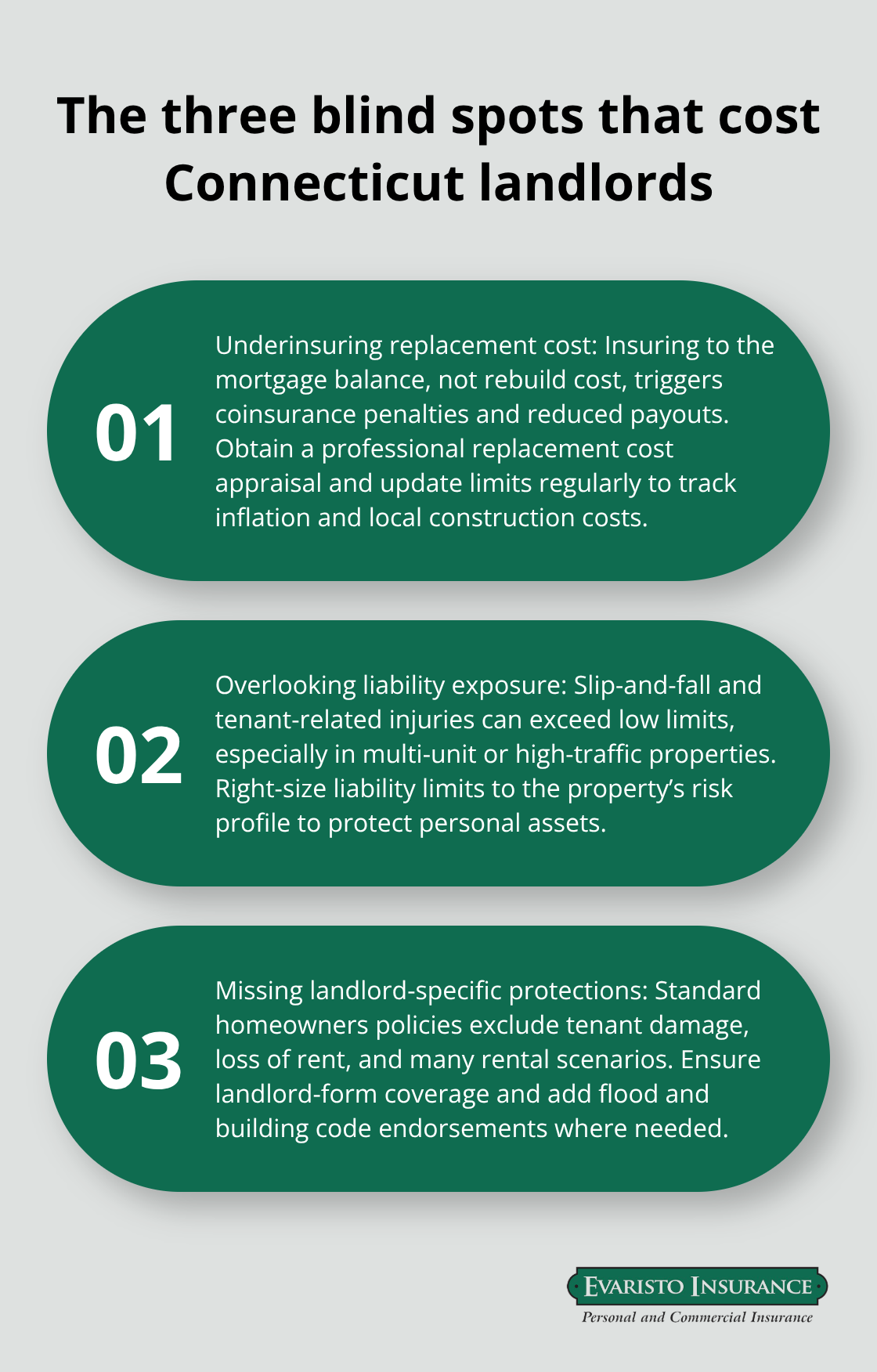

Where Connecticut Landlords Discover Coverage Gaps Too Late

Most Connecticut landlords face three dangerous blind spots that surface only after damage occurs, and by then the financial damage is irreversible.

Underinsuring Properties Based on Replacement Cost

The first gap stems from underinsuring based on what you owe on the mortgage rather than what it actually costs to rebuild. Connecticut’s construction costs run high, especially in older neighborhoods where specialized contractors command premium rates for plumbing and electrical work on pre-1980s homes. If your property would cost $450,000 to fully rebuild but you insure it for only $350,000 to match your mortgage balance, coinsurance penalties kick in immediately. The insurance company calculates your claim payout based on the percentage you’re under-insured, meaning a $100,000 water damage claim pays only $78,000 instead of the full amount.

According to the Connecticut Property Owners Association, many landlords allocate 1-2% of each property’s annual value toward a maintenance reserve, yet fail to increase their insurance limits when replacement costs climb due to inflation or market conditions. You need a professional replacement cost appraisal every three to five years, not a casual estimate based on comparable sales. Connecticut’s freeze-thaw cycles and aging infrastructure mean repair costs accelerate faster than national averages, making outdated valuations particularly dangerous.

Overlooking Liability Exposure from Tenant Activities

The second gap involves liability exposure that escalates with tenant turnover and multi-unit properties. Slip-and-fall injuries from ice, snow, or poorly maintained stairs generate claims regularly across Connecticut’s urban rental markets, yet many landlords carry minimum $100,000 liability limits on properties that justify $500,000 or higher coverage. A single serious injury claim-permanent disability from a fall, for example-can exceed your liability limit and expose your personal assets to judgment.

Properties in Hartford, Bridgeport, and other high-crime areas benefit from higher liability limits and security endorsements that reduce both risk and premiums through documented theft prevention measures. Multi-unit buildings amplify this exposure because more people move through the property annually, increasing slip-and-fall claims proportionally. Your lender requires you to name them as an Additional Insured on the policy, which means the lender receives the same protection as you during claims, ensuring the mortgage lender’s security interest stays intact even after damage occurs.

Missing Coverage for Landlord-Specific Scenarios

The third gap hides in landlord-specific scenarios that standard homeowners policies simply refuse to cover. Tenant damage to the building structure, loss of rent during repairs, and liability for tenant activities on the property fall outside traditional coverage. Many Connecticut landlords also overlook that short-term rental use through platforms like Airbnb or VRBO requires commercial insurance rather than standard landlord policies, creating massive coverage holes if a guest is injured during a stay.

Properties in flood zones require separate flood insurance through the National Flood Insurance Program, which standard landlord policies exclude entirely. Building code endorsements cover the cost of upgrading systems to current code during repairs, addressing the gap between what your policy covers and what local building codes now require. A single claim without this protection can add tens of thousands in unexpected costs, turning a manageable claim into a financial crisis if overlooked. Annual policy reviews with a local agent who understands Connecticut’s specific risks help identify gaps before they cost you thousands.

Final Thoughts

Connecticut landlord insurance protects your rental income, your assets, and your peace of mind when damage or liability claims strike. The coverage gaps we’ve outlined-underinsuring properties, overlooking liability exposure, and missing landlord-specific scenarios-cost Connecticut landlords thousands every year. You now understand what full replacement cost actually means, why loss of rent coverage matters more than most landlords realize, and how flood insurance operates separately from your standard policy.

Pull your current policy and compare it against the three core coverages we’ve discussed (replacement cost valuation, liability limits, and loss of rent protection). Check whether your replacement cost valuation reflects current Connecticut construction costs, verify your liability limits match your property’s actual risk profile, and confirm you have loss of rent protection in place. If you’re unsure whether your policy covers tenant damage, short-term rental use, or building code upgrades, that uncertainty signals a gap worth addressing immediately.

We at Evaristo Insurance have guided Connecticut landlords through this exact process since 1989, and our team understands Connecticut’s specific risks because we live and work in these communities. Contact Evaristo Insurance to review your current coverage, identify gaps, and receive competitive quotes from carriers that understand Connecticut’s rental market. Your rental income is too valuable to leave unprotected.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!