Connecticut Homeowners Insurance Quotes: How to Compare Policies

Shopping for Connecticut homeowners insurance quotes shouldn’t mean spending hours comparing policies alone. We at Evaristo Insurance know that understanding your coverage options and finding the right price takes real guidance.

This guide walks you through the exact steps to compare policies side by side, spot the discounts that actually matter, and avoid overpaying for coverage you don’t need.

What Your Connecticut Homeowners Policy Actually Covers

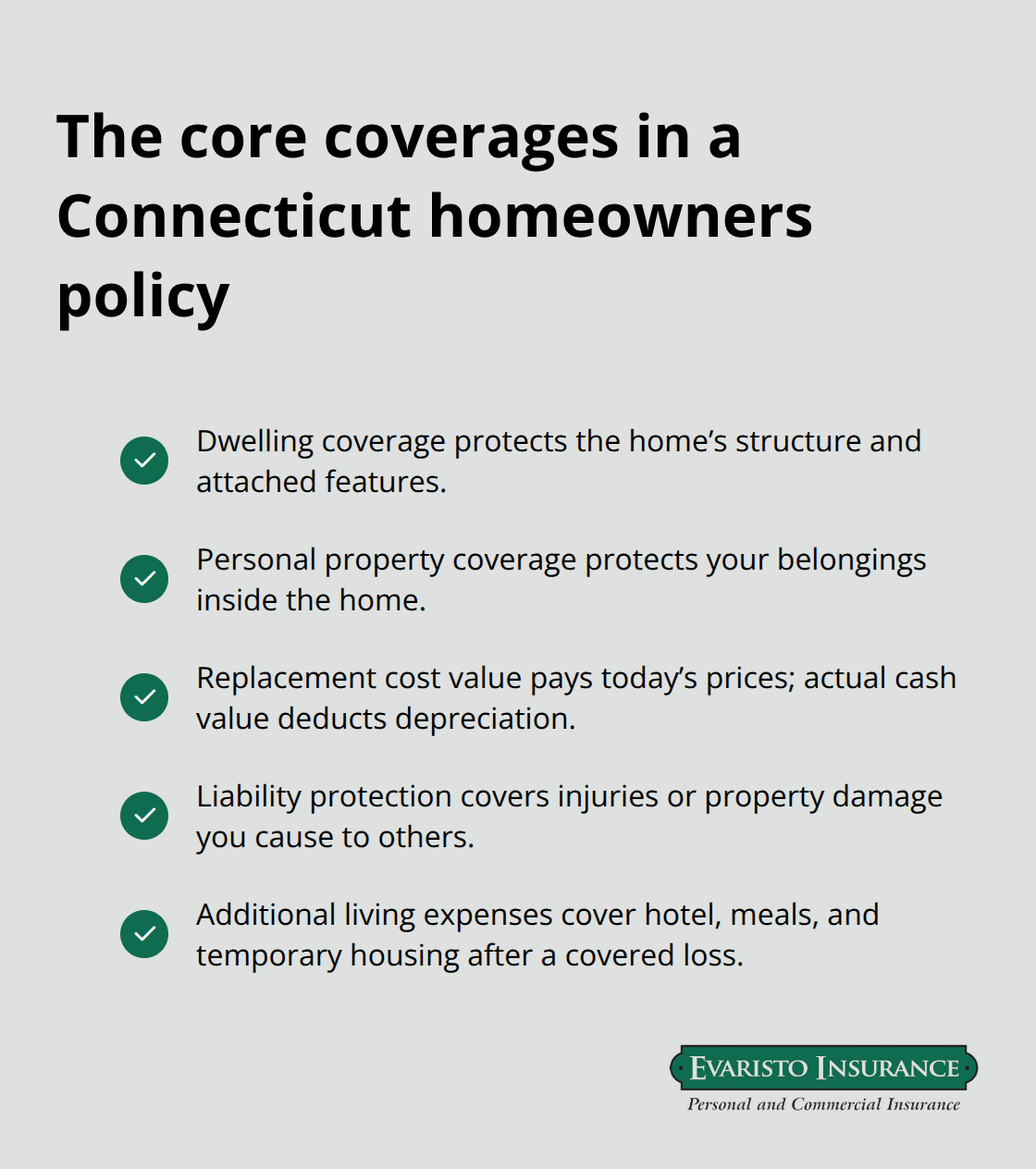

A Connecticut homeowners policy consists of six distinct coverage types, and understanding each one matters because they directly affect your premium and your protection. Dwelling coverage protects your home’s structure itself-the walls, roof, foundation, and attached items like built-in cabinets. According to Bankrate’s analysis, the average Connecticut homeowner carries $300,000 in dwelling coverage, which reflects the median home replacement cost in the state. Personal property coverage typically sits between 50 and 70 percent of your dwelling limit and covers your belongings inside the home: furniture, electronics, clothing, kitchen appliances. This coverage pays on either replacement cost value, which reimburses you at today’s prices, or actual cash value, which deducts depreciation. Replacement cost value yields higher premiums but protects you better when you actually need to replace items. Liability protection covers injuries or property damage you cause to someone else and typically ranges from $100,000 to $500,000 in coverage limits. Additional living expenses cover your hotel, meals, and temporary housing if your home becomes uninhabitable after a covered loss. The data matters here: Bankrate found that Connecticut homeowners pay roughly $1,700 annually for $300,000 in dwelling coverage, which sits about 30 percent below the national average of $2,424, so your baseline cost for solid coverage is genuinely affordable.

Dwelling Coverage Needs in Connecticut

Your dwelling coverage amount should reflect your actual rebuilding cost, not your home’s market value. A home worth $400,000 might cost $250,000 to rebuild because land value doesn’t factor into reconstruction. Most Connecticut homeowners underestimate this figure. The Connecticut Insurance Department identifies home age, construction materials, and roof condition as major premium drivers, which means older homes or those with aging roofing require higher dwelling limits and cost more to insure. If you own a 40-year-old home with an original roof, you’ll pay roughly 20 to 30 percent more than a newer home with similar square footage. Replacement cost endorsements for personal property cost extra but eliminate the depreciation penalty and make claims settlements substantially faster.

Deductible Strategy and Real Savings

Deductible selection directly controls your monthly expense. The Zebra’s Connecticut data shows that moving from a $500 deductible to $1,000 drops your annual premium by roughly $171, while jumping to $2,000 saves about $329 per year. Your deductible choice should reflect what you can actually pay out of pocket if a loss occurs. Higher deductibles make sense only if you have emergency savings to cover them. Connecticut coastal and flood-prone properties need separate flood insurance through FEMA’s National Flood Insurance Program since standard policies exclude flood damage entirely. Standard policies also exclude sewer backup and water damage from ground seepage, so ask your agent about adding water backup endorsements if your neighborhood experiences basement flooding.

Coverage Gaps That Matter in Connecticut

Flood damage represents the most significant gap in standard homeowners policies. FEMA’s National Flood Insurance Program provides up to $250,000 for home structure and $100,000 for personal property, though private insurers may offer higher limits in some case. Sewer backup and sump pump failures also fall outside standard coverage, leaving Connecticut homeowners vulnerable during heavy rain events. Water backup endorsements cost relatively little but protect you substantially when basement flooding occurs. Coastal properties face additional hurricane deductibles (typically 2 to 5 percent of property value) that activate when official hurricane warnings are issued. Understanding these exclusions now prevents expensive surprises later when you file a claim.

Next Steps for Comparing Your Options

With a clear picture of what your policy covers and what gaps exist, you’re ready to gather actual quotes and see how different carriers price these protections. The comparison process reveals significant variations in how insurers value your home and assess your risk.

What Really Drives Your Connecticut Insurance Quote

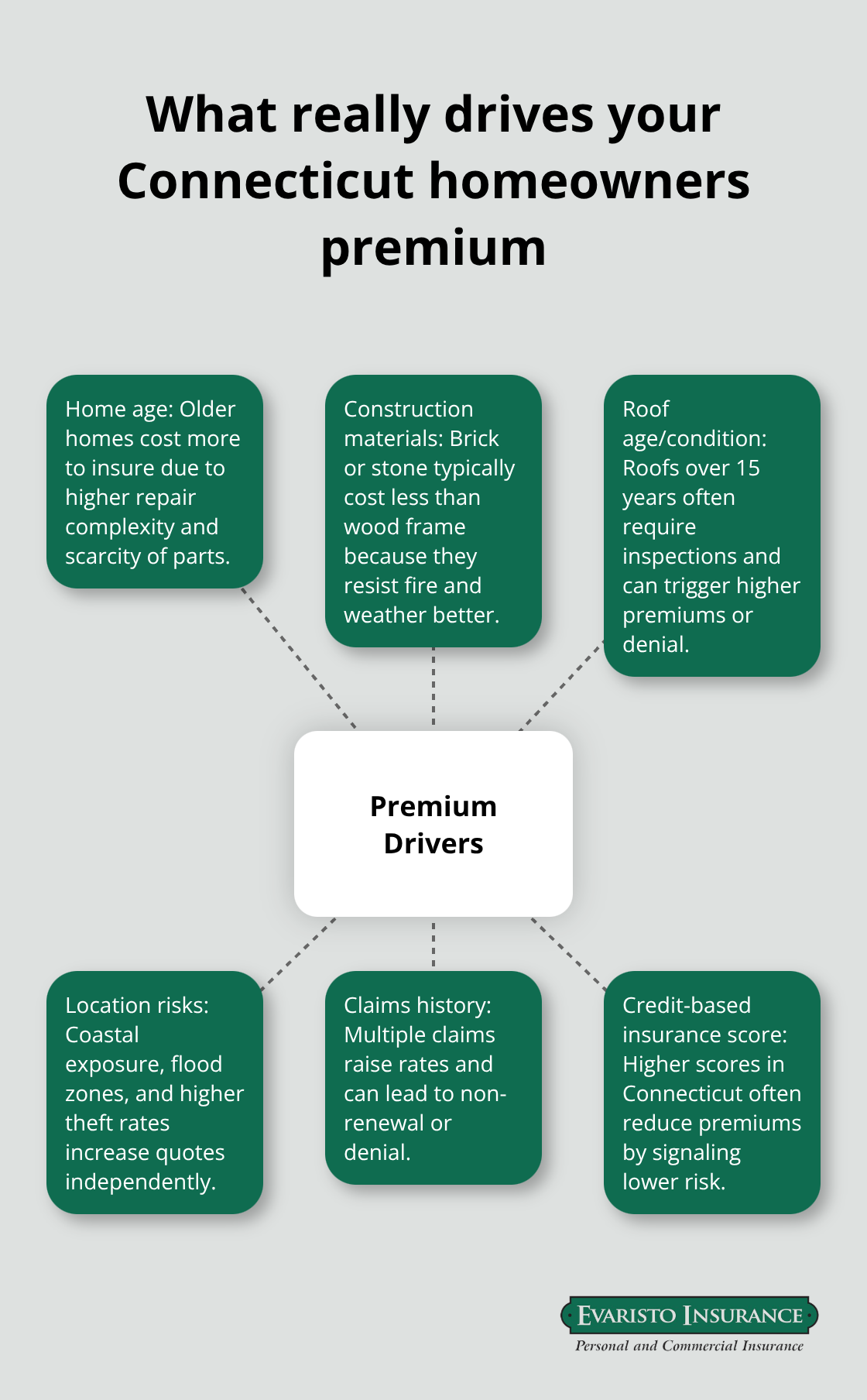

Your dwelling coverage amount, deductible choice, and policy exclusions matter far less to your final premium than the underlying risk factors insurers assess. The Connecticut Insurance Department identifies home age, construction materials, and roof condition as the primary drivers of your quote, which means these three factors alone can swing your annual premium by hundreds of dollars. A home built in 1985 with original wiring and an aging asphalt roof costs significantly more to insure than a 2015 home with updated electrical systems and a newer roof, even if both have identical square footage and location. Insurers charge more for older homes because repair costs climb with age, replacement parts become scarce, and structural issues emerge more frequently. Construction materials matter equally: brick or stone exteriors typically cost less to insure than wood frame construction because they resist fire and weather damage better.

The Connecticut Insurance Department also flags roof age as a standalone premium factor, which is why many insurers now require roof inspections for homes with roofs over 15 years old. If your roof exceeds 20 years, expect either higher premiums or outright coverage denial from some carriers. Updating your roof, upgrading to modern wiring, or installing a new HVAC system reduces your premium because these improvements lower the insurer’s actual loss exposure.

Where You Live Shapes Your Cost More Than You Think

Your specific location within Connecticut determines your homeowners insurance cost, according to Bankrate’s city-by-city analysis. Coastal proximity, flood risk, hurricane exposure, and local theft rates all influence your quote separately. New Haven, Bridgeport, and other coastal or historically urban areas sit well above the state average, while inland towns like Staffordville sit substantially below it. Properties within one mile of a fire station receive lower quotes because response times directly correlate with claim severity. Conversely, homes in neighborhoods with higher theft rates automatically receive higher liability and personal property premiums. Hurricane risk affects coastal Connecticut properties through separate hurricane deductibles that typically run 2 to 5 percent of your home’s insured value, meaning a $300,000 home could face a $6,000 to $15,000 deductible if a hurricane causes damage. Flood zone designation drives the largest cost increase of all: even if your lender doesn’t mandate separate flood insurance, living in a high-risk flood zone will increase your standard homeowners quote by 15 to 25 percent because the insurer factors in elevated water damage probability. Your ZIP code matters enough that moving three miles can change your annual premium by several hundred dollars.

Claims History and Credit Scores Control Your Long-Term Costs

Your previous insurance claims history directly impacts your renewal premium far more than most homeowners realize. Filing even a single claim increases your renewal rate, which is why careful evaluation of whether to file small claims is important because the premium increase often outweighs the benefit over three to five years. Two claims in five years can increase your rate by 25 to 40 percent, while three claims in five years may result in non-renewal or coverage denial from some carriers. Your credit score also influences your premium in Connecticut because insurers use credit-based insurance scores to assess risk. Lower credit scores correlate with higher claim frequency in insurer databases, so maintaining a credit score above 700 typically saves you 10 to 15 percent on your annual premium. Non-smokers receive lower quotes than smokers because smoking increases fire risk, and marital status also factors into pricing because married homeowners historically file fewer claims. These behavioral and financial factors often account for 20 to 30 percent of your total premium, which means improving your credit score or maintaining a clean claims history delivers better value than shopping for a lower deductible alone. Some Connecticut carriers reward claim-free years with discounts that accumulate over time, so staying with one insurer can become increasingly affordable if you avoid losses.

How Protective Devices Lower Your Premium

Installing burglar alarms, smoke detectors, fire extinguishers, sprinkler systems, and deadbolt locks all reduce your annual premium because these devices lower the insurer’s loss exposure. A home with a monitored burglar alarm system typically qualifies for a 5 to 15 percent discount, while smoke detectors and deadbolts offer smaller but meaningful reductions. Sprinkler systems provide the largest discount among protective devices, sometimes reaching 15 to 20 percent, because they dramatically reduce fire damage severity. These upgrades pay for themselves within a few years through premium savings alone, making them smart investments beyond the safety benefits they provide. The Connecticut Insurance Department recognizes these devices as legitimate risk reducers, which is why insurers consistently offer discounts for their installation.

With a clear understanding of what drives your quote, you’re ready to gather actual quotes from multiple carriers and see how different insurers price your specific risk profile.

How to Compare Connecticut Homeowners Insurance Quotes

Request Quotes with Identical Coverage Specifications

Gathering quotes from multiple carriers reveals why shopping matters in Connecticut. The Zebra’s data shows average annual premiums ranging from $927 with MetLife to $1,130 with Merrimack Mutual, a difference of $203 per year for identical coverage. That gap widens dramatically when you adjust coverage amounts: a homeowner selecting $100,000 in dwelling coverage pays roughly $624 annually, while $400,000 in dwelling coverage costs about $1,806 per year. Request quotes from at least three carriers using identical coverage specifications: same dwelling limit, same deductible, same liability limit, same personal property coverage basis (replacement cost or actual cash value). Most insurers allow online quote requests where you enter your home’s age, construction materials, roof age, and desired coverage levels within minutes. Bankrate’s research identified USAA, Amica, State Farm, Travelers, and Farmers as top Connecticut options, though USAA eligibility requires military service or family connection.

When you request quotes, verify that each insurer quotes the same policy type because some carriers offer multiple tiers with different coverage options and endorsement availability. A policy that includes water backup coverage for $50 annually looks cheaper until you realize it excludes sewer backup entirely, making the cheaper quote worthless for your actual risk profile. Document each quote with the carrier name, dwelling coverage amount, personal property limit, liability limit, deductible, and any included or excluded endorsements. This creates an apples-to-apples comparison sheet that prevents confusion when you’re deciding between five different quotes.

Test Multiple Deductible Scenarios

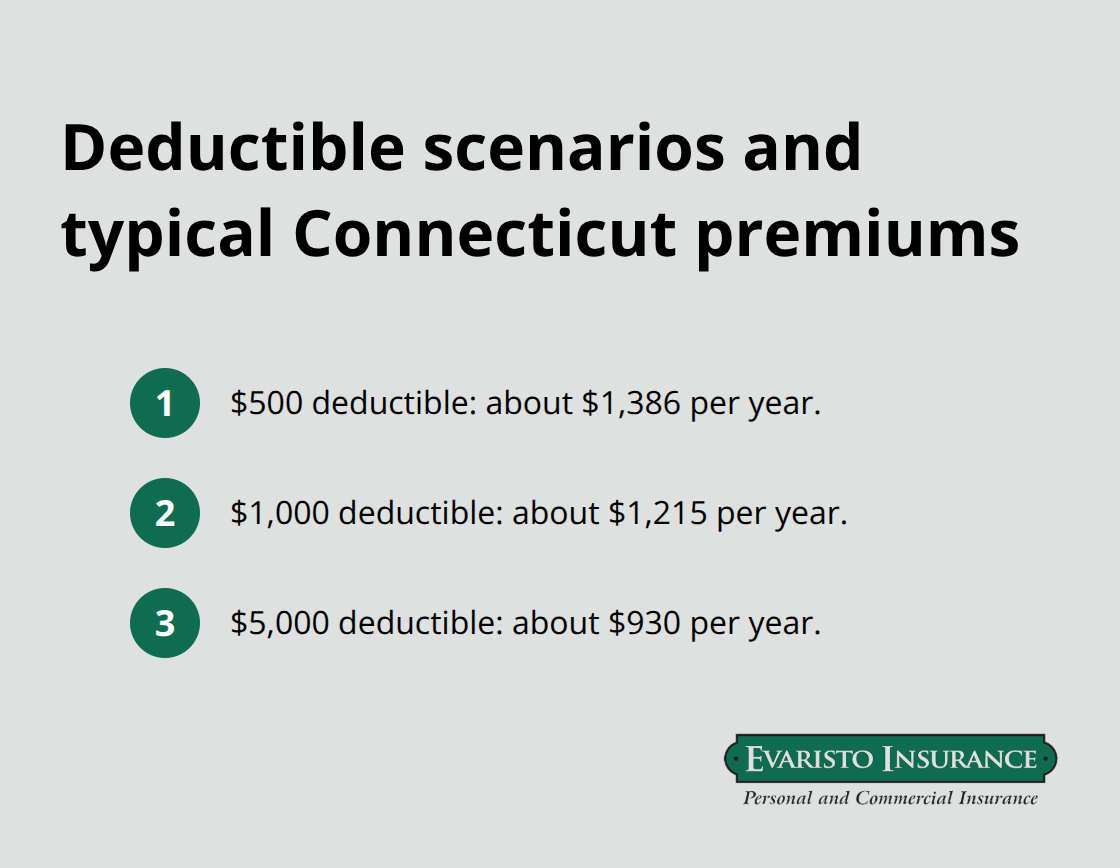

Deductible selection swings your annual cost more than almost any other factor, so test multiple deductible scenarios within each quote. The Zebra found that Connecticut homeowners pay approximately $1,386 annually with a $500 deductible, $1,215 with a $1,000 deductible, and $930 with a $5,000 deductible. That $456 annual difference between $500 and $5,000 deductibles represents real money, but only if you can actually afford the higher deductible when a loss occurs. Most Connecticut homeowners should carry no higher than a $1,000 deductible because it balances premium savings against realistic out-of-pocket capacity.

Identify Bundling Discounts and Safety Device Savings

Beyond coverage and deductibles, bundling home and auto insurance can lead to savings of up to 25%, according to Experian. Ask each carrier what bundling discounts they offer and whether those discounts apply automatically or require explicit request. Some insurers also offer claim-free discounts that accumulate over time, new home discounts for recently constructed properties, and safety device discounts for burglar alarms or sprinkler systems.

Request a complete discount list from each carrier because many homeowners miss savings worth $200 to $400 annually simply by not asking. Verify the discount percentages apply to your specific situation rather than assuming generic descriptions. A new home discount might apply only to homes built within the past two years, while a claim-free discount might require five years without losses. Read the fine print or ask your agent directly what discounts actually apply to your profile, then calculate your true out-of-pocket cost after all discounts before making a final decision.

Calculate Your True Out-of-Pocket Cost

The lowest quote doesn’t always deliver the best value once you factor in coverage gaps and discount eligibility. A carrier offering $50 less annually but excluding water backup coverage leaves you exposed to a $10,000 basement flooding loss. Conversely, a carrier charging $100 more annually but including sewer backup coverage and offering a 15 percent bundling discount might deliver superior protection at lower net cost. Create a final comparison table that lists each carrier’s annual premium, all applicable discounts, resulting net cost, and coverage differences (especially endorsements for water backup, sewer backup, or flood insurance). This approach reveals which carrier actually delivers the best protection at the best price for your specific situation rather than simply selecting the lowest number.

Final Thoughts

Comparing Connecticut homeowners insurance quotes effectively requires you to request identical coverage specifications across multiple carriers, test different deductible scenarios to find your actual out-of-pocket comfort level, and calculate your true net cost after discounts rather than fixating on the lowest premium alone. The difference between a well-researched decision and a rushed one often amounts to several hundred dollars annually, plus the confidence that your coverage actually matches your home’s real risks. Connecticut homeowners who skip this comparison process typically overpay by 15 to 25 percent while carrying gaps in protection that leave them exposed to significant losses.

A local Connecticut agent transforms this process from a solitary research project into a partnership with someone who understands your specific situation and your state’s unique insurance landscape. Your agent knows which carriers offer the best rates in your ZIP code, which endorsements matter most for Connecticut’s flood and hurricane risks, and how to navigate the gap between what standard policies cover and what actually protects your home. They also handle the administrative details that most homeowners find tedious: requesting quotes, comparing specifications, and ensuring your policy documents arrive correctly before closing.

Gather Connecticut homeowners insurance quotes from at least three carriers using identical coverage amounts and deductibles, then contact a local agent to review your options and identify any coverage gaps you might have missed. This combination of independent research and professional guidance delivers the best quotes at the best prices with confidence that your protection covers your home’s real risks.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!