Ellington CT Landlord Insurance: Local Coverage You Can Trust

Owning rental property in Ellington comes with real financial exposure. Standard homeowners policies won’t protect your investment, and Connecticut’s landlord laws create specific obligations you need to understand.

We at Evaristo Insurance help local landlords get the right coverage for their properties. This guide walks you through what Ellington CT landlord insurance actually covers and why it matters for your rental business.

What Your Landlord Policy Actually Protects

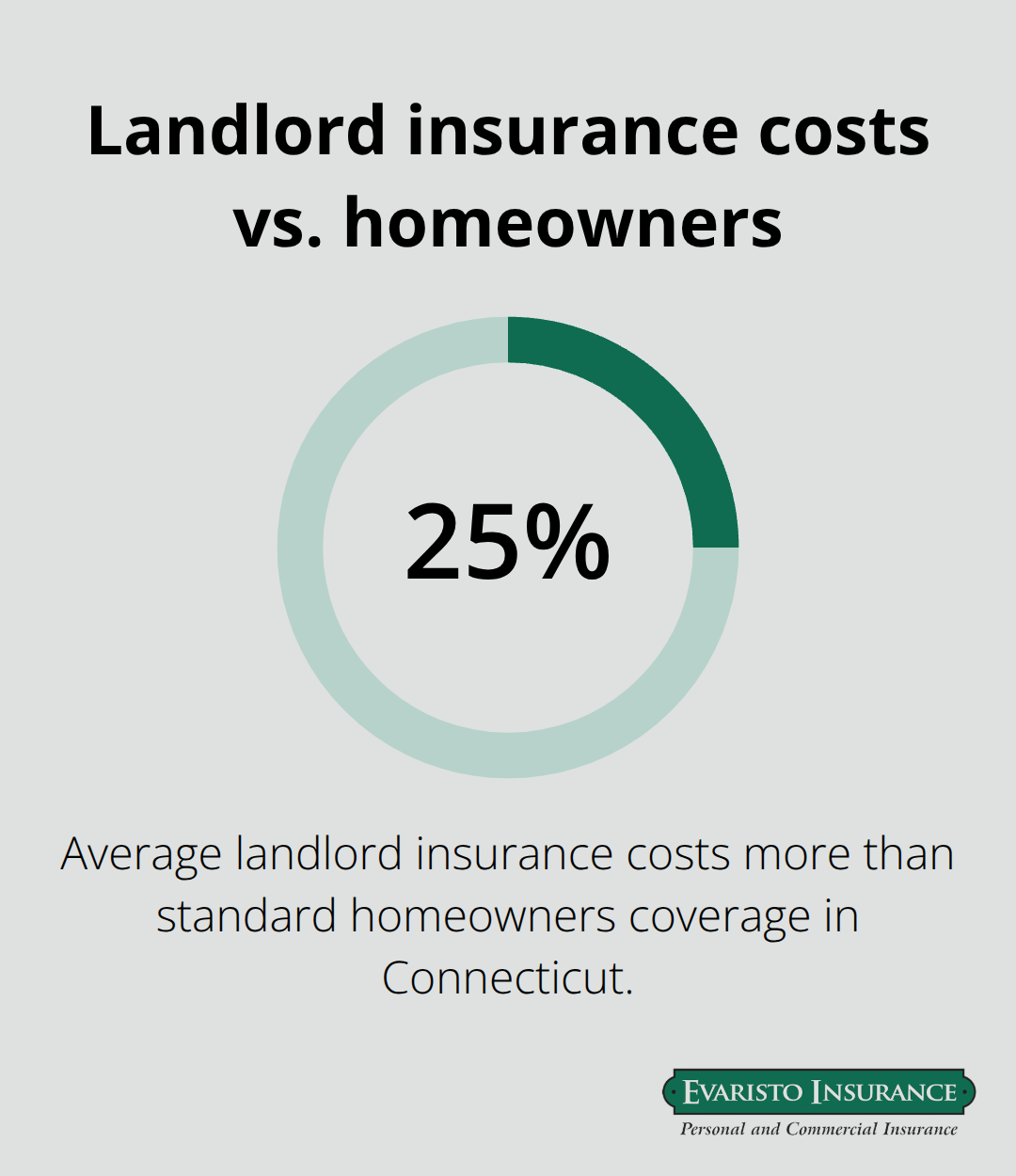

Landlord insurance in Connecticut splits into three distinct coverage buckets, and understanding what each one covers matters if you want real protection. Dwelling coverage protects the rental structure itself-your walls, roof, foundation, and built-in systems-against fire, wind, hail, and other covered perils. This is where most landlords focus, but it’s only one piece of the puzzle. Other structures coverage handles detached buildings on your property like garages, sheds, or fences, which can cost thousands to rebuild and are often forgotten in basic policies. Loss of rental income coverage reimburses you for lost rent while the property sits uninhabitable after a covered event. If a fire damages your Ellington rental and repairs take three months, this coverage protects your cash flow during that gap. Liability coverage shields you if a tenant or visitor is injured on your property. According to the Insurance Information Institute, landlord insurance typically costs about 25 percent more than standard homeowners coverage, with Connecticut averages around $1,083 annually, though Ellington properties vary based on age, location, and construction type.

Why Dwelling Coverage Alone Isn’t Enough

Many landlords treat landlord insurance like homeowners coverage with a different name. That’s dangerous. Your rental property faces different risks than an owner-occupied home. Connecticut’s older housing stock means many rental properties have outdated electrical systems, aging plumbing, and roofs that have seen decades of nor’easters. Dwelling coverage protects the building, but liability coverage protects you when a tenant’s guest slips on ice you didn’t salt, or when faulty wiring causes a fire that damages the neighboring property. Landlord personal property coverage protects your tools and equipment stored on-site for maintenance purposes-not your tenant’s belongings, which is a critical distinction. Tenants must carry their own renters insurance to cover their possessions; your policy won’t touch their furniture or electronics.

The Real Value in Loss of Rental Income

This coverage separates adequate landlord policies from weak ones. If your Ellington rental becomes uninhabitable due to a covered loss, you lose income during repairs. Loss of rental income coverage reimburses that lost rent according to your policy limits. A three-unit property that generates $3,600 monthly and sits empty for four months after a fire represents a $14,400 hit without this coverage. Most Connecticut landlords underestimate how long repairs actually take and how much income they’ll lose. This coverage also protects you if a major tenant injury claim forces you to relocate tenants temporarily or if building code violations discovered during repairs extend timelines significantly. Optional add-ons like building code coverage handle the cost of bringing repairs up to current code standards, which matters in Ellington given local fire prevention and construction standards outlined in Chapter 74 of the town ordinance. Without it, you pay out-of-pocket when code upgrades exceed the cost of replacing damaged materials.

What Connecticut Landlords Often Overlook

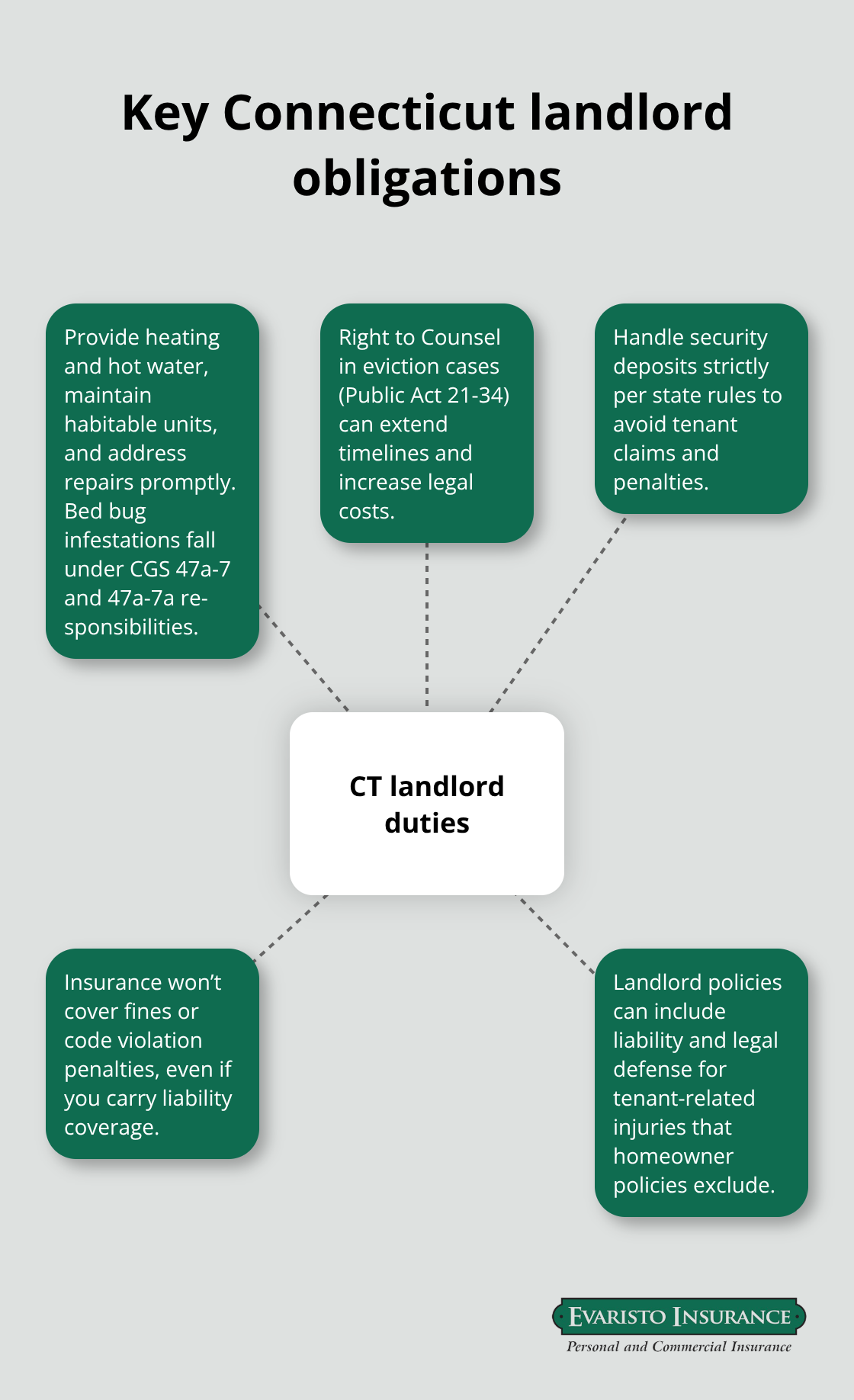

Connecticut’s rental laws create specific obligations that standard policies don’t address. The state requires landlords to provide heating and hot water, maintain habitable units, and address repairs promptly-including bed bug infestations. Failure to meet these obligations can trigger tenant complaints and legal action. Your liability coverage protects you against injury claims, but it won’t cover fines or penalties for code violations. Building code coverage becomes essential when repairs force you to upgrade systems to meet current standards. Ellington’s municipal code (Chapter 138) sets rental property requirements, and Chapter 74 emphasizes fire safety standards that can affect what upgrades your insurer requires. Properties that don’t meet these standards face higher premiums or coverage restrictions. Understanding your local obligations helps you select the right coverage limits and optional add-ons before a loss occurs.

Comparing What Different Carriers Offer

Connecticut landlords have access to multiple carriers-Travelers, Progressive, Stillwater, Safeco, and Foremost all offer landlord coverage with varying limits and optional add-ons. Each carrier prices risk differently based on property age, location, tenant type, and occupancy status. Short-term rentals like Airbnb or VRBO properties often require commercial insurance rather than standard landlord coverage, which changes your options significantly. An independent agent can compare quotes across multiple carriers to find the best combination of coverage and price for your specific property. This approach saves time and money compared to shopping carriers individually. The right policy matches your property’s actual risks, not just the cheapest premium available.

Why Connecticut Landlords Face Different Risks

Connecticut’s Rental Laws Create Real Obligations

Connecticut’s rental laws impose obligations that homeowners never face, and standard homeowner policies simply don’t account for these requirements. The state mandates that landlords provide heating and hot water, maintain habitable units, and address repairs promptly-including bed bug infestations under CGS 47a-7 and 47a-7a. Failure to comply triggers tenant complaints, code enforcement actions, and potential legal liability.

Connecticut also enforces the Right to Counsel in eviction proceedings under Public Act 21-34, meaning tenants can have attorneys present during court proceedings, extending timelines and legal costs. Additionally, security deposit rules are strict; improper handling of deposits invites claims from tenants.

These obligations exist whether you understand them or not, and standard homeowner policies ignore them entirely. Your liability exposure grows when you fail to meet state requirements, and your insurance won’t cover penalties or fines for code violations. Landlord-specific policies address these gaps by including liability coverage for tenant-related injuries and legal defense costs that homeowner policies exclude.

Connecticut’s Older Housing Stock Increases Risk

Your property’s age compounds these risks significantly. Connecticut’s older housing stock means many rental properties contain outdated electrical systems, aging plumbing, and roofs compromised by decades of nor’easters and ice storms. Insurers view older properties as higher risk, and rightfully so-electrical fires, frozen pipes, and roof failures happen more frequently in properties built before 1980. Coastal properties face additional exposure to wind and storm surge damage.

Winter weather in Connecticut causes water damage through failed heating systems and burst pipes more often than most landlords anticipate. Standard homeowner policies don’t account for these Connecticut-specific perils the way landlord policies do.

Standard Homeowner Policies Exclude Rental Properties

Standard homeowner policies exclude rental properties entirely, and that’s the core problem. If you collect rent, you operate a business, not maintain a primary residence. Insurers won’t cover rental income loss under homeowner policies because the policy was never designed for income-generating properties. Liability coverage under homeowner policies often excludes business-related injuries, leaving you exposed if a tenant or contractor is injured while you conduct rental operations.

The distinction matters legally and financially. Connecticut landlords need specialized coverage that addresses tenant-related liability, loss of rental income during repairs, and the higher replacement costs that code compliance upgrades demand. Properties in Ellington specifically must comply with Chapter 138 of the municipal code plus fire safety standards in Chapter 74, which can affect required safety upgrades and insurance costs.

Why Local Expertise Matters for Ellington Properties

Without landlord-specific coverage, you self-insure against risks that could eliminate your rental income for months and expose you to significant liability claims. An independent agent who understands Connecticut’s rental landscape can compare multiple carriers and identify which policies actually match your property’s risks and local obligations. This approach protects you far better than accepting a standard homeowner policy or shopping based on price alone.

How to Shop for Landlord Insurance in Ellington

Compare Quotes Across Multiple Carriers

Comparing carrier quotes side-by-side reveals massive gaps in coverage and price that you’ll miss if you shop alone. Travelers, Progressive, Stillwater, Safeco, and Foremost all write landlord insurance in Connecticut, but each carrier prices your Ellington property differently based on age, location, construction type, and tenant occupancy. A property built in 1955 with a month-to-month tenant will draw higher premiums from some carriers and lower from others depending on their underwriting appetite for older stock and short-term tenants. Progressive might quote $1,200 annually while Stillwater quotes $950 for identical coverage on the same property-a difference worth finding before you bind a policy. Landlord insurance runs roughly 25 percent higher than standard homeowners coverage, but your actual cost depends entirely on which carrier you choose and what optional coverages you add.

Short-term rentals like Airbnb properties often require commercial policies instead of standard landlord coverage, which shifts your pricing and available options completely. An independent agent who represents multiple carriers eliminates the work of calling each company individually and waiting days for quotes.

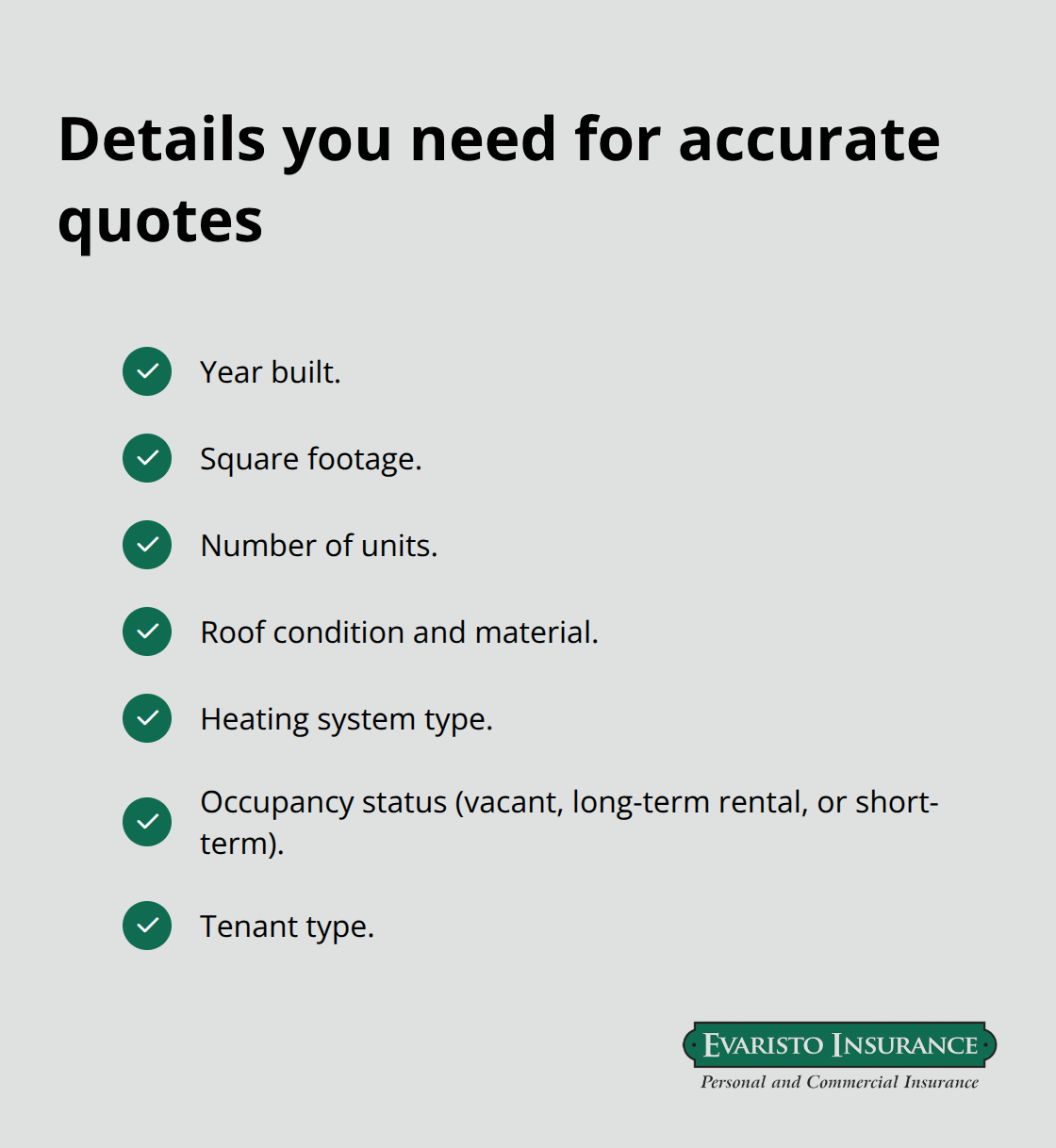

Provide Accurate Property Details for Quotes

Accurate quotes require specific property details that most landlords overlook. Your quote needs to include the property’s year built, square footage, number of units, roof condition and material, heating system type, occupancy status (vacant, long-term rental, or short-term), and tenant type.

Ellington properties must comply with Chapter 138 of the municipal code plus fire safety standards in Chapter 74, which affects what safety upgrades insurers require and how they price risk. A property with updated electrical systems and a recently replaced roof will quote significantly lower than one with original wiring and a 20-year-old roof.

If your property sits vacant between tenants or seasonally, disclose that because vacancy coverage costs extra but protects you during those gaps. Misrepresenting occupancy status to obtain a lower quote creates a coverage problem when you file a claim-insurers will deny it if you lied about how the property is used. Whether you require tenants to carry renters insurance also affects your quote and your overall liability exposure.

Work with an Independent Agent

An independent agent who understands Connecticut’s rental landscape can compare multiple carriers and identify which policies actually match your property’s risks and local obligations. This approach protects you far better than accepting a standard homeowner policy or shopping based on price alone. Evaristo Insurance, a second-generation family-owned independent agency serving Connecticut since 1989, compares multiple top carriers to find the combination that fits your property’s actual risks without overpaying for coverage you don’t need or underinsuring against gaps that could cost thousands.

Contact the Ellington office at 304 Somers Rd or call 860-870-8122 to request quotes based on your property’s specific details, or text 860-407-2006 to start the process. Office hours run Monday through Friday from 9:00 am to 5:00 pm, and the team can walk you through what information you’ll need to gather for accurate pricing.

Final Thoughts

Ellington CT landlord insurance protects your rental income and shields you from liability exposure that standard homeowner policies ignore. The coverage you select determines whether a major loss becomes a manageable claim or a financial catastrophe that forces you to sell the property. Dwelling coverage, liability protection, and loss of rental income coverage form the foundation of adequate protection, while optional add-ons like building code coverage fill gaps that Connecticut’s older housing stock and local regulations create.

Connecticut’s rental laws impose obligations that most landlords underestimate, and Ellington’s municipal code adds local requirements around fire safety and property maintenance that affect what your insurer requires. You must provide heating and hot water, maintain habitable units, and address repairs promptly-failures that expose you to fines, penalties, and tenant claims that standard homeowner policies won’t address. The right policy matches your property’s actual risks, not just the cheapest premium available, and comparing quotes across multiple carriers reveals pricing differences of hundreds of dollars annually for identical coverage.

An independent agent who understands Connecticut’s rental landscape can compare multiple carriers, identify which policies match your property’s specific risks, and guide you through optional coverages that matter for Ellington properties. Contact Evaristo Insurance at 304 Somers Rd or call 860-870-8122 to request quotes based on your property’s details, or text 860-407-2006 to start the process. The team walks you through what information you’ll need and answers questions about coverage options that fit your rental business.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!