General Contractor Insurance CT: Essential Coverage for Pros

Running a contracting business in Connecticut means navigating state-specific requirements that most general contractors overlook. General contractor insurance isn’t just a box to check-it’s the foundation that protects your business, your crew, and your reputation on every job site.

At Evaristo Insurance, we’ve seen too many contractors operate with gaps in their coverage that could cost them everything. This guide walks you through exactly what you need to know to stay protected.

Connecticut Licensing Requirements and Insurance Obligations

What the State Actually Requires

Connecticut’s Department of Consumer Protection divides contractor licensing into three categories, and each one triggers different insurance obligations. If you hold a Major contractor license (what most people call a general contractor license), you must carry general liability insurance and submit a certificate listing the DCP as certificate holder before your license receives approval. The state requires at least $20,000 in general liability coverage as a baseline, though most contractors carry $1 million per occurrence and $2 million aggregate-the combination chosen by about 97% of contractors according to Insureon. If your work stays limited to home improvements or new home construction, you only need to file a contractor registration with the DCP, not a full license, but insurance requirements don’t disappear; they shift instead.

Workers’ compensation insurance becomes mandatory the moment you hire your first employee in Connecticut, and the state requires you to secure coverage through a state-approved insurer. Many contractors assume that their personal business policy covers job site incidents, equipment theft, or employee injuries-it does not. Standard commercial policies contain massive gaps that leave you exposed on multiple fronts.

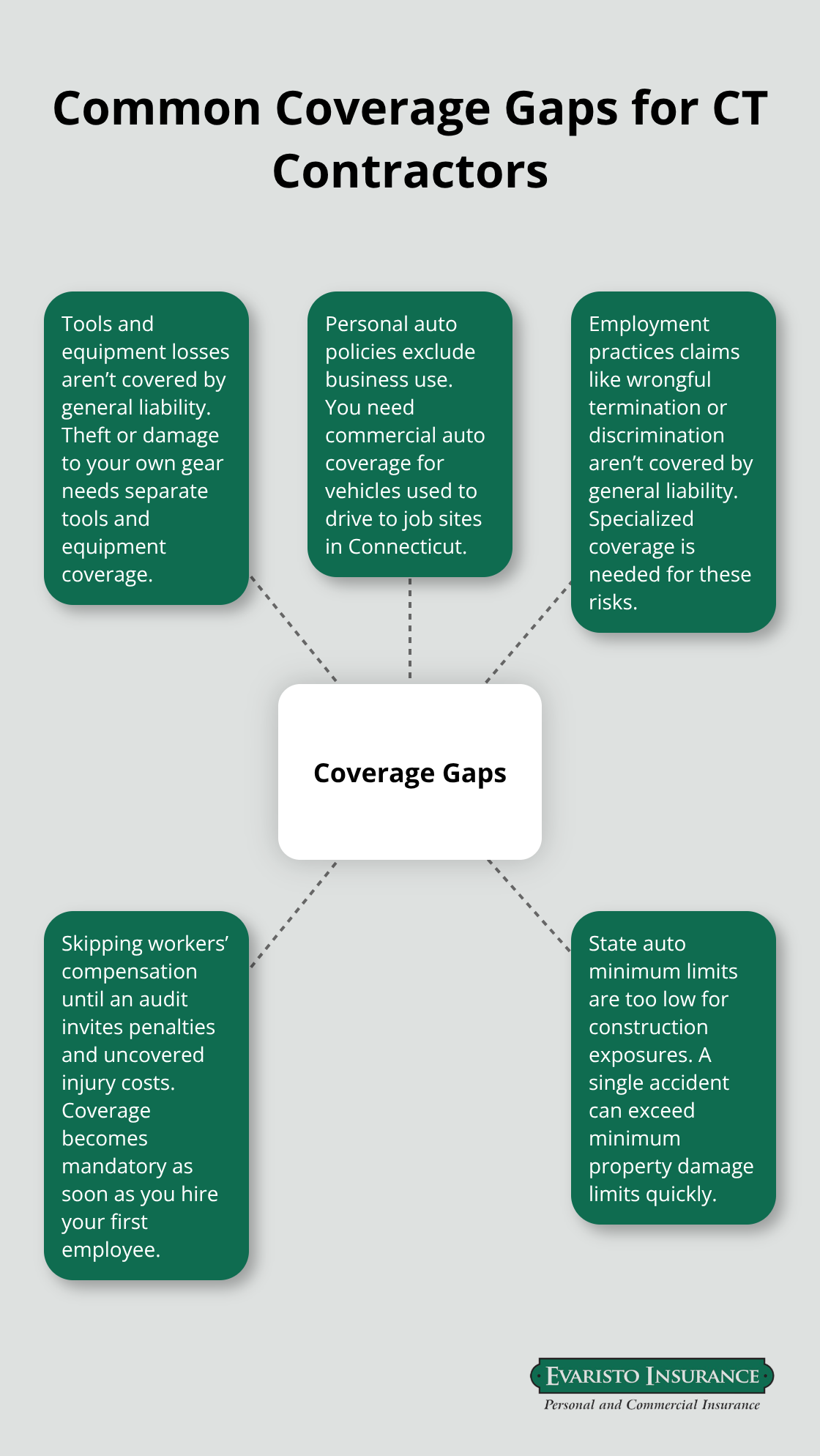

The Coverage Gaps That Cost Contractors Money

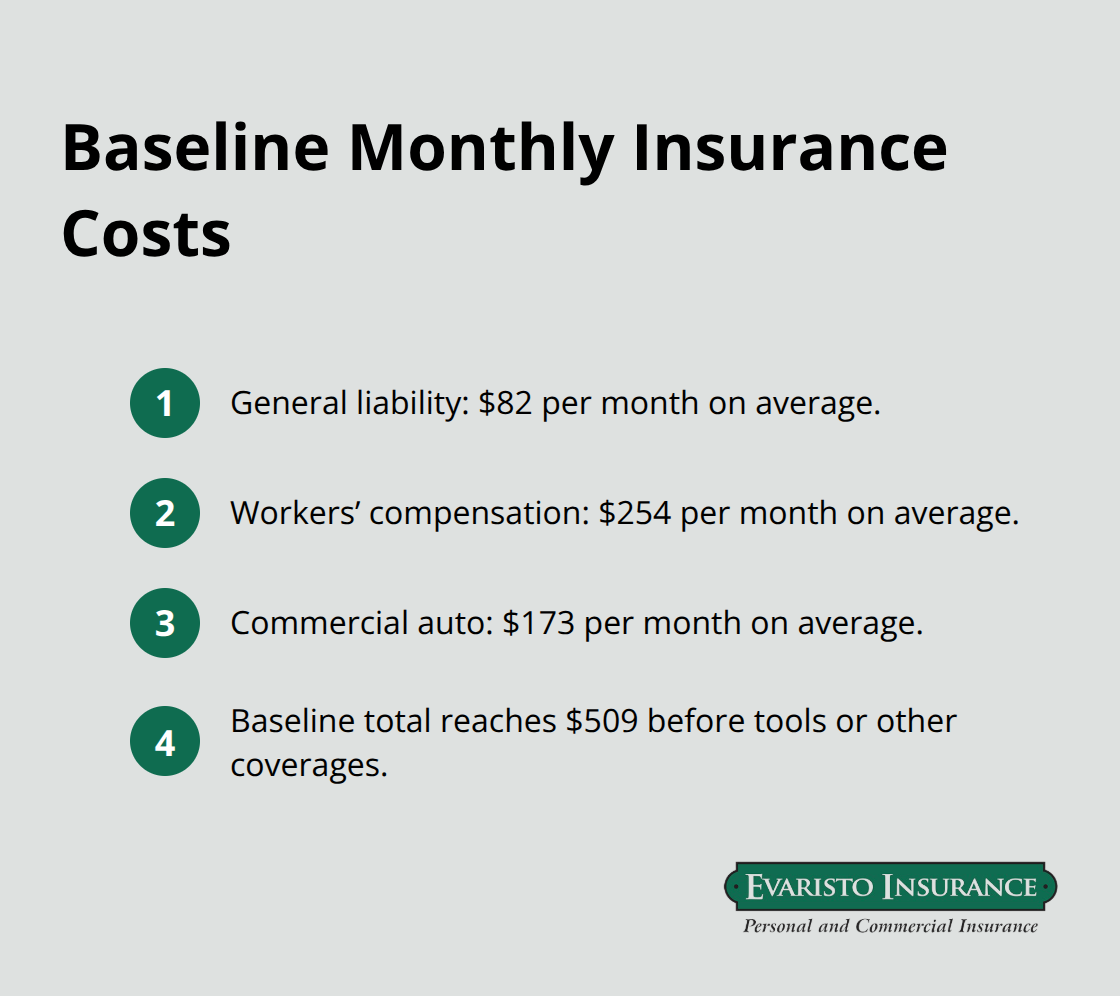

The real danger isn’t what your policy covers; it’s what it doesn’t. A general liability policy protects you if a client sues because you damaged their property or someone gets injured on site, but it won’t cover your own tools stolen from a job, your vehicle used for work, or claims from employees about wrongful termination or discrimination. Roofers in Connecticut pay around $267 per month for general liability alone, while general contractors average closer to $82 per month, yet many skip workers’ compensation coverage entirely until they face a state audit.

Tools and equipment coverage is almost universally missing, leaving contractors vulnerable to theft losses that eat directly into profit margins. Commercial auto insurance represents another blind spot-your personal auto policy explicitly excludes business use, and driving to job sites in a personal vehicle without commercial auto coverage violates Connecticut law and leaves you personally liable. The state’s minimums are $25,000 per person, $50,000 per accident, and $25,000 for property damage, but these limits are dangerously low for construction work.

Building a Coordinated Insurance Stack

You need to stack general liability, workers’ compensation, commercial auto, tools and equipment coverage, and professional liability (errors and omissions) into a coordinated package, not scattered across multiple carriers. This approach costs around $600 to $800 monthly for a typical general contractor operation but prevents the catastrophic gaps that have bankrupted contractors operating with incomplete coverage. The next section breaks down each essential coverage type and shows you exactly what protection each one provides on the job site.

The Three Coverage Pillars Every Connecticut Contractor Needs

General Liability: Your First Line of Defense

General liability insurance protects you when a client sues because you damaged their property or someone gets injured at the job site, but the protection only works if your limits match the actual risk you face. Connecticut contractors carrying the standard $1 million per occurrence and $2 million aggregate limits pay around $82 per month on average according to Insureon, though your actual cost depends entirely on your trade and claims history. Roofers pay triple that amount at roughly $267 per month because the work carries higher injury risk, while a locksmith might pay only $42 monthly. The state’s minimum of $20,000 is laughable for any serious operation-you need at least $1 million per occurrence to protect yourself from a single catastrophic claim.

Workers’ Compensation: Protecting Your Team

When you hire employees, workers’ compensation becomes legally mandatory in Connecticut through a state-approved insurer, and this coverage handles medical expenses, rehabilitation costs, and lost wages when someone gets hurt on the job. Most contractors underestimate the cost, expecting to pay $150 or $200 monthly, but the actual average runs around $254 per month according to Insureon because the calculation depends on your payroll size and the specific risk level of the work you perform. A roofing operation with five employees costs significantly more than a small carpentry crew, and the state requires you to post notices about your coverage and maintain compliance records that regulators inspect during audits.

Tools, Equipment, and Commercial Auto Coverage

Tools and equipment coverage fills a massive gap that general liability completely ignores-if someone steals your $8,000 compressor from a job site or your truck gets broken into overnight, general liability won’t pay a dollar. This coverage protects portable equipment, power tools, vehicles, and materials stored both on-site and in off-site storage, and the monthly cost scales with the total value of equipment you own. Many contractors bundle general liability with commercial property coverage into a Business Owner’s Policy for around $98 monthly, which combines job site protection with coverage for your office or workshop.

Commercial auto insurance represents the third pillar that catches most contractors off guard because they assume their personal auto policy covers work driving-it explicitly does not. Connecticut’s legal minimums are $25,000 per person, $50,000 per accident, and $25,000 for property damage, though these limits are dangerously inadequate for construction work where a single accident can cause $100,000 in damages. The average cost runs about $173 per month for commercial auto coverage, and if you use personal or rented vehicles for work, you need hired and non-owned auto insurance instead.

Building Your Complete Coverage Stack

The practical reality is that stacking general liability at $82 monthly, workers’ compensation at $254, and commercial auto at $173 reaches $509 before you add tools coverage or any other protection-this is the minimum investment for a legitimate operation. Your specific trade determines which additional coverages matter most, and that’s where working with an agent who understands Connecticut’s construction landscape makes a real difference.

The next section shows you how to find the right insurance provider who can customize a package that actually fits your business instead of forcing you into generic policies that leave critical gaps.

Finding the Right Insurance Partner for Your Trade

Compare Quotes from Multiple Carriers

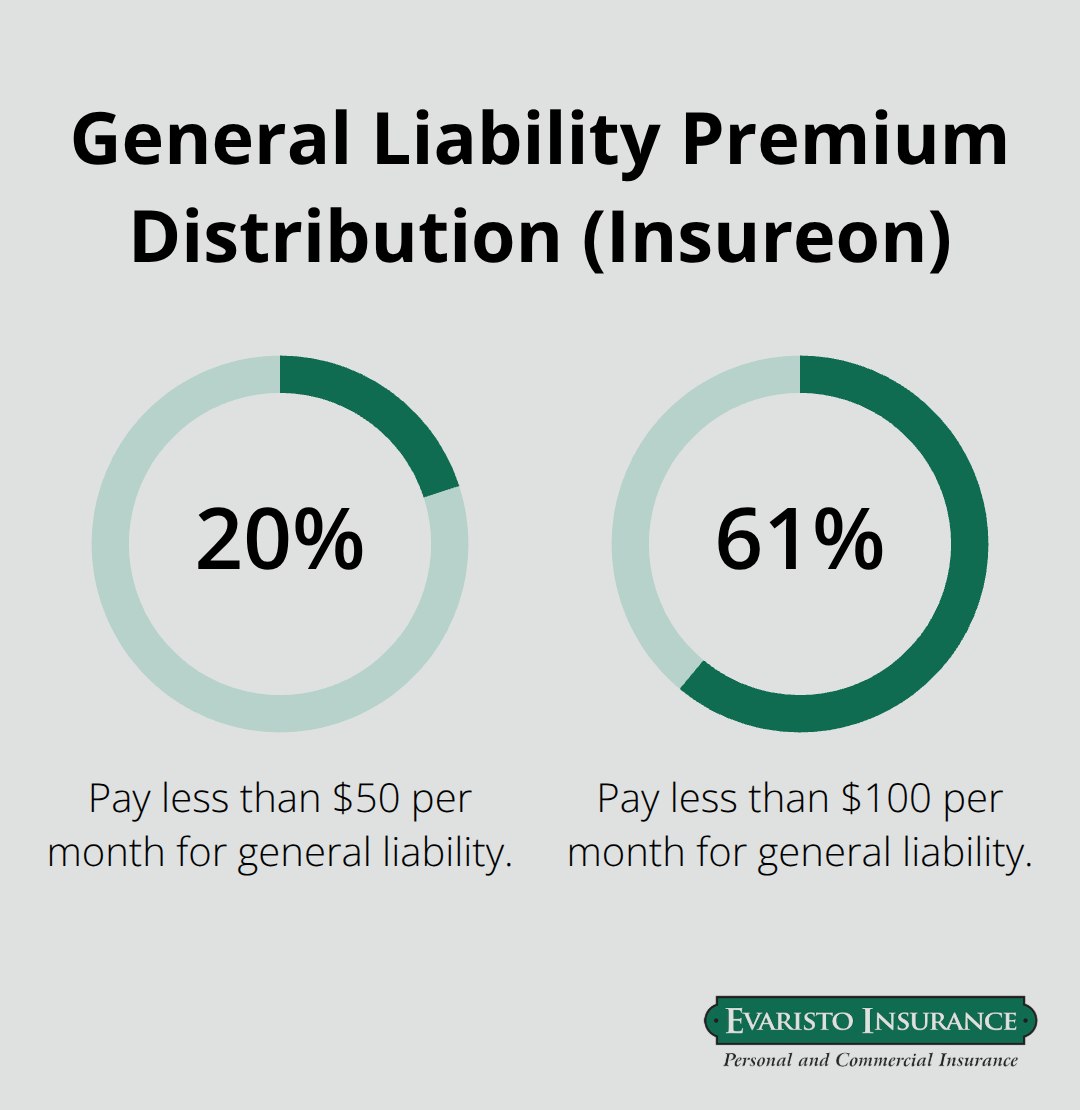

Shopping for contractor insurance in Connecticut means comparing actual quotes from multiple carriers, not calling your personal auto agent and asking them to add a commercial rider. Insurance brokers often push one-size-fits-all packages or spend hours asking irrelevant questions about office square footage when what matters is your specific trade, job site risks, and claims history. Request written quotes from at least three different carriers because premium variations for identical coverage swing 40 to 60 percent depending on how each insurer rates roofing versus carpentry versus general contracting work. Insureon data shows that about 20 percent of construction businesses pay less than $50 monthly for general liability while 61 percent pay less than $100 monthly, which means your actual cost depends entirely on risk assessment, not industry standards. Request written quotes within a few days of your initial conversation, and confirm each quote specifies your coverage limits, deductibles, and exactly which coverages are included because verbal quotes create confusion when bills arrive.

Never choose based on lowest price alone because a carrier quoting $45 monthly for general liability might rate your roofing operation as residential carpentry, creating a coverage denial when you file a claim. The cheapest option often reflects incorrect risk classification rather than legitimate savings.

Work with an Agent Who Understands Connecticut Construction

An independent agency that represents multiple carriers holds far more power to negotiate rates and find carriers willing to insure your specific operation compared to captive agents representing only one company. An agent who understands Connecticut’s construction landscape customizes quotes to match your actual trade rather than forcing you into generic contractor packages. When you contact an agent, bring your contractor registration certificate from the Connecticut Department of Consumer Protection, your current project list, your payroll information, and details about equipment you own and store on job sites because agents need concrete information to request accurate quotes.

Ask directly whether the quotes reflect your actual trade risk and whether the carrier has experience insuring contractors in your specific specialty because some insurers avoid roofing or high-risk trades entirely, pricing them out of the market. Request current certificates of insurance from any carrier you’re considering to verify they’re actively writing Connecticut contractor coverage, and confirm that general liability limits can reach $1 million per occurrence and $2 million aggregate since some carriers cap limits lower than standard.

Optimize Your Coverage Bundle

The agent should explain how bundling general liability with commercial property into a Business Owner’s Policy affects your total cost, since this combination typically runs around $98 monthly and often saves money compared to separate policies. Ask about your specific renewal date and whether the carrier offers online policy management so you can update coverage as your business grows or your project mix changes without waiting for agent callbacks. Confirm that the carrier can adjust your workers’ compensation rates as your payroll fluctuates and that they provide clear documentation of coverage changes throughout the policy year.

Final Thoughts

General contractor insurance in CT protects your business from the financial devastation that follows a single claim, and the coverage gaps most contractors carry cost far more than the premiums they avoid by skipping workers’ compensation or commercial auto protection. You need general liability at $1 million per occurrence, workers’ compensation matching your payroll size, commercial auto coverage for work driving, and tools protection for equipment on job sites-these four pillars address the real risks you face daily. Request written quotes from multiple carriers who understand Connecticut construction work rather than treating your roofing operation like residential carpentry, and compare limits across at least three providers to verify they reach $1 million per occurrence and $2 million aggregate.

An independent agency comparing multiple carriers negotiates rates and finds coverage options that captive agents representing single companies cannot access, and bundling general liability with commercial property into a Business Owner’s Policy often saves money while simplifying administration. Bring your DCP registration certificate, current project details, and equipment inventory to those conversations because agents need concrete information to quote accurately and match your specific trade risk. Verify that each carrier has active experience insuring your trade and confirm the quote specifies your coverage limits, deductibles, and exactly which coverages are included.

We at Evaristo Insurance have served Connecticut contractors since 1989, comparing top carriers to deliver tailored protection and competitive pricing rather than forcing generic packages that leave critical gaps. Our local offices in Ellington and West Hartford mean you work with agents who understand Connecticut’s licensing requirements, state-specific coverage gaps, and the actual risks your trade faces on the job site. Contact us to discuss your specific operation and receive quotes that reflect your real business instead of industry assumptions.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!