Smart Ways To Maximize Value With Business Insurance Bundle Options

Business owners in Connecticut often overpay for insurance because they’re buying policies separately instead of bundling them together. At Evaristo Insurance, we’ve seen firsthand how the right business insurance bundle options can cut costs while actually improving your coverage.

When you bundle policies, you’re not just saving money on premiums-you’re also simplifying how you manage your protection. This guide shows you exactly how to find and choose bundles that work for your business.

Why Business Insurance Bundles Cut Your Real Costs

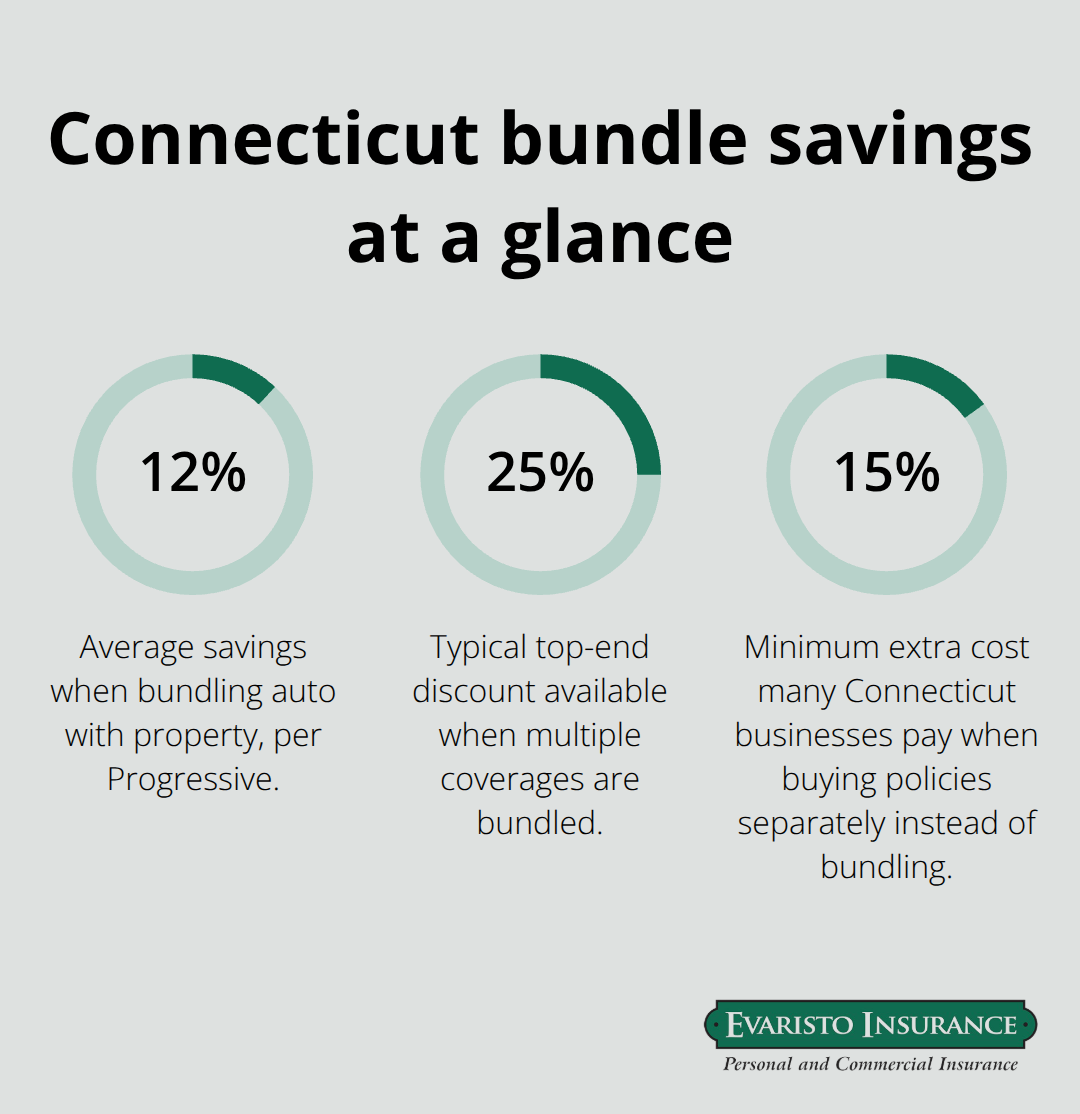

Connecticut businesses that purchase policies separately typically pay 15–25% more than those who bundle comparable coverage. Progressive reports that bundling auto coverage with property generates average savings of about 12%, and adding more coverages to the mix increases those discounts further. A sole proprietor paying $200 per month for separate policies versus $155 for a bundled package saves $540 annually-money that stays in your business instead of going to your insurance carrier.

How Insurers Price Bundled Policies

Insurers offer package discounts because bundled policies reduce their administrative costs and lower their risk across your account. When you consolidate with one carrier, they manage fewer policies, process fewer claims, and handle streamlined renewals. That efficiency translates directly into lower premiums for you. A landscaper in Bristol might pay different rates than a tree trimmer in New Haven due to location and business type, but both benefit from discounts applied across their entire package. The Connecticut Workers’ Compensation Board requires employers to compensate their employees who suffer work-related injuries or occupational diseases, regardless of who is at fault, and bundling workers’ compensation with your general liability and property policies typically delivers better pricing than purchasing workers’ comp separately.

One Policy, One Renewal Date, One Agent

Separate policies mean separate renewal dates, separate billing statements, and separate conversations with different agents. A bundled package consolidates everything into one policy with one renewal date and one point of contact. This matters when you need to update coverage limits, add employees, or file a claim. A single agent managing your bundle knows your entire risk profile instead of handling just one piece of it. You avoid the common mistake of letting coverage gaps develop because you forgot to renew a separate policy or didn’t realize one policy excluded something another covered.

The Business Owner’s Policy Advantage

A Business Owner’s Policy coordinates property coverage, general liability, and business interruption insurance under one framework. This structure simplifies everything from annual reviews to claims processing. You receive coordinated protection rather than disconnected pieces, which means your coverages work together instead of against each other. When you file a claim, one agent manages the entire process across all three coverage types. This coordination prevents the frustration of discovering that one policy covers a loss while another doesn’t, or that your coverages overlap in some areas while leaving gaps in others.

The right bundle transforms how you manage risk. Now that you understand the financial and operational advantages, the next step involves identifying which specific bundle options align with your industry and business structure.

Business Insurance Bundle Combinations That Actually Work

Connecticut businesses face different risk profiles depending on their industry and structure, which means the bundles that work best vary significantly from one company to the next. A restaurant owner needs different coverage than a consulting firm, and a sole proprietor has different requirements than a business with ten employees. The bundles available through most carriers fall into three practical categories, each addressing specific business scenarios you’ll recognize immediately.

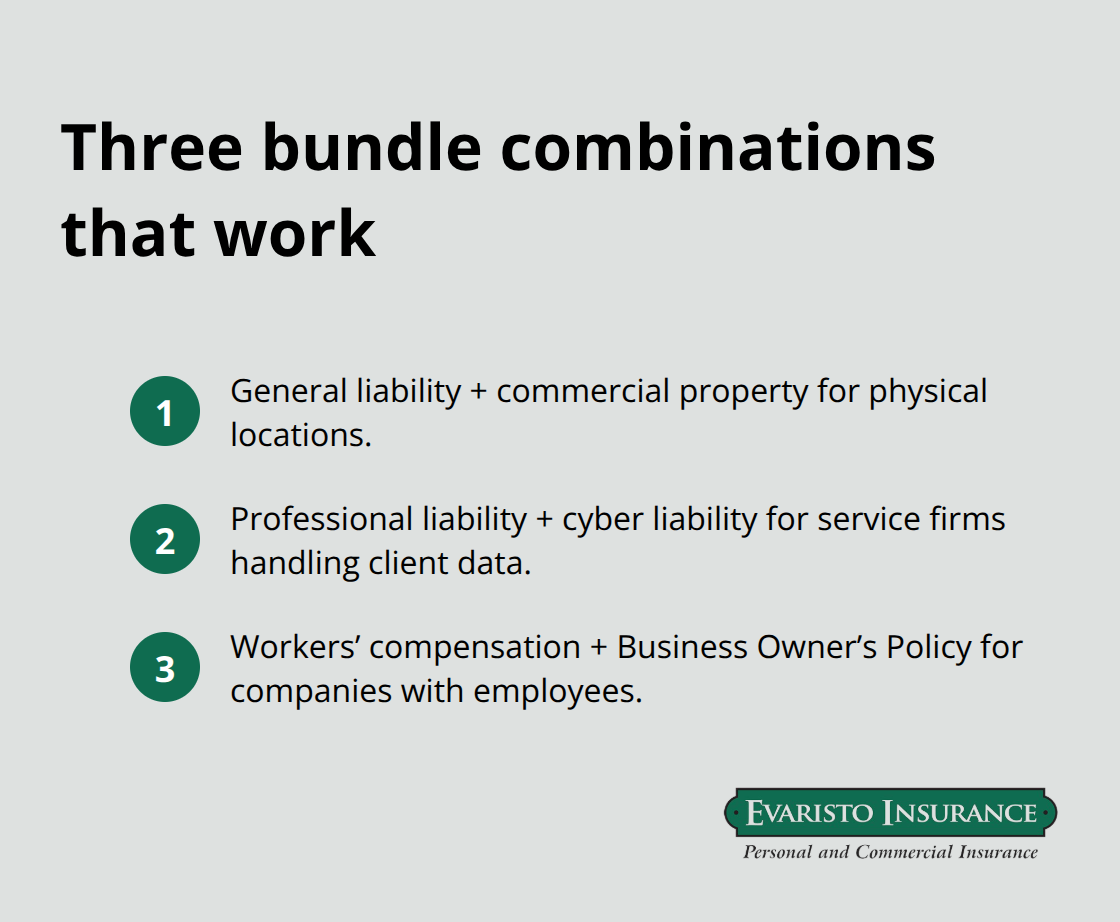

General Liability and Property Coverage for Physical Locations

General liability paired with commercial property coverage protects businesses that own or lease physical space and need protection against both third-party claims and on-site damage. A Hartford restaurant carrying general liability and property coverage can handle a slip-and-fall claim from a patron while also protecting against fire or water damage that forces temporary closure. This combination works because the coverages complement each other-liability covers what happens to others at your location, while property covers what happens to your building and equipment. The two policies operate together rather than in isolation, which means your agent can coordinate coverage limits and ensure no gaps exist between them.

Professional Liability and Cyber Liability for Service Firms

Professional service firms and businesses handling customer data benefit most from pairing professional liability with cyber liability coverage. Professional liability, also called errors and omissions insurance, covers mistakes in your work that cause client losses. A tax accountant’s calculation error that costs a client thousands in missed deductions receives coverage under professional liability. Cyber liability protects against data breaches, ransomware attacks, and the costs of notifying affected clients, plus legal and forensic investigation expenses. These two work together because service firms increasingly store client information digitally, creating exposure on both fronts. The combination addresses both operational risks (your work performance) and technology risks (your data security) in one coordinated package.

Workers’ Compensation and Business Owner’s Policy for Companies With Employees

The third major bundle combines workers’ compensation with a Business Owner’s Policy for companies with employees. Connecticut law requires workers’ compensation for any business with employees, and bundling it with property and liability coverage under a single BOP streamlines administration while generating meaningful discounts. A small manufacturing operation with five employees bundling workers’ comp, property, and general liability pays less than purchasing those coverages separately, and manages everything through one renewal cycle instead of three separate ones.

Matching Your Bundle to Your Actual Business

Each bundle type targets real business scenarios, and your choice depends on what you actually do and who works for you. A sole proprietor consultant needs different protection than a contractor with a crew and equipment. Location matters too-a Bristol business faces different seasonal risks than one in New Haven. The next step involves assessing your specific industry risks so you can identify which bundle structure aligns with your operation and where you might need additional coverage beyond the standard packages.

Choosing the Right Bundle for Your Connecticut Business

Start with what actually happens at your business. A restaurant owner faces slip-and-fall claims and property damage from kitchen fires. A consulting firm handles client data and professional mistakes. A contractor with employees manages job-site injuries and equipment theft. These aren’t abstract risks-they’re the specific exposures that generate claims. Once you identify what can go wrong, you can evaluate which bundle addresses those exposures and where you need additional coverage beyond the standard package.

Assess Your Industry’s Real Exposure

Connecticut businesses with owned or leased property need general liability paired with commercial property coverage because landlords typically require liability as a lease condition, and property damage from fire or water can force temporary closure. Service-based businesses handling client information must include cyber liability with professional liability to cover both data breach costs and work performance errors. A contractor with employees cannot skip workers’ compensation because Connecticut law requires it for any business with employees, making a business owners insurance bundle that includes workers’ comp non-negotiable.

Your industry determines which risks matter most. A restaurant’s exposure differs completely from a consulting firm’s exposure, which differs from a contractor’s exposure. The bundle you select should address the specific claims your business actually faces, not generic risks that don’t apply to your operation.

Match Your Bundle to Headcount and Location

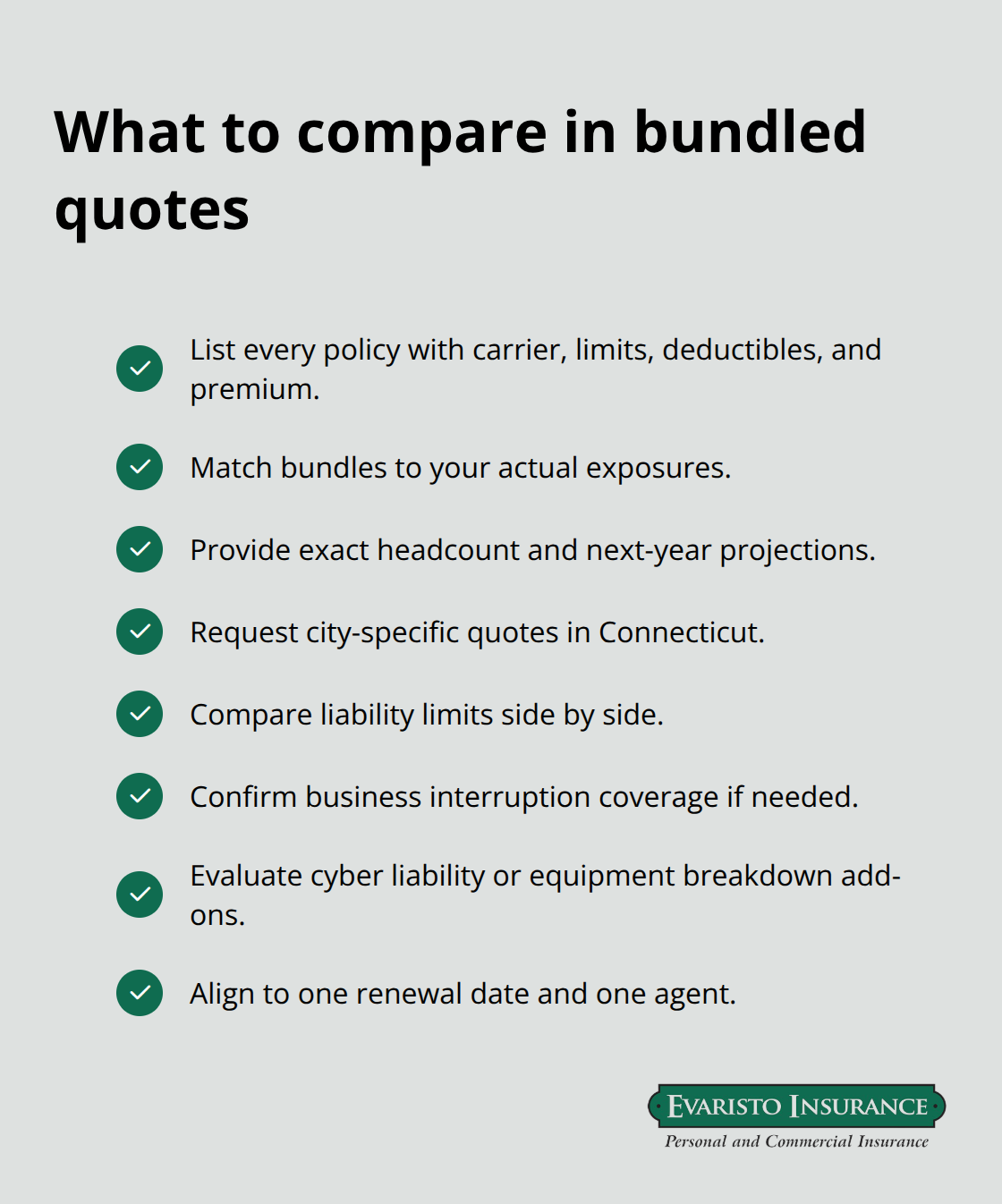

The number of employees you have directly affects both your coverage needs and your premium costs. A sole proprietor pays significantly less for workers’ compensation than a business with ten employees because payroll determines the cost. When requesting quotes, provide your exact current headcount and realistic employee projections for the next year-underestimating headcount leads to underpayment now and coverage gaps later.

Location within Connecticut matters more than most owners realize. A Bristol business and a New Haven business in the same industry can pay different rates based on local loss history, labor costs, and claim frequencies. When comparing bundled quotes from different carriers, get pricing for your specific city rather than treating all of Connecticut as one market.

Compare Coverage Details, Not Just Premium Price

Two bundles priced identically can provide vastly different protection. One might include business interruption coverage that replaces lost income after a fire, while another covers only the physical property damage. One might set general liability limits at one million dollars per occurrence while another offers two million. Higher limits increase premiums but provide substantially better protection against catastrophic claims.

A small restaurant should carry higher liability limits than a home-based consulting firm because the exposure differs dramatically. When comparing bundles across providers, list the specific coverage limits, deductibles, and included protections side by side rather than just comparing premium prices. A bundle costing fifty dollars more monthly might include equipment breakdown protection or cyber liability add-ons that another bundle excludes entirely.

The true cost of a bundle isn’t the premium-it’s the premium plus the risk you retain because coverage is too narrow or limits are too low. Connecticut small businesses often choose bundles based purely on price and later discover that their coverage leaves critical gaps. A local insurance agent can compare multiple carriers and show you what each bundle actually includes, helping you identify which option truly fits your business rather than just costing the least.

Final Thoughts

Bundling your business insurance delivers three concrete advantages that separate policies cannot match: you save money through package discounts that typically range from 12% to 25%, you eliminate the administrative burden of managing multiple renewal dates and billing statements, and you gain coordinated protection where your coverages work together instead of creating gaps. A Connecticut business owner paying $200 monthly for separate policies versus $155 for a bundled package keeps $540 annually in operating capital. That’s real money that funds growth instead of padding insurance company margins.

Start reviewing your current coverage by listing every policy you carry, including the carrier, coverage limits, deductibles, and annual premium for each. Next to each policy, note what it covers and what it excludes. This inventory reveals where you have overlapping coverage and where gaps exist-many Connecticut business owners discover they’re paying for duplicate coverage in some areas while leaving critical exposures unprotected in others. Once you see the full picture, you can identify which business insurance bundle options would consolidate your protection while reducing your total cost.

An independent agent representing several top insurers can show you bundled options from different companies, explain what each bundle includes, and help you match coverage to your actual industry risks rather than generic protection that doesn’t fit your operation. We at Evaristo Insurance have served Connecticut businesses since 1989, comparing multiple carriers to deliver bundled protection tailored to your specific needs. Contact us to review your current coverage and explore how the right business insurance bundle can cut your costs while improving your protection.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.