Home Insurance Policy Features: A Quick Look At Coverage Options

Your home insurance policy features determine what’s actually protected when something goes wrong. Most homeowners don’t realize how much variation exists between policies-and that gap can cost thousands when you need coverage most.

We at Evaristo Insurance help Connecticut homeowners understand their options so they can make informed decisions. This guide breaks down dwelling coverage, personal property protection, liability, and the add-ons that matter for your specific situation.

Dwelling Coverage and Structural Protection

Dwelling coverage forms the foundation of your homeowners policy. It protects the structure of your home itself-the walls, roof, foundation, built-in appliances, flooring, and attached structures like decks or patios. Personal property coverage, by contrast, protects your belongings inside the home. In Connecticut, dwelling coverage rebuilds your house after a fire, windstorm, or other covered damage. The average Connecticut homeowner carries about $400,000 in dwelling coverage according to U.S. News & World Report data, though your specific limit depends entirely on what it would cost to rebuild your home from the ground up today, not what you paid for it years ago. This distinction matters enormously-construction costs have risen significantly, and underestimating replacement cost leaves you short thousands of dollars when you need to rebuild.

How Coverage Limits Translate to Real Protection

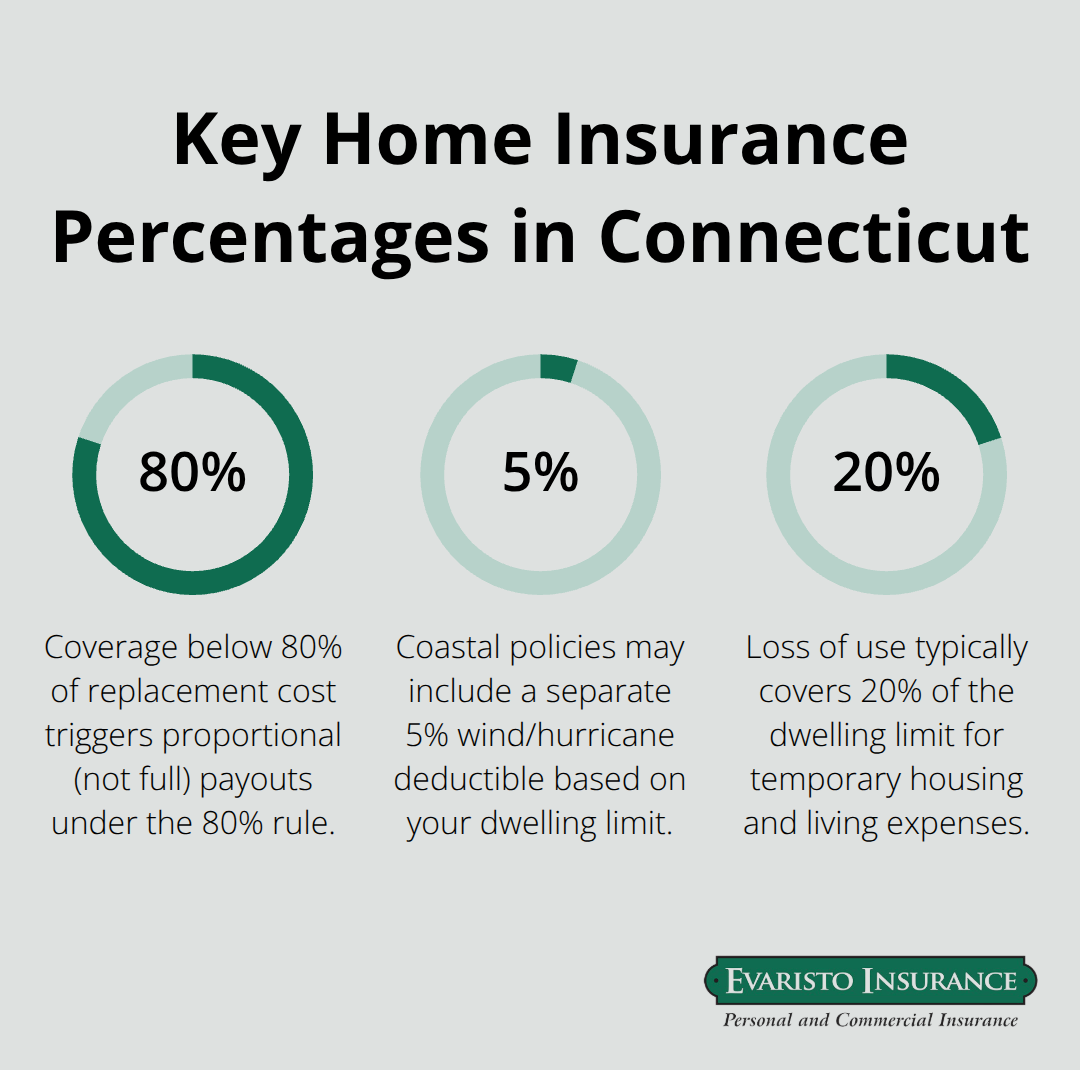

Your dwelling coverage limit determines your maximum payout for structural damage, but the way this limit works often surprises homeowners. If your home would cost $300,000 to rebuild and you carry $300,000 in dwelling coverage, you’re at the right level. However, if you only carry $240,000 (80% of replacement cost), Connecticut insurers apply what’s called the 80% rule-meaning you’ll only recover a proportional share of losses rather than full replacement cost. For example, if a fire causes $50,000 in damage and you’re underinsured at 80%, you recover only $40,000 instead. This penalty applies even to partial losses, so meeting replacement cost levels isn’t optional if you want full protection.

Coastal Connecticut homeowners face an additional complication: windstorm and hurricane deductibles often apply separately, meaning you could face a 5% deductible on top of your regular deductible after a storm (on a $300,000 home, that’s $15,000 out of pocket before coverage kicks in).

Replacement Cost Versus Actual Cash Value

Replacement cost coverage pays what it costs to rebuild or replace damaged items new, while actual cash value subtracts depreciation from the payout. This difference can be thousands of dollars. A roof that costs $15,000 to replace might only receive a depreciated payout if it’s 15 years old, even though you still need to pay the full $15,000 to fix your home. Most Connecticut homeowners should insist on replacement cost coverage for dwelling protection because your goal after a loss is to restore your home to its current condition, not accept a depreciated settlement. Some policies offer this automatically, but others charge extra for replacement cost coverage-typically a 10–15% premium increase that’s well worth the cost. When you review your policy, confirm whether you have replacement cost or actual cash value, and if it’s actual cash value, contact your agent immediately about upgrading. The out-of-pocket difference after a major loss could exceed $20,000, making this one of the most important choices in your entire policy.

What Happens When You’re Underinsured

Underinsurance creates real financial consequences that extend beyond the initial loss. The 80% rule means Connecticut insurers won’t pay full replacement cost if you fall short of adequate coverage limits. You pay the difference out of pocket, and that gap compounds when construction costs spike or you face multiple damaged areas. Coastal properties add another layer of complexity with separate windstorm deductibles that can reach 5% of your dwelling limit. These deductibles apply independently of your standard deductible, so a major hurricane could leave you responsible for thousands before your insurance pays anything. Understanding your actual replacement cost-not your home’s market value-protects you from this trap. Work with your agent to calculate what it would truly cost to rebuild your home today, then carry that amount in coverage.

Personal Property and Liability Protection

What Personal Property Coverage Actually Protects

Your personal property coverage pays to replace or repair your belongings inside your home when damage or theft occurs. This includes furniture, electronics, clothing, kitchen appliances, and everything else you own. That sounds reasonable until you actually inventory your possessions. Most homeowners discover they own far more than they think. A single television costs $2,000, a bedroom set runs $5,000, kitchen appliances add another $8,000, and clothing and personal items easily total $15,000 or more. If theft or a fire destroys your contents, your coverage limit disappears fast.

The coverage also depends on whether you have replacement cost or actual cash value. With actual cash value, a five-year-old laptop worth $1,200 new pays you only $400 because depreciation strips away two-thirds of its value. Replacement cost coverage pays what you need to buy a new laptop today, which is why it matters far more than most Connecticut homeowners realize. You should strongly consider upgrading to replacement cost coverage for personal property, even though it increases your premium by roughly 15–20%. The alternative is accepting thousands in losses out of pocket when you need to rebuild.

Protection Against Theft and Water Damage

Theft and water damage represent the two biggest threats to your contents in Connecticut homes. According to FBI crime data, property crime rates in Connecticut averaged around 1,600 incidents per 100,000 residents in recent years, making theft a real concern in many neighborhoods. Standard homeowners policies cover theft of personal property, but they impose limits on specific categories. Jewelry, cash, and collectibles often have sub-limits of just $1,500 to $2,500 per item, even if your total contents coverage is much higher. If you own an engagement ring worth $8,000 or collectible artwork valued at $10,000, that standard limit leaves you massively exposed.

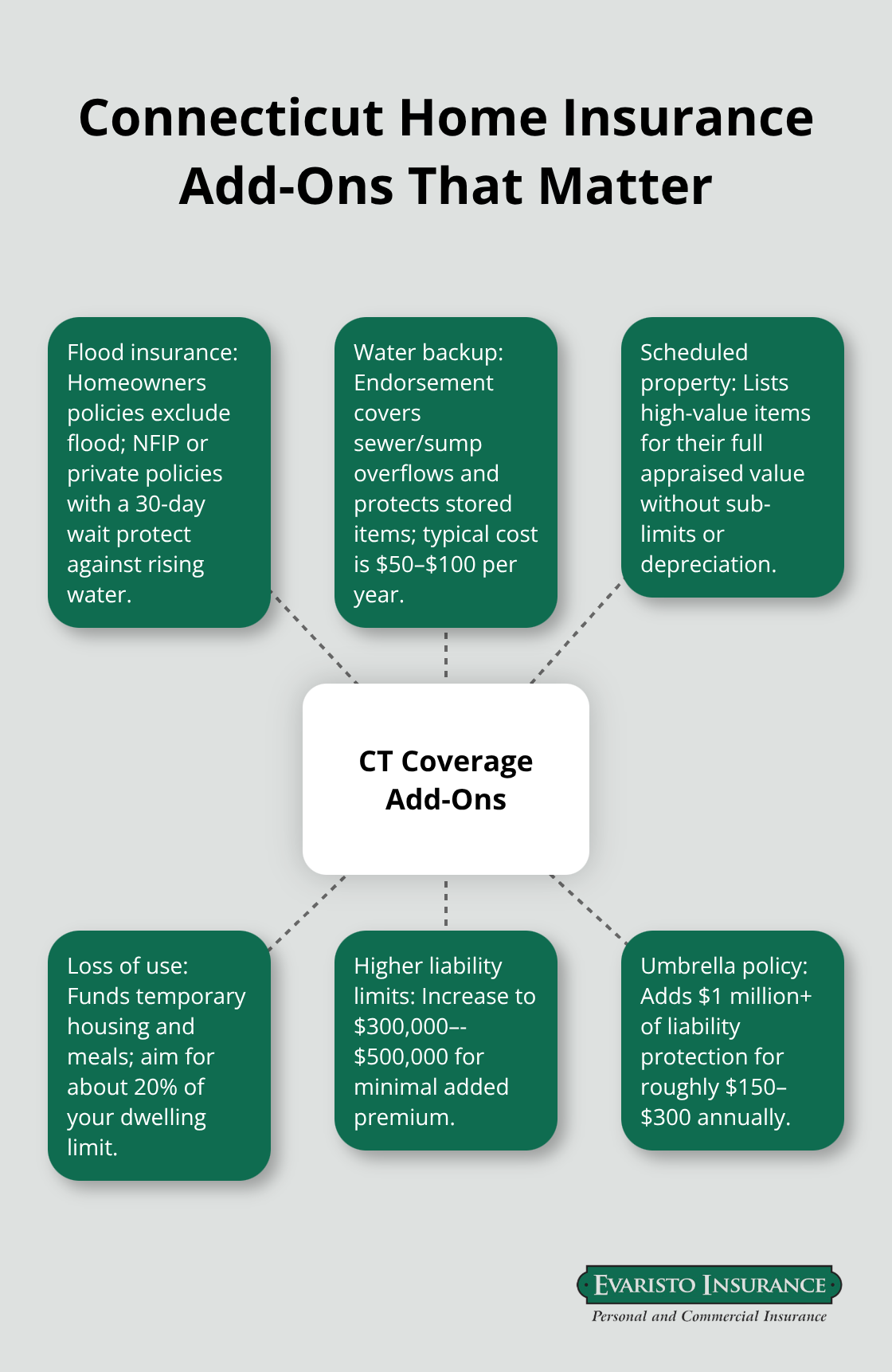

A scheduled personal property endorsement lists high-value items separately and covers them for their full appraised value without sub-limits or depreciation. You’ll need an appraisal or receipt for each item, but the protection is absolute. Water damage from burst pipes, ice dams, or sump pump failure also damages personal property, but only if the water damage itself is covered. Many policies exclude water damage from flooding or snowmelt, so a basement full of stored items receives no protection if water seeps in during spring thaw. Adding water backup coverage to your policy protects against sewage backups and sump pump overflow specifically. For items stored in basements or lower levels, this endorsement is worth its modest cost.

Liability Coverage for Injuries on Your Property

Your liability coverage protects you when someone is injured on your property or you accidentally damage someone else’s belongings. Connecticut homeowners policies typically include $100,000 in personal liability coverage, which sounds substantial until you consider a serious injury lawsuit. Medical bills for a hospitalized guest, lost wages, and pain-and-suffering awards can easily exceed $100,000. If you face a $250,000 judgment and your policy only covers $100,000, you’re personally responsible for the $150,000 difference. That’s when creditors can pursue your wages and assets.

Increasing your liability limit to $300,000 or $500,000 costs only $15–30 extra per year, making it one of the cheapest upgrades available. If you have significant assets or substantial income, an umbrella policy extends liability protection to $1 million or more at a cost of roughly $150–300 annually. Medical payments to others coverage, typically $1,000 per person, pays immediate medical bills for injuries on your property regardless of fault, which can prevent small incidents from becoming lawsuits. Connecticut homeowners should prioritize adequate liability limits because the cost is minimal compared to the financial exposure you face.

These personal property and liability protections form the backbone of your coverage, but they work best when paired with the additional coverages and optional add-ons that address Connecticut’s specific risks.

Additional Coverages and Optional Add-Ons

Water Damage and Flood Protection

Connecticut homeowners face three distinct risks that standard policies either exclude or undercover: water intrusion, high-value possessions, and temporary displacement after a loss. Flood damage alone costs Connecticut residents an average of $25,000 per incident according to FEMA data, yet standard homeowners policies exclude all flood damage. Water backup coverage protects against sewage overflow and sump pump failure during heavy storms, which damages basements and stored items regularly across the state.

Flood insurance through the National Flood Insurance Program requires a 30-day waiting period before coverage begins, so waiting until storm season arrives leaves you unprotected. Connecticut homeowners outside traditional flood zones often skip flood coverage, but floods occur outside mapped zones regularly, especially in areas with poor drainage or near streams that swell during heavy rain. A private flood policy costs roughly $500 to $1,200 annually depending on location and coverage limits, far less than a single flood loss. Water backup coverage adds $50 to $100 yearly to your homeowners policy and protects against the most common water damage claims in Connecticut.

Specialty Items and High-Value Possessions

A scheduled personal property endorsement lists high-value items separately and covers them for their full appraised value without sub-limits or depreciation. You’ll need an appraisal or receipt for each item, but the protection is absolute. Standard policies cap jewelry, art, and collectibles at $1,500 to $2,500 per item regardless of actual value. If you own an engagement ring worth $8,000 or collectible artwork valued at $10,000, that standard limit leaves you massively exposed. The scheduled endorsement eliminates this gap entirely.

Loss of Use and Additional Living Expenses

Loss of use coverage prevents financial catastrophe when you cannot live in your home during repairs. It pays for temporary housing, meals, and other living expenses while reconstruction happens, typically covering 20 percent of your dwelling limit. Connecticut’s most common natural disasters include floods, snowstorms, and windstorms, making this coverage a practical necessity rather than an optional extra. If you carry $300,000 in dwelling coverage, your loss of use should reach $60,000 minimum.

This amount covers roughly six months of temporary housing and living expenses, which matches typical reconstruction timelines for major damage.

Connecticut homeowners who skip these endorsements discover during claims that they’re significantly underprotected for the state’s actual hazards. The cost of adding water backup coverage, scheduling high-value items, and increasing loss of use protection remains modest compared to the financial exposure you face without them.

Final Thoughts

Your home insurance policy features determine whether you face financial catastrophe or solid protection when disaster strikes. Connecticut homeowners who calculate actual replacement cost, verify replacement cost coverage for both structure and contents, and add water backup protection avoid losses exceeding $50,000 after major claims. Schedule high-value items like jewelry separately, increase liability limits to $300,000 minimum, and ensure loss of use coverage reaches at least 20 percent of your dwelling limit to cover temporary housing during reconstruction.

Connecticut’s specific hazards demand specific protections that standard policies don’t automatically provide. Coastal properties require separate windstorm deductible planning, flood-prone areas need dedicated flood insurance despite the 30-day waiting period, and basements storing valuable items need water backup endorsements. Your policy review should address each of these gaps before disaster strikes rather than discovering them during a claim.

We at Evaristo Insurance work directly with Connecticut homeowners to review coverage, identify gaps, and implement the right endorsements that match your actual risks and budget. Contact our local offices in Ellington and West Hartford today to schedule a policy review and confirm your home insurance protection meets your family’s needs.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.