Landlord Insurance Claims Process Demystified And Streamlined

Filing a landlord insurance claim shouldn’t feel like navigating a maze. Most Connecticut landlords we work with at Evaristo Insurance find the process confusing because they don’t know what to expect at each stage.

This guide walks you through the landlord insurance claims process step by step, from the moment you report damage to when you receive your payout. You’ll learn how common claims are handled and what you can do right now to make everything faster and smoother.

What Happens When You File a Landlord Insurance Claim

The moment you discover damage to your rental property, time matters. Most landlords don’t realize that the first 24 hours set the tone for how quickly your claim moves forward. When you call your insurer, you provide your policy number, a detailed description of what happened, the date and time of the incident, and whether anyone was injured. The insurer assigns a claim number immediately-write this down and keep it accessible because you’ll reference it in every follow-up.

Document Everything Before Cleanup Starts

Documentation is not optional; it’s the foundation of your entire claim. Take photos and videos of all damage before you touch anything or start cleanup. Photograph wide shots that show the overall scope of damage, then close-ups of specific areas. If water damage occurred, capture wet spots, stains, and any visible mold growth. For theft or break-ins, photograph entry points, broken locks, and empty spaces where items were stored. This visual record prevents disputes later about what the damage actually looked like.

Connecticut landlords often make the mistake of cleaning up immediately to get tenants back into the unit faster, but this can hurt your claim because the insurer loses the chance to see the original condition. If you must make emergency repairs to prevent further damage-such as boarding up a broken window or stopping an active leak-document those repairs with photos and keep all receipts and contractor invoices. Your insurer will want to see what you spent to mitigate additional loss.

The Adjuster’s Inspection Determines Your Payout

Within a few days, an adjuster from your insurance company will contact you to schedule an inspection. This is not a conversation to rush through or delegate entirely to a property manager. The adjuster will visit the property, measure damage, assess repair costs, and determine whether the loss falls within your coverage.

Bring any maintenance records you have-this is where that detailed damages and repairs log pays off. If you’ve documented regular maintenance like roof inspections, plumbing checks, or electrical updates, show those records to the adjuster. Properties with strong maintenance histories typically receive faster approvals because the adjuster can rule out negligence or pre-existing conditions. If the damage is significant, the insurer may hire a third-party estimator or engineer to assess structural issues, especially for fire, wind, or water damage. This adds time to the process but increases accuracy.

Once the adjuster completes the inspection, they prepare a damage report and estimate repair costs. You’ll receive a copy showing what’s covered, what’s excluded, and the amount the insurer will pay. This is where understanding your policy exclusions matters. Wind damage is covered, but flood damage typically is not unless you have a separate flood rider. Theft is covered, but only up to your policy limits. Tenant-caused damage is usually covered, but intentional damage by the landlord is not.

Coverage Decisions Vary by Claim Complexity

Your insurer will make a coverage determination within 10 to 30 days in most cases, though complex claims involving multiple types of damage or disputed liability can take longer. If the insurer approves your claim, they send a settlement offer stating the amount they’ll pay. You can accept it, negotiate it, or request a formal review if you believe the estimate is too low.

Understanding which claims are most common helps you anticipate what information the adjuster will want. For wind damage, they’ll ask about roof condition and age. For water damage, they’ll want to know about your plumbing maintenance history. For fire, they’ll investigate the origin and cause. Have this information ready before the adjuster arrives.

What Happens If Your Claim Gets Denied

If your claim is denied or partially denied, the insurer must provide a written explanation of why. Connecticut law requires transparency here. If you disagree with the decision, you have the right to request an appraisal or appeal, though this adds weeks or months to the timeline. A local agent who understands Connecticut landlord-tenant law and insurance regulations can review the denial letter, spot errors, and advocate on your behalf-which is why the next section focuses on how to streamline your entire claims process from start to finish.

Common Landlord Insurance Claims and How They’re Handled

Tenant-Caused Water Damage and Property Loss

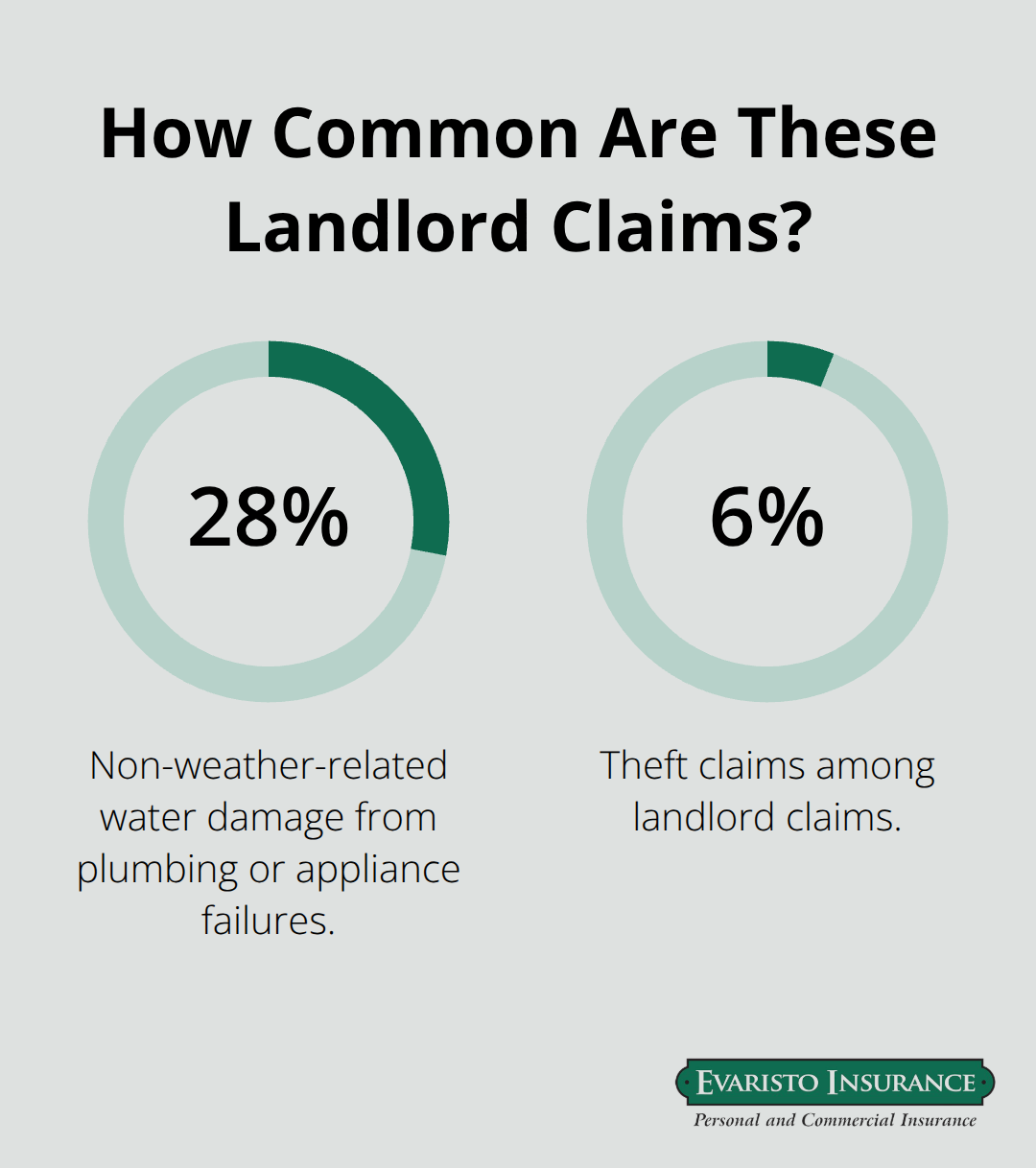

Tenant-caused damage represents the bulk of landlord claims, and it varies in how your policy handles it depending on whether negligence played a role. Non-weather-related water damage from plumbing or appliance failures accounts for nearly 28% of all home insurance claims, making it the second most common claim type after wind damage. When a tenant’s negligence causes this damage-say, they ignore a leaking dishwasher for weeks-your policy typically covers the structural repairs, but the tenant may owe the deductible or any portion exceeding your coverage limits.

The adjuster will scrutinize your maintenance records closely in these situations. If you documented regular plumbing inspections and the tenant failed to report the leak, the claim moves faster and the insurer is more likely to approve full coverage. If your records show no preventive maintenance history, the adjuster may question whether the damage was foreseeable and preventable, which can slow approval or reduce your payout. Theft claims make up 6% of landlord claims and require a police report before the insurer will process your claim. File that report immediately after discovering the loss, then provide the report number to your adjuster. Photograph the entry point, broken locks, and empty spaces where items were stored. Without the police report, many insurers will deny the claim outright.

Liability Claims from Tenant Injuries

Liability claims arise when someone is hurt on your property and sues you for damages. Your landlord policy includes liability coverage, typically $300,000 to $1,000,000 depending on your coverage limits, which protects you if a tenant or visitor is injured due to a condition you failed to maintain. A tenant slips on ice you didn’t salt, or someone is injured by a faulty railing-these fall under your liability coverage.

The claim process differs from property damage claims because it involves potential legal action. Report the injury to your insurer immediately, even if you don’t think you’re liable. Connecticut law holds landlords responsible for maintaining safe premises, defined in Connecticut General Statutes §47a-7, which means you must fix hazards promptly. If a tenant files a lawsuit, your insurer will assign a defense attorney and handle settlement negotiations on your behalf. In cases where litigation is brought against you and damages exceed your standard policy limits, additional coverage may protect your assets.

Loss of Rental Income Coverage

Loss of rental income coverage reimburses you when your property becomes uninhabitable due to a covered loss. Fire damage that forces you to close the unit, or severe water damage that requires extensive repairs, triggers this coverage. The insurer will pay your lost rent for the period the property was unrentable, up to your policy limit, usually calculated as a percentage of your annual rental income.

This coverage bridges the gap between when damage occurs and when you can re-rent the unit. Document your actual monthly rent and keep lease agreements accessible so the adjuster can verify your loss of income claim quickly. The faster you provide this documentation, the sooner you receive reimbursement for lost revenue during the repair period.

Understanding these three claim types prepares you to respond effectively when damage strikes. The next section shows you exactly how to streamline your entire claims process so you recover faster and spend less time managing the aftermath.

How to Streamline Your Claims Process

Document Your Property Before Damage Strikes

The difference between a claim that settles in two weeks and one that drags for two months starts with documentation you create before any loss occurs. Build a detailed property inventory with photos of every room, the roof condition, the plumbing system, electrical panels, and appliances. Store this digitally in cloud storage so you can access it from anywhere. When damage strikes, this baseline documentation proves what the property looked like before the incident, which eliminates disputes about pre-existing conditions. The Connecticut Department of Housing provides a Pre-Occupancy Walk-Through Checklist specifically designed for landlords to document condition before tenants move in; use this same approach for your overall property.

Maintain a separate damages and repairs log with dates, photos, contractor notes, and tenant communications. Include maintenance records like roof inspections, plumbing checks, and electrical updates. Properties with documented maintenance histories receive faster claim approvals because adjusters can rule out negligence or deferred maintenance as contributing factors. When the adjuster schedules an inspection, have all these records organized and ready. Adjusters spend 30 to 45 minutes on average at a property; if you force them to search for records, you waste time and create friction that can slow your claim.

Respond Fast to Every Adjuster Request

Speed matters after you file the claim. Respond to every request from your insurer within 24 hours, not 48 hours or a week. If the adjuster asks for additional photos, receipts, or a contractor estimate, send it the same day. Claims experts at major insurers report that responsiveness is the single biggest factor in claim resolution time. If your claim requires a third-party estimator for structural damage, provide access to the property on the first available date the estimator proposes; delaying access extends the timeline.

When you receive the adjuster’s estimate, review it carefully against your own contractor quotes. If the estimate seems low, gather competing bids from local contractors and submit them to your insurer within one week. Connecticut landlords who push back on low estimates with solid documentation typically negotiate higher settlements.

Work with an Agent Who Knows Connecticut Landlord Law

Your policy is only as valuable as your ability to enforce it when disputes arise. Work with an insurance agent who knows Connecticut landlord-tenant law, not just general insurance. An agent familiar with Connecticut General Statutes §47a-7 and §47a-16, which define landlord and tenant responsibilities, can review claim denials, spot coverage gaps in your policy, and advocate with your insurer when decisions seem unfair. When a claim gets denied or partially denied, having an agent who can challenge the decision on your behalf often means the difference between accepting a lowball payout and recovering what you’re owed. An independent agent (one who compares multiple carriers rather than representing a single company) gives you the advantage of leverage-if one insurer denies your claim unfairly, your agent can escalate the issue or explore coverage options with other carriers.

Final Thoughts

The landlord insurance claims process moves fastest when you document your property before damage strikes, respond immediately to adjuster requests, and understand your coverage limits and exclusions. Connecticut landlords who maintain detailed maintenance records, photograph damage within the first 24 hours, and provide complete documentation to their insurer typically see claims resolved within two to four weeks instead of two to four months. Local expertise makes a real difference when claims get complicated, since Connecticut landlord-tenant law is specific and your policy language matters.

An agent who understands both your coverage and the state’s regulations can spot coverage gaps, challenge unfair denials, and negotiate higher settlements on your behalf. We at Evaristo Insurance work with Connecticut landlords to navigate the claims process and protect their investments. Your next step is to review your current landlord policy and compare it against the claim types covered in this guide-do you have adequate liability limits, sufficient loss of rental income coverage, and no gaps in water damage or theft protection?

Contact Evaristo Insurance to discuss your landlord coverage and ensure you’re protected when damage strikes.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.