Connecticut Homeowners Insurance Comparison: Find the Best Value

Finding the right homeowners insurance in Connecticut means comparing coverage options, rates, and service quality. Your home is likely your biggest investment, and the right policy protects it without draining your budget.

At Evaristo Insurance, we help Connecticut homeowners navigate their options and find policies that match their needs and finances. This guide walks you through what matters most when comparing plans.

What Coverage and Limits Actually Protect Your Home

Connecticut homeowners must understand the difference between what a standard policy includes and what leaves gaps in protection. A standard homeowners policy covers your dwelling structure, personal property inside, liability if someone gets injured on your property, and additional living expenses if you cannot stay in your home temporarily. However, the limits you choose matter far more than most homeowners realize. Dwelling coverage limits in Connecticut should reflect that housing costs around $405,000 on average, 10% higher than the U.S. average. When comparing quotes, you will see options ranging from $300,000 to $500,000 in dwelling coverage. For Connecticut homes built after 2010, a $400,000 limit typically represents the minimum to avoid substantial out-of-pocket costs in a total loss.

How Your Deductible Shapes Your Premium and Protection

The deductible is your out-of-pocket cost when you file a claim, and it represents one of the few levers you control to manage your premium. Connecticut homeowners should view this strategically rather than simply picking the lowest premium option. If you file small claims regularly, you actually harm your long-term rates; the Connecticut Insurance Department advises withholding small claims to avoid premium increases. This means choosing a higher deductible makes sense if you can afford to absorb $1,000 or $2,500 out of pocket without financial stress. For homeowners with excellent emergency savings, a $2,500 deductible can reduce annual premiums significantly compared to a $500 deductible. The choice between a $1,000 deductible versus $500 can save you 15% to 20% annually, but it also means you will pay more when a claim happens. The Connecticut average homeowners insurance cost is roughly $1,244 annually, according to Bankrate data, but this varies widely based on deductible choice and other factors.

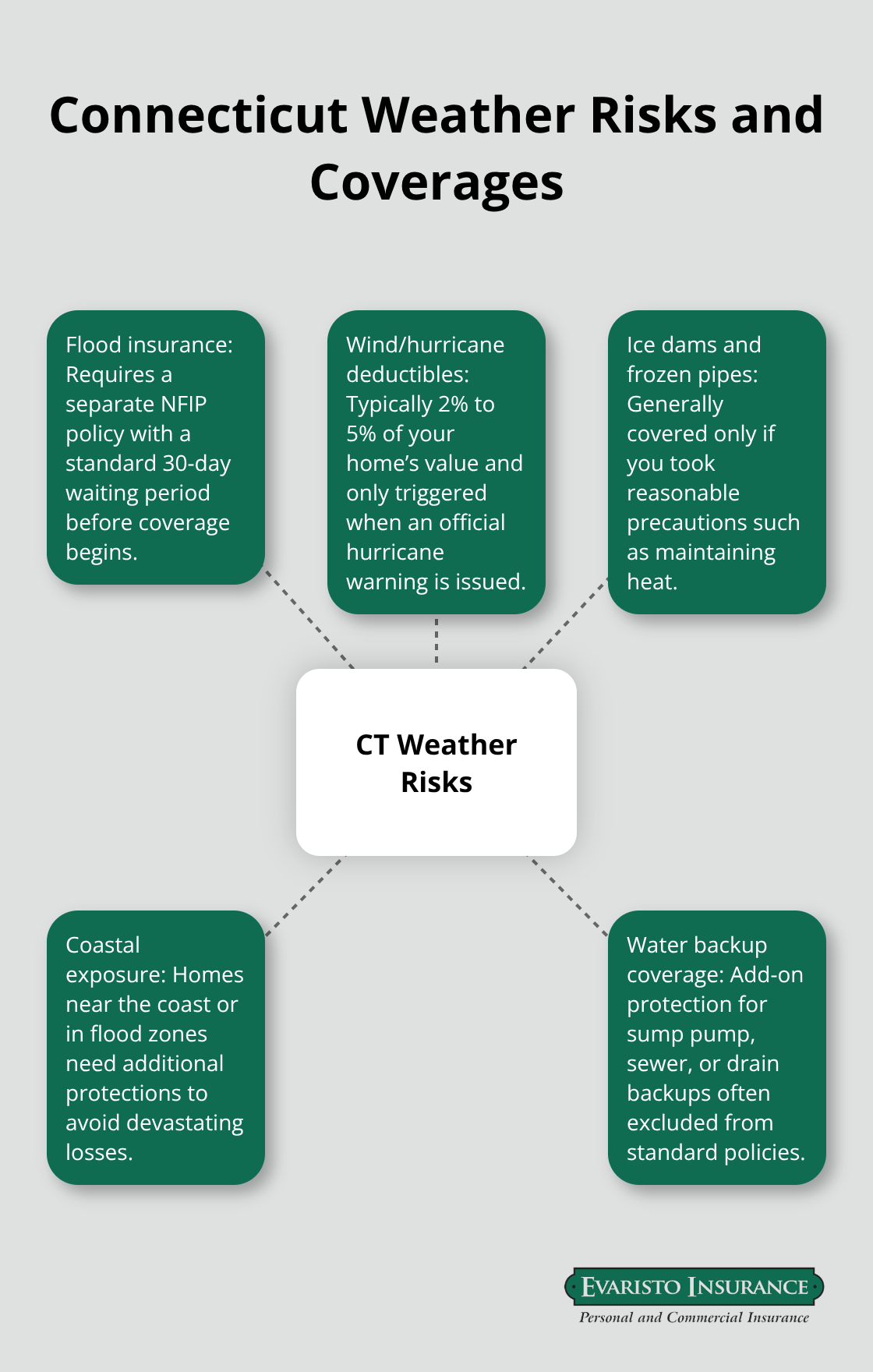

Connecticut Weather Creates Specific Coverage Needs

Connecticut’s climate creates risks that standard policies may not fully address. Winter storms cause ice dams and frozen pipe damage, which are technically covered under standard policies but only if you took reasonable precautions like maintaining heat in your home. Flooding from heavy rain or snowmelt is not covered by any standard homeowners policy in Connecticut; you need separate flood insurance through the National Flood Insurance Program, which has a standard 30-day waiting period before coverage begins. Wind and hurricane deductibles in Connecticut typically run 2% to 5% of your home’s value and only apply when an official hurricane warning is issued. If your home sits near the coast or in a flood zone, these additional protections are not optional-they are essential to avoid devastating financial loss.

Water Backup Coverage Prevents Costly Surprises

Water backup coverage represents the protection most Connecticut homeowners overlook until their sump pump fails during heavy rain. Standard policies do not cover water entering your home through drains, sewers, or sump pump failures, which occur increasingly often in Connecticut’s wet climate. Adding water backup coverage costs between $50 and $150 annually but prevents claims that can total $10,000 to $50,000. Similarly, if your roof is older than 20 years, some insurers apply additional scrutiny or require roof inspections before issuing or renewing coverage. Connecticut’s roofing costs rank among the highest in the nation due to labor and material costs, making roof condition a major factor in your premium.

Replacement Cost Coverage Protects Your Belongings

Replacement cost coverage means insurers pay what it costs to replace damaged items today rather than what you paid for them years ago-a significant difference for older belongings. Location creates dramatic premium differences across Connecticut as well. A homeowner in Hartford might pay $1,470 annually with Amica at a standard deductible, while someone in Bridgeport pays $1,950 for the same coverage. Understanding these regional variations helps you set realistic expectations when comparing quotes from different carriers and locations throughout the state.

What Actually Drives Your Connecticut Homeowners Insurance Premium

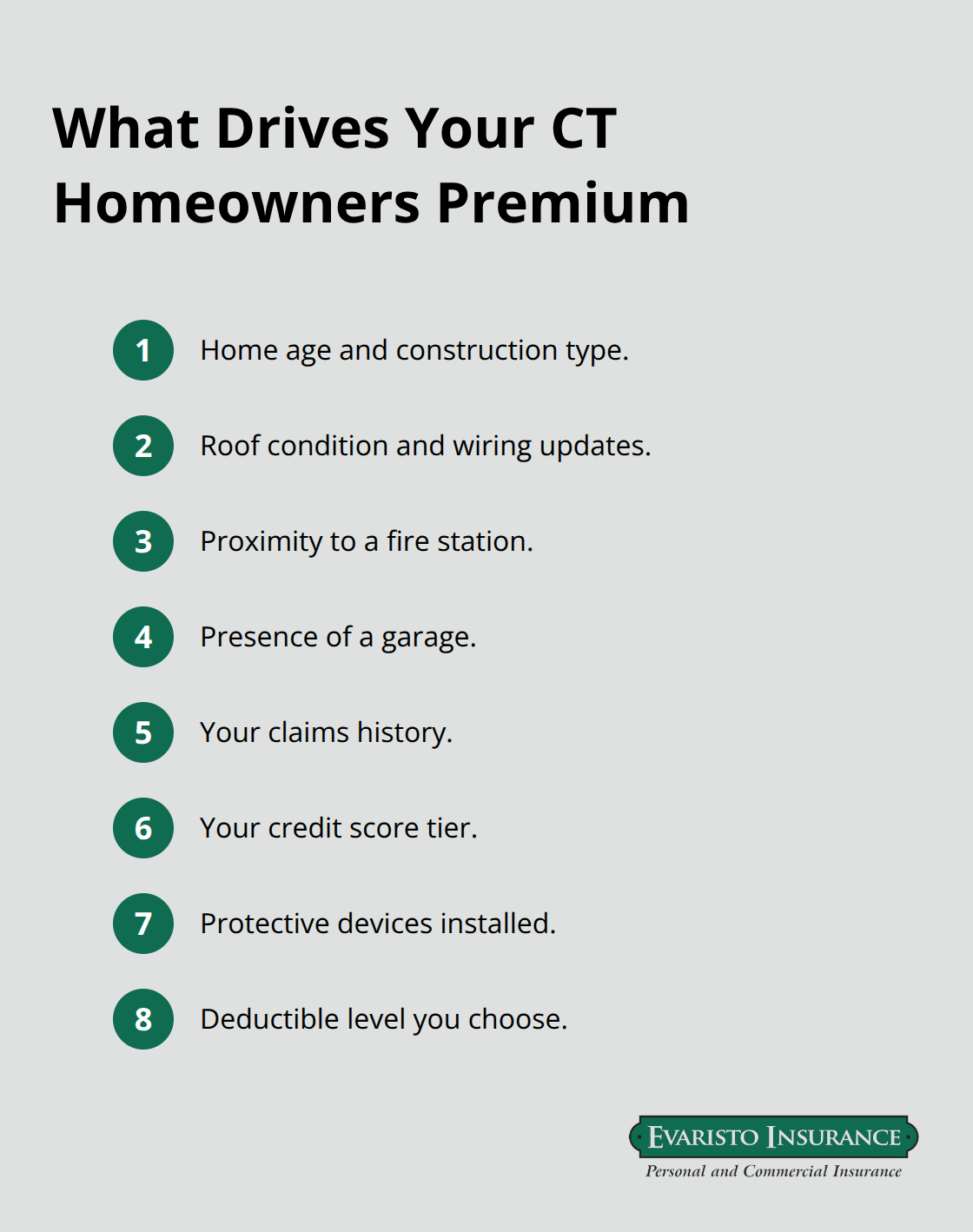

Your Connecticut homeowners insurance premium reflects far more than just your home’s value. The Connecticut Insurance Department identifies specific factors that directly impact what you pay: the age and construction type of your home, the condition of your roof and wiring, proximity to a fire station, whether you have a garage, and your claims history. A home built in 1950 with original wiring costs substantially more to insure than a 2015 home with updated electrical systems. Similarly, a roof that is 25 years old versus 10 years old can create a premium difference of 20% or more, since roof replacement costs in Connecticut have risen significantly due to labor shortages and material expenses. Your credit score matters more than most homeowners expect: someone with poor credit pays roughly $3,610 annually for coverage that costs only $1,870 for a homeowner with good credit, according to NerdWallet data-a 93% difference for the exact same home and coverage. Non-smokers receive preferential rates, and protective devices installed in your home such as deadbolt locks, smoke detectors, fire extinguishers, burglar alarm systems, and sprinkler systems all reduce your premium. Proximity to a fire station also influences your rate; homes closer to fire protection typically cost less to insure.

The deductible you choose remains the single most controllable factor: moving from a $500 deductible to $1,000 can reduce your annual premium by 15% to 20%, while a $2,500 deductible saves even more.

How Location Shapes What You Pay Across Connecticut

Regional variation across Connecticut creates dramatic premium differences that many homeowners overlook when shopping. Hartford homeowners pay approximately $1,470 annually with Amica for standard coverage, while residents in Bridgeport pay $1,950 for identical protection-a $480 annual difference driven entirely by location. USAA shows Hartford at roughly $769 annually and Bridgeport at $1,181 for a $300,000 dwelling, illustrating how coastal and urban areas command higher premiums. Connecticut’s statewide average homeowners insurance cost sits around $1,244 annually according to Bankrate, roughly 12% below the national average, but this figure masks significant local variation. Connecticut’s weather patterns, local property values, and state regulations demand coverage tailored to your specific situation.

Which Carriers Offer the Best Rates in Connecticut

Amica offers the cheapest average rates in Connecticut at approximately $1,083 annually for standard coverage, while USAA comes in second at roughly $1,193 annually but requires military affiliation. State Farm, Travelers, and Progressive all fall between $1,737 and $2,169 annually depending on dwelling coverage selected. Shopping across multiple carriers reveals substantial savings opportunities for your specific situation.

Discounts That Actually Reduce Your Annual Cost

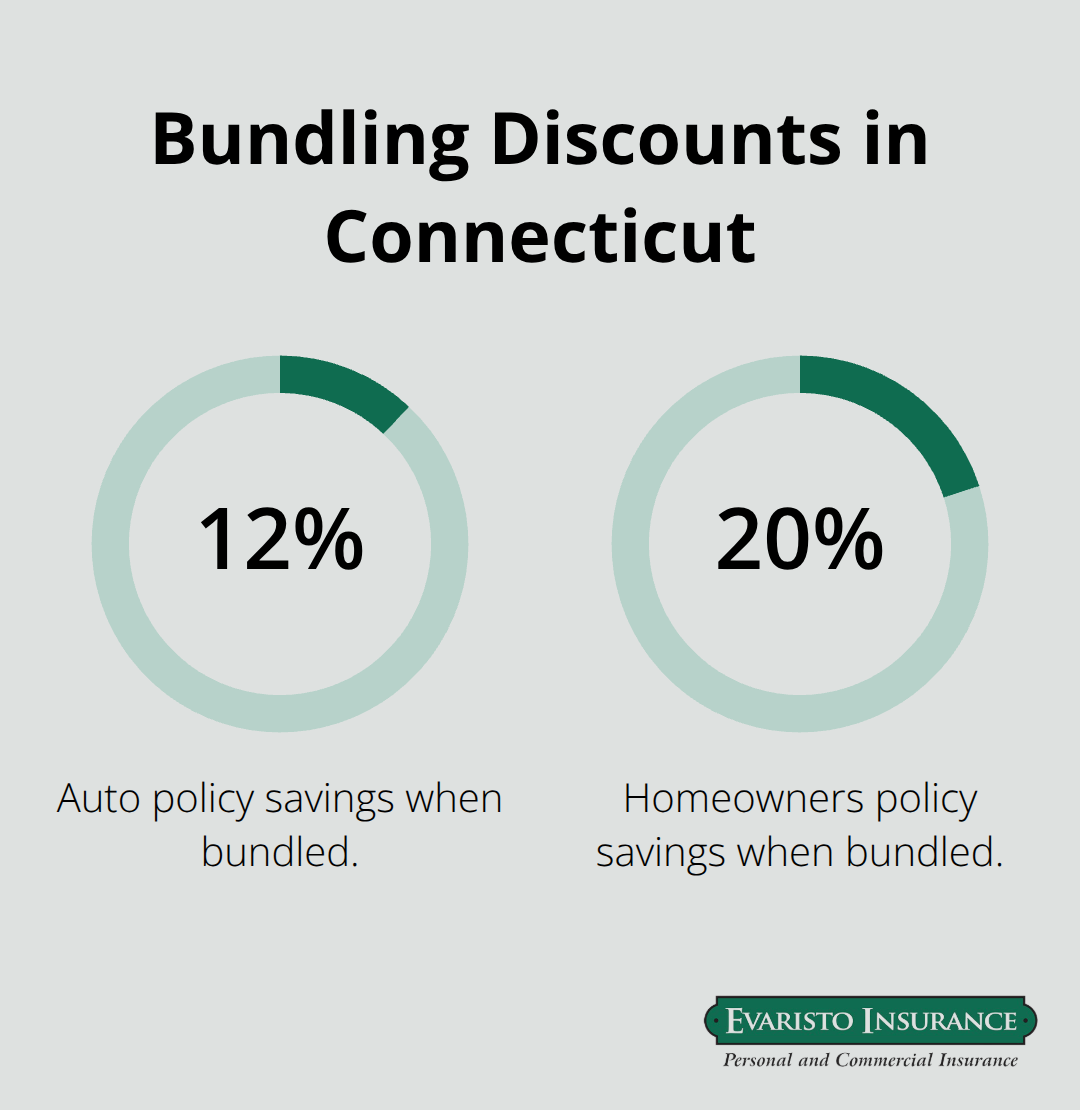

The most impactful discounts available to Connecticut homeowners include bundling auto and home insurance, which yields savings up to 12% on auto and 20% on homeowners coverage with providers like The Hartford AARP program, totaling roughly $963 in average bundled savings. Additional discounts flow from maintaining a claims-free history, installing wind mitigation features that qualify you for specific credit forms, adding monitored security systems or fire sprinkler protection, and purchasing a newly built or recently purchased home.

Loyalty discounts and discounts for paying your premium in full upfront also reduce costs at most carriers. The strategy that works best involves comparing quotes across at least three carriers using identical coverage amounts, then asking each carrier specifically what discounts apply to your situation based on your home’s condition, safety features, and claims history. These conversations with carriers often reveal savings you would otherwise miss.

Who Actually Delivers When You File a Claim

The difference between carriers in Connecticut extends far beyond their advertised rates. When you file a claim, you discover whether an insurer’s customer service promises translate into real action. Amica ranks highest among Connecticut insurers on the JD Power customer satisfaction scale and offers a dividend option that can return up to 20% of your annual premium, according to Bankrate data, but this benefit only matters if claims get handled smoothly. State Farm maintains an extensive local agent network across Connecticut yet shows relatively higher complaint activity with the National Association of Insurance Commissioners, suggesting that availability does not guarantee satisfaction. Travelers provides robust optional coverages like contents replacement cost and water backup, but customers report lower satisfaction scores compared to top-rated carriers.

How Financial Strength Protects Your Claim

Financial strength matters more than most homeowners realize because it determines whether a carrier can actually pay claims during catastrophic events. Chubb and The Andover Companies rank highest overall on NerdWallet’s Connecticut homeowners analysis, with Chubb designed explicitly for higher-value homes and The Andover Companies offering guaranteed replacement cost coverage for both structure and personal belongings. NJM provides standard coverage that can pay the full cost to rebuild your home even if it exceeds your dwelling limit, a notable feature during Connecticut’s rising construction costs. Openly offers guaranteed replacement cost coverage for the structure plus broad personal belongings coverage without breed restrictions on dogs, appealing to homeowners with diverse households.

What to Ask Carriers About Claims Handling

When comparing carriers, contact their claims departments directly and ask how long typical claims take to settle, whether they offer 24/7 reporting, and whether they assign a specific adjuster to your claim rather than rotating through multiple people. Connecticut homeowners who experience water damage or wind damage need carriers that respond quickly; delays of weeks or months create additional stress when your home is damaged. Cincinnati Insurance adds green upgrade endorsements and eco-friendly coverages through local independent agents, though online quotes are unavailable.

Local Expertise Versus National Coverage

Local expertise matters because Connecticut’s coastal risks, aging housing stock, and regional weather patterns demand carriers familiar with state-specific challenges. Carriers like USAA operate nationally but lack local knowledge, while regional specialists understand which neighborhoods command higher premiums and why certain coverage gaps matter more in Connecticut than elsewhere. An independent agency like Evaristo Insurance compares multiple top carriers to deliver tailored protection and hands-on customer advocacy, meaning you receive honest assessments of which carriers perform best for your specific situation rather than being locked into a single company. This approach handles the comparison work so you receive competitive pricing without the frustration of contacting dozens of insurers separately.

Final Thoughts

Connecticut homeowners insurance comparison reveals that the cheapest quote rarely delivers the best value. Your coverage needs depend on your home’s age, location, roof condition, and proximity to flood zones, while your deductible choice matters more than most homeowners realize because moving from $500 to $1,000 reduces premiums by 15% to 20% annually. Water backup coverage, flood insurance, and wind mitigation features address Connecticut-specific risks that standard policies ignore, and credit scores, protective devices like deadbolt locks and smoke detectors, plus claims history all shape your final premium.

Contact at least three insurers using identical coverage amounts and deductible levels so you compare apples to apples. Ask each carrier what discounts apply to your situation, whether bundling auto and home insurance saves money, and how their claims process actually works when you need it. Regional variation across Connecticut means Hartford premiums differ dramatically from Bridgeport or coastal areas, so local context matters when setting expectations.

Finding the right fit means balancing three factors: competitive pricing, strong claims handling, and local expertise. An independent agency can compare multiple top carriers to deliver tailored protection without locking you into a single company. Start by gathering quotes, then contact carriers directly about their claims process and available discounts to ensure your Connecticut home receives protection that matches both your budget and your actual risk profile.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!