Construction Contractor Insurance CT: Shielding Your Projects

Construction contractors in Connecticut face unique insurance challenges that go far beyond basic coverage. One miscalculation or gap in your construction contractor insurance CT can expose your business to significant financial risk.

At Evaristo Insurance, we’ve helped countless contractors across Connecticut build protection strategies tailored to their actual project needs. This guide walks you through the coverage types, state requirements, and provider selection process that matter most to your bottom line.

What Connecticut Contractors Actually Need to Insure

State Requirements Create a False Safety Net

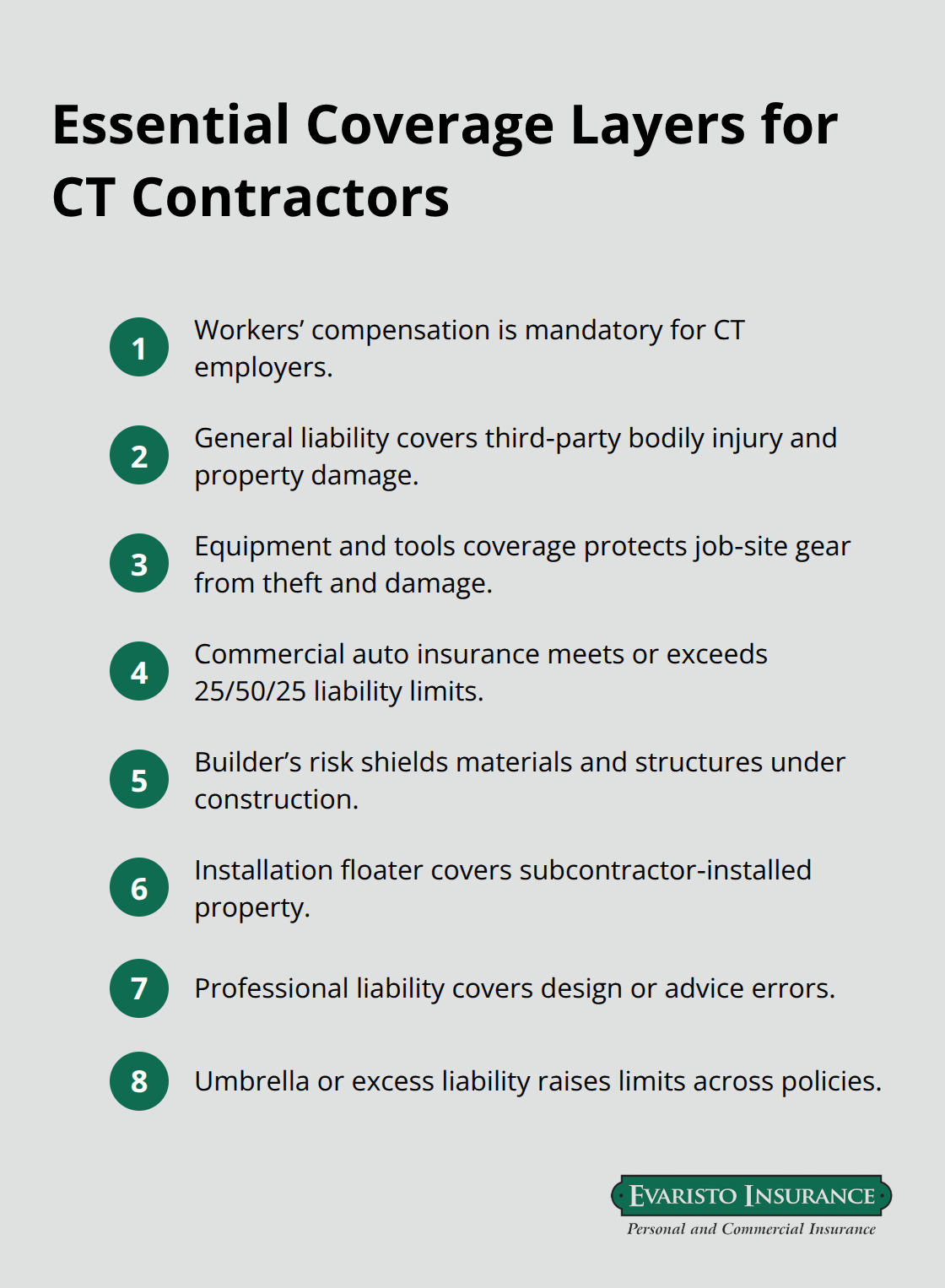

Connecticut’s construction licensing system creates a false sense of security for many contractors. The Connecticut Department of Consumer Protection requires major contractors to carry general liability insurance with the DCP listed as certificate holder, and this requirement alone has convinced some contractors that a basic GL policy handles all their risk. It doesn’t. The state mandate covers third-party bodily injury and property damage claims, but it ignores the financial devastation that follows when your equipment gets stolen from a job site, when a subcontractor fails to complete work, or when weather delays push your project past deadline. Connecticut contractors operating with only state-mandated coverage walk a tightrope over a canyon of unprotected losses.

Workers’ Compensation and Payroll Exposure

Workers’ compensation insurance is mandatory for any Connecticut construction business with employees, and the state enforces it aggressively. This coverage protects your crew when injuries occur on the job, but it also protects your business from lawsuits related to worker injuries. You cannot skip this requirement without facing serious penalties. General liability insurance averages around $1,351 annually for construction businesses, though a typical $1,000,000 policy runs closer to $69 monthly, depending on your crew size, claims history, and the types of projects you tackle. But here’s where most contractors miss the mark: they stop there.

Equipment, Vehicles, and Hidden Gaps

Tools and equipment coverage protects your saws, compressors, and power tools when thieves steal them or damage occurs on site-a real problem in Connecticut’s affluent communities where job sites attract criminal activity. Commercial auto insurance is equally overlooked, yet Connecticut’s minimum auto coverage requirements include 25/50/25 commercial auto liability limits, and vehicles used on job sites absolutely need this protection. The IAT Insurance Group headquarters renovation in Cheshire, completed in December 2022, demonstrates the complexity of modern Connecticut projects: 24,000 square feet across two floors with extensive glass walls, drainage upgrades, and exterior patio work. A project like that exposes you to glass breakage, water intrusion, slip-and-fall hazards, and third-party injuries-none of which a standalone GL policy adequately addresses.

Layered Protection for Complex Projects

You need builder’s risk coverage for the physical assets under construction, installation insurance for subcontractor work, and professional liability if your firm provides design services. The Hartford’s construction insurance solutions show what comprehensive programs actually look like: they layer general liability, excess liability, equipment coverage, and specialized options like pollution liability or delay-in-startup insurance depending on project scope. Contractors who treat insurance as a checkbox item rather than a strategic business decision consistently underestimate their exposure and overpay for gaps later. The right coverage strategy protects your assets, your crew, and your reputation-which is exactly why selecting the right insurance provider matters far more than most contractors realize.

Building the Coverage Your Connecticut Projects Actually Require

Workers’ Compensation Protects Your Crew and Your Business

Connecticut mandates workers’ compensation insurance for any contractor with employees, and the state enforces this requirement aggressively. Operating without it exposes you to fines, license suspension, and personal liability if a worker gets injured on the job. Workers’ comp covers medical expenses, rehabilitation, and lost wages for injured employees-protecting both your crew and your business from the financial fallout of workplace injuries. However, workers’ compensation alone leaves a critical gap: it doesn’t shield you from third-party claims when a subcontractor’s crew member damages a client’s property or injures a bystander. This is where general liability becomes your essential second layer.

General Liability Covers the Claims Workers’ Comp Doesn’t

General liability covers bodily injury and property damage claims from third parties-the homeowner whose driveway your equipment damaged, the neighbor injured when scaffolding fails, the client claiming your crew broke their windows during installation. Without this coverage, these claims come directly from your bank account. The IAT Insurance Group headquarters project in Cheshire demonstrates why this matters: with extensive glass walls and outdoor patio work completed in December 2022, the risk of property damage claims was substantial. General liability handled that exposure, but only because the contractor recognized the gap between state-mandated coverage and actual project risk.

Equipment and Job Site Coverage Protect Your Investments

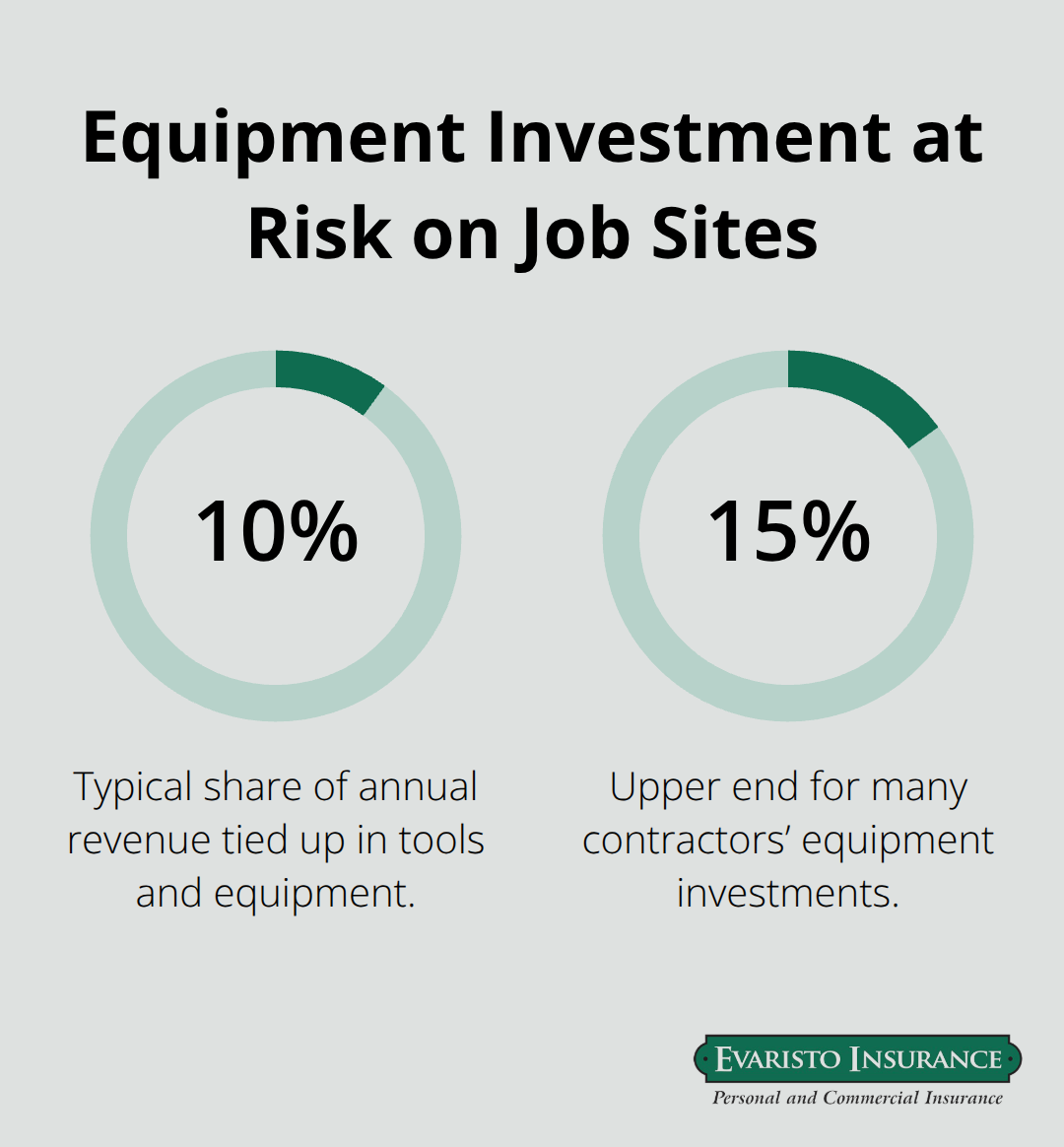

Tools, equipment, and job site coverage represents the third layer most Connecticut contractors skip until they experience a loss. Theft from job sites is a genuine problem in affluent Connecticut communities-compressors, power tools, and specialty equipment disappear regularly. Equipment coverage reimburses you for repairs or replacements when gear is stolen or damaged on site, protecting investments that often represent 10 to 15 percent of your annual revenue.

Commercial auto insurance for vehicles used on job sites is equally essential but frequently overlooked. Connecticut’s minimum commercial auto liability is 25/50/25, meaning $25,000 per person and $25,000 for property damage, but most contractors operating multiple projects need higher limits or umbrella insurance once primary coverage reaches its boundaries.

Builder’s Risk and Installation Insurance Close Critical Gaps

Builder’s risk coverage protects the physical assets under construction-materials, temporary structures, and installed equipment-from fire, theft, weather damage, and vandalism. Installation insurance specifically covers property that subcontractors install, closing a gap that general liability typically excludes. These coverages work together to create a comprehensive shield around your projects, preventing the overlaps and gaps that plague contractors who cobble together coverage from multiple carriers. The Hartford offers these coverages as integrated programs rather than scattered policies, which simplifies administration and reduces the risk of leaving exposures unprotected.

Tailoring Coverage to Your Specific Projects

Your project types, crew size, and claims history determine which combination of coverages actually protects your business. A residential renovation crew faces different exposures than a commercial interior fitout like the Cheshire project, which required protection against glass breakage, water intrusion, slip-and-fall hazards, and third-party injuries across a 24,000-square-foot space. Selecting the right insurance provider matters far more than most contractors realize because the right partner evaluates your specific risks rather than selling you policies you don’t need or leaving you exposed to risks you haven’t considered. This evaluation process-comparing carriers, assessing local expertise, and customizing policies-determines whether your coverage actually protects your bottom line or simply creates a false sense of security.

How to Choose the Right Contractor Insurance Provider in Connecticut

Price Comparisons Reveal Hidden Gaps in Coverage

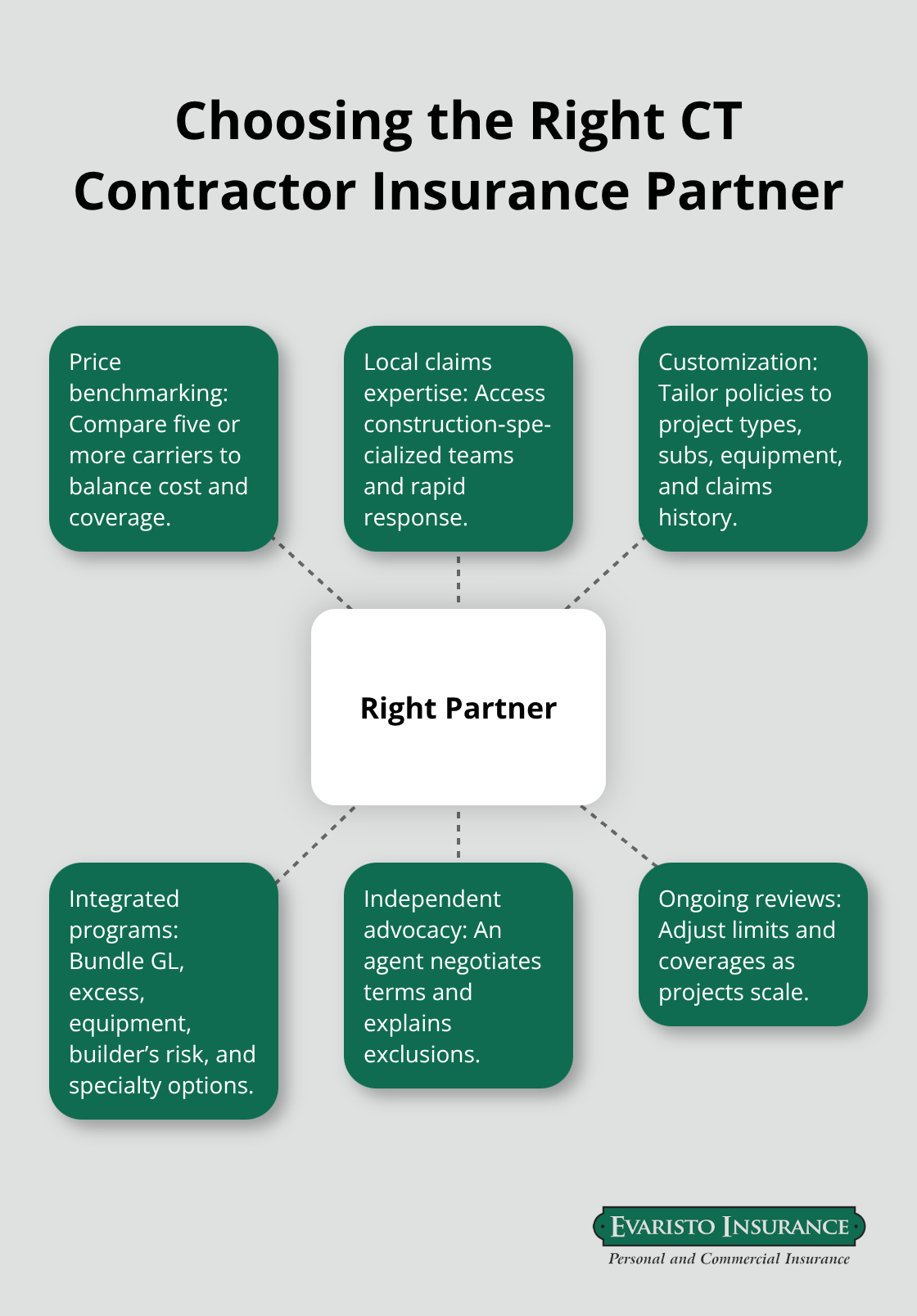

Comparing carriers on price alone guarantees you’ll overpay for the wrong coverage or underpay and face gaps when claims hit. Most Connecticut contractors request quotes from two or three carriers, pick the lowest number, and move forward-a decision that costs thousands when a claim reveals what the cheap policy actually excludes. A $1,000,000 general liability policy costs approximately $31 to $464 monthly for typical contractors, but that baseline shifts dramatically based on your crew size, project types, claims history, and the scope of work you handle. An agent comparing quotes from five carriers instead of two can identify $200 to $400 annual savings while simultaneously closing coverage gaps that cost far more than the premium difference. The Hartford offers construction-specific programs that integrate general liability, excess liability, equipment coverage, and specialized options like delay-in-startup insurance, demonstrating what comprehensive protection actually looks like. You need an independent agent who represents multiple top carriers and understands which combination of policies protects your specific operations rather than selling you standard packages that miss your actual exposures.

Local Expertise Transforms Claims Into Resolutions

Local expertise and claims support matter more than most contractors realize because the agent handling your quote rarely handles your claim. When a subcontractor gets injured on your job site or your equipment disappears from a locked trailer, you’re dealing with a claims team that either understands Connecticut construction operations or doesn’t. The Hartford’s specialized claims teams-including their Major Case Team and Rapid Response unit-demonstrate what happens when insurers invest in construction-specific expertise. Evaristo Insurance, a second-generation family-owned independent agency serving Connecticut since 1989, compares multiple top carriers to connect you with providers that offer this level of claims sophistication rather than forcing you to navigate the process alone. Your local agent advocates on your behalf, translating the technical language of your policy into real protection when you need it most.

Customizing Coverage to Match Your Actual Projects

Your policy should reflect the specific risks of your projects: a residential renovation crew faces different exposures than a 24,000-square-foot commercial interior fitout requiring protection against glass breakage, water intrusion, and third-party injuries across multiple floors. An agent who asks detailed questions about your project types, subcontractor relationships, equipment investments, and claims history will customize your policy stack accordingly. Carriers offer project-wrap options like OCIP or CCIP that centralize coverage on large builds, while smaller operations need flexible monoline policies with the ability to add coverage as projects expand.

This customization process-evaluating your actual exposures rather than selling standard packages-determines whether you’re protected strategically or simply paying premiums for policies that don’t fit your business. The right insurance partner identifies which combination of coverages actually shields your bottom line rather than creating a false sense of security.

Final Thoughts

Construction contractor insurance CT protects far more than your legal compliance-it protects your business from the financial devastation that follows when claims hit. State-mandated general liability coverage creates a false sense of security, workers’ compensation protects your crew but leaves third-party claims unshielded, and equipment theft from job sites happens regularly in affluent Connecticut communities. The right coverage strategy addresses all three gaps simultaneously, and the contractors who survive and grow in Connecticut’s competitive market build layered protection that matches their actual project exposures rather than buying the cheapest policy available.

Audit your current policies against the exposures outlined in this guide. Pull your general liability declarations page and verify that the Connecticut Department of Consumer Protection appears as certificate holder, check whether you carry workers’ compensation for all employees, confirm equipment coverage for tools and machinery, and verify commercial auto insurance for vehicles used on job sites. Identify which projects require builder’s risk or installation insurance, and determine whether your current carrier offers specialized coverages like delay-in-startup insurance or pollution liability that larger projects demand.

Working with a local Connecticut agent transforms this audit from a frustrating paperwork exercise into a strategic business decision. Evaristo Insurance compares multiple top carriers rather than pushing you toward one company’s standard package, understands Connecticut’s construction market, and identifies which combination of coverages actually protects your bottom line. Contact us today to build a protection strategy that delivers competitive pricing, comprehensive coverage, and hands-on advocacy when claims occur.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.