Homeowners Insurance Discounts Connecticut: Tips to Save on Your Policy

Connecticut homeowners pay some of the highest insurance premiums in the nation, with average annual costs exceeding $1,200. The good news is that homeowners insurance discounts in Connecticut are more accessible than most people realize.

At Evaristo Insurance, we help local homeowners identify and claim every discount available to them. This blog post walks you through the specific strategies that can meaningfully reduce your policy costs.

Where Connecticut Homeowners Find Real Savings

Bundle Auto and Home Policies Across Multiple Carriers

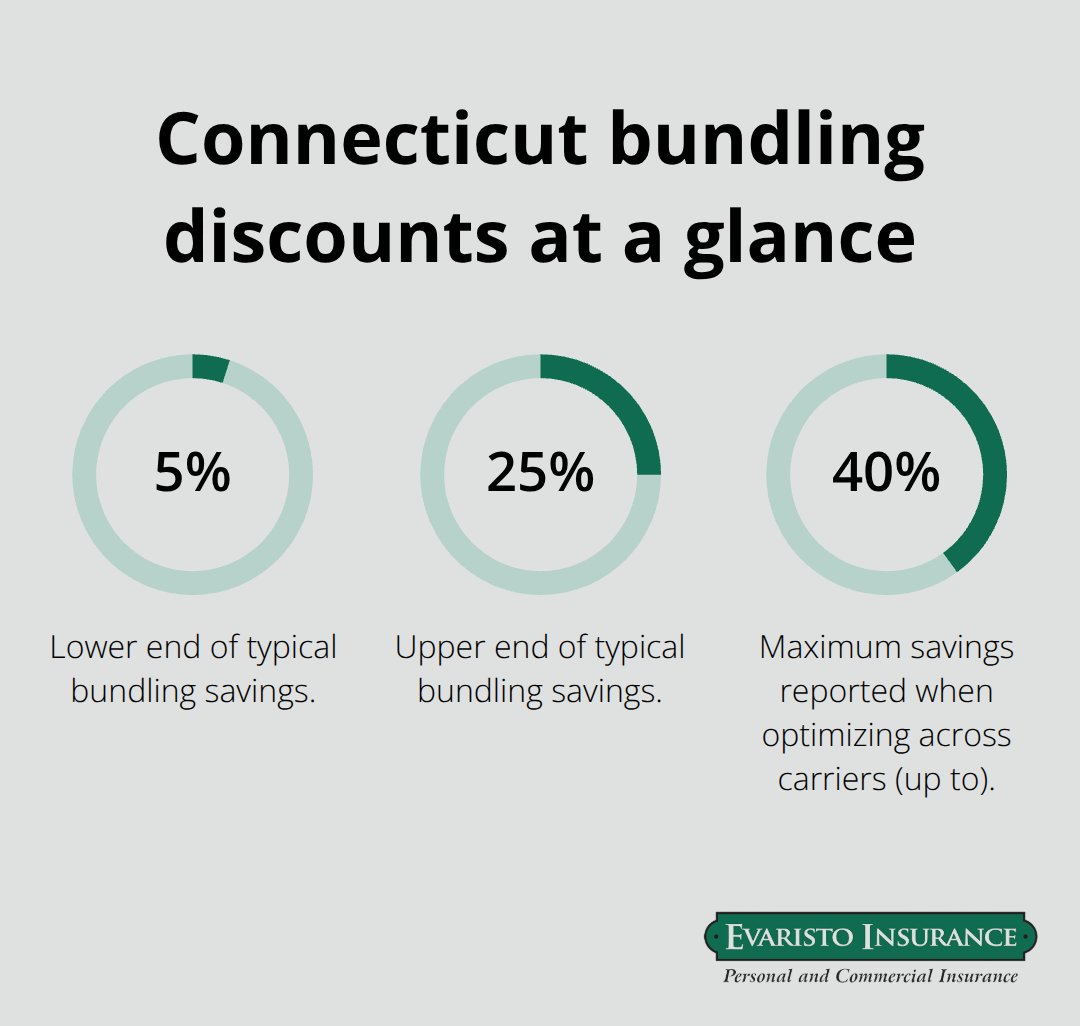

Bundling your auto and home policies cuts premiums by 5% to 25% on average. Most Connecticut homeowners leave money on the table because they assume they must stay with one carrier to capture the bundling discount. This assumption costs them hundreds annually. You can pair the cheapest home rate from one insurer with the best auto rate from another and still capture meaningful discounts through strategic bundling. For Connecticut residents, bundling discounts commonly range between 5% and 25%, with some customers saving up to 40% when they optimize across carriers.

The average Connecticut homeowner pays roughly $1,329 per year for homeowners insurance, so a 25% savings through smart bundling translates to over $330 annually. Start by collecting home quotes from multiple carriers, then collect auto quotes from different companies, then check if bundling options exist across combinations. This takes 30 minutes but often reveals savings that loyalty to a single carrier would never deliver.

Home Security and System Upgrades Reduce Your Rate

Safety features directly reduce your risk profile in an insurer’s eyes, which means they reduce your premium. Monitored burglar alarms and smoke detectors yield 15% to 20% savings in some cases, and dead-bolt locks qualify for additional discounts at many carriers. Upgrading the systems inside your home-electrical wiring, plumbing, and heating-signals to insurers that your property has lower fire and water damage risk. Historic Connecticut homes, common in areas like Litchfield County and throughout Fairfield County, often face higher premiums due to aging infrastructure, but modernizing these systems can open up better coverage options and potentially lower rates through specialized endorsements. If you’ve recently completed renovations or upgraded key systems, contact your insurer immediately-many don’t apply these discounts automatically.

Loyalty Discounts Exist, But Shopping Delivers Better Results

Staying with one insurer for several years does generate loyalty discounts, typically about 5% after 3 to 5 years and 10% after 6 or more years. However, this loyalty often masks rate creep. Carriers adjust pricing for long-standing customers just as they do for new ones, and the current Connecticut homeowners market is tight enough that actively shopping around every 2 to 3 years typically beats the loyalty discount you’d earn by staying put. A claims-free discount can reach up to 20% after several years without a claim, which is substantial, but this discount exists across carriers-you’re not locked into one company to claim it. The practical strategy involves reviewing quotes every 2 to 3 years, stacking discounts (pay-in-full discounts typically run 5% to 10%, quote-in-advance discounts reach about 15%), and comparing what multiple carriers actually offer you, not what they promise long-term customers.

Stack Multiple Discounts to Maximize Your Savings

Most Connecticut homeowners claim only one or two discounts when carriers offer five to eight simultaneously. Non-smoker status, paying your premium in full upfront, and obtaining quotes before your renewal date each yield separate savings. HOA or gated-community homes qualify for lower premiums due to added security and maintenance. Wind mitigation features (permanent storm shutters or impact-resistant glass) lower premiums in Connecticut when you install qualifying upgrades. The key is asking your insurer which discounts apply to your specific situation and which ones you haven’t yet claimed. Many carriers don’t apply discounts automatically, so you must actively request them. When you stack a 10% pay-in-full discount with a 15% quote-in-advance discount and a 5% safety-feature discount, you’ve reduced your premium by roughly 30% before loyalty or bundling even enters the picture. This approach requires more effort than accepting your renewal notice, but the financial payoff justifies the time investment.

Your Next Step: Compare Quotes and Identify Your Specific Discounts

The Connecticut homeowners insurance market offers meaningful savings opportunities for those who take action. Shopping around, upgrading your home’s systems, and stacking discounts can reduce your annual costs by hundreds of dollars. The question isn’t whether discounts exist in Connecticut-they do-but whether you’ve claimed all the ones available to your specific situation. As you move forward with optimizing your coverage, understanding how to evaluate quotes and select the right carrier becomes equally important.

How to Actually Lower Your Connecticut Homeowners Insurance Costs

Compare Quotes Across Multiple Carriers

Shopping for homeowners insurance in Connecticut requires a specific approach that most people get wrong. The instinct to contact your current carrier and ask about discounts wastes time and money. Connecticut insurers price policies individually based on their own risk models, meaning the quote you receive from State Farm differs significantly from what Vermont Mutual or USAA would offer for the identical coverage. According to Policygenius data updated in March 2026, Connecticut homeowners shopping across multiple carriers discover rate variations wide enough to justify the effort. Vermont Mutual often provides the lowest average rates in Connecticut at roughly $720 per year for standard coverage, while other carriers price the same home at $1,200 or higher. This isn’t about finding a better deal on the same policy-it’s about recognizing that each carrier evaluates your property differently.

Collect quotes from at least three carriers before making a decision. Request quotes for identical coverage limits across all companies so you can compare apples to apples. The National Association of Insurance Commissioners provides a tool to review state rate ranges and complaint histories, which helps you evaluate not just price but also how reliably each insurer pays claims when you need them.

Increase Your Deductible to Lower Monthly Payments

Raising your deductible stands as the single most direct way to lower your monthly payment, yet Connecticut homeowners often overlook this lever entirely. Increasing your deductible from $500 to $1,000 reduces premiums by roughly 10% to 25%, according to the Insurance Information Institute. For a homeowner currently paying $1,329 annually, this adjustment saves between $130 and $330 per year. The critical question is whether you can actually pay that deductible out-of-pocket if a claim occurs. If you lack $1,000 in emergency savings, a higher deductible creates financial stress rather than savings. However, if you maintain a solid emergency fund, moving to a $1,000 deductible makes financial sense.

Coastal Connecticut properties face additional considerations-windstorm deductibles typically range from 2% to 5% of dwelling coverage in coastal zones, meaning a homeowner with $400,000 in dwelling coverage might pay $8,000 to $20,000 out-of-pocket before windstorm coverage activates. Understanding these separate deductibles matters because they apply in addition to your standard deductible.

Maintain Your Home to Prevent Claims and Keep Rates Down

Home maintenance directly affects your rate renewal. Insurers increasingly use aerial imagery from companies like Nearmap to assess your property’s condition, looking for overhanging trees, roof damage, pooling water, and other risk features. A roof older than 20 years commonly triggers premium increases or non-renewal. If you’ve replaced your roof recently, inform your insurer immediately-this upgrade often reduces premiums because carriers view newer roofs as lower risk.

Updating electrical, plumbing, and heating systems signals reduced fire and water damage potential, and many carriers recognize these improvements through lower rates or better coverage options, particularly for older Connecticut homes where system upgrades are common. These upgrades matter most for historic properties throughout Fairfield County and Litchfield County, where aging infrastructure typically commands higher premiums. Taking photos and maintaining records of your home’s condition and recent improvements strengthens your position when you shop for new quotes or file a claim.

Why an Independent Agent Simplifies Your Connecticut Insurance Search

The Quote-Comparison Problem Most Homeowners Face

The quote-comparison strategy outlined above works, but it creates friction most Connecticut homeowners won’t tolerate. Collecting quotes from Vermont Mutual, State Farm, Amica, Farmers, USAA, and five other carriers requires contacting each company separately, providing identical information repeatedly, and then manually comparing coverage details across different policy structures. Most people abandon this process halfway through and accept their renewal notice instead. An independent agent compresses the entire comparison into a single conversation. You provide your information once. The agent collects quotes from multiple top carriers simultaneously and presents them side by side with identical coverage applied across all options. This eliminates the data-entry repetition and reveals rate differences instantly.

Discount Identification That Direct Insurers Miss

Carriers don’t advertise all available discounts prominently, and many don’t apply them automatically. When you contact an insurer directly about your renewal, their goal is to keep your business at your current rate, not to hunt for five additional discounts that would reduce your payment. An independent agent’s incentive structure inverts this dynamic. The agent earns commission regardless of which carrier you select, so the only motivation is to reduce your actual cost and improve your coverage. This means the agent actively asks about wind mitigation discounts for your storm shutters, security-system discounts for your monitored alarm, loyalty discounts for your claims-free history, payment discounts for paying in full, and quote-in-advance discounts for shopping early.

Coverage Limits and Rebuild Cost Verification

An independent agent also verifies that your coverage limits match your actual rebuild cost-not your home’s market value-which Connecticut homeowners frequently miscalculate. A homeowner in Fairfield County might have a $600,000 market-value home but only $450,000 in actual rebuild costs due to land value. Overinsuring costs you money; underinsuring leaves you exposed. An agent reviews this calculation explicitly rather than letting you guess.

Local Expertise in Connecticut’s Insurance Landscape

Connecticut’s insurance market presents unique challenges that require local knowledge. Coastal properties face windstorm deductibles ranging from 2% to 5% of dwelling coverage. Winter storms in northern areas like Litchfield County demand different coverage priorities than coastal hurricane exposure. Flood insurance availability and pricing vary by location, and Connecticut law from 2026 requires insurers to notify homeowners about flood insurance at policy issuance and renewal. An agent familiar with Connecticut’s specific risks, carrier practices, and regulatory requirements helps you navigate these complexities without trial and error.

Final Thoughts

Connecticut homeowners insurance discounts exist across every carrier in the state, but claiming them requires action. The strategies outlined in this post-bundling across carriers, stacking multiple discounts, raising your deductible, and maintaining your home-reduce premiums by hundreds annually when applied together. Shopping every 2 to 3 years beats loyalty to a single insurer, and upgrading your home’s systems signals lower risk to underwriters.

The friction point most Connecticut homeowners face is execution. Collecting quotes from multiple carriers, verifying coverage limits match rebuild costs, and identifying which discounts apply to your specific situation demands time and attention to detail. An independent agent compresses the entire quote-comparison process into a single conversation, identifies discounts your current carrier never mentioned, and verifies your coverage limits protect you adequately without overinsuring.

Contact Evaristo Insurance for a quote comparison and let us handle the complexity. Bring your current policy details, and we’ll collect quotes from multiple carriers, stack your available discounts, and present your options side by side. The difference between your current premium and what you’ll actually pay often justifies the conversation within minutes.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.