How to Get Cheap Auto Insurance Quotes Without Sacrificing Coverage

Finding cheap auto insurance quotes in Connecticut doesn’t mean settling for bare-bones coverage. We at Evaristo Insurance know that affordability and protection aren’t mutually exclusive.

This guide walks you through the exact strategies that help Connecticut drivers cut costs while keeping the coverage they actually need.

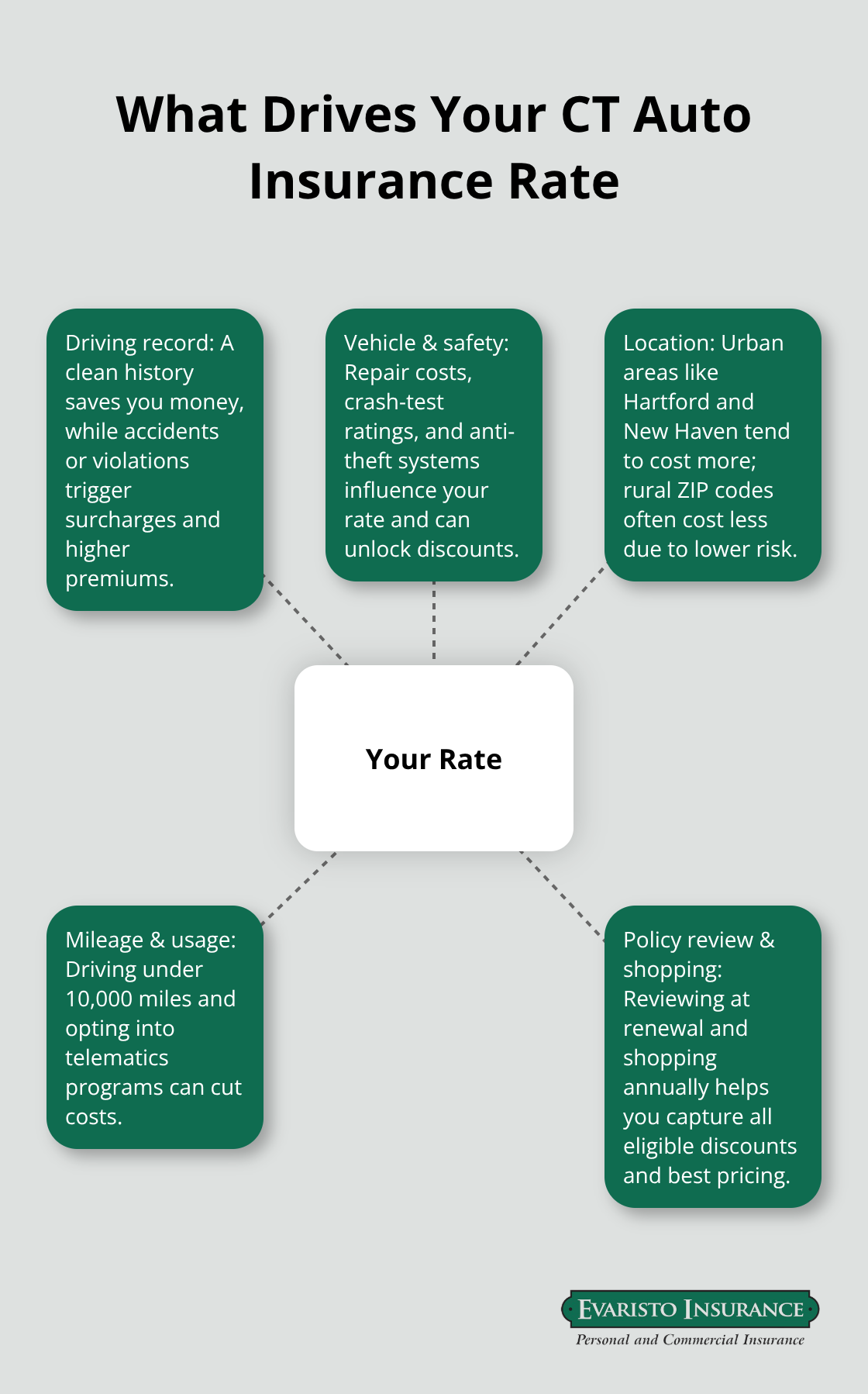

What Really Drives Your Connecticut Auto Insurance Rate

Your Driving Record Sets the Foundation

Your driving record is the single biggest factor insurers examine, and Connecticut data backs this up. The Insurance Research Council reports that uninsured motorist rates have declined significantly over the past decade. A clean driving history-no accidents, no violations-saves you hundreds annually compared to drivers with claims on file. One accident or moving violation increases your premium by 20% to 40% depending on severity. Insurers pull your Motor Vehicle Record before quoting, so any incident appears immediately.

If you have violations, some insurers offer accident forgiveness programs or discounts for defensive driving courses approved by Connecticut’s DMV. An approved course like AARP Smart Driver or IMPROV online lowers your rate, especially if you are 60 or older. Connecticut law mandates at least a 5% discount for seniors who complete an approved course, though some carriers offer more.

Vehicle Type and Safety Features Impact Your Quote

Your vehicle type matters significantly because repair costs directly affect what insurers charge. A Honda Civic costs less to insure than a BMW because replacement parts and labor are cheaper. Safety features also factor in; vehicles with strong crash test ratings and anti-theft systems qualify for discounts. An anti-theft device installed on your vehicle can help lower your premium substantially.

Location and Mileage Control What You Pay

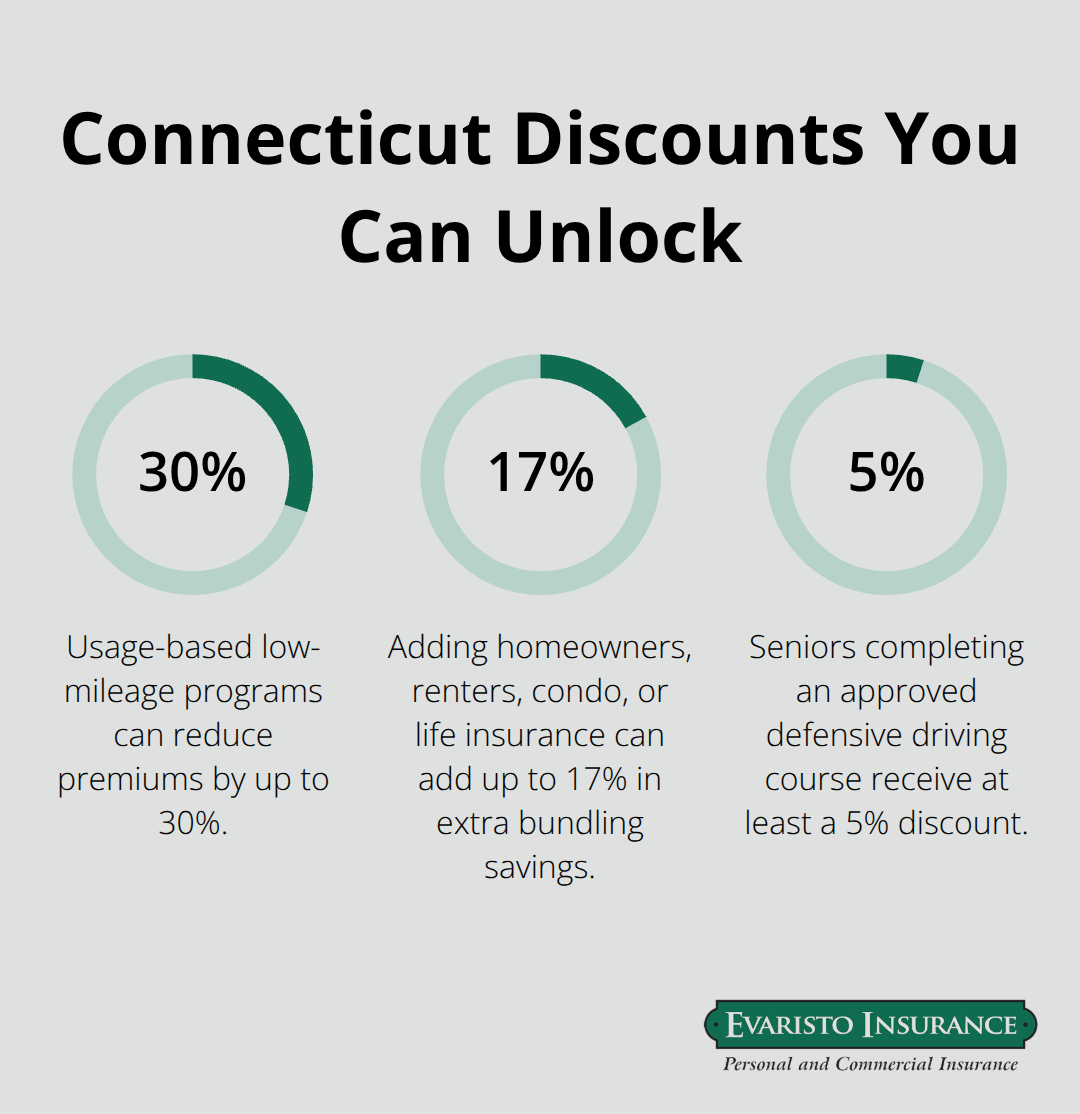

Your location in Connecticut influences rates more than many drivers realize. Urban areas like Hartford and New Haven typically have higher rates due to increased accident and theft frequency, while rural zones often cost less. Annual mileage is another concrete lever you control. If you drive under 10,000 miles yearly, mention this to your insurer-usage-based programs like Progressive’s Snapshot reward low-mileage drivers with discounts up to 30%.

The Connecticut Department of Insurance emphasizes reviewing your policy at every renewal and shopping around yearly to confirm you receive all eligible discounts and the best price for your specific situation. These three factors-your record, your vehicle, and how you use it-form the foundation of your quote. Understanding them positions you to take action on the strategies that actually work.

How to Cut Your Connecticut Premiums Without Cutting Coverage

Bundle Your Policies for Immediate Savings

Bundling your auto policy with home or renters insurance is the fastest way to lower your quote, and Connecticut carriers reward this strategy heavily. Bundle your policies can save you up to $1,429 when combining auto and home insurance, with potential additional savings of up to 17% when adding homeowners, renters, condo, or life insurance. When you request quotes, always ask insurers what bundling discounts they offer before comparing final numbers-some carriers bundle more aggressively than others. Geico, State Farm, and Progressive all emphasize bundling in their Connecticut offerings, so getting quotes from at least three carriers lets you see which one values your multi-policy business most. The Connecticut Department of Insurance specifically recommends bundling as a cost-reduction strategy, and it works because insurers view bundled customers as lower-risk and more loyal.

Raise Your Deductible Strategically

Your deductible is the out-of-pocket amount you pay when filing a claim, and raising it directly lowers your monthly premium. Moving from a $500 deductible to $1,000 typically reduces your premium by 15% to 25%, depending on your insurer and driving history. The catch is straightforward: you must have $1,000 cash available if you cause an accident. This strategy works best if you have an emergency fund and drive cautiously. Connecticut drivers with clean records and low annual mileage benefit most from higher deductibles because they file fewer claims.

Qualify for Low-Mileage and Safety Discounts

Low-mileage drivers also qualify for specific discounts that many overlook-if you drive under 10,000 miles yearly, Progressive’s Snapshot program and similar usage-based tools can cut rates an additional 10% to 30%. Anti-theft devices installed on your vehicle unlock another discount tier with most carriers. When requesting quotes, mention all eligible discounts explicitly: anti-theft features, low mileage, multi-vehicle discounts if you insure more than one car, and any approved defensive driving courses you have completed.

Connecticut carriers are required to offer these discounts, but they won’t apply them unless you ask.

These three levers-bundling, deductible adjustment, and discount activation-work together to shrink your premium substantially. The next step involves comparing those reduced quotes across multiple carriers to confirm you’ve found the best rate for your actual coverage needs.

How to Compare Quotes and Spot Real Coverage Match

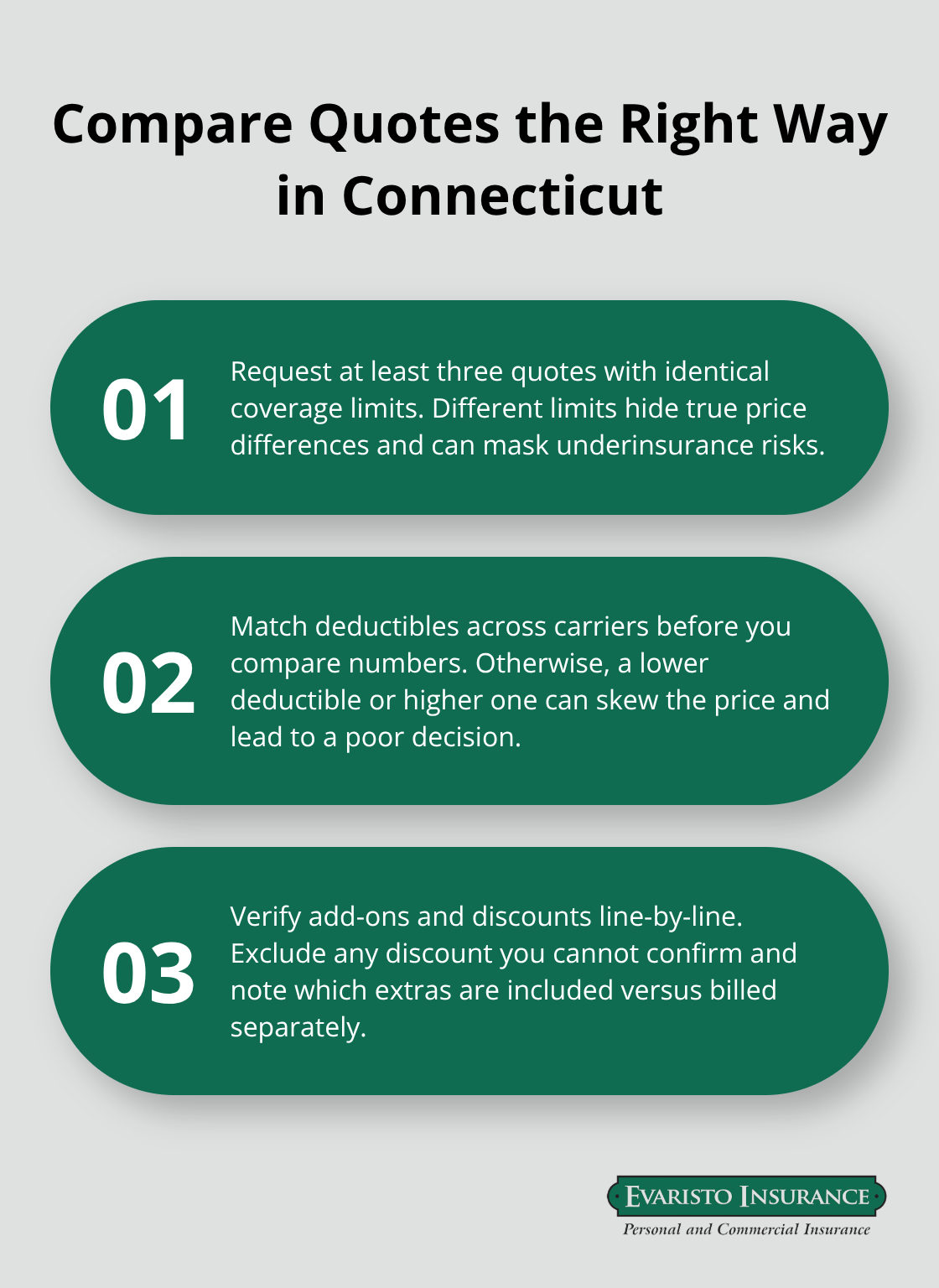

Request Quotes with Identical Coverage Limits

Three quotes from different carriers is non-negotiable if you want the best Connecticut rate, but most drivers compare them incorrectly. They request quotes with different coverage levels, different deductibles, and different add-ons, then pick the lowest number. That approach guarantees you’ll miss actual savings or accidentally cut coverage you need. The Connecticut Department of Insurance recommends shopping around yearly, but only when you compare identical protection across carriers.

Start by deciding what coverage you actually want. Connecticut’s minimum requirements are $25,000 per person and $50,000 per accident for bodily injury liability and $25,000 for property damage, but professional guidance commonly suggests at least $100,000 per person and $300,000 per accident for bodily injury to protect your assets in a serious crash. Once you’ve decided on limits, request quotes from at least three major Connecticut carriers with those exact same limits.

Match Deductibles Before You Compare Numbers

When you call Geico, State Farm, and Progressive with the same bodily injury, property damage, collision, and comprehensive limits, the differences in their quotes reflect real pricing variations, not coverage gaps. Write down each quote’s deductibles too. If one insurer quotes you with a 500 deductible and another with 1,000, adjust them to match before comparing final numbers.

The Connecticut Department of Insurance emphasizes that sample premiums vary widely by ZIP code, driving history, credit, vehicle, and coverage choices, so your actual quotes will differ from published averages. U.S. News data shows Geico averages 1,272 annually in Connecticut while Amica runs 2,372 and Progressive sits at 2,992, but these are just benchmarks for typical profiles.

Verify What Each Quote Includes and Excludes

Review what each quote actually includes and excludes before deciding. Some carriers bundle roadside assistance, rental car reimbursement, and medical payments into their base quote while others charge extra. Progressive’s Snapshot program and State Farm’s usage-based options appear in their quotes but only if you ask about them.

Ask each carrier explicitly what discounts they’ve applied to your quote and what discounts you might still qualify for. Many Connecticut drivers miss anti-theft discounts, good driver discounts, or multi-car discounts because they don’t ask. When comparing, exclude any discount you can’t verify you’ll receive.

Check Customer Service Before You Bind Coverage

Once you have three comparable quotes with identical coverage, deductibles, and confirmed discounts, the choice becomes straightforward. The lowest quote with the coverage you need wins. But verify that insurer’s customer service reputation before binding coverage. Connecticut drivers report varying experiences with claims handling and responsiveness, so a quote that’s 50 dollars cheaper means nothing if you wait weeks for claim approval. Check complaint ratios through the National Association of Insurance Commissioners before finalizing your choice. This approach takes an hour but locks in real savings without gambling on coverage adequacy.

Final Thoughts

Finding cheap auto insurance quotes in Connecticut requires three concrete actions: understanding what drives your rate, activating every discount available, and comparing identical coverage across at least three carriers. Your driving record, vehicle type, location, and mileage form the foundation of your premium, while bundling policies, raising your deductible strategically, and qualifying for low-mileage or safety discounts shrink that number substantially. When you request quotes, match your coverage limits and deductibles exactly so you compare real pricing differences, not coverage gaps.

Working with a local agent saves you hours of phone calls and quote requests while uncovering discounts you’d miss on your own. An independent agency compares multiple carriers simultaneously and knows which insurers value bundling most aggressively in your ZIP code, which ones offer the best accident forgiveness programs, and which carriers handle claims fastest when you need them. They also adjust your coverage as your life changes-something that matters far more than most Connecticut drivers realize.

Your next step is straightforward: gather your current policy details, decide what coverage limits protect your assets adequately, and request cheap auto insurance quotes from at least three carriers with identical limits. If you prefer guidance through that process, contact Evaristo Insurance to speak with a local agent who understands Connecticut’s specific rates and requirements. The difference between shopping alone and working with someone who knows the market often exceeds the agent’s value many times over.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.