Homeowners Policy Explained: A Clear Guide To Your Coverage

Homeowners insurance protects your biggest investment, but many Connecticut homeowners don’t fully understand what their policy actually covers. The gap between what you think you’re protected against and what you actually are can be costly.

At Evaristo Insurance, we’ve helped countless homeowners in Connecticut navigate their coverage options. This guide breaks down the essentials so you can make informed decisions about your protection.

What Your Homeowners Policy Actually Covers

Dwelling Coverage: Protecting Your Home’s Structure

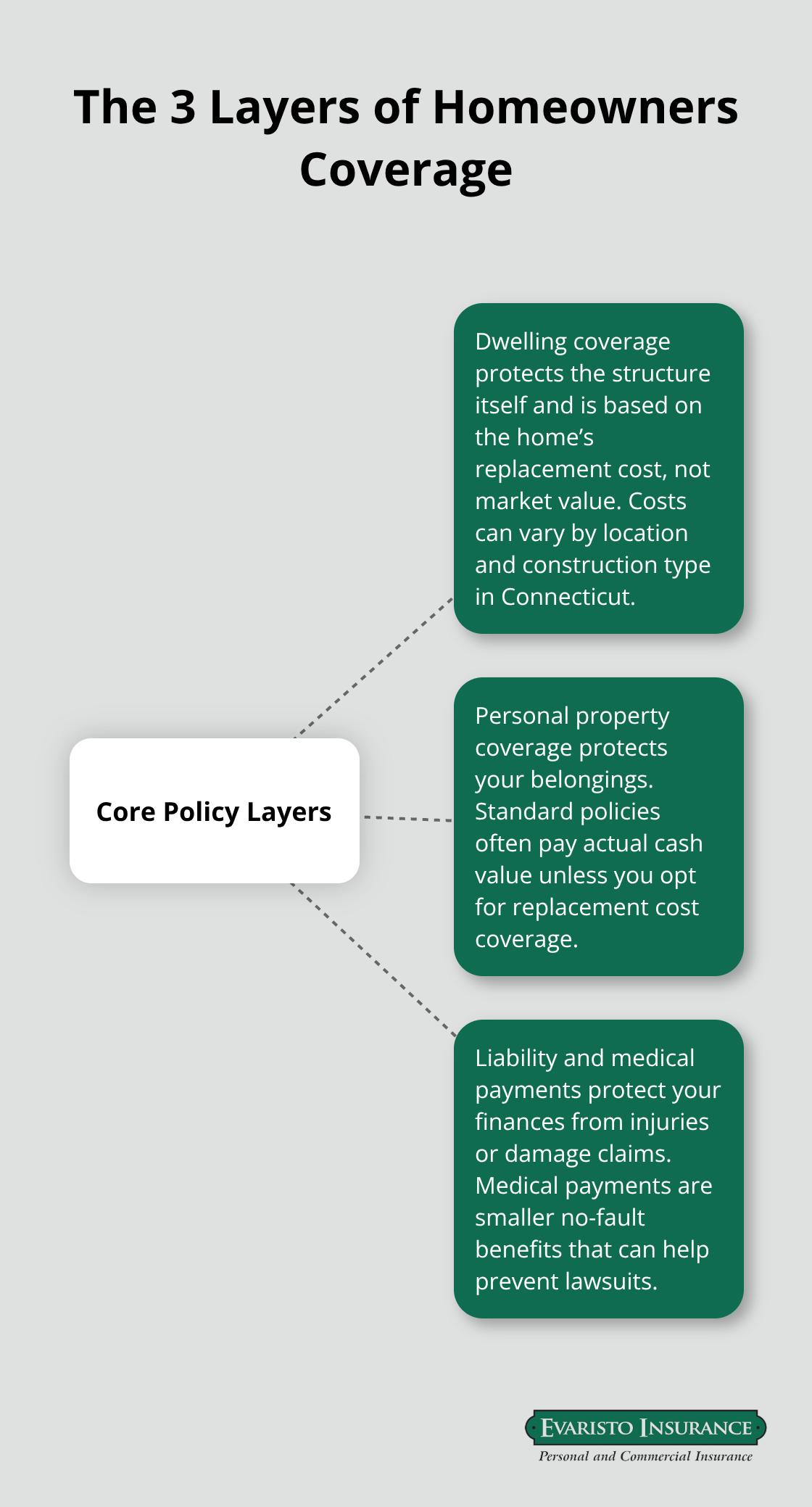

Your homeowners policy has three core protection layers, and each one works differently with real limits you need to understand. Dwelling coverage protects the structure itself-your walls, roof, foundation, and built-in systems like plumbing and electrical wiring. This forms the foundation of your policy and is calculated based on your home’s replacement cost, not its market value.

Connecticut homeowners with a $400,000 dwelling typically pay around $2,019 annually according to U.S. News & World Report data, though this varies significantly by location and construction type. If you live in Fairfield County near the coast, you’ll pay roughly $3,188 per year because proximity to water increases wind and hurricane risk. Inland Hartford County homes run closer to $2,492 annually.

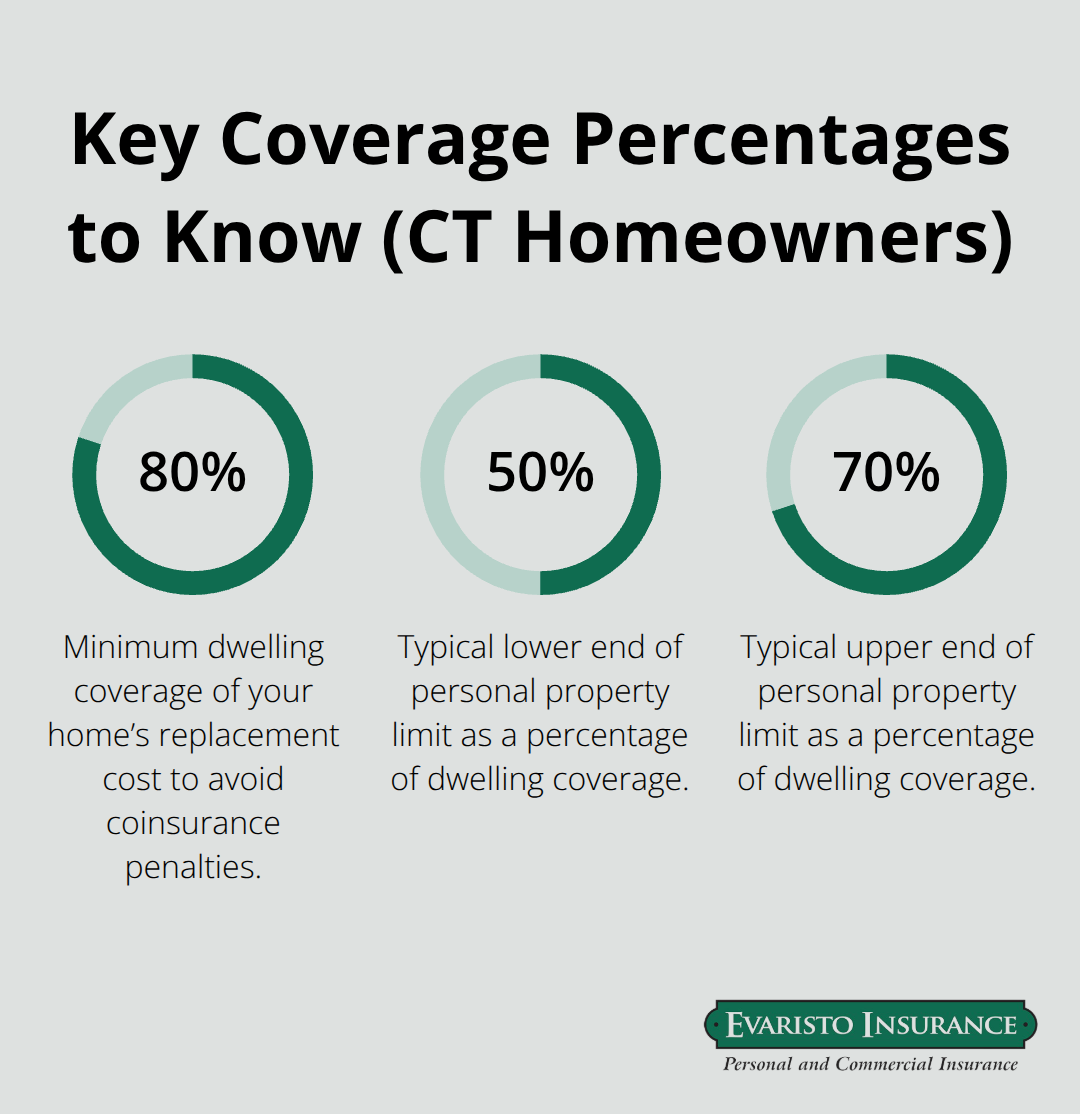

The detail most homeowners miss: you need dwelling coverage equal to at least 80 percent of your home’s replacement cost to avoid coinsurance penalties. If your home costs $300,000 to rebuild but you only insure it for $200,000, you’ll absorb a portion of repair costs even on covered losses. This directly impacts your out-of-pocket expenses after a claim.

Personal Property Coverage: Protecting Your Belongings

Personal property coverage protects your belongings inside the home, from furniture to electronics to clothing. Standard policies cover these items at actual cash value, meaning depreciation reduces what you receive. A five-year-old television worth $1,200 new might only pay out $400. Replacement cost coverage eliminates depreciation but costs more in premiums-a trade-off worth evaluating if you own newer or high-value items.

Liability and Medical Payments: Your Financial Protection

Liability coverage protects your finances if someone gets injured on your property or you accidentally damage someone else’s property. Connecticut standard policies typically include $100,000 to $300,000 in liability limits, though your actual assets should determine your chosen limit. If you own significant investments or rental property, higher liability limits make sense because they protect those assets if you’re sued. Medical payments coverage is separate and smaller-usually $1,000 to $5,000-covering guest injuries regardless of fault, which can prevent minor incidents from becoming lawsuits.

Comparing Coverage Across Carriers

Request quotes with consistent dwelling coverage and deductible amounts across multiple insurers so you’re comparing actual protection levels, not just prices. This approach reveals which carriers offer genuine value versus those simply undercutting on coverage. Understanding these three layers positions you to evaluate what gaps exist in your current protection-and that’s where exclusions become critical to address.

What Your Policy Won’t Protect

Your homeowners policy has strict boundaries, and the exclusions matter more than you might think. Water damage sits at the top of the exclusion list, and this distinction confuses most Connecticut homeowners. Standard policies cover sudden water events like a burst pipe inside your walls or an ice dam that forces water through your roof, but they absolutely will not cover flooding from external sources. If a hurricane pushes ocean water into your home, or heavy rain overwhelms storm drains and floods your basement, your standard policy pays nothing. Connecticut’s coastal exposure makes this critical-yet most homeowners assume their existing coverage handles it.

Flood Insurance: A Separate Purchase You Can’t Delay

You need separate flood insurance purchased through the National Flood Insurance Program, which has a mandatory 30-day waiting period before coverage activates. This timing matters significantly: you cannot buy flood insurance right before or after a hurricane, so waiting creates genuine risk. If you live within approximately 1,500 feet of the coast in Fairfield County, flood insurance transitions from optional to essential because proximity dramatically increases exposure. Inland properties in Hartford County face lower flood risk but may still encounter basement water infiltration during heavy spring snowmelt or summer thunderstorms.

Earthquake and Ground Movement Coverage

Earthquake and ground movement represent another complete exclusion, though Connecticut’s seismic activity remains relatively low compared to western states. Earthquake coverage remains available as a separate policy in Connecticut if you want additional peace of mind, though the risk profile stays low for most homeowners in the state.

Wear, Tear, and Maintenance Failures

Wear and tear, maintenance failures, and gradual damage fall outside coverage-if your roof leaks because shingles deteriorated over time, that’s your responsibility, not your insurer’s. Connecticut’s harsh winters create particular vulnerability: frozen pipes are covered when they burst, but the damage from negligent heating maintenance is not. The key distinction between exclusions involves whether damage results from a sudden event or gradual neglect, and that line determines whether your claim receives approval or denial.

Closing Coverage Gaps With Optional Endorsements

Equipment breakdown coverage fills gaps that standard policies leave open-if your HVAC system fails, standard coverage provides nothing, but this optional protection can cover repair or replacement costs. Water backup coverage addresses limited basement flooding scenarios that standard exclusions leave unprotected. Some optional endorsements vary between carriers, so reviewing your specific policy’s water exclusions matters because the language differs. These targeted additions transform your protection from basic to comprehensive, addressing the real risks Connecticut homeowners face. Understanding what your policy excludes positions you to evaluate whether your current limits match your actual exposure-and that assessment requires knowing exactly how much protection you need.

Setting Your Coverage Limits

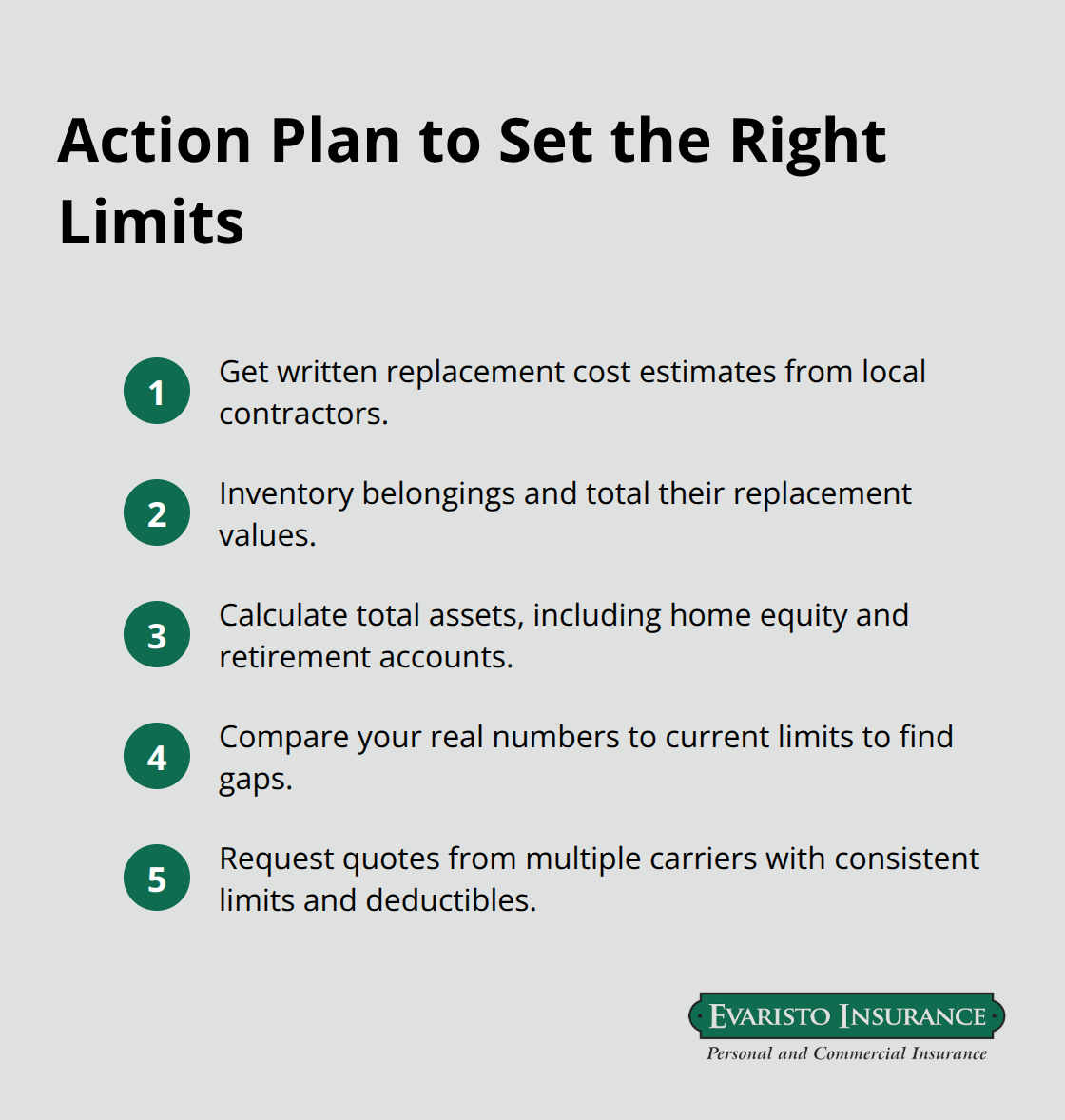

Choosing coverage limits separates homeowners who recover fully after a loss from those who face financial shortfall. The Connecticut average of $2,019 annually for a $400,000 dwelling tells you what protection costs, but it doesn’t tell you what you actually need. Your home’s replacement cost drives dwelling coverage, and this number differs fundamentally from your home’s market value or your mortgage balance. A $500,000 home in Fairfield County might cost $600,000 to rebuild due to labor and material costs, while the same structure inland could cost $480,000 to reconstruct. Underinsure by $100,000 and you absorb that gap yourself after a total loss, no matter how catastrophic the damage. Contact local contractors or request a professional replacement cost assessment before you lock in your dwelling limit, because this single decision determines whether you rebuild or compromise on restoration quality.

Assess Your Home’s Replacement Cost

Your dwelling coverage amount should match what it actually costs to rebuild your home from the ground up. Market value and replacement cost diverge significantly-a home worth $500,000 on the market might require $600,000 in construction costs to fully restore after total loss. Labor rates, material availability, and local building codes all factor into this calculation. Connecticut’s coastal areas face higher rebuild costs than inland regions due to specialized construction requirements for wind and water resistance. Contact three local contractors and request written estimates for complete reconstruction of your home’s structure, or hire a professional replacement cost assessor who specializes in this work. This investment in accuracy prevents the costly mistake of underinsuring your most valuable asset.

Quantify Your Personal Property Exposure

Personal property coverage limits typically range from 50 to 70 percent of your dwelling coverage, which works for average households but fails if you own significant valuables. Jewelry, art, collectibles, and electronics face sub-limits under standard policies-jewelry might cap at $2,500 regardless of actual value, while electronics hit $5,000 across your entire collection.

If you own jewelry worth $15,000 or artwork valued at $20,000, standard coverage leaves you dramatically underprotected. Scheduled personal property endorsements protect high-value items like jewelry and fine art beyond standard policy limits. Walk through your home and document what you actually own-furniture, electronics, clothing, tools-then compare that inventory against your proposed limit. Most Connecticut homeowners underestimate their belongings’ total value until they complete this exercise.

Match Liability Limits to Your Financial Reality

Liability coverage protects your assets if someone sues you successfully, which means your chosen limit should reflect what you actually own. Connecticut homeowners with $300,000 in home equity, $200,000 in retirement accounts, and ongoing income need liability limits significantly higher than the standard $100,000 many policies offer. If you face a $350,000 lawsuit and your policy covers only $100,000, creditors can pursue your assets and future wages for the remaining $250,000. Higher liability limits cost surprisingly little-increasing from $100,000 to $300,000 typically adds $15 to $30 annually to your premium. Jumping to $500,000 in coverage runs roughly $40 to $60 more per year. These marginal costs make minimal sense not to purchase adequate protection given what you’re protecting. If you own rental property, operate a home-based business, or have significant savings, $500,000 becomes the minimum reasonable limit rather than an optional luxury.

Final Thoughts

Your homeowners policy explained comes down to matching your protection to your actual exposure rather than accepting standard limits that may leave you vulnerable. Dwelling coverage must reflect your home’s true replacement cost, personal property limits must account for what you actually own, and liability protection must shield your assets and future income from lawsuit risk. Connecticut homeowners who take time to assess these three areas avoid the costly mistakes of underinsuring critical protection.

Start by gathering your home’s replacement cost through contractor estimates, document your personal belongings with a detailed inventory, and calculate your total assets including home equity and retirement accounts. Compare these real numbers against your current coverage to identify gaps that become your shopping priorities when requesting quotes from multiple carriers.

The homeowner who invests this effort discovers whether their existing policy truly protects them or leaves them exposed to financial catastrophe.

We at Evaristo Insurance help Connecticut homeowners align their coverage with their actual situation and budget. Contact us to review your homeowners policy and confirm your protection matches what you’re protecting.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.