Homeowners Insurance Deductible Connecticut: What to Expect

Your homeowners insurance deductible in Connecticut directly shapes both your monthly costs and out-of-pocket expenses when you file a claim. Choosing the wrong amount can leave you either overpaying for coverage you don’t need or facing unexpected bills when damage strikes.

At Evaristo Insurance, we help Connecticut homeowners navigate these decisions with clarity. This guide walks you through deductible options, regulations specific to our state, and how to pick the amount that fits your financial situation.

Understanding Your Deductible and Premium Trade-off

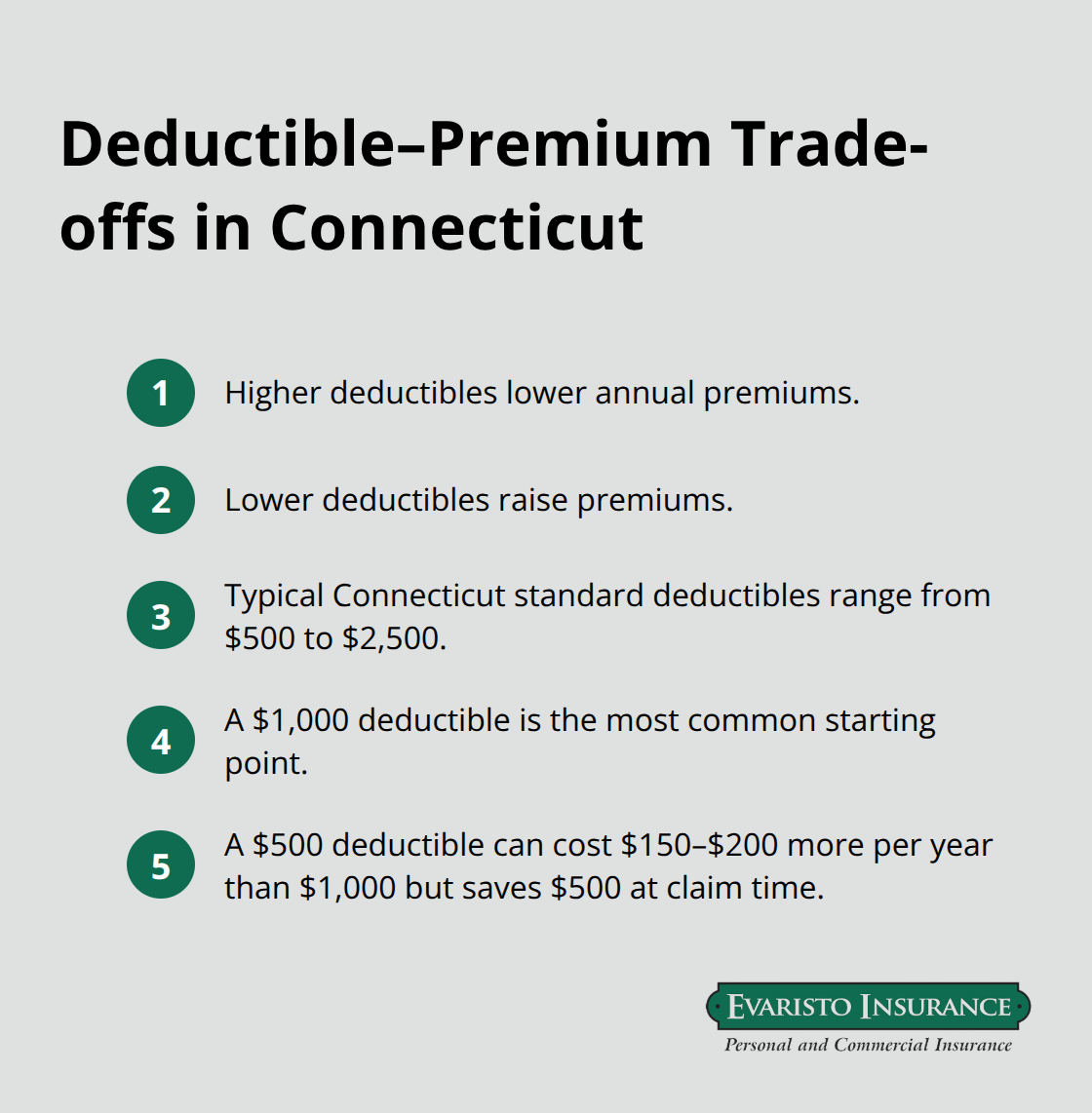

A homeowners insurance deductible is the amount you pay out of pocket when you file a claim, and it directly determines your annual premium. This relationship is straightforward: higher deductibles lower your premiums, while lower deductibles increase them. In Connecticut, standard homeowners insurance deductibles typically range from $500 to $2,500, with $1,000 as the most common starting point. According to Insure.com data, the average Connecticut homeowner pays about $2,205 annually for a standard policy with $300,000 dwelling coverage, $100,000 liability, and a $1,000 deductible. If you increase that deductible to $2,500, your premium drops noticeably, but you’ll pay significantly more when a claim occurs.

The math matters here: a $500 deductible might cost you $150 to $200 more per year than a $1,000 deductible, but it saves you $500 out of pocket if you file a claim. This trade-off should reflect your ability to cover unexpected costs without financial strain, not just which option sounds cheaper on paper.

Percentage vs. Fixed Deductibles in Connecticut

Connecticut insurers commonly offer two deductible structures. Fixed deductibles are straightforward-you pay a set dollar amount like $1,000 or $2,500 regardless of your home’s value. Percentage deductibles, however, are calculated as a percentage of your home’s insured value, typically ranging from 1% to 2%. If your dwelling is insured for $300,000 with a 2% deductible, you’d pay $6,000 out of pocket for a covered loss-far higher than most homeowners expect. Coastal properties and high-value homes often face percentage deductibles, particularly for wind and hurricane damage. Many Connecticut homeowners find percentage deductibles problematic because they scale with home value, creating unexpectedly large out-of-pocket costs. This is why flat deductibles remain preferable for most-they’re predictable and manageable. When you shop for quotes, confirm whether your deductible is fixed or percentage-based and calculate the actual dollar amount you’d pay in a claim scenario.

How Location and Peril Type Change Your Deductible

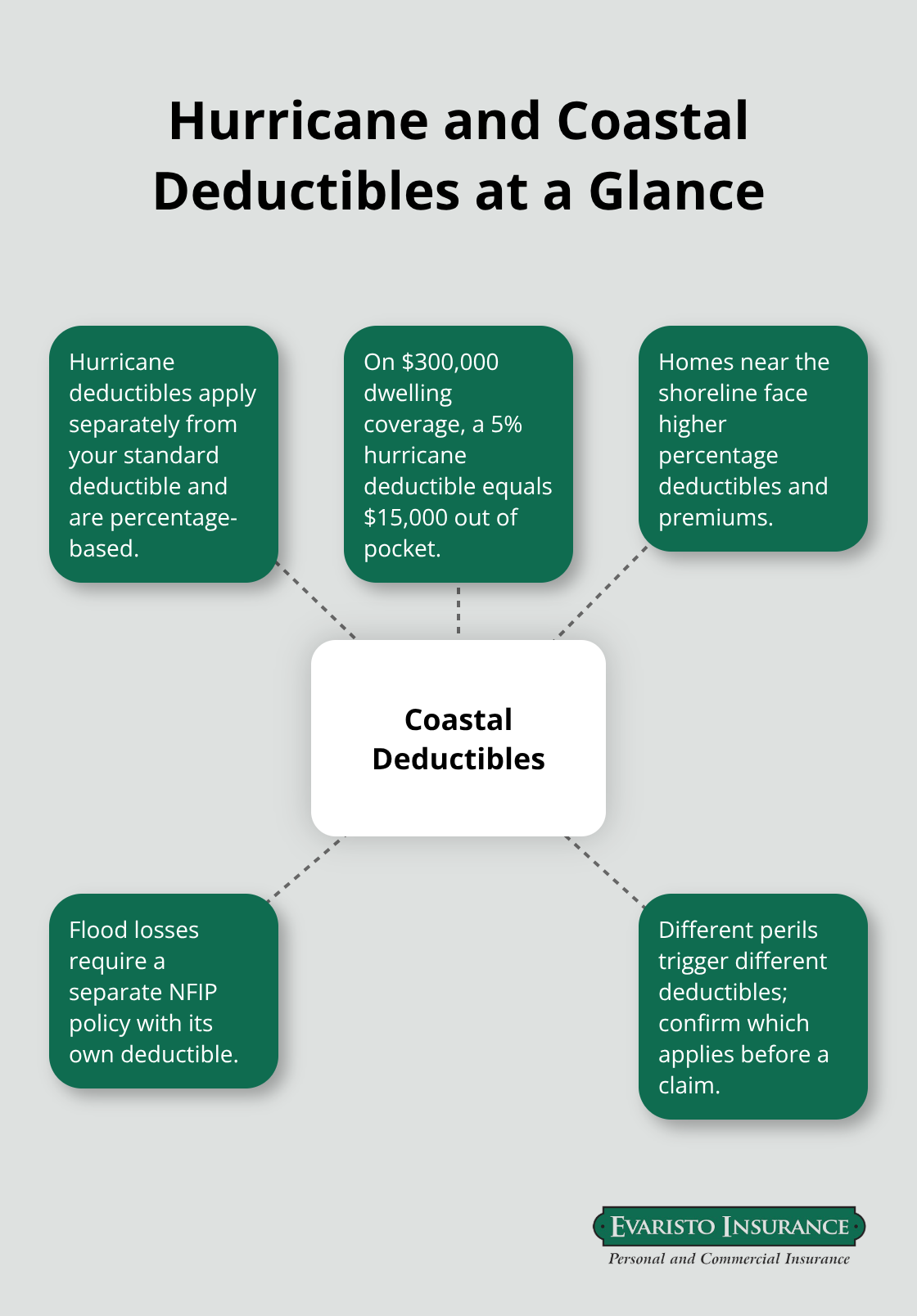

Connecticut’s geographic risk profile creates deductible variations that don’t apply everywhere else. Homes near the coast face hurricane deductibles, which are typically percentage-based and separate from your standard deductible. A property in Fairfield County near the shoreline might have a 5% hurricane deductible on top of a $1,000 standard deductible for other perils. This means a hurricane claim triggers the higher percentage deductible while a fire or theft claim uses the $1,000 amount. Water damage creates additional complexity-sewer backup and plumbing failures aren’t covered under standard policies, requiring separate endorsements with their own deductibles. Flood damage, which Connecticut residents in flood-prone areas absolutely need to address, requires a completely separate flood insurance policy through the National Flood Insurance Program, with deductibles starting at $500. The Connecticut Insurance Department advises reviewing these distinctions with a local agent because your actual out-of-pocket costs depend on which peril causes the damage, not just a single deductible number.

Why Your Specific Situation Demands a Closer Look

The deductible amount that works for your neighbor won’t necessarily work for you. Your financial cushion, your home’s location, and your risk tolerance all shape the right choice. A homeowner with substantial savings can comfortably absorb a $2,500 deductible and enjoy lower monthly payments. Another homeowner with limited reserves needs the security of a $500 or $1,000 deductible, even if premiums cost more. Connecticut’s coastal exposure adds another layer-if you live within a few miles of the shoreline, wind and hurricane deductibles apply separately, and those percentage-based amounts can reach thousands of dollars. Understanding how these pieces fit together requires more than a quick online quote. A local agent walks you through the actual dollars you’d pay in different scenarios, helping you make a decision that protects both your home and your wallet.

Choosing the Right Deductible for Your Connecticut Home

Match Your Deductible to Your Emergency Fund

Your deductible decision hinges on one critical question: how much can you afford to pay out of pocket without jeopardizing your financial stability? This isn’t about choosing the lowest premium-it’s about selecting the amount you can actually handle when a claim happens. If you have three to six months of expenses in savings, a $2,500 deductible makes sense because you can absorb that cost without derailing your budget. If your emergency fund covers only a month or two, a $1,000 deductible is safer, even if your monthly premium runs $15 to $25 higher.

Insure.com data shows Connecticut homeowners with $300,000 dwelling coverage pay roughly $2,205 annually with a $1,000 deductible. Jumping to $2,500 saves money each month, but costs you an extra $1,500 when damage occurs. The trap many homeowners fall into is selecting a deductible based purely on the premium difference without calculating their actual ability to pay. Many Connecticut homeowners can reduce premiums by increasing their standard deductible from $500 to $1,000, which sounds significant until you face a claim and realize you chose an amount you cannot comfortably pay.

Connecticut homeowners in Fairfield County average $2,225 annually according to competitor data, while Hartford County runs about $1,721, showing how location alone shifts your baseline costs before you even adjust the deductible. Your choice should reflect what you’d actually pay, not what sounds reasonable in theory.

Account for Coastal Hurricane Deductibles

Coastal properties demand extra scrutiny because hurricane deductibles operate separately from your standard deductible and are almost always percentage-based. A home in coastal Fairfield County with a 5% hurricane deductible on $300,000 dwelling coverage means you’d pay $15,000 out of pocket for wind damage-far higher than a standard deductible. This is why homeowners near the shoreline must factor two separate deductible amounts into their financial planning.

Homes within 1,500 feet of the coast face steeper premiums than those 15 miles inland, and those higher costs often reflect the percentage deductibles applied by insurers. If you live in a flood zone, you also need flood insurance through the National Flood Insurance Program with its own deductible starting at $500. The Connecticut Insurance Department emphasizes that homeowners must understand which deductible applies to which peril because your actual out-of-pocket cost depends on what caused the damage.

Understand How Different Perils Trigger Different Deductibles

A fire uses your standard deductible; a hurricane uses the percentage deductible; flooding uses the separate flood policy deductible. Many Connecticut homeowners discover this too late, expecting one amount and facing another at claim time. A local agent can walk you through realistic scenarios-what you’d actually pay for a roof claim versus a hurricane claim versus a basement flood-so you make decisions based on numbers, not guesses. This clarity transforms your deductible choice from a confusing decision into a straightforward financial plan that protects both your home and your wallet.

Deductible Options Beyond Standard Coverage

Connecticut homeowners often discover too late that their standard deductible tells only part of the story. Your policy contains multiple deductibles layered across different perils, and understanding this structure separates those who face surprises at claim time from those who plan accurately. When you file a claim for wind damage, your percentage-based hurricane deductible applies, not your standard $1,000 amount. When water backs up through your basement drain, that loss falls outside standard coverage entirely unless you purchased a sewer backup endorsement. When flooding occurs, your standard homeowners policy pays nothing regardless of your deductible-you need a completely separate flood insurance policy with its own deductible structure. This complexity reflects the different risk levels insurers assign to different perils. Coastal Connecticut properties face especially complicated deductible arrangements because hurricane exposure justifies percentage deductibles that climb into the thousands of dollars. A home in coastal Fairfield County with $500,000 dwelling coverage and a 5% hurricane deductible means you pay $25,000 out of pocket for wind damage, completely separate from whatever standard deductible you selected for other losses.

Wind and Hurricane Deductibles Demand Separate Planning

Connecticut’s coastal exposure creates a deductible reality that inland homeowners never face. Insurers apply percentage-based deductibles specifically to wind and hurricane damage, and these percentages typically range from 2% to 5% of your dwelling coverage. The closer you live to the shoreline, the higher this percentage climbs. A property 1,500 feet from the coast faces steeper hurricane deductibles than one 15 miles inland, and your premiums reflect this risk stratification directly. The National Hurricane Center data shows Atlantic hurricane activity has produced significant coastal damage throughout Connecticut’s history, which explains why insurers separate wind deductibles from standard deductibles. Many homeowners assume their standard deductible applies to all claims, then face a substantial bill when a hurricane strikes. This gap between expectation and reality causes genuine financial hardship. You must know both numbers-your standard deductible and your hurricane deductible-and understand which peril triggers which amount. A local agent can show you exactly what you’d pay for a hurricane claim versus a fire claim, eliminating guesswork from your financial planning. Increasing your standard deductible from $500 to $1,000 is a strategy many Connecticut homeowners use to reduce premiums while managing their overall deductible structure.

Water Damage and Flood Insurance Create Separate Deductible Tiers

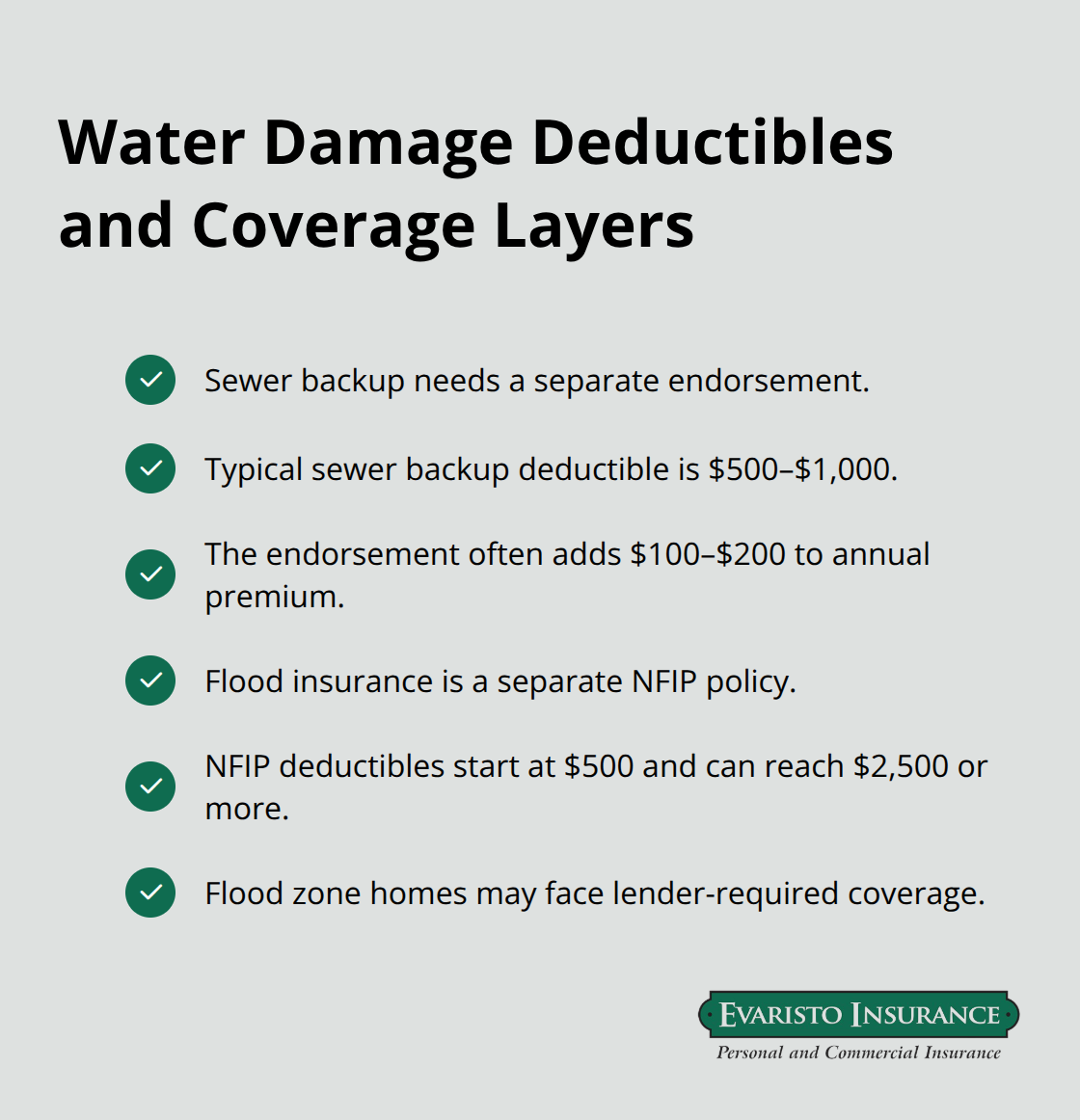

Water damage claims reveal the most dangerous deductible gaps in standard homeowners policies. Sewer backup, plumbing failures, and foundation seepage do not appear in your basic policy, yet many Connecticut homeowners assume they are covered. If your basement floods from a backed-up sewer line, your standard deductible does not matter because the loss simply is not covered. You need a separate sewer backup endorsement, which carries its own deductible-typically $500 to $1,000-and adds roughly $100 to $200 to your annual premium. Flood damage from heavy rain or storm surge requires an entirely separate flood insurance policy through the National Flood Insurance Program, with deductibles starting at $500 and climbing to $2,500 or higher depending on your coverage choices. Connecticut’s flood risk varies significantly by location. Homes in designated flood zones face mandatory flood insurance requirements from mortgage lenders, while properties outside flood zones can choose whether to purchase coverage.

FloodSmart.gov provides detailed flood risk mapping and premium estimates for Connecticut addresses. The critical mistake homeowners make is treating flood insurance as optional when they live anywhere near a flood-prone area. Heavy rainfall events have increased in frequency across Connecticut, and even homes outside traditional flood zones experience water damage from these events. A local agent can assess your specific flood risk, explain what your standard policy excludes, and recommend appropriate endorsements and separate flood coverage. This layered approach to water damage deductibles protects you against the most expensive claims homeowners face.

Final Thoughts

Your homeowners insurance deductible in Connecticut shapes both your monthly costs and what you actually pay when damage strikes. The decision requires you to match your deductible to your emergency fund, account for separate hurricane deductibles if you live near the coast, and understand that water damage often demands additional coverage with its own deductible structure. Connecticut’s coastal exposure and variable flood risk mean your strategy must account for factors that don’t apply in other states.

A local agent transforms this decision from confusion into a clear financial plan. They walk you through realistic claim scenarios, calculate what you’d pay for different types of damage, and explain how Connecticut-specific factors affect your total out-of-pocket costs. They compare quotes from multiple carriers, identify available discounts, and confirm your coverage matches your home’s actual value and location risks.

We at Evaristo Insurance help Connecticut homeowners navigate these decisions with clarity and expertise. Contact us today to review your current policy, explore deductible options that fit your budget, and confirm you have appropriate coverage for Connecticut’s specific risks. Your homeowners insurance deductible Connecticut decision deserves guidance from someone who understands your state’s unique insurance landscape.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!