CT Landscaper Insurance Quotes: A Local Guide for Connecticut Professionals

Running a landscaping business in Connecticut means managing more than just plants and equipment-you also need the right insurance protection. We at Evaristo Insurance understand that finding the right CT landscaper insurance quotes can feel overwhelming when you’re focused on growing your business.

This guide walks you through exactly what coverage you need, how to get accurate quotes, and what factors affect your premiums. You’ll have the clarity to make decisions that protect your business without overpaying.

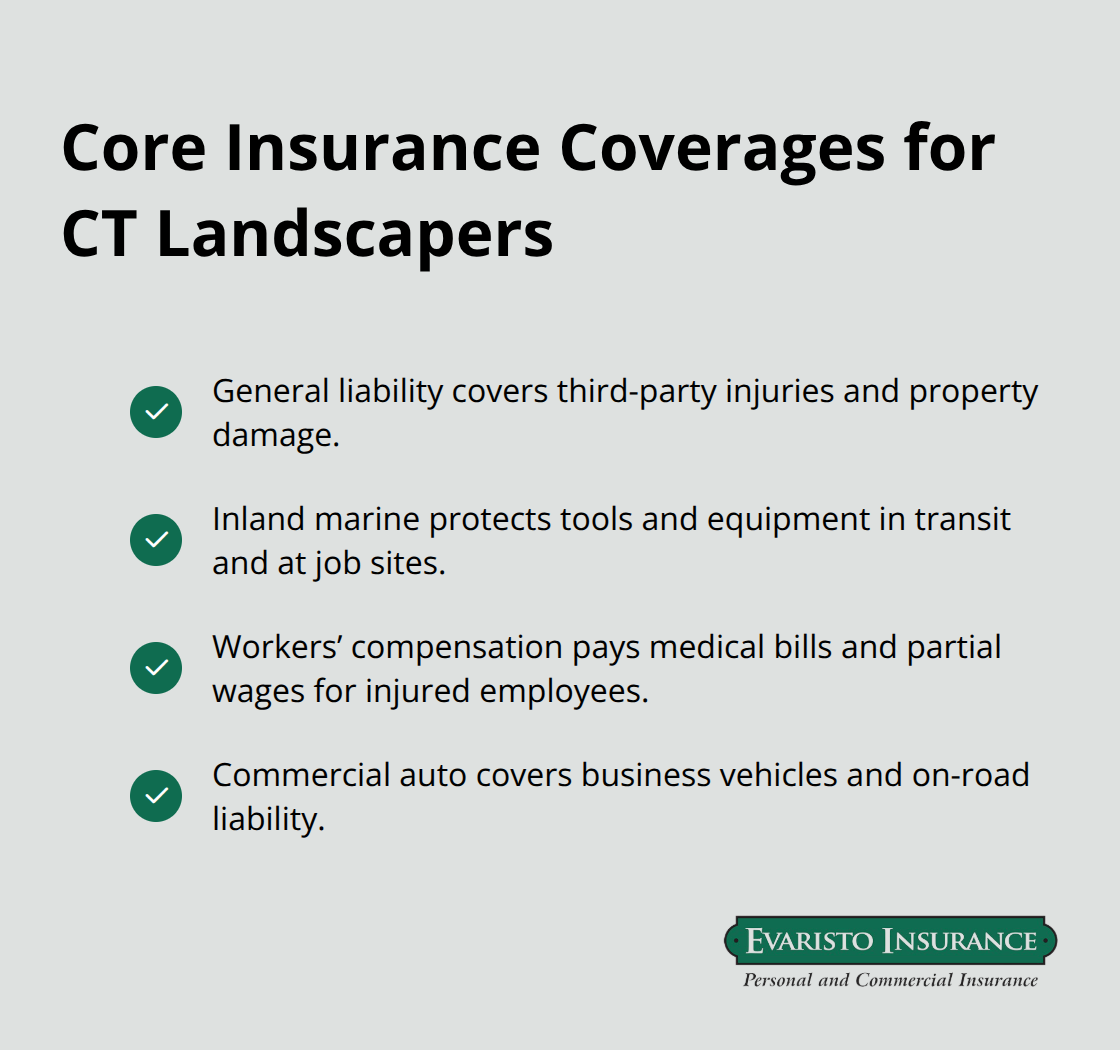

What Coverage Connecticut Landscapers Need Most

Liability Coverage Protects Your Business and Your Clients

Liability coverage protects your business when someone gets injured on a job site or your work damages client property. Connecticut law doesn’t mandate general liability insurance for landscapers, but commercial clients almost always require it before hiring you. The standard expectation is 1 million dollars per occurrence and 2 million dollars aggregate. A single accident-a crew member injuring a homeowner or your equipment damaging a fence-can create financial exposure that threatens your entire operation. General liability covers medical expenses, legal fees, and property damage claims, making it the foundation of any landscaper’s protection strategy.

Equipment Theft Represents Real Financial Risk

Tools and equipment represent serious financial exposure for landscaping businesses. Inland marine insurance protects your mowers, trimmers, blowers, and trailers while they’re in transit or sitting at job sites. A single theft can wipe out months of profit and halt operations for weeks. Many landscapers underestimate this risk until they experience it-a trailer stolen overnight or equipment vandalized at a residential property creates immediate operational problems. Protecting your tools keeps your business running without interruption.

Workers Compensation Covers Your Team and Your Liability

Workers’ compensation insurance is mandatory for all businesses with employees in Connecticut, including landscaping companies. Non-compliance brings fines and potential criminal charges, making this coverage mandatory rather than discretionary. Workers’ comp covers medical expenses and partial wage replacement when an employee gets injured on the job. A crew member injured while trimming branches or operating equipment creates immediate financial and legal liability without proper coverage.

Baseline workers’ compensation costs start around 19 dollars monthly, though Connecticut rates vary by payroll and risk profile.

What Happens When You Get Quotes

Accurate quotes depend on providing carriers with complete information about your business operations, employee count, and service types. Different insurers evaluate risk differently, so comparing multiple quotes reveals significant price variations and coverage options. Understanding what each policy excludes prevents gaps that could leave you exposed when you file a claim.

How to Get Accurate Landscaper Insurance Quotes in Connecticut

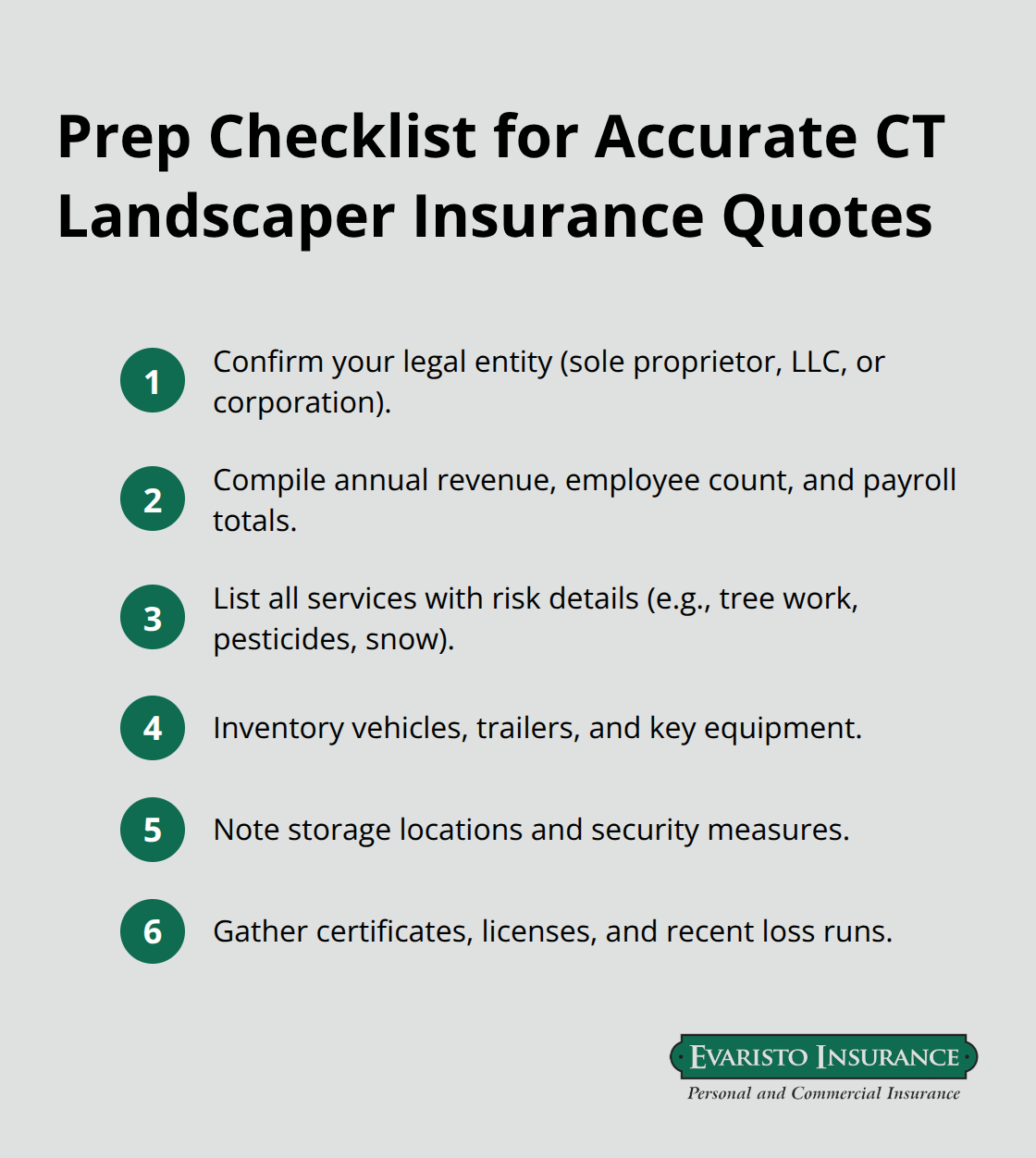

Prepare Your Business Information Before Requesting Quotes

Requesting quotes without preparation wastes time and produces incomplete comparisons that hide important coverage gaps. Start by documenting your actual business structure-whether you operate as a sole proprietor, LLC, or corporation-because carriers price differently based on legal entity type. Write down your total annual revenue, number of employees, and payroll figures; Connecticut workers’ compensation rates depend heavily on payroll size and job classifications. List every service you offer in detail: basic lawn maintenance, tree trimming, landscape design, pesticide application, or snow removal all carry different risk profiles and premium impacts. Carriers need to know if you operate commercial vehicles, how many pieces of equipment you own, and whether you store materials at a yard or office location. The more specific your information, the more accurate your quotes become.

Connecticut landscapers commonly underestimate their payroll when requesting quotes, leading to artificially low premium estimates that spike during renewal when actual figures are verified.

Compare Multiple Carriers to Find Real Value

Comparing quotes across multiple carriers reveals that prices vary dramatically. Request quotes from at least three carriers and ask each one to explain why their pricing differs from competitors; sometimes higher premiums reflect better coverage, lower deductibles, or superior claims handling rather than poor value. Pay attention to coverage limits and what’s actually excluded from each policy, not just the bottom-line price. Many landscapers focus exclusively on general liability costs and miss significant gaps in workers’ compensation or equipment coverage that create real exposure.

Ask the Right Questions About Coverage Details

Ask carriers directly whether product liability coverage applies if you apply chemicals or fertilizers, since this protection can be essential for your service mix. Request instant online certificates of insurance from each carrier to verify they can provide proof of coverage quickly when clients demand it-this operational capability matters more than most landscapers realize. Understanding what each policy excludes prevents gaps that could leave you exposed when you file a claim. An independent agency like Evaristo Insurance represents multiple top-rated carriers and can explain trade-offs between options rather than pushing a single product, helping you move forward with confidence about your coverage choices.

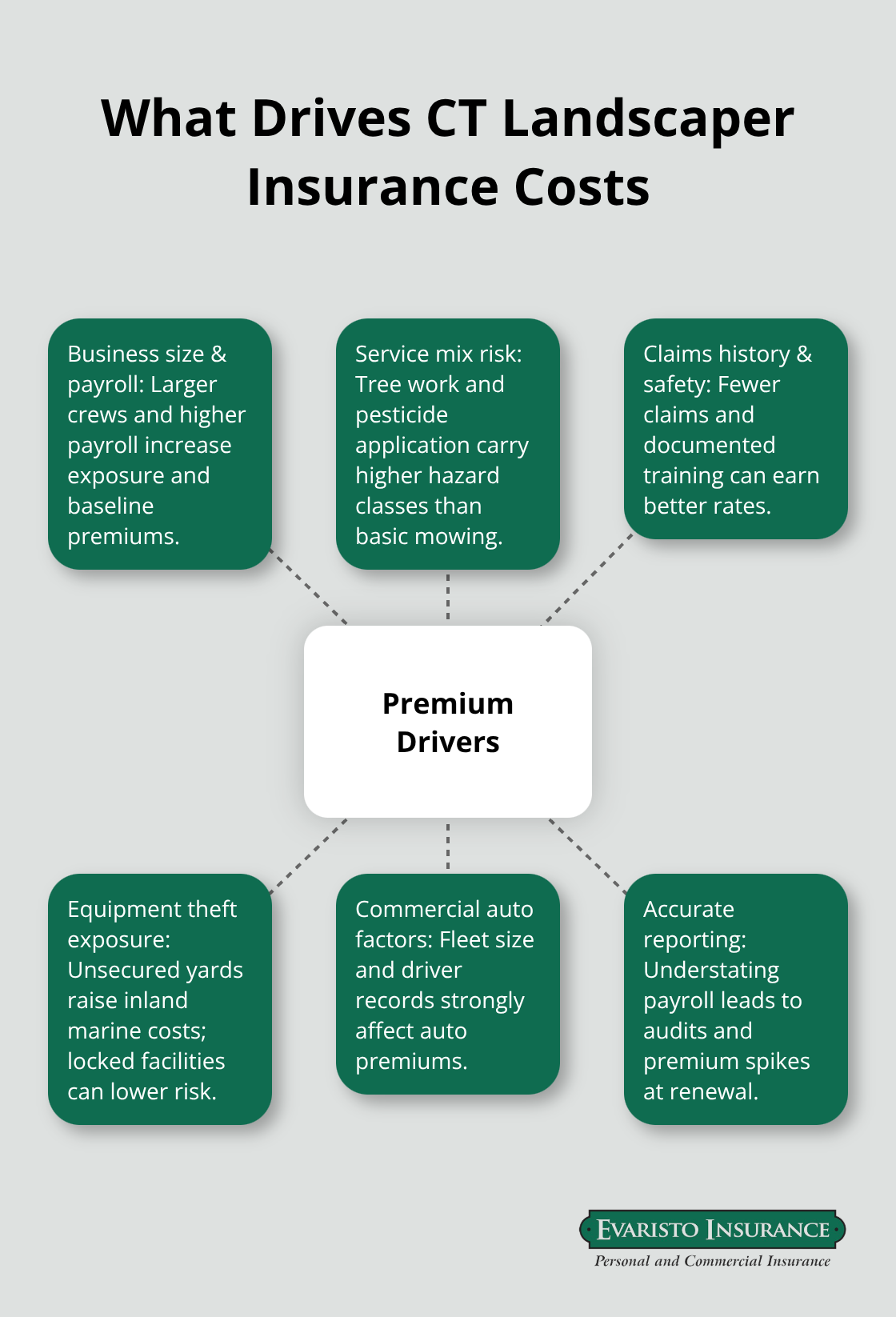

Cost Factors That Impact Your Landscaper Insurance Premiums

Your landscaping insurance premiums depend on specific operational factors that carriers evaluate differently, which means understanding these drivers helps you control costs and negotiate better rates.

Business Size Shapes Your Premium Foundation

Business size matters significantly because larger operations with higher payroll and more employees create greater exposure than solo operators or small crews. Connecticut general liability insurance for landscapers typically ranges from $31 to $464 monthly, but this variation reflects real differences in business scale and risk profile. A sole proprietor doing basic lawn maintenance pays far less than a company running fifteen crews and offering tree removal services. Your annual revenue directly influences workers’ compensation premiums since Connecticut rates tie to payroll figures; understating your revenue when requesting quotes creates artificially low estimates that jump dramatically at renewal when carriers verify actual payroll records. This surprise spike frustrates landscapers who thought they understood their costs, so accuracy upfront prevents budget problems later.

Service Type Drives the Largest Cost Swings

The specific services you offer create the biggest premium variations because tree trimming and pesticide application carry substantially higher risk than basic mowing and maintenance. Connecticut landscapers applying pesticides must hold a Commercial Supervisory Certificate from the Department of Energy and Environmental Protection, and carriers charge premium surcharges for this higher-risk work. Client injuries on your job sites create the most expensive liability claims because they involve medical expenses, legal fees, and sometimes permanent disability costs. Equipment theft also influences pricing; a company storing expensive equipment at an unsecured yard location pays more than one keeping tools in a locked facility.

Claims History and Safety Practices Determine Your Rate Class

Your claims history and safety practices determine whether carriers view you as a responsible operator or a risky bet. A business with zero claims over five years qualifies for better rates than one filing multiple claims, while formal safety programs and documented training reduce premiums because they prove you take injury prevention seriously. Workers’ compensation premiums for Connecticut landscaping businesses vary based on your specific operations and claims history, but this cost increases when your crew has previous injury claims or operates high-risk equipment without documented safety protocols. Commercial auto insurance costs depend on your fleet size and driver records, yet this cost increases if your drivers have accidents or violations on their records.

Get Multiple Quotes to Reveal Your True Pricing Leverage

The smartest approach involves conducting a formal risk assessment of your actual operations and then shopping quotes with multiple carriers who understand your specific service mix, because generic quotes miss the pricing leverage available when you clearly communicate how you manage risk.

Final Thoughts

Finding the right CT landscaper insurance quotes requires you to understand what coverage protects your business, compare multiple carriers to reveal real pricing differences, and recognize how your specific operations drive premium costs. General liability, workers’ compensation, and equipment protection form the foundation of any landscaper’s insurance strategy in Connecticut, but the exact coverage you need depends on your service mix, employee count, and risk profile. Accuracy matters when requesting quotes because understating your payroll or omitting high-risk services like tree trimming or pesticide application creates artificially low estimates that spike dramatically at renewal.

Connecticut’s local business environment creates unique insurance challenges that generic online quotes often miss. Your clients expect proof of coverage quickly, and local carriers understand Connecticut’s specific regulatory requirements for pesticide licensing and workers’ compensation compliance. A solo operator doing basic lawn maintenance faces completely different insurance needs than a company running multiple crews and offering specialized services, yet many landscapers shop quotes without clearly communicating these operational differences to carriers.

Contact Evaristo Insurance today to get accurate CT landscaper insurance quotes tailored to your actual operations. We serve Connecticut businesses with hands-on advocacy that protects your business without overpaying for coverage you don’t need.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.