Connecticut Contractor Insurance: A Practical Guide to Protection for Builders

One accident on a job site can cost your contracting business thousands of dollars-or worse, put you out of business entirely. Connecticut contractor insurance isn’t optional; it’s the foundation that protects your livelihood, your employees, and your clients.

At Evaristo Insurance, we’ve helped countless builders across Connecticut understand exactly what coverage they need and why. This guide walks you through the insurance types that matter most, how to evaluate your specific risks, and how to choose policies that actually protect your business.

Why Contractors in Connecticut Actually Need Specialized Insurance

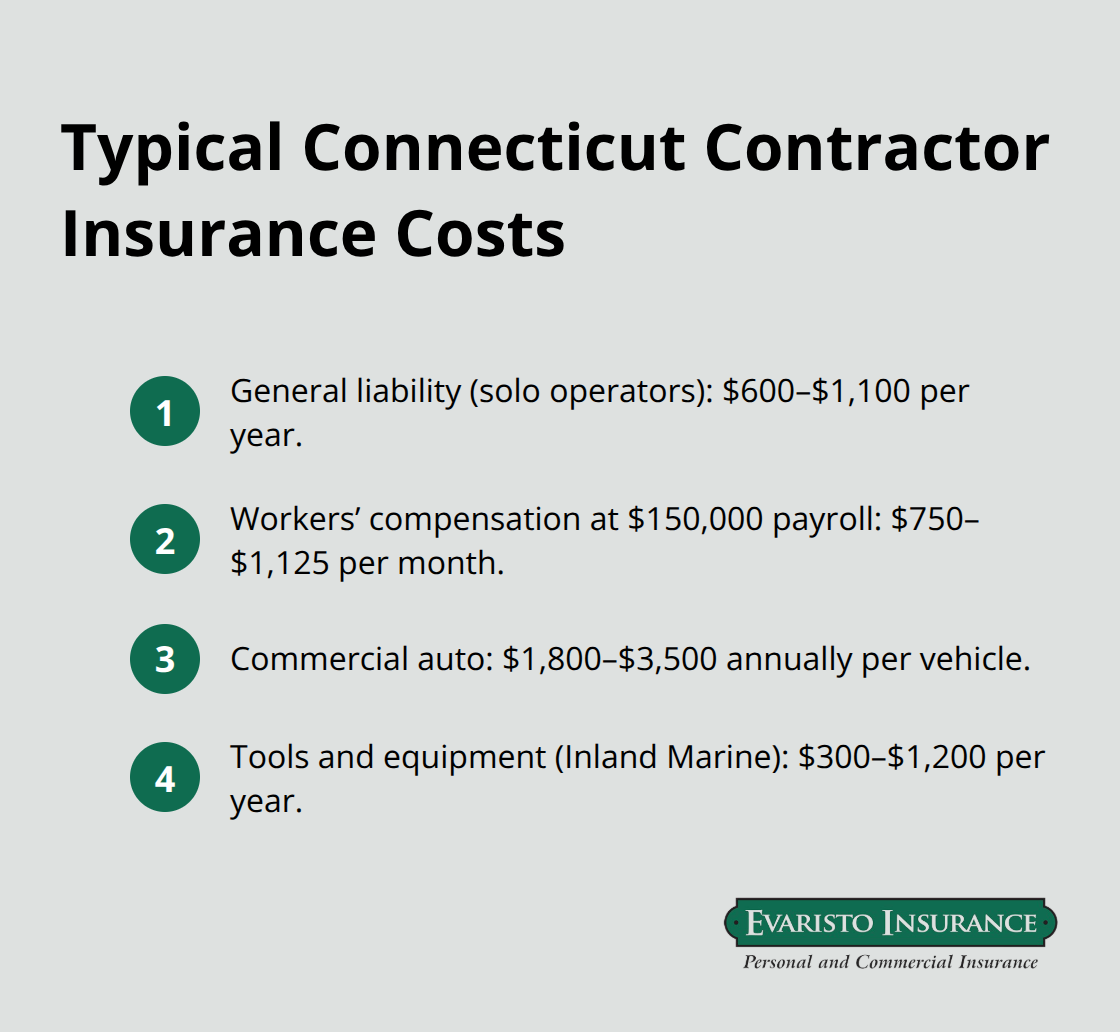

A single liability claim drains your business reserves fast. Connecticut contractors face real exposure on every project-someone gets hurt on your job site, property gets damaged, or a client sues over work quality, and suddenly you’re writing checks from your operating account. General liability insurance costs Connecticut builders roughly $50 to $92 per month for solo operators, and $92 to $250 monthly for crews of 2 to 5 employees, according to current Connecticut Department of Insurance data. That investment sounds steep until you realize a moderate injury claim hits $100,000 or more. Without coverage, you pay it yourself. With it, your insurer covers the legal defense and settlement, keeping your business intact.

Tools and Equipment Losses Hit Your Bottom Line Hard

Contractors lose thousands annually to theft and damage on job sites. Tools disappear from trucks, equipment gets damaged during transport, and materials vanish overnight. Inland Marine coverage-the insurance product that covers tools and equipment-typically costs $300 to $1,200 per year in Connecticut, depending on what you own and where you store it. That’s cheap compared to replacing a $5,000 power tool or $15,000 worth of materials. This coverage reimburses you for repairs or full replacement at current market prices, which keeps you operational when loss happens. Without it, you either absorb the cost or halt work while you source replacements out of pocket.

Connecticut Law Mandates Coverage Before You Can Register

Connecticut’s Department of Consumer Protection mandates that home improvement contractors carry at least $20,000 in general liability insurance before they can register. Major contractors face even stricter requirements-you must submit a certificate of insurance naming the DCP as certificate holder with your license application. Workers’ compensation is equally non-negotiable-Connecticut requires coverage before you hire your first employee, with no exceptions. The cost averages $750 to $1,125 monthly for a general contractor with a $150,000 annual payroll, based on current Connecticut rate data. Skipping it exposes you to fines, license suspension, and personal liability if an employee gets hurt.

Client Contracts Demand Proof of Coverage

Most residential and commercial clients now require proof of coverage before they let you on site. Many demand you carry $1 million per occurrence minimum, and some commercial projects or government bids require $2 million or higher. If you can’t produce a current certificate of insurance, you lose the job. Commercial auto insurance protects you when you drive to job sites in a work vehicle; Connecticut minimum is $25,000 per person and $50,000 per accident, though most clients require higher limits. These aren’t optional add-ons-they’re the legal and contractual foundation your business must have to operate legally and win work. Understanding what each policy covers and how much protection you actually need separates contractors who stay competitive from those who scramble to meet client demands.

What Coverage Do Connecticut Contractors Actually Need

General Liability: Your Foundation Against Third-Party Claims

General liability insurance protects you when someone gets hurt on your job site or you damage a client’s property during work. This coverage is non-negotiable. Connecticut sits in the mid-range cost range for contractor insurance, with general liability running from approximately $600–$1,100 for solo operators. These aren’t inflated numbers; they reflect actual risk pricing based on your trade and claims history. Solo operators pay the least, starting around $50 per month, but the moment you hire employees, your premiums jump. A crew of 2 to 5 people typically costs $92 to $250 monthly. The jump happens because more workers means more exposure. Many clients now demand $2 million per occurrence on commercial or government projects, which costs more but opens doors to bigger contracts.

Workers’ Compensation: Mandatory Coverage That Protects Your Crew

Connecticut enforces workers’ compensation strictly-you must carry it the moment you hire your first employee. For a general contractor with a $150,000 annual payroll, expect $750 to $1,125 monthly. HVAC contractors pay $475 to $688 monthly under the same payroll assumption; roofers face the highest burden at $1,250 to $2,250.

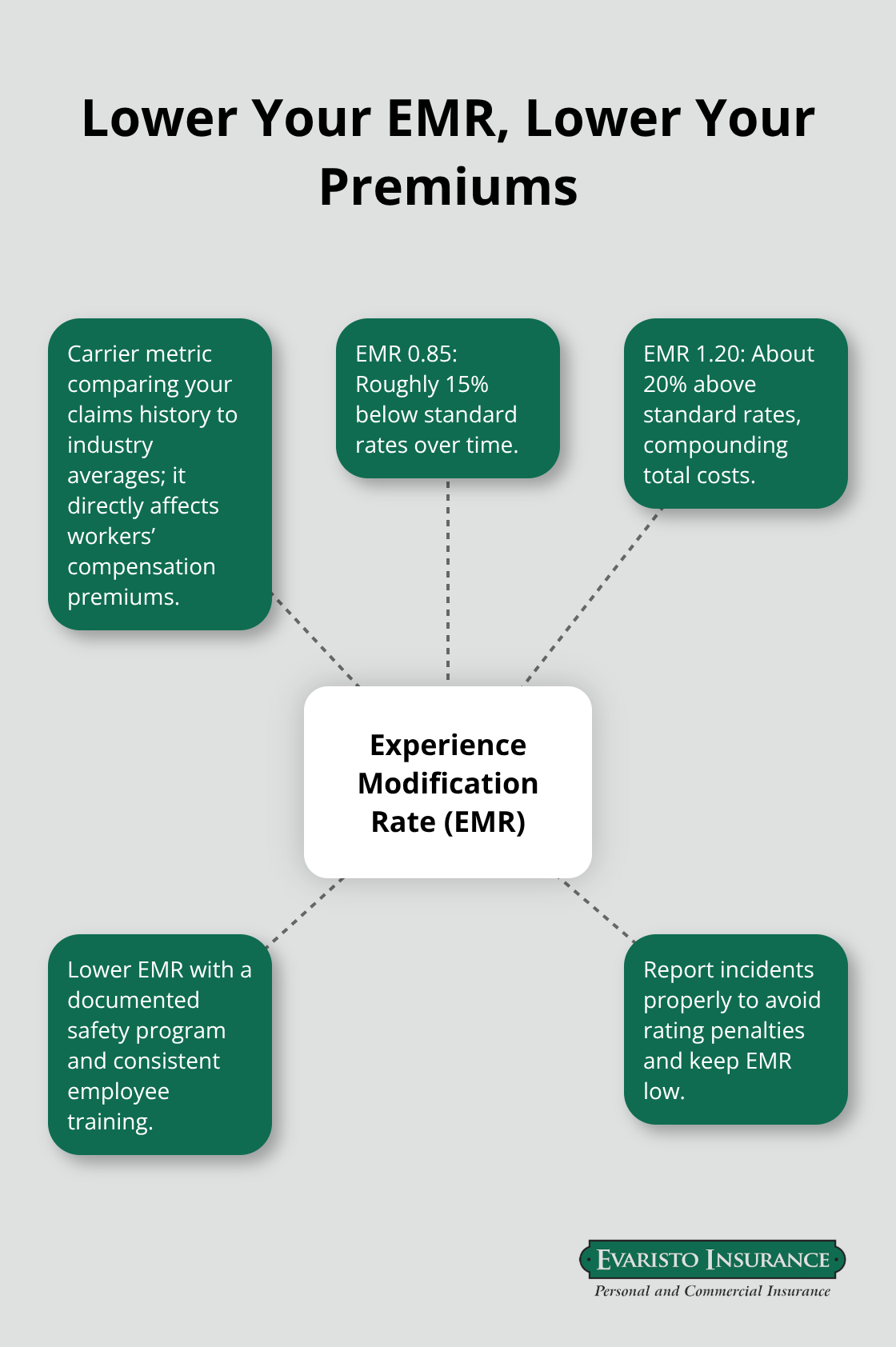

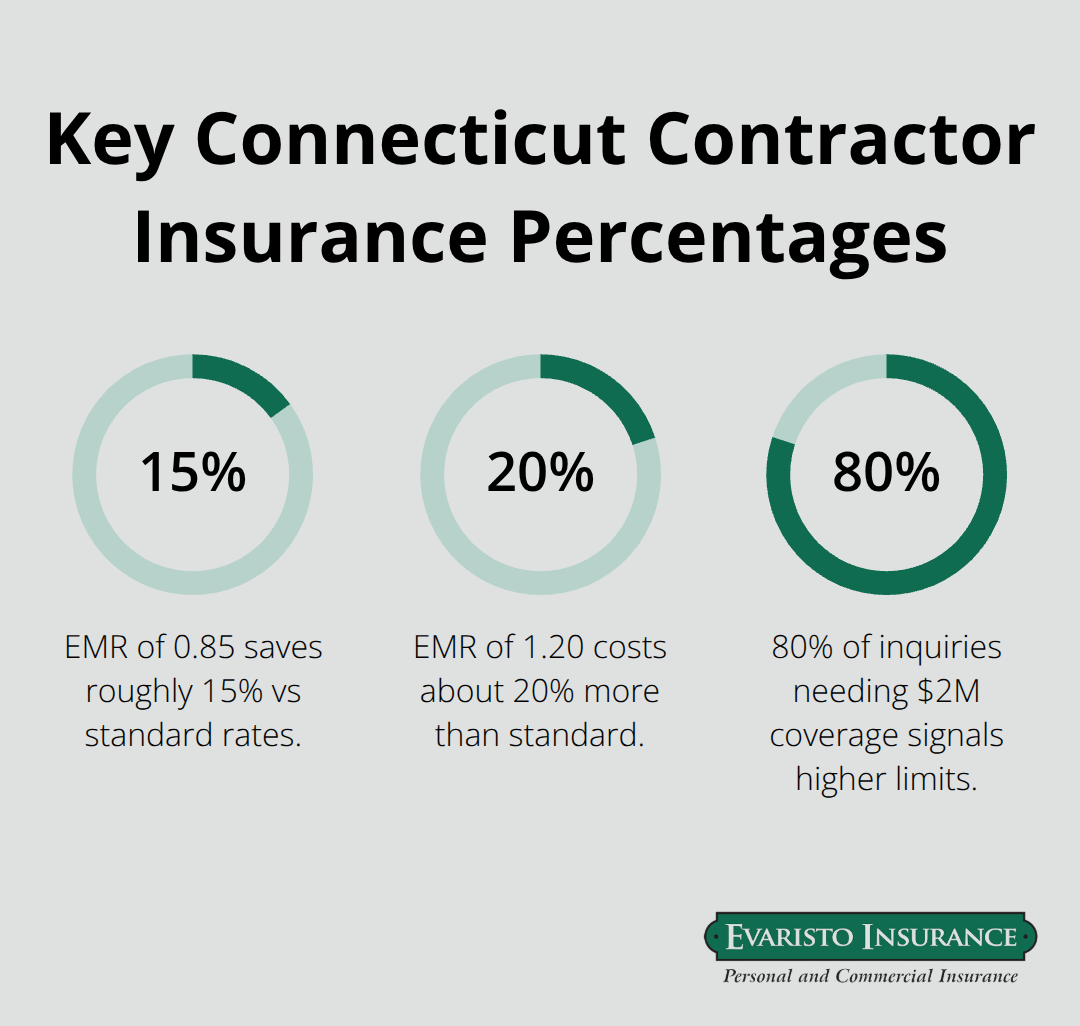

Your Experience Modification Rate (EMR) directly affects what you pay. An EMR of 0.85 saves you roughly 15% compared to an EMR of 1.20, which compounds over years. Maintain a solid safety program, document training, and report incidents properly to keep your EMR low. These actions reduce your long-term costs significantly.

Commercial Auto and Tools: Protecting Your Mobile Assets

Commercial auto insurance protects you when you drive work vehicles to job sites. Connecticut’s legal minimum is $25,000 per person and $50,000 per accident, but most clients require higher limits. Expect $1,800 to $3,500 annually per vehicle; fleet pricing helps if you operate multiple trucks.

Tools and equipment coverage-called Inland Marine insurance-costs $300 to $1,200 yearly depending on inventory value and storage location. This coverage reimburses you for theft, damage during transport, and weather-related losses. Many contractors skip this until they lose $8,000 in tools to a job site break-in, then wish they’d purchased the coverage months earlier.

Bundling Coverage for Better Pricing

Combine general liability, auto, and tools coverage with one carrier to receive 10 to 20% multi-policy discounts that offset the individual costs. This approach simplifies your policy management and reduces your overall premium burden. Shopping the market at renewal with 2 to 3 quotes prevents you from overpaying; ensure your classification codes reflect actual operations to avoid mischarges. Higher deductibles on lower-risk policies can lower premiums if you have cash reserves to cover small losses.

Your coverage choices directly determine whether you can bid on larger projects and meet client contract requirements. The next section walks you through how to evaluate your specific risks and select policies that actually fit your business model.

How to Choose the Right Contractor Insurance Policy

Match Coverage to Your Actual Job Mix

Start by listing every project type you’ve completed in the past two years and every project you plan to pursue in the next twelve months. This isn’t busy work-it’s the foundation of selecting the right coverage. A general contractor who primarily handles residential renovations below $500,000 faces different exposure than one bidding commercial projects or government work. Residential work typically requires $1 million per occurrence in general liability; commercial and government projects demand $2 million or higher. Connecticut Department of Consumer Protection registration requirements mandate minimum coverage for home improvement contractors, but that floor doesn’t reflect real-world protection. If you’re bidding projects worth $2 million, a $1 million policy leaves you underinsured. Conversely, carrying $5 million in coverage on $150,000 residential jobs wastes premium dollars. Review your client contracts from the past year-what coverage limits did they require? That requirement signals your actual market need. If 80 percent of your inquiries come from clients demanding $2 million coverage, purchasing only $1 million in limits costs you jobs.

Identify your highest-risk work too. Roofing contractors pay $2,400 to $6,600 annually for general liability in Connecticut, roughly three times what HVAC contractors pay, because fall hazards and weather exposure drive up claims frequency. If you expand into roofing or structural work, your premiums will jump accordingly. Plan for it rather than fight the market.

Deductibles and Claims History Shape Your Real Cost

A $2,500 deductible costs less monthly than a $500 deductible, but only if you have cash reserves to absorb small losses without strain. Many contractors choose $1,000 deductibles as the practical middle ground-low enough that a minor claim doesn’t wipe out reserves, high enough to reduce monthly premiums by 15 to 25 percent. Your Experience Modification Rate, or EMR, directly determines whether you qualify for lower rates. Carriers calculate this metric by comparing your claims history against industry averages. An EMR of 0.85 means you pay 15 percent less than standard rates; an EMR of 1.20 means you pay 20 percent more. If you’ve had zero claims in five years, you likely qualify for preferred rates. If you’ve filed two workers’ compensation claims in three years, expect to pay the standard rate or higher. When shopping quotes, ask each carrier for your EMR calculation and request documentation showing how they arrived at it. Some carriers use outdated data or misclassify your work, inflating your rate unnecessarily. Verify that your classification codes match your actual operations-a general contractor misclassified as a specialty trade can overpay significantly. Request quotes with both your current deductible and with a higher deductible to see the premium difference. Many contractors discover that increasing from $500 to $2,500 saves $30 to $60 monthly, which adds up to $360 to $720 yearly with zero additional risk if you maintain adequate cash flow.

Work with a Local Agent Who Understands Connecticut Requirements

Connecticut’s contractor insurance market rewards agents who understand state-specific requirements and local carrier relationships. The Department of Consumer Protection mandates that major contractor applicants name the DCP as certificate holder on their general liability policy-a requirement many online quote tools miss entirely. New home construction contractors must verify that coverage aligns with their registration type, not just their business structure. A solo operator working as an LLC needs different coverage than an individual operating as a sole proprietor, yet many carriers and agents fail to clarify this distinction until renewal time, when you discover coverage gaps. We at Evaristo Insurance, a second-generation family-owned independent agency serving Connecticut since 1989, specialize in exactly these details. We compare multiple top carriers to identify policies that meet Connecticut’s specific registration requirements while delivering competitive pricing. When you work with a local agent, you gain access to carrier relationships that national quote sites cannot replicate. Some Connecticut insurers offer multi-policy discounts of 10 to 20 percent when you bundle general liability, commercial auto, and tools coverage-discounts that don’t appear on generic online platforms. An agent familiar with Connecticut’s construction market also catches misclassifications before they inflate your rates. If your EMR seems high or your classification code doesn’t match your work, a local agent pushes back on the carrier’s initial quote and secures corrections that save hundreds annually. Request quotes from at least two carriers before committing, and ensure each quote explicitly lists coverage limits, deductibles, EMR assumptions, and classification codes. Compare apples to apples-a $1,000 deductible with $2 million coverage is not the same as a $2,500 deductible with $1 million coverage, even if monthly premiums look similar. Ask each carrier how they handle certificate of insurance requests and whether they offer endorsements for additional insureds without delay. Some carriers process COI requests in hours; others take weeks. When a client demands a certificate before work starts, slow turnaround costs you jobs.

Final Thoughts

Connecticut contractor insurance protects your business from the financial devastation that follows a single accident or claim. General liability, workers’ compensation, commercial auto, and tools protection form the backbone of sound risk management and allow you to bid confidently on larger projects while meeting client contract requirements. Without this coverage, you operate exposed to liability claims that drain your reserves or force closure.

Your next step is straightforward: list your current coverage gaps and contact an agent who understands Connecticut’s specific registration and insurance requirements. Request quotes from at least two carriers, compare coverage limits and deductibles side by side, and verify that classification codes match your actual work. Ask about multi-policy discounts when bundling general liability, auto, and tools coverage-these discounts often save 10 to 20 percent annually but don’t appear on generic platforms.

We at Evaristo Insurance have spent over three decades helping Connecticut contractors navigate these decisions through our local offices in Ellington and West Hartford. We compare multiple top carriers to deliver tailored protection and competitive pricing that reflects your actual risk profile, catch misclassifications, and handle certificate of insurance requests without delay. Contact us today to discuss your Connecticut contractor insurance needs and get a quote that reflects the real value of your business.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.