Rental Property Coverage: Building A Solid Foundation For Landlords

Owning rental property in Connecticut comes with real financial responsibility. Standard homeowners insurance won’t protect you-it explicitly excludes rental income and liability from tenants. We at Evaristo Insurance see landlords lose thousands because they didn’t have proper rental property coverage in place.

This guide walks you through what you actually need to protect your investment.

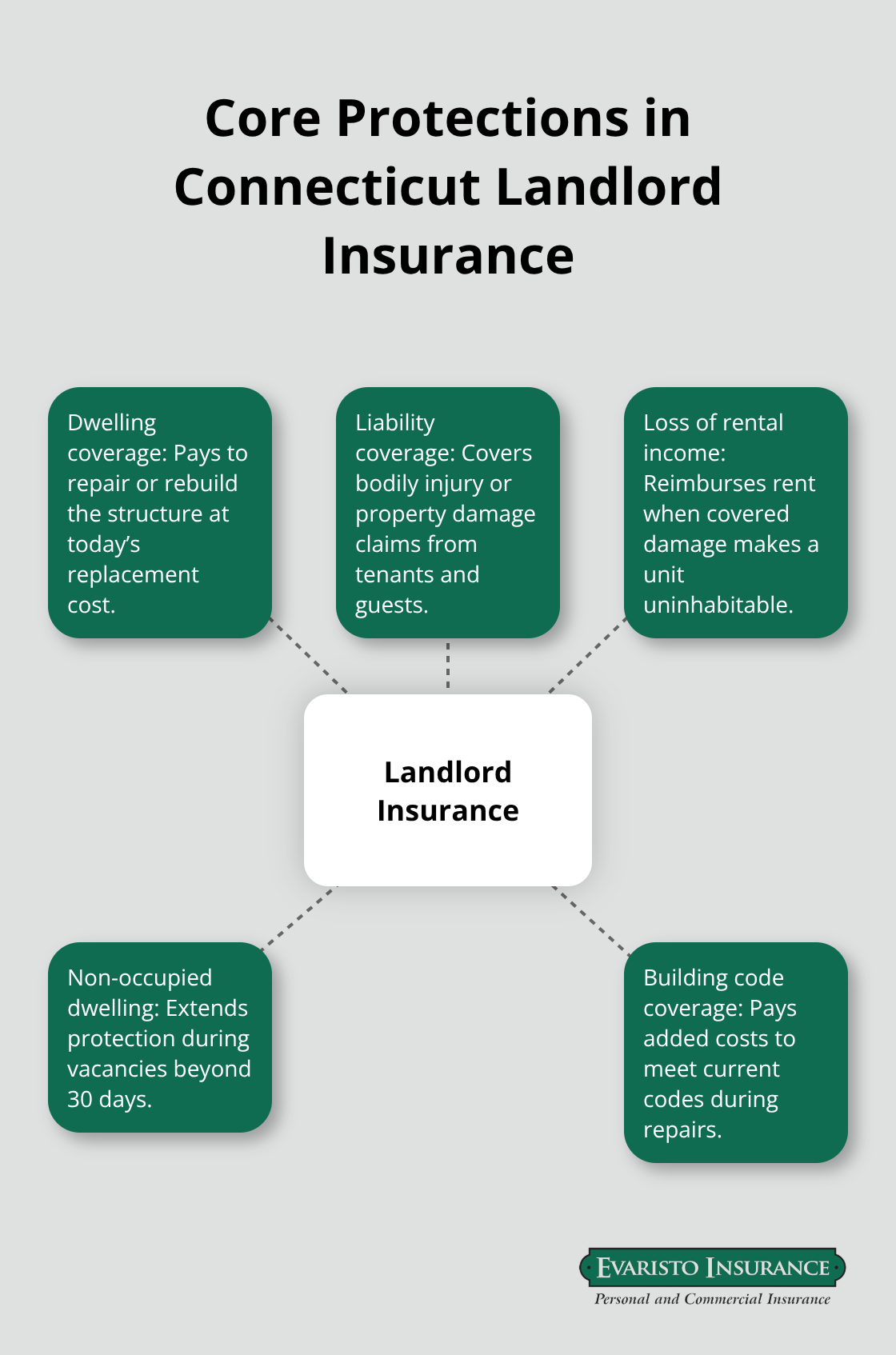

What Landlord Insurance Actually Protects

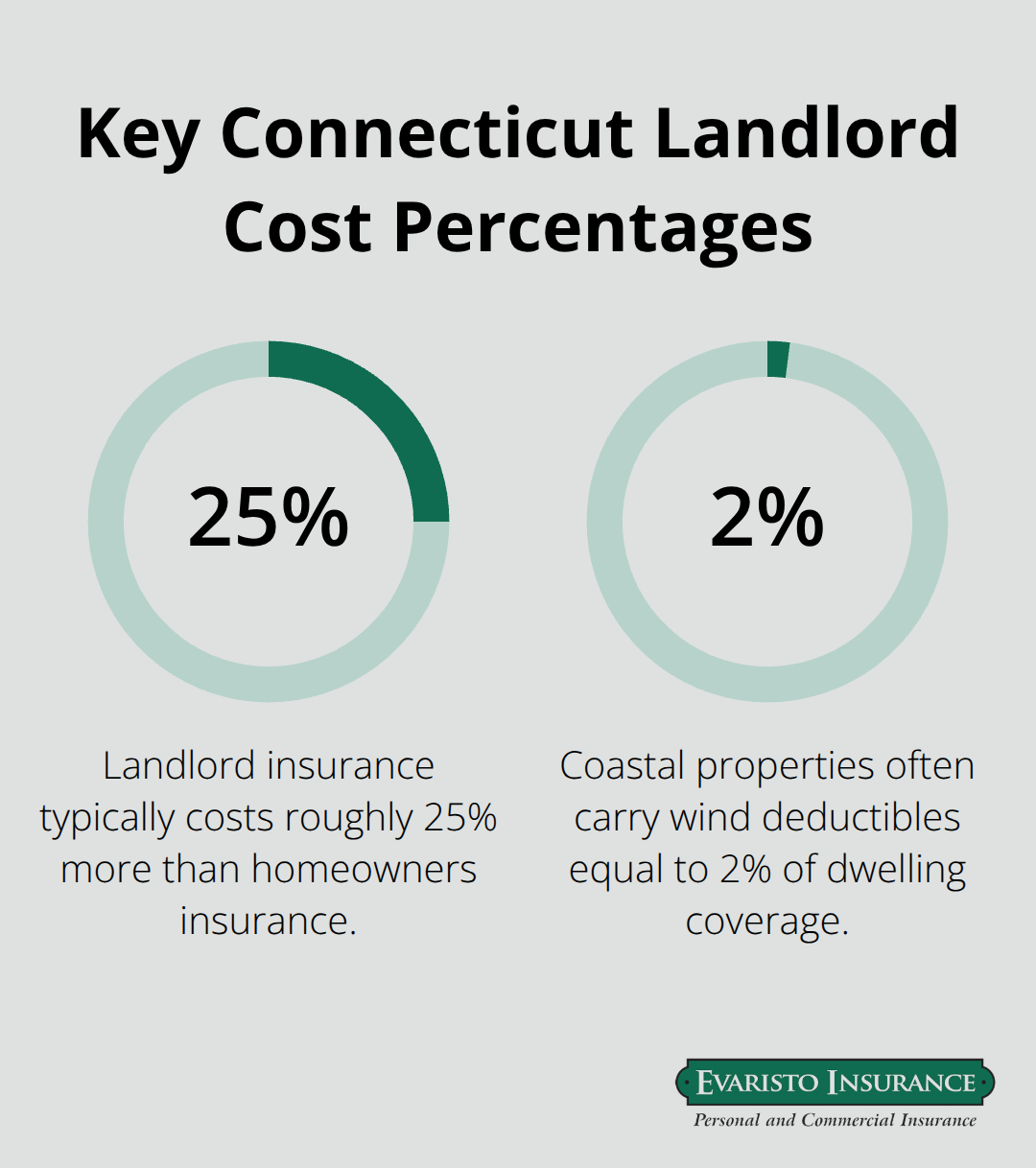

Landlord insurance covers three distinct areas that standard homeowners policies explicitly exclude: the building itself, your legal liability to tenants and their guests, and the rent you lose when damage makes a unit uninhabitable. Connecticut landlords typically pay between $800 and $3,000 annually for a standard three-bedroom property, with coastal locations running higher due to hurricane and storm exposure along Long Island Sound. The Insurance Information Institute reports that landlord coverage costs roughly 25% more than homeowners insurance, but that premium difference buys protection you cannot get any other way. Your dwelling coverage should be set at replacement cost, not actual cash value, because depreciation will leave you thousands short after a claim. If your property cost $250,000 to build today, that is your coverage floor-not some outdated assessment from five years ago. Review this limit annually and after any major renovations to keep pace with current construction costs in Connecticut’s market.

Property Damage and Structural Protection

Property damage coverage pays for repairs to the structure, roof, and landlord-owned appliances when a covered peril strikes. This protection stands separate from what tenants own; their belongings fall under their renters insurance, which you can require by lease. Landlord-owned items like refrigerators or water heaters receive coverage, but tenant possessions do not. Your dwelling limit should reflect what it would cost to rebuild your property today, not what you paid for it years ago. Connecticut construction costs have risen steadily, so adjust your coverage limits to match current market values, or you will face a shortfall when you file a claim.

Liability Coverage and Legal Duty

Liability coverage protects you when someone is injured on your property and sues. Connecticut property owners have a legal duty to maintain safe premises, and courts recognize different duty levels based on visitor status. An invitee-like a tenant or their guest-receives the highest duty of care, meaning you must inspect regularly, repair known hazards, and warn of nonobvious risks. A slip-and-fall on a cracked sidewalk or stairs you failed to maintain can trigger a premises liability claim that costs far more than your policy deductible. Most Connecticut landlords carry $500,000 in liability coverage per incident, with aggregate limits up to $2,000,000 for one- to four-unit properties. If your tenant’s guest breaks a leg on your back deck, medical expenses alone can exceed $100,000, and pain-and-suffering awards add substantially more. Consider an umbrella policy for additional protection if you own multiple properties or rent frequently.

Income Protection During Repairs

Loss of rental income coverage reimburses the rent you lose when a covered peril makes a unit unlivable. A kitchen fire that requires three months of repairs means three months without income-unless you have this coverage. Connecticut insurers typically cap reimbursement at 12 months or a specific dollar amount, so calculate your exposure as monthly rent multiplied by your expected repair timeline. If you collect $2,000 monthly and repairs typically take two months, you need at least $4,000 in loss-of-income coverage. This protection does not cover tenant unemployment or financial hardship; it covers only your lost rent due to physical damage.

Additional Protections for Connecticut Properties

Non-occupied dwelling coverage protects your property during vacancies beyond 30 days, a critical gap since standard policies limit coverage during extended absences. Building code coverage pays the extra cost to bring repairs up to current codes, a benefit older Connecticut properties especially value when foundation or electrical work becomes necessary during repairs. These endorsements fill gaps that leave many landlords underprotected. The next section examines why standard homeowners policies fail rental property owners and what specific gaps you must address.

Common Gaps in Standard Homeowners Policies

Your homeowners insurance policy contains explicit language excluding rental income and tenant-related liability. This is not a gray area or something an agent might overlook-it appears directly in your policy documents. Landlord insurance is designed for rental properties, while homeowners insurance is designed to cover the property you live in. When you rent out your Connecticut home, your insurer treats it as a business activity that falls outside the policy’s scope. Many landlords discover this gap only after filing a claim and watching their insurer deny coverage for lost rent or a tenant’s injury. Yet those premiums still buy zero protection for rental scenarios. You cannot patch this problem with a phone call to your current agent; you need a separate landlord policy that specifically covers what homeowners insurance excludes.

Why Homeowners Insurance Falls Short for Rental Properties

Standard homeowners policies exclude rental activities by design. Your insurer underwrites the policy based on owner-occupied risk, not the higher exposure that comes with tenants and their guests occupying your property year-round. When you introduce rental income, you introduce liability scenarios-injuries, property damage caused by tenants, loss of income-that fall completely outside your homeowners coverage. An independent agent can show you exactly where your current policy stops protecting you and where landlord coverage begins. This clarity prevents costly surprises when you file a claim and discover your insurer will not pay.

Vacant Property Exclusions and Limitations

Vacant property clauses create another critical blind spot. Most Connecticut insurers limit coverage during extended vacancies to 30 or 60 days, meaning a property sitting empty while you find tenants or complete renovations receives minimal protection. If a pipe bursts during a three-month vacancy, your standard homeowners policy may deny the claim entirely. You must notify your insurer about vacancies and often add a non-occupied dwelling endorsement to maintain coverage beyond those initial weeks. Properties left unoccupied for longer periods face serious coverage restrictions that landlord policies address directly.

Liability Limits That Leave You Exposed

Liability limits in homeowners policies fall dangerously short for rental properties. A typical homeowners policy offers $300,000 in liability coverage, which sounds adequate until a guest suffers a serious injury on your property. A slip-and-fall resulting in spinal surgery can easily exceed $200,000 in medical costs alone, with pain-and-suffering awards doubling or tripling that amount. Connecticut courts recognize landlords’ legal duty to maintain safe premises, and juries award substantial damages when that duty is breached. Your $300,000 limit evaporates quickly, leaving you personally liable for amounts above that threshold. Landlord policies start at $500,000 in liability per incident for good reason-rental properties face higher exposure because strangers occupy the space year-round. An independent agent comparing multiple carriers can identify which Connecticut insurers offer the coverage depth you actually need, rather than leaving you exposed to claims that standard homeowners policies will not pay.

The gaps between homeowners and landlord coverage are substantial enough that choosing the right policy becomes your next critical decision. Understanding what each type of landlord policy offers-and how to match those offerings to your specific property and tenant situation-determines whether you truly protect your investment or simply hope nothing goes wrong.

How to Choose the Right Landlord Insurance Policy

Assess Your Property’s True Replacement Value

Calculate what your property would cost to rebuild today, not what you paid for it or what your mortgage lender says it’s worth. Connecticut construction costs have climbed steadily, and underestimating replacement value guarantees a shortfall when you file a claim. A contractor can provide a rebuild estimate for $300–$500, money well spent before you commit to coverage limits. Your dwelling coverage should reflect current market values, or you will face a significant gap after a loss.

Calculate Loss-of-Income Coverage Needs

Determine your monthly rental income and multiply it by the number of months repairs typically require in your area. If your three-bedroom rental collects $2,200 monthly and major repairs average 90 days, you need at least $6,600 in loss-of-income coverage. This calculation prevents you from underinsuring your most predictable revenue stream. Standard policies cap reimbursement at 12 months or a specific dollar amount, so match your coverage to realistic repair timelines.

Account for Coastal and Flood Risks

Coastal properties face higher wind deductibles-often 2% of dwelling coverage-because hurricane exposure along Long Island Sound drives up claims. A $250,000 dwelling limit means a $5,000 wind deductible before your insurer pays anything, so factor this into your financial planning. Properties within FEMA flood zones must carry flood insurance through the National Flood Insurance Program or private carriers. Non-occupied dwelling coverage becomes essential if your property sits vacant for more than 30 days during tenant transitions or renovations-standard policies restrict claims during extended absences, leaving you unprotected when pipes freeze or theft occurs.

Compare Carriers and Customize Coverage

An independent agent comparing multiple carriers reveals dramatic differences in pricing and coverage breadth that shopping online cannot match. Travelers, Progressive, Stillwater, Safeco, and Foremost all serve Connecticut landlords, but their underwriting standards and endorsement options vary significantly. Some carriers exclude wind coverage entirely in high-risk zones and force you into Connecticut’s FAIR Plan, while others offer competitive rates with reasonable deductibles. An experienced independent agent knows which carriers offer the best rates for your specific situation-a coastal two-unit property faces completely different pricing than an inland single-family rental.

Leverage Discounts and Endorsements

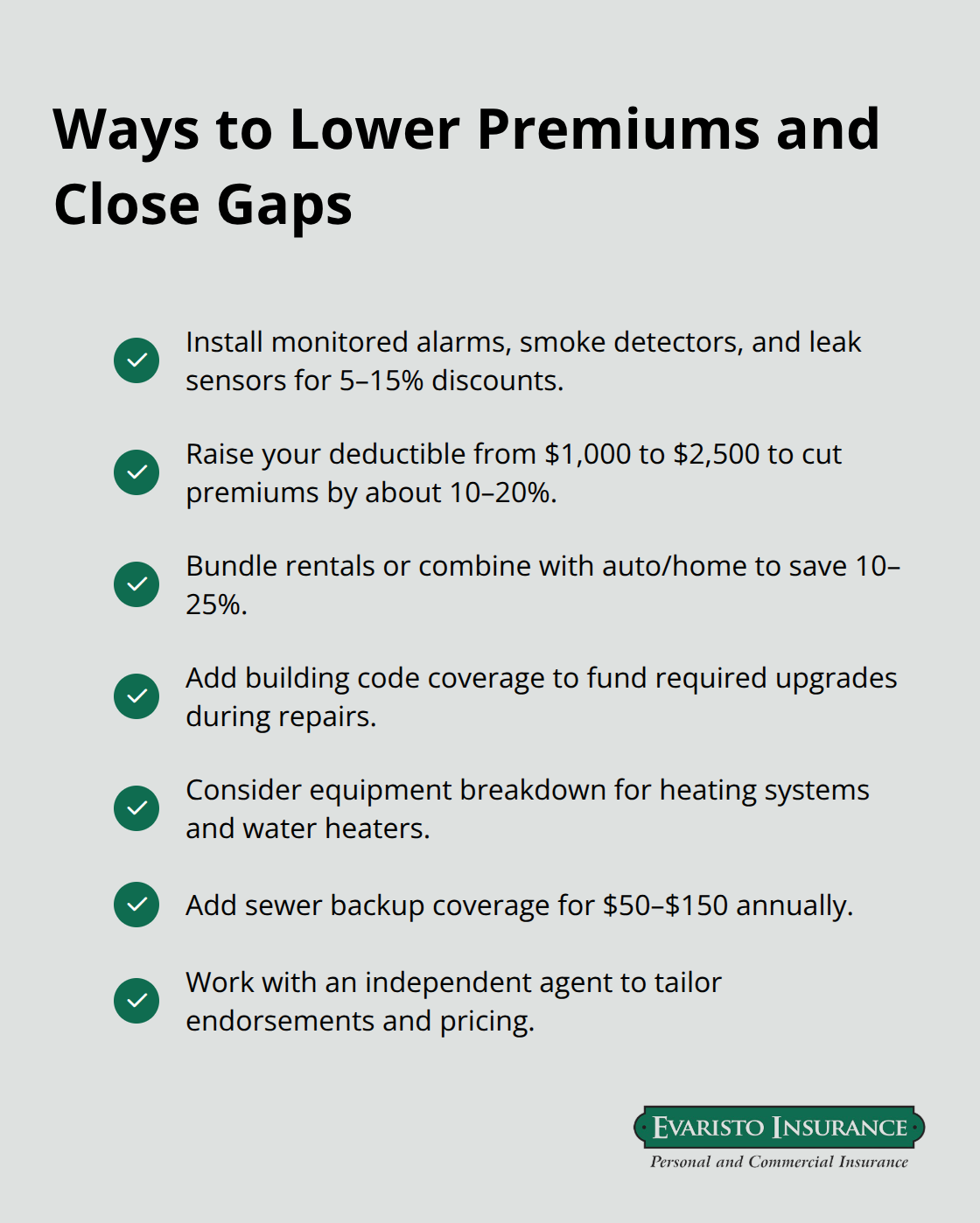

Adding security features like monitored alarms, smoke detectors, and water-leak sensors typically generates 5–15% safety discounts across most carriers. Raising your deductible from $1,000 to $2,500 cuts premiums by roughly 10–20%, a meaningful reduction if cash flow matters.

Bundling multiple rental properties or linking landlord coverage with your personal auto or homeowners policy yields 10–25% in savings. Your agent also explains endorsements worth considering: building code coverage for older properties needing upgrades during repairs, equipment breakdown protection for heating systems and water heaters, and sewer backup coverage for $50–$150 annually. This personalized approach prevents you from overpaying for coverage you don’t need while closing gaps that leave you exposed.

Final Thoughts

Protecting your Connecticut rental property requires more than hoping your homeowners policy covers tenant-related claims. You now understand what landlord insurance actually covers, where standard policies fail, and how to match coverage limits to your specific property and income needs. The three core protections-dwelling coverage at replacement cost, liability limits of at least $500,000 per incident, and loss-of-income reimbursement calculated from your actual monthly rent-form the foundation of solid rental property coverage.

Coastal properties demand special attention to wind deductibles and flood insurance through the National Flood Insurance Program, while older buildings benefit from building code endorsements that cover upgrade costs during repairs. Security discounts, higher deductibles, and bundled policies can reduce your premiums by 10–25%, making comprehensive protection affordable without sacrificing coverage depth. Connecticut landlords face distinct risks from hurricane exposure, aging building stock, and seasonal vacancy periods that require customized solutions, not generic policies.

An independent agent compares multiple carriers rather than pushing a single insurer’s products and identifies which ones offer competitive rates for your situation. We at Evaristo Insurance serve Connecticut landlords with rental property coverage tailored to your specific needs, competitive pricing, and hands-on advocacy when claims arise. Contact us today to review your current coverage and build the protection your rental investment actually deserves.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.