Connecticut Homeowners Policy Guide: Choosing the Right Plan

Homeowners insurance in Connecticut isn’t one-size-fits-all. Your home’s value, location, and personal circumstances all shape what coverage you actually need.

At Evaristo Insurance, we’ve helped countless Connecticut homeowners navigate policy options and avoid costly gaps. This guide walks you through the coverage types available, how to evaluate your specific needs, and what protection gaps to watch for.

What Your Connecticut Homeowners Policy Actually Covers

Connecticut homeowners policies typically include six core coverage sections, but understanding what each one protects-and what it doesn’t-separates smart buyers from those who face gaps when they need help most. Coverage A protects your home’s structure itself, including walls, roofing, and built-in systems. Coverage B extends that protection to detached structures like garages, sheds, and fences, though it’s usually limited to 10 percent of your dwelling coverage amount. Coverage C covers personal property inside your home and belongings damaged or stolen outside it, typically set at 50 to 70 percent of your dwelling coverage. Coverage D reimburses temporary housing and meal costs if your home becomes uninhabitable after a covered loss-a protection many homeowners underestimate. Coverage E provides liability protection if someone is injured on your property or you damage someone else’s property and you’re legally responsible. Coverage F covers medical expenses for injuries on your property regardless of fault, protecting you from lawsuits over accidents you didn’t cause.

Winter Weather Damage in Connecticut Requires Specific Attention

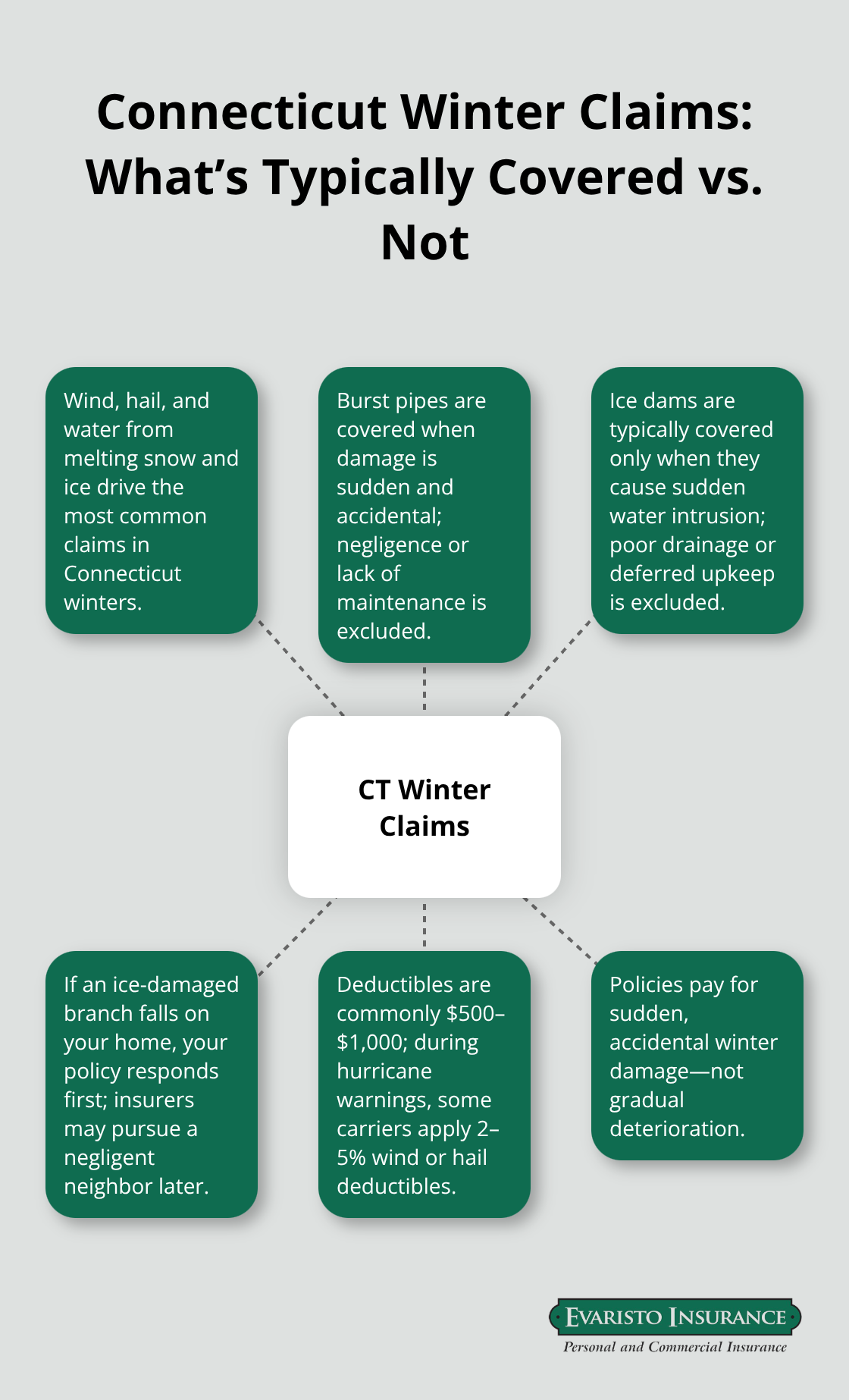

Connecticut’s harsh winters create unique claim patterns. Wind, hail, and water damage from melting snow and ice account for the most common homeowners insurance claims in Connecticut. Burst pipes from freezing temperatures receive coverage if the damage is sudden and accidental, not from negligence or lack of maintenance. Ice dam damage is typically covered, but only if it results in sudden water intrusion-not from poor drainage or deferred upkeep.

A tree branch damaged by ice and falling onto your home receives coverage; however, damage from a neighbor’s tree requires your own policy to pay first, with your insurer potentially pursuing the negligent neighbor for recovery. Connecticut policies cover sudden, accidental winter damage, not gradual deterioration. Most policies include standard deductibles of $500 or $1,000 for winter losses, though some carriers offer wind or hail-specific deductibles during hurricane season, typically 2 to 5 percent of your dwelling’s value when an official hurricane warning is issued.

High-Value Items and Specialty Coverage Gaps

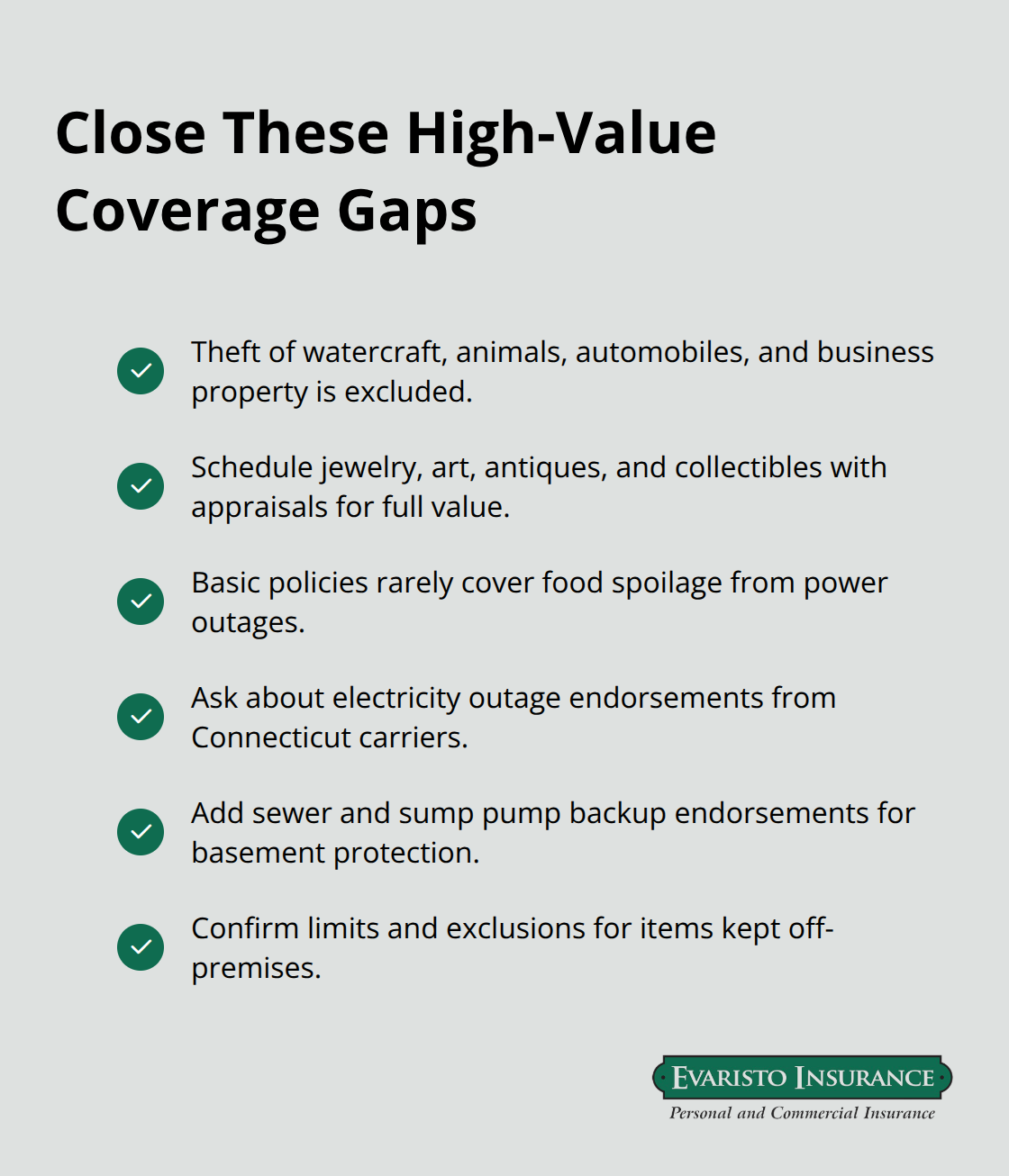

Standard homeowners policies exclude theft of watercraft, animals, automobiles, and business property, meaning these items require separate policies or endorsements. Antique furniture, jewelry, art, or collectibles receive only actual cash value settlements unless you obtain updated appraisals and list insured values directly in your policy. Food spoilage from power outages typically lacks coverage under basic policies, though some Connecticut carriers now offer limited electricity outage endorsements worth discussing with your agent.

Sewer backups and sump pump failures are almost always excluded unless you add a specific endorsement, which matters if your home has a basement or sits in a flood-prone area. Your standard policy has boundaries, and knowing them prevents surprises when you file a claim.

Understanding What Triggers Coverage vs. Exclusions

The distinction between covered and excluded losses often hinges on how the damage occurs. Sudden, accidental damage typically qualifies for payment, while gradual wear or negligence does not. Your policy language determines the exact boundaries-what one carrier covers, another may exclude. This is where comparing quotes from multiple carriers becomes essential, as different insurers weigh risk factors differently and offer varying endorsements. A local Connecticut agent can help you identify which gaps matter most for your specific situation and which endorsements make financial sense for your home and family.

Picking the Right Coverage Limits for Your Connecticut Home

Calculate Replacement Cost, Not Market Value

The gap between underinsurance and overinsurance costs Connecticut homeowners thousands annually. Most families either buy too little coverage and face financial exposure after a loss, or they purchase excessive limits they’ll never need. Your home’s sale price tells you nothing about reconstruction expenses. If you own a 1,500-square-foot home in Hartford valued at $250,000, rebuilding might cost $180,000 to $220,000 depending on current labor and material prices. Construction costs have risen significantly, and the state averages roughly $1,700 annually for $300,000 in dwelling coverage. However, this figure masks enormous regional variation. Coastal towns like Old Saybrook and New Haven run $2,000 to $2,189 per year for the same coverage, while inland areas like Staffordville and Scotland cost around $1,320 to $1,338 annually. The difference stems from exposure to wind, water, and winter damage. Request a professional replacement cost estimate from your contractor or ask your agent to use industry tools that factor in your specific home’s age, materials, square footage, and local building codes. This number becomes your Coverage A baseline.

Set Personal Property and Liability Limits to Match Your Assets

Next, set personal property coverage at 50 to 70 percent of dwelling coverage, as your policy typically limits it there, but verify this matches your actual belongings inventory. Liability coverage should reflect your net worth and assets at risk. Connecticut homeowners with significant equity or retirement accounts should carry at least $300,000 in liability protection, ideally $500,000 or higher. A single lawsuit from a serious injury on your property can exceed $1 million in damages, and your policy serves as your only shield against catastrophic financial loss.

Compare Quotes Across Multiple Carriers

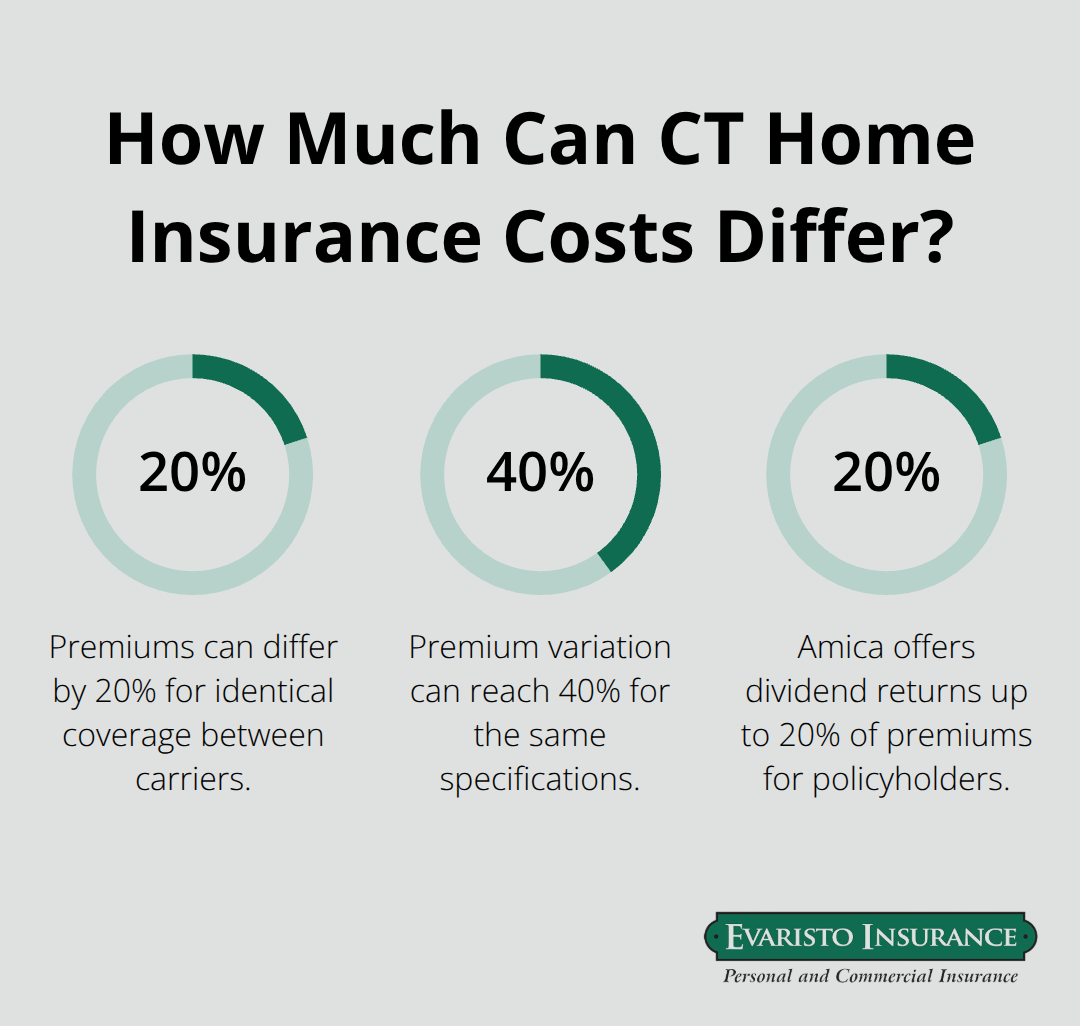

Comparing quotes reveals how much underwriting standards differ between carriers. Request identical coverage specifications from at least three to five insurers using the same dwelling amount, liability limit, and deductible. You’ll see premiums vary by 20 to 40 percent for identical protection because each carrier weights roof age, location, claims history, and credit score differently. USAA offers the lowest Connecticut premiums for eligible military families and veterans, while Amica provides strong value with dividend returns reaching up to 20 percent of premiums for policyholders.

State Farm dominates through local agent networks across Connecticut, and Travelers delivers broad optional endorsements for water backup and identity theft protection.

Identify Discounts and Adjust Your Deductible

When you receive quotes, ask each carrier which discounts apply to your situation-claim-free discounts, multi-policy bundling, protective device installations, and roof mitigation upgrades can reduce premiums by 10 to 25 percent. Raising your deductible from $500 to $1,000 typically lowers your annual premium by $100 to $150, a smart move if you have emergency savings to cover a larger out-of-pocket loss. Don’t chase the lowest price alone; verify the insurer’s financial strength through AM Best ratings and check customer complaint ratios at the National Association of Insurance Commissioners. A $200 annual savings means nothing if claims handling takes months or disputes arise.

Schedule Quotes Early for Older Homes and Flood-Prone Areas

Schedule quotes early, especially if your roof is older than 15 years or you live in a flood-prone area, since some carriers restrict coverage or impose higher premiums based on these factors. Once you’ve selected coverage limits that protect your assets without overpaying, the next step involves identifying the specific gaps that standard policies leave unprotected-and which endorsements actually matter for your Connecticut home.

What Your Connecticut Policy Won’t Cover

Flood Damage Requires Separate Protection

Flood damage tops the list of protection gaps that catch Connecticut homeowners off guard. Your standard homeowners policy excludes all flood losses, period-whether from heavy rain, coastal storm surge, or overflowing rivers. Flood Insurance Program through FEMA covers this exposure, but you must purchase it separately. If you own a home, condo or business in a high-risk flood zone and have a government-backed mortgage, your lender will require it. Check your flood risk at FloodSmart.gov using your address; coastal properties in towns like Clinton, Westbrook, and Niantic face elevated premiums because these areas sit in flood zones where standard coverage fails. If you live in a flood-prone area and skip this endorsement, a single storm surge or heavy rainfall event can cost $50,000 to $100,000 in uninsured losses.

High-Value Items Need Scheduled Coverage

Jewelry, art, antiques, and collectibles receive only actual cash value unless you schedule them separately with updated appraisals; a $5,000 engagement ring might settle for $2,500 under actual cash value when replacement costs $6,000 today. Watercraft, animals, and business property require separate policies entirely-your homeowners coverage won’t touch them. Sewer backups and sump pump failures sit in a grey area; most standard policies exclude these unless you add a specific endorsement, which costs $50 to $150 annually but prevents $15,000 to $30,000 in basement damage claims.

Weather and Utility Gaps in Connecticut Coverage

Earthquake damage falls outside standard Connecticut policies, though this risk matters far less here than in California-Connecticut experiences minor seismic activity, making earthquake coverage a low priority for most homeowners. Food spoilage from power outages typically lacks coverage under basic policies, though some Connecticut carriers now offer limited electricity outage endorsements. Winter weather creates additional exposure; ice dams, burst pipes, and roof damage from heavy snow demand attention to your policy’s specific language around sudden versus gradual damage.

Map Your Assets and Close Real Gaps

The practical move involves mapping your actual assets and exposure, then filling the gaps that matter. Request detailed appraisals for high-value items, ask your agent which endorsements apply to your home’s specific risks, and budget $200 to $400 annually for endorsements that close real gaps rather than hypothetical ones. Standard policies protect the typical home adequately, but Connecticut properties face unique flood and winter weather risks that demand intentional gap coverage.

Final Thoughts

Choosing the right Connecticut homeowners policy guide requires you to understand what your coverage protects, calculate limits that match your home’s replacement cost and your assets, and identify the specific gaps that matter for your situation. Standard policies cover dwelling structure, personal property, liability, and additional living expenses, but they exclude flood damage, high-value items without scheduling, and certain weather-related losses unless you add endorsements. The difference between adequate protection and financial exposure often hinges on decisions you make during the shopping process, not after a loss occurs.

Your Connecticut home’s unique characteristics demand a tailored approach. Coastal properties face different risks than inland homes, older roofs attract underwriter scrutiny, and basements in flood-prone areas need sewer backup coverage. Comparing quotes from multiple carriers reveals how dramatically premiums and coverage options vary for identical protection levels, because each insurer weights risk factors differently based on their underwriting philosophy. A local Connecticut agent transforms this process from overwhelming to manageable by identifying which endorsements actually protect your home and which ones waste money.

At Evaristo Insurance, we compare multiple top carriers to deliver tailored protection and competitive pricing rather than pushing a single company’s products. Our local offices in Ellington and West Hartford mean you work with people who understand Connecticut’s insurance landscape and your community’s specific risks. Start by gathering your home’s replacement cost estimate, documenting your personal property value, and identifying your flood risk at FloodSmart.gov, then contact Evaristo Insurance to discuss your Connecticut homeowners policy options and secure protection that matches your needs.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.

Leave a Reply

Want to join the discussion?Feel free to contribute!